Wood Resources Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

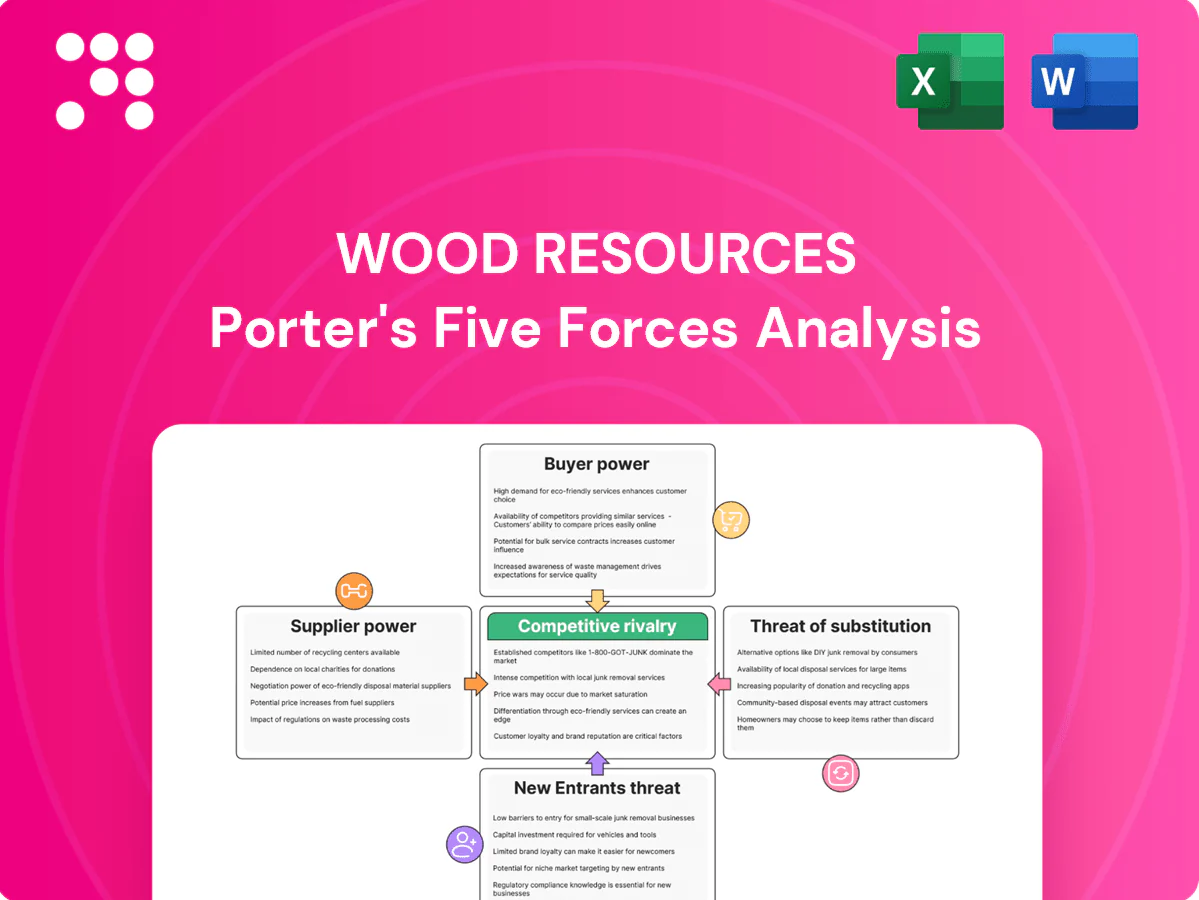

Wood Resources faces varied pressures across supplier leverage, buyer concentration, substitute materials, entry barriers, and competitive rivalry—shaping margins and strategic choices; this snapshot highlights where risks and advantages cluster. The full Porter’s Five Forces Analysis uncovers force-by-force ratings, data-driven implications, and visuals to guide investment or strategic moves. Unlock the complete report for a consultant-grade breakdown tailored to Wood Resources.

