Sidley Austin Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

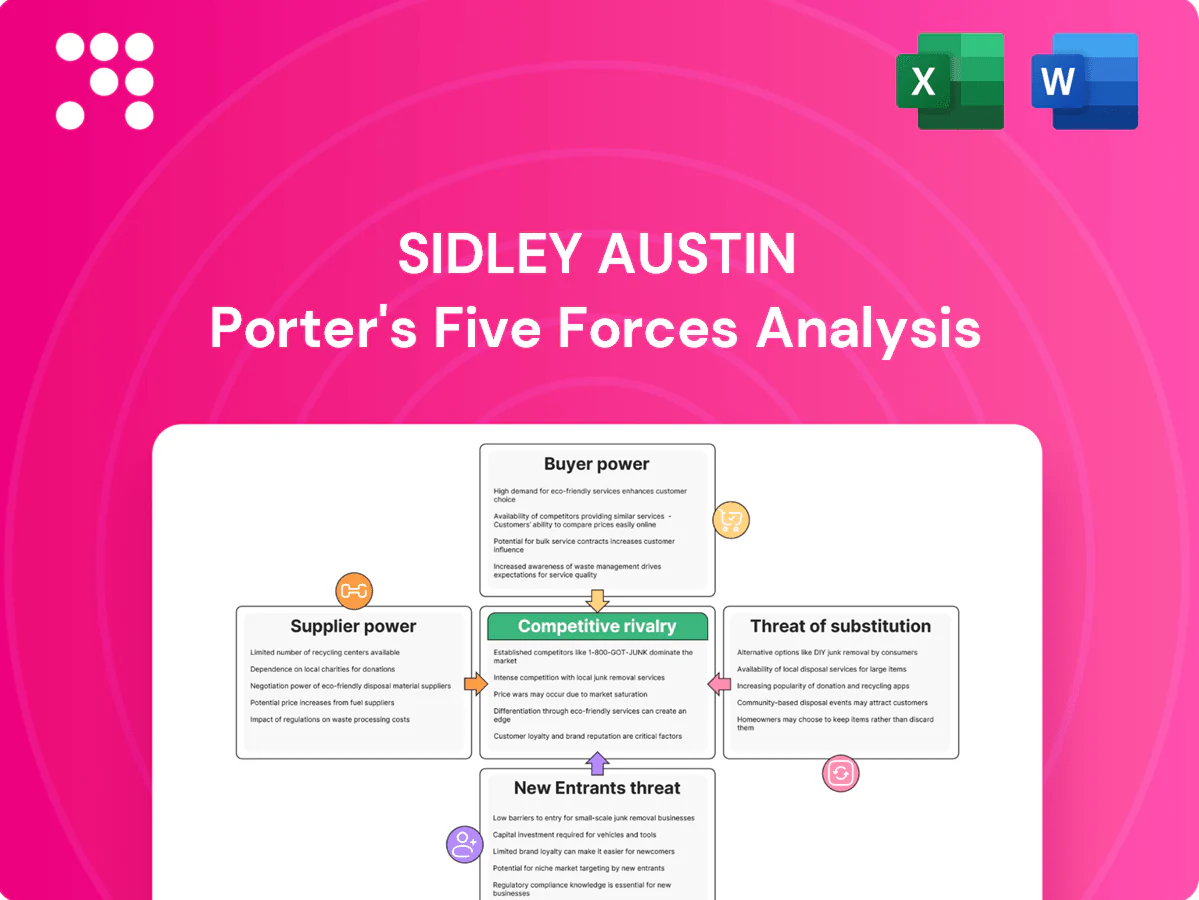

Sidley Austin's Porter’s Five Forces snapshot highlights competitive intensity across supplier and buyer power, barriers to entry, substitute threats, and rivalry among peers, revealing strategic pressure points and growth levers. This brief teases key insights; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Elite legal talent dependence

Star partners and specialized associates are primary inputs and command premium compensation: top‑firm starting salaries hit $215,000 in 2024, while rainmakers in antitrust, PE and life sciences command higher partner premiums. Scarcity in those practices elevates leverage and retention/lateral competition raises switching costs. Wage inflation and escalating bonus cycles have pressured Am Law margins (average PEP ~ $1.7M in 2023), compressing margins.

