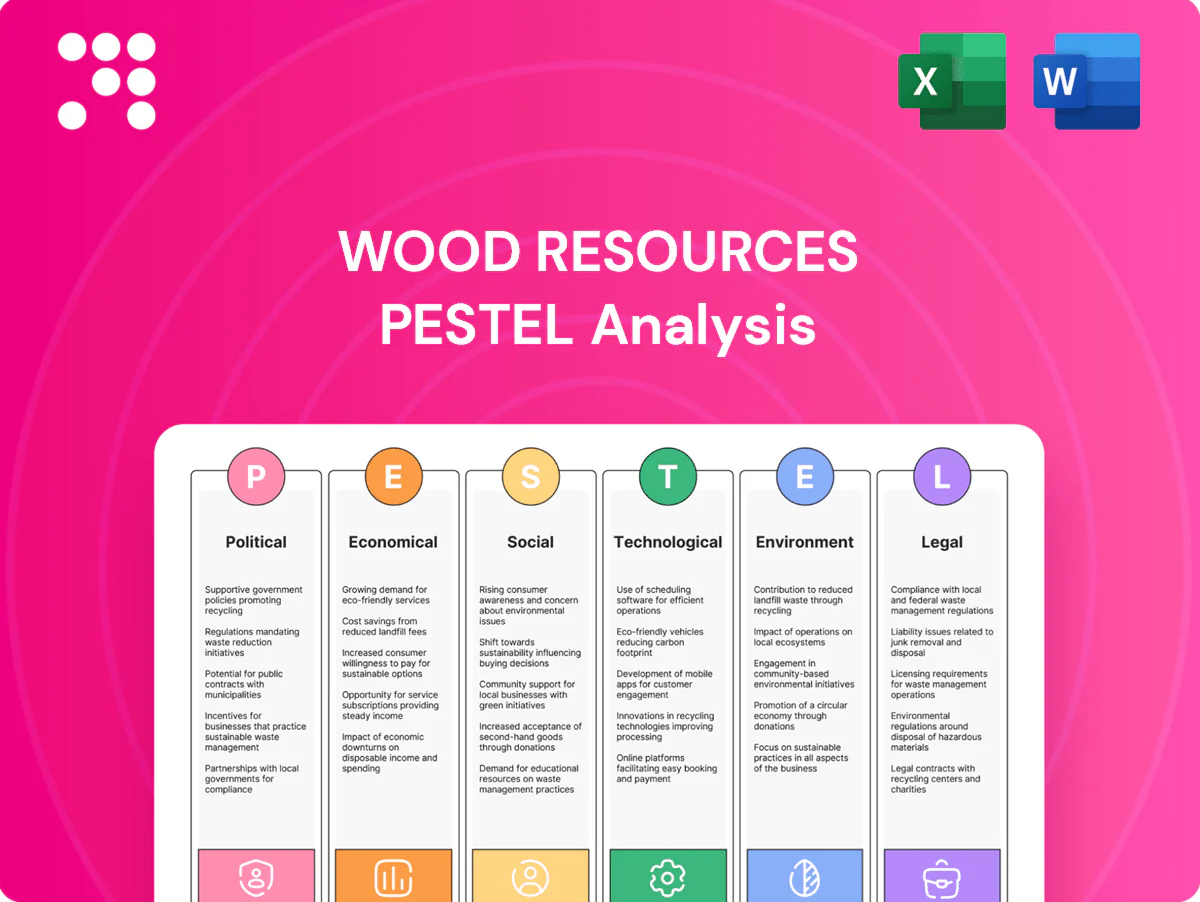

Wood Resources PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock the forces shaping Wood Resources with our concise PESTLE snapshot—covering political, economic, social, technological, legal, and environmental trends that matter to investors and strategists. For a full, actionable breakdown and ready-to-use charts, purchase the complete PESTLE analysis and make smarter, faster decisions.

Political factors

Trade policy shifts

Changes to tariffs, quotas and sanctions reshape wood flows and price arbitrage, with recent policy moves producing tariff swings that have shifted landed costs by an estimated 5–15% in key corridors. WRI must monitor WTO disputes and bilateral deals that alter fiber and lumber competitiveness, as a 2024 tariff action between major suppliers delayed shipments and widened spreads. Rapid updates let clients re-route sourcing and hedge exposure, while scenario maps quantify winners and losers by corridor.