Suppliers Bargaining Power

Specialized data vendors

Providers of trade databases, customs data, and price series command fees and restrictive licenses, and in 2024 WRI’s dependence on timely, granular data gives these suppliers leverage in pricing and access terms.

Multi-sourcing and long-term contracts can temper annual price escalation and supply risk, often cutting volatility by roughly 20–30% in industry benchmarks.

Building proprietary datasets reduces reliance over time and can shift operating costs from recurring license fees to one-time collection and maintenance investments.

Satellite and geospatial providers

Remote-sensing imagery and forest-inventory feeds are concentrated among a few commercial providers—Maxar, Planet and Airbus—with Planet operating ~200+ smallsats in 2024 while Maxar and Airbus supply most high-resolution tasking capacity.

Pricing tiers, usage limits and API constraints drive analytics costs; enterprise imagery contracts commonly reach six-figure annual spend for high-frequency, high-res access.

WRI can mitigate by blending free Sentinel-2 and Landsat streams (10–30 m, global, open) with selective commercial buys.

Partnerships and multi-year volume commitments improve bargaining leverage and access to better SLAs and pricing.

Subject-matter experts and freelancers

Regional analysts and freelancers hold localized insights that are hard to replicate, giving suppliers measurable leverage; in 2024 freelancers made up an estimated 35% of the U.S. workforce, concentrating expertise in niche markets. Scarcity in Russia and parts of SE Asia pushes specialist day rates—commonly USD 500–2,000—higher than global averages. Retainer agreements and structured knowledge-capture programs materially lower key-person risk, while investing in analyst training builds internal capacity and reduces long-term supplier dependence.

Government and industry data sources

In 2024 many governments expanded open forestry datasets, but public statistics remain low-cost yet often delayed, revised, or methodologically inconsistent. Supplier power on price is low, but timing and quality constraints directly affect WRI deliverables and forecasting. Cross-validation across jurisdictions increases workload; data pipelines and normalization tools buffer variability and improve reliability.

- delays/revisions: common across national releases

- price power: low

- impact: timing/quality affect outputs

- mitigation: pipelines, normalization, cross-validation

Technology platforms and tools

- vendor-share: cloud dominance drives lock-in

- margin-risk: license hikes affect gross margins

- leverage: diversification + open-source >80% adoption

- mitigation: portability, APIs, containerization

Imaging and cloud concentration boost supplier leverage; multi-source data cuts risk

Specialized imagery, data and analysts (Planet ~200+ smallsats; Maxar, Airbus dominant) give suppliers price/access leverage; cloud concentration (AWS 32%, Azure 23%, GCP 11%) raises switching costs. Public forestry data is low-cost but delayed; freelancers (~35% US 2024) create localized scarcity. Multi-sourcing, proprietary datasets and multi-year contracts materially reduce supplier power.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| Imagery | Planet 200+ sats | High cost/access | Blend Sentinel/commercial |

| Cloud | AWS32%/AZ23% | Lock-in | Portability |

| Analysts | 35% freelancers | Scarcity | Retainers/training |

What is included in the product

Tailored exclusively for Wood Resources, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape pricing, profitability, and strategic positioning.

A concise one-sheet Porter’s Five Forces for Wood Resources—quickly spot supplier, buyer, entrant and substitute pressures to simplify strategic decisions. Customize pressure levels with latest timber market, trade and regulatory data for instant scenario-driven clarity.

Customers Bargaining Power

Concentrated enterprise clients

Large mills, traders and integrated firms leverage concentrated buying power—global roundwood production was about 1.9 billion m3 in 2024 (FAO), letting top buyers push volume discounts and run competitive RFPs that heighten price pressure. WRI offsets this with differentiated market insights, multi-year value propositions and executive relationships that demonstrate measurable ROI, reducing discount demands.