Technology and AI vendors

Core systems (DMS, eDiscovery, AI research, cybersecurity) are concentrated among a few providers—Relativity, Microsoft, iManage and OpenText dominate market deployments—driving pricing power toward established platforms; multi-year contracts (often 3–5 years) and integration complexity raise vendor stickiness, while strict data-security and compliance requirements materially limit rapid switching and preserve supplier leverage in 2024.

Legal research and data providers

Thomson Reuters (Westlaw) and RELX (Lexis) function as a duopoly, together commanding roughly 70–80% of the US legal research market, creating dependency for firms like Sidley Austin. Bundled packages—research, analytics, drafting tools—increase lock‑in and make migration costly; vendors report annual price escalators commonly in the mid single digits and tiered usage fees that can raise total spend by 10–25%. Alternatives exist (Fastcase, Casetext, Bloomberg Law) but switching risks workflow disruption and variable quality.

Real estate and premium locations

Tier-1 offices in global financial centres remain costly and scarce, with long-term leases typically 5–15 years constraining relocation despite hybrid work; landlords of trophy assets therefore keep strong leverage on rent, break clauses and incentives. High fit-out and branding costs, commonly $100–$400 per sq ft in 2024, raise switching friction and lock tenants into prime locations.

- Limited supply: tier-1 scarcity

- Lease length: 5–15 years

- Landlord leverage: trophy asset terms

- Fit-out cost: $100–$400/sq ft (2024)

Referral and expert networks

Referral and expert networks (specialist experts, local counsel, litigation support firms) act as niche suppliers to Sidley Austin; limited substitutes in complex jurisdictions or technical areas elevate their bargaining power. High-stakes, case-critical deadlines temper Sidley’s leverage and can push rates higher, while relationship capital and repeat engagements partially mitigate pricing pressure; expert-network industry revenue ~1.5bn (2024 est.).

- Specialists: niche, high value

- Substitutes: limited in complex jurisdictions

- Deadlines: reduce bargaining leverage

- Relationships: lower price pressure

- Data: 1.35M US lawyers (ABA), expert networks ~$1.5B (2024 est.)

Suppliers drive lock-in: talent premiums and research concentration 70-80%

Suppliers exert material leverage: talent premiums (top‑firm starts $215,000 in 2024; AmLaw avg PEP ~$1.7M 2023) and niche experts raise costs and switching friction. Core tech and research duopolies (Westlaw/Lexis ~70–80% share) plus 3–5 year contracts boost vendor stickiness. Tier‑1 real estate scarcity and fit‑out costs ($100–$400/sq ft 2024) further constrain mobility.

| Supplier | Key metric |

|---|---|

| Talent | Top start $215k (2024); PEP ~$1.7M (2023) |

| Research | Westlaw/Lexis 70–80% market share |

| Tech/leases | Contracts 3–5 yrs; fit‑out $100–$400/sq ft (2024) |

| Experts | Expert networks ~$1.5B (2024) |

What is included in the product

Uncovers key drivers of competition, client influence, and entry risks for Sidley Austin, detailing bargaining power of clients and suppliers, threat of substitutes, and rivalry among elite law firms. Highlights disruptive factors, regulatory shifts, and strategic defenses that protect its market position.

A concise one-sheet Porter's Five Forces for Sidley Austin highlighting competitive pressures and mitigation strategies—easy to drop into decks, update with new market or regulatory data, and instantly communicate strategic risk to partners and boards.

Customers Bargaining Power

Institutional client consolidation

Institutional client consolidation sees many Fortune 500 corporates centralize legal panels in 2024, boosting buyer negotiating power. Competitive RFPs and volume discounts increasingly pressure hourly and alternative rates. Cross-border mandates give buyers leverage on staffing and jurisdictional pricing, though multi-year relationships still allow firms to command premium fees.

Price sensitivity and AFAs

Clients pushed AFAs in 2024—about 54% of in-house teams sought fixed or blended fees, constraining rate expansion and making matter-level economics transparent. Risk-sharing and success fees have increased margin variability, transferring upside and downside to firms like Sidley Austin, which reported roughly $1.6B revenue in 2024. Procurement professionalization—about 70% of large corporates using formal legal procurement—intensifies fee negotiation and budget discipline.