Forestry subsidies and incentives

Government supports for bioenergy, reforestation and sawmill upgrades—including US Inflation Reduction Act investments (~$369 billion into clean energy and resilience)—can distort regional stumpage, chip and pellet supply by redirecting feedstock and capital. WRI benchmarks quantify subsidy impacts across stumpage, chip and pellet markets to show price and volume effects. Clients require clarity on incentive durability across election cycles, and sensitivity analysis models subsidy withdrawal risk.

Geopolitical disruptions

Conflicts and sanctions such as the Russia–Ukraine war and ensuing EU measures in 2022–23 have abruptly constrained key exporters and transit routes for timber. WRI tracks political risk premia embedded in delivered costs as geopolitical shocks reshape sourcing economics in 2024. Clients require contingency sourcing playbooks and inventory buffers. Country-risk matrices guide portfolio diversification across suppliers and corridors.

Carbon and climate policy

- National NDC alignment: raises demand for low‑carbon wood

- Carbon taxes/ETS: €100–120/t current benchmark

- CBAM: trade‑level impact since 2023

- WRI price pathways: used for go/no‑go assessments

Public land and permitting regimes

- Regional fiber shifts reduce local supply, raising delivered cost pressure

- Typical lead times 6–24 months; permitting delays often >12 months

- Permit bottlenecks lower mill run-rates and increase outage risk

- Policy advocacy tracking used to protect access and guide capex timing

5–15% · $369bn · €100–120/t tariffs & policy reshape supply

Tariff shifts alter landed costs by 5–15% and WTO disputes drive corridor re‑routing. Policy supports (US IRA ~$369bn) and EU ETS at €100–120/t (2024–25) redirect feedstock and capex. Harvesting right changes with 6–24 month lead times and permitting delays >12 months raise outage risk.

| Metric | Value |

|---|---|

| Tariff impact | 5–15% |

| US IRA | $369bn |

| EU ETS (2024–25) | €100–120/t |

| Lead times | 6–24 months |

What is included in the product

Explores how macro-environmental forces uniquely affect Wood Resources across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

A concise, visually segmented PESTLE summary of Wood Resources that distills regulatory, market and environmental risks for easy inclusion in presentations and planning sessions, enabling quick alignment across teams and customizable notes for regional or business-line context.

Economic factors

Construction cycle exposure

Lumber demand closely follows US housing starts (≈1.35 million annualized in 2024) and a repair/maintenance market near $450 billion; higher mortgage and Fed policy rates (federal funds ≈5.25% in 2024) have tempered activity. Wood Resources International links these macro indicators to sawtimber and lumber price forecasts, so clients calibrate inventory and pricing at cycle turns. Elasticity estimates inform product‑mix shifts toward higher‑value items when volumes fall.

Currency and freight volatility

FX swings—USD appreciated about 8–10% vs major currencies in 2024—together with ocean rate volatility (Asia–NA container rates averaged roughly $2,000/FEU in 2024) routinely re-rank export competitiveness across basins. WRI embeds bunker (~$450/t 2024), container and breakbulk costs into delivered-price curves; clients hedge FX and freight using corridor-level breakevens, with real-time indices enabling tactical intraday trades.

Inflation and capital costs

Input inflation (US CPI ~3.4% in 2024) and higher borrowing costs (Fed funds ~5.25–5.50%) compress mill margins and can shave project IRRs by several hundred basis points. Wood Resources International stress-tests cash costs and capex across rate scenarios to quantify sensitivity. Clients are revising contract terms and raising hurdle rates while cost pass-through analysis informs dynamic pricing and indexation clauses.

Emerging market demand

Rising urbanization in Asia, MENA (urbanization >60%) and Africa (urban share approaching 50%) is lifting panel and lumber consumption, expanding construction and retail demand markets in 2024–25. Wood Resources International (WRI) sizes addressable growth and port/logistics constraints to quantify realistic volumes and bottlenecks. Clients prioritize markets with clear demand-to-supply gaps and higher margin potential. Entry sequencing is aligned to logistics capacity and policy risk, prioritizing ports and stable regulatory regimes.

- Urbanization: MENA >60%, Africa ~50% (UN, 2022–23)

- WRI: addressesable growth vs port constraints

- Clients: favor markets with demand-supply gaps

- Entry: sequenced by logistics and policy risk

Substitution and product mix

Price spreads drive shifts between hardwood/softwood, chips/pellets, and engineered wood; WRI quantifies cross-price elasticities and mill switching costs to model substitution and short-run supply response. Clients optimize feedstock contracts and product slate using these elasticities and scenario runs. Margin bridges identify where incremental capacity deployment yields the highest return.