Availability of alternatives

Clients can easily compare Wood Resources International against niche consultancies and broad data vendors, giving buyers leverage because report switching costs are low. Embedding deliverables into client workflows and offering APIs raises stickiness by creating operational dependence. Proprietary benchmarks and indices, however, reduce direct comparability and help preserve pricing power.

In-house analytics capability

Major clients increasingly internalize forecasting and data engineering; by 2024 roughly 60% of large industrial buyers had dedicated analytics teams, creating credible make-or-buy options that cap pricing pressure on WRI.

To retain value WRI must outperform on breadth, speed, and independent perspective, offering cross-market datasets and faster model turnarounds than client teams.

Co-sourcing models—shared pipelines, white‑label reports, joint governance—can convert the threat into partnership revenue and higher retention.

Price sensitivity by segment

- segment: SMEs — high elasticity, ~20–25% churn

- strategics — pay 10–30% premium for customization

- pricing: tiered — +15% ARPU

- contracts: outcome-based — ~30% churn reduction

Demand for timeliness and accuracy

Clients penalize delays or inaccuracies, driving higher service-level expectations and more stringent contract terms that often include explicit penalties and audit rights.

WRI’s QA, systematic back-testing and rapid updates preserve trust, while transparent methodology reduces disputes and costly renegotiations by making assumptions and data provenance verifiable.

- Service penalties: explicit SLA clauses

- QA: routine back-testing

- Updates: rapid corrections to data

- Transparency: fewer disputes

Large buyers pressure prices; 60% use analytics; tiered pricing adds 15%

Large buyers (global roundwood ~1.9bn m3 in 2024) exert strong price pressure; 60% of large industrial buyers had analytics teams in 2024, raising make-or-buy threat. SMEs show 20–25% churn and high price elasticity; strategics pay 10–30% premium. Tiered pricing (+15% ARPU) and outcome-based contracts (≈30% lower churn) mitigate bargaining power.

| Metric | 2024 |

|---|---|

| Roundwood | 1.9bn m3 |

| Buyer analytics | 60% |

| SME churn | 20–25% |

| Strategic premium | 10–30% |

Preview the Actual Deliverable

Wood Resources Porter's Five Forces Analysis

This preview shows the exact Wood Resources Porter's Five Forces Analysis you'll receive upon purchase—no surprises, no placeholders. The document displayed is the professionally written, fully formatted analysis ready for immediate download and use the moment you buy. You’re previewing the final file; once you complete payment, you’ll get instant access to this same deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Wood Resources faces varied pressures across supplier leverage, buyer concentration, substitute materials, entry barriers, and competitive rivalry—shaping margins and strategic choices; this snapshot highlights where risks and advantages cluster. The full Porter’s Five Forces Analysis uncovers force-by-force ratings, data-driven implications, and visuals to guide investment or strategic moves. Unlock the complete report for a consultant-grade breakdown tailored to Wood Resources.

Suppliers Bargaining Power

Specialized data vendors

Providers of trade databases, customs data, and price series command fees and restrictive licenses, and in 2024 WRI’s dependence on timely, granular data gives these suppliers leverage in pricing and access terms.

Multi-sourcing and long-term contracts can temper annual price escalation and supply risk, often cutting volatility by roughly 20–30% in industry benchmarks.

Building proprietary datasets reduces reliance over time and can shift operating costs from recurring license fees to one-time collection and maintenance investments.

Satellite and geospatial providers

Remote-sensing imagery and forest-inventory feeds are concentrated among a few commercial providers—Maxar, Planet and Airbus—with Planet operating ~200+ smallsats in 2024 while Maxar and Airbus supply most high-resolution tasking capacity.

Pricing tiers, usage limits and API constraints drive analytics costs; enterprise imagery contracts commonly reach six-figure annual spend for high-frequency, high-res access.

WRI can mitigate by blending free Sentinel-2 and Landsat streams (10–30 m, global, open) with selective commercial buys.

Partnerships and multi-year volume commitments improve bargaining leverage and access to better SLAs and pricing.