Switching and multi-firm strategies

Clients routinely split matters across several firms to benchmark performance, with GC panels in 2024 commonly ranging from 3 to 6 firms. Low switching costs for commoditized work—e.g., routine transactions or document review—amplify buyer power and drive price competition. High‑stakes litigation or M&A carry higher switching frictions but still prompt bake‑offs; conflicts of interest often compel clients to diversify counsel.

In-house capability growth

Expanded corporate legal teams retain more work internally as sophisticated GCs unbundle matters and dictate staffing, pushing Sidley to handle only complex or peak-load work; standardized services face growing rate pressure and alternative delivery models. External counsel is increasingly engaged for high-value, specialized matters while commodity work moves in-house.

Regulatory and cross-border complexity

Regulatory and cross-border complexity gives clients scope leverage as multi-jurisdiction matters require coordinated coverage and single-invoice solutions; the global legal services market surpassed $700 billion in 2024, driving demand for seamless provider networks. Coordination burdens shift to the firm, justifying volume-based discounts, though deep niche expertise can reduce buyer bargaining in specialized areas.

- Multi-jurisdiction scope

- Single-invoice demand

- Firm bears coordination costs

- Volume discounts justified

- Niche expertise lowers buyer power

Procurement, AFAs and 3-6 firm GC panels lift buyer leverage across global legal market

Institutional consolidation and procurement professionalization (≈70% of large corporates) raised buyer leverage in 2024, with GC panels commonly 3–6 firms. About 54% of in-house teams sought AFAs, pressuring rate growth and matter-level margins; Sidley reported ~$1.6B revenue in 2024. Cross-border scope (global legal market >$700B) shifts coordination costs to firms but niche expertise reduces buyer power on specialized mandates.

| Metric | 2024 |

|---|---|

| AFAs requested | 54% |

| Procurement use | ≈70% |

| GC panel size | 3–6 firms |

| Sidley revenue | ≈$1.6B |

| Global market | >$700B |

Same Document Delivered

Sidley Austin Porter's Five Forces Analysis

This preview shows the exact Sidley Austin Porter's Five Forces analysis you'll receive after purchase—no samples or placeholders. It is the full, professionally formatted document, ready for immediate download and use. What you see here is the deliverable you’ll get instantly upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Sidley Austin's Porter’s Five Forces snapshot highlights competitive intensity across supplier and buyer power, barriers to entry, substitute threats, and rivalry among peers, revealing strategic pressure points and growth levers. This brief teases key insights; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Elite legal talent dependence

Star partners and specialized associates are primary inputs and command premium compensation: top‑firm starting salaries hit $215,000 in 2024, while rainmakers in antitrust, PE and life sciences command higher partner premiums. Scarcity in those practices elevates leverage and retention/lateral competition raises switching costs. Wage inflation and escalating bonus cycles have pressured Am Law margins (average PEP ~ $1.7M in 2023), compressing margins.

Technology and AI vendors

Core systems (DMS, eDiscovery, AI research, cybersecurity) are concentrated among a few providers—Relativity, Microsoft, iManage and OpenText dominate market deployments—driving pricing power toward established platforms; multi-year contracts (often 3–5 years) and integration complexity raise vendor stickiness, while strict data-security and compliance requirements materially limit rapid switching and preserve supplier leverage in 2024.

Legal research and data providers

Thomson Reuters (Westlaw) and RELX (Lexis) function as a duopoly, together commanding roughly 70–80% of the US legal research market, creating dependency for firms like Sidley Austin. Bundled packages—research, analytics, drafting tools—increase lock‑in and make migration costly; vendors report annual price escalators commonly in the mid single digits and tiered usage fees that can raise total spend by 10–25%. Alternatives exist (Fastcase, Casetext, Bloomberg Law) but switching risks workflow disruption and variable quality.

Real estate and premium locations

Tier-1 offices in global financial centres remain costly and scarce, with long-term leases typically 5–15 years constraining relocation despite hybrid work; landlords of trophy assets therefore keep strong leverage on rent, break clauses and incentives. High fit-out and branding costs, commonly $100–$400 per sq ft in 2024, raise switching friction and lock tenants into prime locations.