- WRI: cross-price elasticities, switching costs

- Clients: feedstock contract + product slate optimization

- Margin bridges: capacity deployment signals

5–15% · $369bn · €100–120/t tariffs & policy reshape supply

Macroeconomic drivers (US housing starts ≈1.35m 2024, Fed funds ≈5.25%, US CPI ≈3.4%) moderate lumber demand and compress mill margins. USD appreciation (~8–10% 2024) and ocean rates (~$2,000/FEU, bunker ~$450/t) reshape export competitiveness. Urbanization (MENA >60%, Africa ~50%) lifts panel demand; WRI models elasticities to guide product mix and hedge strategies.

| Metric | 2024/25 |

|---|---|

| US housing starts | ≈1.35m |

| Fed funds | ≈5.25% |

| USD vs majors | +8–10% |

| Container rate | $2,000/FEU |

| Bunker | $450/t |

Full Version Awaits

Wood Resources PESTLE Analysis

The Wood Resources PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock the forces shaping Wood Resources with our concise PESTLE snapshot—covering political, economic, social, technological, legal, and environmental trends that matter to investors and strategists. For a full, actionable breakdown and ready-to-use charts, purchase the complete PESTLE analysis and make smarter, faster decisions.

Political factors

Trade policy shifts

Changes to tariffs, quotas and sanctions reshape wood flows and price arbitrage, with recent policy moves producing tariff swings that have shifted landed costs by an estimated 5–15% in key corridors. WRI must monitor WTO disputes and bilateral deals that alter fiber and lumber competitiveness, as a 2024 tariff action between major suppliers delayed shipments and widened spreads. Rapid updates let clients re-route sourcing and hedge exposure, while scenario maps quantify winners and losers by corridor.

Forestry subsidies and incentives

Government supports for bioenergy, reforestation and sawmill upgrades—including US Inflation Reduction Act investments (~$369 billion into clean energy and resilience)—can distort regional stumpage, chip and pellet supply by redirecting feedstock and capital. WRI benchmarks quantify subsidy impacts across stumpage, chip and pellet markets to show price and volume effects. Clients require clarity on incentive durability across election cycles, and sensitivity analysis models subsidy withdrawal risk.

Geopolitical disruptions

Conflicts and sanctions such as the Russia–Ukraine war and ensuing EU measures in 2022–23 have abruptly constrained key exporters and transit routes for timber. WRI tracks political risk premia embedded in delivered costs as geopolitical shocks reshape sourcing economics in 2024. Clients require contingency sourcing playbooks and inventory buffers. Country-risk matrices guide portfolio diversification across suppliers and corridors.

Carbon and climate policy

- National NDC alignment: raises demand for low‑carbon wood

- Carbon taxes/ETS: €100–120/t current benchmark

- CBAM: trade‑level impact since 2023

- WRI price pathways: used for go/no‑go assessments

Public land and permitting regimes

- Regional fiber shifts reduce local supply, raising delivered cost pressure

- Typical lead times 6–24 months; permitting delays often >12 months

- Permit bottlenecks lower mill run-rates and increase outage risk

- Policy advocacy tracking used to protect access and guide capex timing

5–15% · $369bn · €100–120/t tariffs & policy reshape supply

Tariff shifts alter landed costs by 5–15% and WTO disputes drive corridor re‑routing. Policy supports (US IRA ~$369bn) and EU ETS at €100–120/t (2024–25) redirect feedstock and capex. Harvesting right changes with 6–24 month lead times and permitting delays >12 months raise outage risk.

| Metric | Value |

|---|---|

| Tariff impact | 5–15% |

| US IRA | $369bn |

| EU ETS (2024–25) | €100–120/t |

| Lead times | 6–24 months |

What is included in the product

Explores how macro-environmental forces uniquely affect Wood Resources across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

A concise, visually segmented PESTLE summary of Wood Resources that distills regulatory, market and environmental risks for easy inclusion in presentations and planning sessions, enabling quick alignment across teams and customizable notes for regional or business-line context.

Economic factors

Construction cycle exposure

Lumber demand closely follows US housing starts (≈1.35 million annualized in 2024) and a repair/maintenance market near $450 billion; higher mortgage and Fed policy rates (federal funds ≈5.25% in 2024) have tempered activity. Wood Resources International links these macro indicators to sawtimber and lumber price forecasts, so clients calibrate inventory and pricing at cycle turns. Elasticity estimates inform product‑mix shifts toward higher‑value items when volumes fall.

Currency and freight volatility

FX swings—USD appreciated about 8–10% vs major currencies in 2024—together with ocean rate volatility (Asia–NA container rates averaged roughly $2,000/FEU in 2024) routinely re-rank export competitiveness across basins. WRI embeds bunker (~$450/t 2024), container and breakbulk costs into delivered-price curves; clients hedge FX and freight using corridor-level breakevens, with real-time indices enabling tactical intraday trades.