Subject-matter experts and freelancers

Regional analysts and freelancers hold localized insights that are hard to replicate, giving suppliers measurable leverage; in 2024 freelancers made up an estimated 35% of the U.S. workforce, concentrating expertise in niche markets. Scarcity in Russia and parts of SE Asia pushes specialist day rates—commonly USD 500–2,000—higher than global averages. Retainer agreements and structured knowledge-capture programs materially lower key-person risk, while investing in analyst training builds internal capacity and reduces long-term supplier dependence.

Government and industry data sources

In 2024 many governments expanded open forestry datasets, but public statistics remain low-cost yet often delayed, revised, or methodologically inconsistent. Supplier power on price is low, but timing and quality constraints directly affect WRI deliverables and forecasting. Cross-validation across jurisdictions increases workload; data pipelines and normalization tools buffer variability and improve reliability.

- delays/revisions: common across national releases

- price power: low

- impact: timing/quality affect outputs

- mitigation: pipelines, normalization, cross-validation

Technology platforms and tools

- vendor-share: cloud dominance drives lock-in

- margin-risk: license hikes affect gross margins

- leverage: diversification + open-source >80% adoption

- mitigation: portability, APIs, containerization

Imaging and cloud concentration boost supplier leverage; multi-source data cuts risk

Specialized imagery, data and analysts (Planet ~200+ smallsats; Maxar, Airbus dominant) give suppliers price/access leverage; cloud concentration (AWS 32%, Azure 23%, GCP 11%) raises switching costs. Public forestry data is low-cost but delayed; freelancers (~35% US 2024) create localized scarcity. Multi-sourcing, proprietary datasets and multi-year contracts materially reduce supplier power.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| Imagery | Planet 200+ sats | High cost/access | Blend Sentinel/commercial |

| Cloud | AWS32%/AZ23% | Lock-in | Portability |

| Analysts | 35% freelancers | Scarcity | Retainers/training |

What is included in the product

Tailored exclusively for Wood Resources, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape pricing, profitability, and strategic positioning.

A concise one-sheet Porter’s Five Forces for Wood Resources—quickly spot supplier, buyer, entrant and substitute pressures to simplify strategic decisions. Customize pressure levels with latest timber market, trade and regulatory data for instant scenario-driven clarity.

Customers Bargaining Power

Concentrated enterprise clients

Large mills, traders and integrated firms leverage concentrated buying power—global roundwood production was about 1.9 billion m3 in 2024 (FAO), letting top buyers push volume discounts and run competitive RFPs that heighten price pressure. WRI offsets this with differentiated market insights, multi-year value propositions and executive relationships that demonstrate measurable ROI, reducing discount demands.

Availability of alternatives

Clients can easily compare Wood Resources International against niche consultancies and broad data vendors, giving buyers leverage because report switching costs are low. Embedding deliverables into client workflows and offering APIs raises stickiness by creating operational dependence. Proprietary benchmarks and indices, however, reduce direct comparability and help preserve pricing power.

In-house analytics capability

Major clients increasingly internalize forecasting and data engineering; by 2024 roughly 60% of large industrial buyers had dedicated analytics teams, creating credible make-or-buy options that cap pricing pressure on WRI.

To retain value WRI must outperform on breadth, speed, and independent perspective, offering cross-market datasets and faster model turnarounds than client teams.

Co-sourcing models—shared pipelines, white‑label reports, joint governance—can convert the threat into partnership revenue and higher retention.

Price sensitivity by segment

- segment: SMEs — high elasticity, ~20–25% churn

- strategics — pay 10–30% premium for customization

- pricing: tiered — +15% ARPU

- contracts: outcome-based — ~30% churn reduction

Demand for timeliness and accuracy

Clients penalize delays or inaccuracies, driving higher service-level expectations and more stringent contract terms that often include explicit penalties and audit rights.

WRI’s QA, systematic back-testing and rapid updates preserve trust, while transparent methodology reduces disputes and costly renegotiations by making assumptions and data provenance verifiable.