- Limited supply: tier-1 scarcity

- Lease length: 5–15 years

- Landlord leverage: trophy asset terms

- Fit-out cost: $100–$400/sq ft (2024)

Referral and expert networks

Referral and expert networks (specialist experts, local counsel, litigation support firms) act as niche suppliers to Sidley Austin; limited substitutes in complex jurisdictions or technical areas elevate their bargaining power. High-stakes, case-critical deadlines temper Sidley’s leverage and can push rates higher, while relationship capital and repeat engagements partially mitigate pricing pressure; expert-network industry revenue ~1.5bn (2024 est.).

- Specialists: niche, high value

- Substitutes: limited in complex jurisdictions

- Deadlines: reduce bargaining leverage

- Relationships: lower price pressure

- Data: 1.35M US lawyers (ABA), expert networks ~$1.5B (2024 est.)

Suppliers drive lock-in: talent premiums and research concentration 70-80%

Suppliers exert material leverage: talent premiums (top‑firm starts $215,000 in 2024; AmLaw avg PEP ~$1.7M 2023) and niche experts raise costs and switching friction. Core tech and research duopolies (Westlaw/Lexis ~70–80% share) plus 3–5 year contracts boost vendor stickiness. Tier‑1 real estate scarcity and fit‑out costs ($100–$400/sq ft 2024) further constrain mobility.

| Supplier | Key metric |

|---|---|

| Talent | Top start $215k (2024); PEP ~$1.7M (2023) |

| Research | Westlaw/Lexis 70–80% market share |

| Tech/leases | Contracts 3–5 yrs; fit‑out $100–$400/sq ft (2024) |

| Experts | Expert networks ~$1.5B (2024) |

What is included in the product

Uncovers key drivers of competition, client influence, and entry risks for Sidley Austin, detailing bargaining power of clients and suppliers, threat of substitutes, and rivalry among elite law firms. Highlights disruptive factors, regulatory shifts, and strategic defenses that protect its market position.

A concise one-sheet Porter's Five Forces for Sidley Austin highlighting competitive pressures and mitigation strategies—easy to drop into decks, update with new market or regulatory data, and instantly communicate strategic risk to partners and boards.

Customers Bargaining Power

Institutional client consolidation

Institutional client consolidation sees many Fortune 500 corporates centralize legal panels in 2024, boosting buyer negotiating power. Competitive RFPs and volume discounts increasingly pressure hourly and alternative rates. Cross-border mandates give buyers leverage on staffing and jurisdictional pricing, though multi-year relationships still allow firms to command premium fees.

Price sensitivity and AFAs

Clients pushed AFAs in 2024—about 54% of in-house teams sought fixed or blended fees, constraining rate expansion and making matter-level economics transparent. Risk-sharing and success fees have increased margin variability, transferring upside and downside to firms like Sidley Austin, which reported roughly $1.6B revenue in 2024. Procurement professionalization—about 70% of large corporates using formal legal procurement—intensifies fee negotiation and budget discipline.

Switching and multi-firm strategies

Clients routinely split matters across several firms to benchmark performance, with GC panels in 2024 commonly ranging from 3 to 6 firms. Low switching costs for commoditized work—e.g., routine transactions or document review—amplify buyer power and drive price competition. High‑stakes litigation or M&A carry higher switching frictions but still prompt bake‑offs; conflicts of interest often compel clients to diversify counsel.

In-house capability growth

Expanded corporate legal teams retain more work internally as sophisticated GCs unbundle matters and dictate staffing, pushing Sidley to handle only complex or peak-load work; standardized services face growing rate pressure and alternative delivery models. External counsel is increasingly engaged for high-value, specialized matters while commodity work moves in-house.

Regulatory and cross-border complexity

Regulatory and cross-border complexity gives clients scope leverage as multi-jurisdiction matters require coordinated coverage and single-invoice solutions; the global legal services market surpassed $700 billion in 2024, driving demand for seamless provider networks. Coordination burdens shift to the firm, justifying volume-based discounts, though deep niche expertise can reduce buyer bargaining in specialized areas.