Inflation and capital costs

Input inflation (US CPI ~3.4% in 2024) and higher borrowing costs (Fed funds ~5.25–5.50%) compress mill margins and can shave project IRRs by several hundred basis points. Wood Resources International stress-tests cash costs and capex across rate scenarios to quantify sensitivity. Clients are revising contract terms and raising hurdle rates while cost pass-through analysis informs dynamic pricing and indexation clauses.

Emerging market demand

Rising urbanization in Asia, MENA (urbanization >60%) and Africa (urban share approaching 50%) is lifting panel and lumber consumption, expanding construction and retail demand markets in 2024–25. Wood Resources International (WRI) sizes addressable growth and port/logistics constraints to quantify realistic volumes and bottlenecks. Clients prioritize markets with clear demand-to-supply gaps and higher margin potential. Entry sequencing is aligned to logistics capacity and policy risk, prioritizing ports and stable regulatory regimes.

- Urbanization: MENA >60%, Africa ~50% (UN, 2022–23)

- WRI: addressesable growth vs port constraints

- Clients: favor markets with demand-supply gaps

- Entry: sequenced by logistics and policy risk

Substitution and product mix

Price spreads drive shifts between hardwood/softwood, chips/pellets, and engineered wood; WRI quantifies cross-price elasticities and mill switching costs to model substitution and short-run supply response. Clients optimize feedstock contracts and product slate using these elasticities and scenario runs. Margin bridges identify where incremental capacity deployment yields the highest return.

- WRI: cross-price elasticities, switching costs

- Clients: feedstock contract + product slate optimization

- Margin bridges: capacity deployment signals

5–15% · $369bn · €100–120/t tariffs & policy reshape supply

Macroeconomic drivers (US housing starts ≈1.35m 2024, Fed funds ≈5.25%, US CPI ≈3.4%) moderate lumber demand and compress mill margins. USD appreciation (~8–10% 2024) and ocean rates (~$2,000/FEU, bunker ~$450/t) reshape export competitiveness. Urbanization (MENA >60%, Africa ~50%) lifts panel demand; WRI models elasticities to guide product mix and hedge strategies.

| Metric | 2024/25 |

|---|---|

| US housing starts | ≈1.35m |

| Fed funds | ≈5.25% |

| USD vs majors | +8–10% |

| Container rate | $2,000/FEU |

| Bunker | $450/t |

Full Version Awaits

Wood Resources PESTLE Analysis

The Wood Resources PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock the forces shaping Wood Resources with our concise PESTLE snapshot—covering political, economic, social, technological, legal, and environmental trends that matter to investors and strategists. For a full, actionable breakdown and ready-to-use charts, purchase the complete PESTLE analysis and make smarter, faster decisions.

Political factors

Trade policy shifts

Changes to tariffs, quotas and sanctions reshape wood flows and price arbitrage, with recent policy moves producing tariff swings that have shifted landed costs by an estimated 5–15% in key corridors. WRI must monitor WTO disputes and bilateral deals that alter fiber and lumber competitiveness, as a 2024 tariff action between major suppliers delayed shipments and widened spreads. Rapid updates let clients re-route sourcing and hedge exposure, while scenario maps quantify winners and losers by corridor.

Forestry subsidies and incentives

Government supports for bioenergy, reforestation and sawmill upgrades—including US Inflation Reduction Act investments (~$369 billion into clean energy and resilience)—can distort regional stumpage, chip and pellet supply by redirecting feedstock and capital. WRI benchmarks quantify subsidy impacts across stumpage, chip and pellet markets to show price and volume effects. Clients require clarity on incentive durability across election cycles, and sensitivity analysis models subsidy withdrawal risk.

Geopolitical disruptions

Conflicts and sanctions such as the Russia–Ukraine war and ensuing EU measures in 2022–23 have abruptly constrained key exporters and transit routes for timber. WRI tracks political risk premia embedded in delivered costs as geopolitical shocks reshape sourcing economics in 2024. Clients require contingency sourcing playbooks and inventory buffers. Country-risk matrices guide portfolio diversification across suppliers and corridors.