- Service penalties: explicit SLA clauses

- QA: routine back-testing

- Updates: rapid corrections to data

- Transparency: fewer disputes

Large buyers pressure prices; 60% use analytics; tiered pricing adds 15%

Large buyers (global roundwood ~1.9bn m3 in 2024) exert strong price pressure; 60% of large industrial buyers had analytics teams in 2024, raising make-or-buy threat. SMEs show 20–25% churn and high price elasticity; strategics pay 10–30% premium. Tiered pricing (+15% ARPU) and outcome-based contracts (≈30% lower churn) mitigate bargaining power.

| Metric | 2024 |

|---|---|

| Roundwood | 1.9bn m3 |

| Buyer analytics | 60% |

| SME churn | 20–25% |

| Strategic premium | 10–30% |

Preview the Actual Deliverable

Wood Resources Porter's Five Forces Analysis

This preview shows the exact Wood Resources Porter's Five Forces Analysis you'll receive upon purchase—no surprises, no placeholders. The document displayed is the professionally written, fully formatted analysis ready for immediate download and use the moment you buy. You’re previewing the final file; once you complete payment, you’ll get instant access to this same deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Wood Resources faces varied pressures across supplier leverage, buyer concentration, substitute materials, entry barriers, and competitive rivalry—shaping margins and strategic choices; this snapshot highlights where risks and advantages cluster. The full Porter’s Five Forces Analysis uncovers force-by-force ratings, data-driven implications, and visuals to guide investment or strategic moves. Unlock the complete report for a consultant-grade breakdown tailored to Wood Resources.

Suppliers Bargaining Power

Specialized data vendors

Providers of trade databases, customs data, and price series command fees and restrictive licenses, and in 2024 WRI’s dependence on timely, granular data gives these suppliers leverage in pricing and access terms.

Multi-sourcing and long-term contracts can temper annual price escalation and supply risk, often cutting volatility by roughly 20–30% in industry benchmarks.

Building proprietary datasets reduces reliance over time and can shift operating costs from recurring license fees to one-time collection and maintenance investments.

Satellite and geospatial providers

Remote-sensing imagery and forest-inventory feeds are concentrated among a few commercial providers—Maxar, Planet and Airbus—with Planet operating ~200+ smallsats in 2024 while Maxar and Airbus supply most high-resolution tasking capacity.

Pricing tiers, usage limits and API constraints drive analytics costs; enterprise imagery contracts commonly reach six-figure annual spend for high-frequency, high-res access.

WRI can mitigate by blending free Sentinel-2 and Landsat streams (10–30 m, global, open) with selective commercial buys.

Partnerships and multi-year volume commitments improve bargaining leverage and access to better SLAs and pricing.

Subject-matter experts and freelancers

Regional analysts and freelancers hold localized insights that are hard to replicate, giving suppliers measurable leverage; in 2024 freelancers made up an estimated 35% of the U.S. workforce, concentrating expertise in niche markets. Scarcity in Russia and parts of SE Asia pushes specialist day rates—commonly USD 500–2,000—higher than global averages. Retainer agreements and structured knowledge-capture programs materially lower key-person risk, while investing in analyst training builds internal capacity and reduces long-term supplier dependence.

Government and industry data sources

In 2024 many governments expanded open forestry datasets, but public statistics remain low-cost yet often delayed, revised, or methodologically inconsistent. Supplier power on price is low, but timing and quality constraints directly affect WRI deliverables and forecasting. Cross-validation across jurisdictions increases workload; data pipelines and normalization tools buffer variability and improve reliability.