- Multi-jurisdiction scope

- Single-invoice demand

- Firm bears coordination costs

- Volume discounts justified

- Niche expertise lowers buyer power

Procurement, AFAs and 3-6 firm GC panels lift buyer leverage across global legal market

Institutional consolidation and procurement professionalization (≈70% of large corporates) raised buyer leverage in 2024, with GC panels commonly 3–6 firms. About 54% of in-house teams sought AFAs, pressuring rate growth and matter-level margins; Sidley reported ~$1.6B revenue in 2024. Cross-border scope (global legal market >$700B) shifts coordination costs to firms but niche expertise reduces buyer power on specialized mandates.

| Metric | 2024 |

|---|---|

| AFAs requested | 54% |

| Procurement use | ≈70% |

| GC panel size | 3–6 firms |

| Sidley revenue | ≈$1.6B |

| Global market | >$700B |

Same Document Delivered

Sidley Austin Porter's Five Forces Analysis

This preview shows the exact Sidley Austin Porter's Five Forces analysis you'll receive after purchase—no samples or placeholders. It is the full, professionally formatted document, ready for immediate download and use. What you see here is the deliverable you’ll get instantly upon payment.

Description

Go Beyond the Preview—Access the Full Strategic Report

Sidley Austin's Porter’s Five Forces snapshot highlights competitive intensity across supplier and buyer power, barriers to entry, substitute threats, and rivalry among peers, revealing strategic pressure points and growth levers. This brief teases key insights; unlock the full Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Elite legal talent dependence

Star partners and specialized associates are primary inputs and command premium compensation: top‑firm starting salaries hit $215,000 in 2024, while rainmakers in antitrust, PE and life sciences command higher partner premiums. Scarcity in those practices elevates leverage and retention/lateral competition raises switching costs. Wage inflation and escalating bonus cycles have pressured Am Law margins (average PEP ~ $1.7M in 2023), compressing margins.

Technology and AI vendors

Core systems (DMS, eDiscovery, AI research, cybersecurity) are concentrated among a few providers—Relativity, Microsoft, iManage and OpenText dominate market deployments—driving pricing power toward established platforms; multi-year contracts (often 3–5 years) and integration complexity raise vendor stickiness, while strict data-security and compliance requirements materially limit rapid switching and preserve supplier leverage in 2024.

Legal research and data providers

Thomson Reuters (Westlaw) and RELX (Lexis) function as a duopoly, together commanding roughly 70–80% of the US legal research market, creating dependency for firms like Sidley Austin. Bundled packages—research, analytics, drafting tools—increase lock‑in and make migration costly; vendors report annual price escalators commonly in the mid single digits and tiered usage fees that can raise total spend by 10–25%. Alternatives exist (Fastcase, Casetext, Bloomberg Law) but switching risks workflow disruption and variable quality.

Real estate and premium locations

Tier-1 offices in global financial centres remain costly and scarce, with long-term leases typically 5–15 years constraining relocation despite hybrid work; landlords of trophy assets therefore keep strong leverage on rent, break clauses and incentives. High fit-out and branding costs, commonly $100–$400 per sq ft in 2024, raise switching friction and lock tenants into prime locations.

- Limited supply: tier-1 scarcity

- Lease length: 5–15 years

- Landlord leverage: trophy asset terms

- Fit-out cost: $100–$400/sq ft (2024)

Referral and expert networks

Referral and expert networks (specialist experts, local counsel, litigation support firms) act as niche suppliers to Sidley Austin; limited substitutes in complex jurisdictions or technical areas elevate their bargaining power. High-stakes, case-critical deadlines temper Sidley’s leverage and can push rates higher, while relationship capital and repeat engagements partially mitigate pricing pressure; expert-network industry revenue ~1.5bn (2024 est.).

- Specialists: niche, high value

- Substitutes: limited in complex jurisdictions

- Deadlines: reduce bargaining leverage

- Relationships: lower price pressure

- Data: 1.35M US lawyers (ABA), expert networks ~$1.5B (2024 est.)