Carbon and climate policy

- National NDC alignment: raises demand for low‑carbon wood

- Carbon taxes/ETS: €100–120/t current benchmark

- CBAM: trade‑level impact since 2023

- WRI price pathways: used for go/no‑go assessments

Public land and permitting regimes

- Regional fiber shifts reduce local supply, raising delivered cost pressure

- Typical lead times 6–24 months; permitting delays often >12 months

- Permit bottlenecks lower mill run-rates and increase outage risk

- Policy advocacy tracking used to protect access and guide capex timing

5–15% · $369bn · €100–120/t tariffs & policy reshape supply

Tariff shifts alter landed costs by 5–15% and WTO disputes drive corridor re‑routing. Policy supports (US IRA ~$369bn) and EU ETS at €100–120/t (2024–25) redirect feedstock and capex. Harvesting right changes with 6–24 month lead times and permitting delays >12 months raise outage risk.

| Metric | Value |

|---|---|

| Tariff impact | 5–15% |

| US IRA | $369bn |

| EU ETS (2024–25) | €100–120/t |

| Lead times | 6–24 months |

What is included in the product

Explores how macro-environmental forces uniquely affect Wood Resources across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and forward-looking insights to help executives, consultants, and entrepreneurs identify risks, opportunities, and strategic responses.

A concise, visually segmented PESTLE summary of Wood Resources that distills regulatory, market and environmental risks for easy inclusion in presentations and planning sessions, enabling quick alignment across teams and customizable notes for regional or business-line context.

Economic factors

Construction cycle exposure

Lumber demand closely follows US housing starts (≈1.35 million annualized in 2024) and a repair/maintenance market near $450 billion; higher mortgage and Fed policy rates (federal funds ≈5.25% in 2024) have tempered activity. Wood Resources International links these macro indicators to sawtimber and lumber price forecasts, so clients calibrate inventory and pricing at cycle turns. Elasticity estimates inform product‑mix shifts toward higher‑value items when volumes fall.

Currency and freight volatility

FX swings—USD appreciated about 8–10% vs major currencies in 2024—together with ocean rate volatility (Asia–NA container rates averaged roughly $2,000/FEU in 2024) routinely re-rank export competitiveness across basins. WRI embeds bunker (~$450/t 2024), container and breakbulk costs into delivered-price curves; clients hedge FX and freight using corridor-level breakevens, with real-time indices enabling tactical intraday trades.

Inflation and capital costs

Input inflation (US CPI ~3.4% in 2024) and higher borrowing costs (Fed funds ~5.25–5.50%) compress mill margins and can shave project IRRs by several hundred basis points. Wood Resources International stress-tests cash costs and capex across rate scenarios to quantify sensitivity. Clients are revising contract terms and raising hurdle rates while cost pass-through analysis informs dynamic pricing and indexation clauses.

Emerging market demand

Rising urbanization in Asia, MENA (urbanization >60%) and Africa (urban share approaching 50%) is lifting panel and lumber consumption, expanding construction and retail demand markets in 2024–25. Wood Resources International (WRI) sizes addressable growth and port/logistics constraints to quantify realistic volumes and bottlenecks. Clients prioritize markets with clear demand-to-supply gaps and higher margin potential. Entry sequencing is aligned to logistics capacity and policy risk, prioritizing ports and stable regulatory regimes.

- Urbanization: MENA >60%, Africa ~50% (UN, 2022–23)

- WRI: addressesable growth vs port constraints

- Clients: favor markets with demand-supply gaps

- Entry: sequenced by logistics and policy risk

Substitution and product mix

Price spreads drive shifts between hardwood/softwood, chips/pellets, and engineered wood; WRI quantifies cross-price elasticities and mill switching costs to model substitution and short-run supply response. Clients optimize feedstock contracts and product slate using these elasticities and scenario runs. Margin bridges identify where incremental capacity deployment yields the highest return.

- WRI: cross-price elasticities, switching costs

- Clients: feedstock contract + product slate optimization

- Margin bridges: capacity deployment signals

5–15% · $369bn · €100–120/t tariffs & policy reshape supply

Macroeconomic drivers (US housing starts ≈1.35m 2024, Fed funds ≈5.25%, US CPI ≈3.4%) moderate lumber demand and compress mill margins. USD appreciation (~8–10% 2024) and ocean rates (~$2,000/FEU, bunker ~$450/t) reshape export competitiveness. Urbanization (MENA >60%, Africa ~50%) lifts panel demand; WRI models elasticities to guide product mix and hedge strategies.

| Metric | 2024/25 |

|---|---|

| US housing starts | ≈1.35m |

| Fed funds | ≈5.25% |

| USD vs majors | +8–10% |

| Container rate | $2,000/FEU |

| Bunker | $450/t |

Full Version Awaits

Wood Resources PESTLE Analysis

The Wood Resources PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are exactly what you’ll download immediately after payment. No placeholders or teasers—this is the final, professionally structured file.