- delays/revisions: common across national releases

- price power: low

- impact: timing/quality affect outputs

- mitigation: pipelines, normalization, cross-validation

Technology platforms and tools

- vendor-share: cloud dominance drives lock-in

- margin-risk: license hikes affect gross margins

- leverage: diversification + open-source >80% adoption

- mitigation: portability, APIs, containerization

Imaging and cloud concentration boost supplier leverage; multi-source data cuts risk

Specialized imagery, data and analysts (Planet ~200+ smallsats; Maxar, Airbus dominant) give suppliers price/access leverage; cloud concentration (AWS 32%, Azure 23%, GCP 11%) raises switching costs. Public forestry data is low-cost but delayed; freelancers (~35% US 2024) create localized scarcity. Multi-sourcing, proprietary datasets and multi-year contracts materially reduce supplier power.

| Supplier | 2024 metric | Impact | Mitigation |

|---|---|---|---|

| Imagery | Planet 200+ sats | High cost/access | Blend Sentinel/commercial |

| Cloud | AWS32%/AZ23% | Lock-in | Portability |

| Analysts | 35% freelancers | Scarcity | Retainers/training |

What is included in the product

Tailored exclusively for Wood Resources, this Porter's Five Forces overview uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes, and emerging threats that shape pricing, profitability, and strategic positioning.

A concise one-sheet Porter’s Five Forces for Wood Resources—quickly spot supplier, buyer, entrant and substitute pressures to simplify strategic decisions. Customize pressure levels with latest timber market, trade and regulatory data for instant scenario-driven clarity.

Customers Bargaining Power

Concentrated enterprise clients

Large mills, traders and integrated firms leverage concentrated buying power—global roundwood production was about 1.9 billion m3 in 2024 (FAO), letting top buyers push volume discounts and run competitive RFPs that heighten price pressure. WRI offsets this with differentiated market insights, multi-year value propositions and executive relationships that demonstrate measurable ROI, reducing discount demands.

Availability of alternatives

Clients can easily compare Wood Resources International against niche consultancies and broad data vendors, giving buyers leverage because report switching costs are low. Embedding deliverables into client workflows and offering APIs raises stickiness by creating operational dependence. Proprietary benchmarks and indices, however, reduce direct comparability and help preserve pricing power.

In-house analytics capability

Major clients increasingly internalize forecasting and data engineering; by 2024 roughly 60% of large industrial buyers had dedicated analytics teams, creating credible make-or-buy options that cap pricing pressure on WRI.

To retain value WRI must outperform on breadth, speed, and independent perspective, offering cross-market datasets and faster model turnarounds than client teams.

Co-sourcing models—shared pipelines, white‑label reports, joint governance—can convert the threat into partnership revenue and higher retention.

Price sensitivity by segment

- segment: SMEs — high elasticity, ~20–25% churn

- strategics — pay 10–30% premium for customization

- pricing: tiered — +15% ARPU

- contracts: outcome-based — ~30% churn reduction

Demand for timeliness and accuracy

Clients penalize delays or inaccuracies, driving higher service-level expectations and more stringent contract terms that often include explicit penalties and audit rights.

WRI’s QA, systematic back-testing and rapid updates preserve trust, while transparent methodology reduces disputes and costly renegotiations by making assumptions and data provenance verifiable.

- Service penalties: explicit SLA clauses

- QA: routine back-testing

- Updates: rapid corrections to data

- Transparency: fewer disputes

Large buyers pressure prices; 60% use analytics; tiered pricing adds 15%

Large buyers (global roundwood ~1.9bn m3 in 2024) exert strong price pressure; 60% of large industrial buyers had analytics teams in 2024, raising make-or-buy threat. SMEs show 20–25% churn and high price elasticity; strategics pay 10–30% premium. Tiered pricing (+15% ARPU) and outcome-based contracts (≈30% lower churn) mitigate bargaining power.

| Metric | 2024 |

|---|---|

| Roundwood | 1.9bn m3 |

| Buyer analytics | 60% |

| SME churn | 20–25% |

| Strategic premium | 10–30% |

Preview the Actual Deliverable

Wood Resources Porter's Five Forces Analysis

This preview shows the exact Wood Resources Porter's Five Forces Analysis you'll receive upon purchase—no surprises, no placeholders. The document displayed is the professionally written, fully formatted analysis ready for immediate download and use the moment you buy. You’re previewing the final file; once you complete payment, you’ll get instant access to this same deliverable.