Suppliers drive lock-in: talent premiums and research concentration 70-80%

Suppliers exert material leverage: talent premiums (top‑firm starts $215,000 in 2024; AmLaw avg PEP ~$1.7M 2023) and niche experts raise costs and switching friction. Core tech and research duopolies (Westlaw/Lexis ~70–80% share) plus 3–5 year contracts boost vendor stickiness. Tier‑1 real estate scarcity and fit‑out costs ($100–$400/sq ft 2024) further constrain mobility.

| Supplier | Key metric |

|---|---|

| Talent | Top start $215k (2024); PEP ~$1.7M (2023) |

| Research | Westlaw/Lexis 70–80% market share |

| Tech/leases | Contracts 3–5 yrs; fit‑out $100–$400/sq ft (2024) |

| Experts | Expert networks ~$1.5B (2024) |

What is included in the product

Uncovers key drivers of competition, client influence, and entry risks for Sidley Austin, detailing bargaining power of clients and suppliers, threat of substitutes, and rivalry among elite law firms. Highlights disruptive factors, regulatory shifts, and strategic defenses that protect its market position.

A concise one-sheet Porter's Five Forces for Sidley Austin highlighting competitive pressures and mitigation strategies—easy to drop into decks, update with new market or regulatory data, and instantly communicate strategic risk to partners and boards.

Customers Bargaining Power

Institutional client consolidation

Institutional client consolidation sees many Fortune 500 corporates centralize legal panels in 2024, boosting buyer negotiating power. Competitive RFPs and volume discounts increasingly pressure hourly and alternative rates. Cross-border mandates give buyers leverage on staffing and jurisdictional pricing, though multi-year relationships still allow firms to command premium fees.

Price sensitivity and AFAs

Clients pushed AFAs in 2024—about 54% of in-house teams sought fixed or blended fees, constraining rate expansion and making matter-level economics transparent. Risk-sharing and success fees have increased margin variability, transferring upside and downside to firms like Sidley Austin, which reported roughly $1.6B revenue in 2024. Procurement professionalization—about 70% of large corporates using formal legal procurement—intensifies fee negotiation and budget discipline.

Switching and multi-firm strategies

Clients routinely split matters across several firms to benchmark performance, with GC panels in 2024 commonly ranging from 3 to 6 firms. Low switching costs for commoditized work—e.g., routine transactions or document review—amplify buyer power and drive price competition. High‑stakes litigation or M&A carry higher switching frictions but still prompt bake‑offs; conflicts of interest often compel clients to diversify counsel.

In-house capability growth

Expanded corporate legal teams retain more work internally as sophisticated GCs unbundle matters and dictate staffing, pushing Sidley to handle only complex or peak-load work; standardized services face growing rate pressure and alternative delivery models. External counsel is increasingly engaged for high-value, specialized matters while commodity work moves in-house.

Regulatory and cross-border complexity

Regulatory and cross-border complexity gives clients scope leverage as multi-jurisdiction matters require coordinated coverage and single-invoice solutions; the global legal services market surpassed $700 billion in 2024, driving demand for seamless provider networks. Coordination burdens shift to the firm, justifying volume-based discounts, though deep niche expertise can reduce buyer bargaining in specialized areas.

- Multi-jurisdiction scope

- Single-invoice demand

- Firm bears coordination costs

- Volume discounts justified

- Niche expertise lowers buyer power

Procurement, AFAs and 3-6 firm GC panels lift buyer leverage across global legal market

Institutional consolidation and procurement professionalization (≈70% of large corporates) raised buyer leverage in 2024, with GC panels commonly 3–6 firms. About 54% of in-house teams sought AFAs, pressuring rate growth and matter-level margins; Sidley reported ~$1.6B revenue in 2024. Cross-border scope (global legal market >$700B) shifts coordination costs to firms but niche expertise reduces buyer power on specialized mandates.

| Metric | 2024 |

|---|---|

| AFAs requested | 54% |

| Procurement use | ≈70% |

| GC panel size | 3–6 firms |

| Sidley revenue | ≈$1.6B |

| Global market | >$700B |

Same Document Delivered

Sidley Austin Porter's Five Forces Analysis

This preview shows the exact Sidley Austin Porter's Five Forces analysis you'll receive after purchase—no samples or placeholders. It is the full, professionally formatted document, ready for immediate download and use. What you see here is the deliverable you’ll get instantly upon payment.