Sigma Healthcare PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Sigma Healthcare—three concise sections reveal how political shifts, economic pressures, and tech trends will shape growth and risk. Ideal for investors and strategists seeking actionable insights. Purchase the full report to access the complete, editable breakdown and make informed decisions today.

Political factors

PBS and pricing policy

Commonwealth PBS settings drive about 240 million scripts p.a. and roughly AUD 11 billion in government PBS spending, directly shaping Sigma’s wholesale volumes and margins.

Price disclosure and statutory price reductions have historically compressed distributor rebates and can shave percentage points off slim wholesale margins.

Policy shifts on co‑payments or 60‑day dispensing change order frequency and inventory turns, affecting working capital.

Sigma must pursue active policy advocacy and rapid contract and stocking model adjustments to protect margins and cash flow.

Community Pharmacy Agreements

Successive Community Pharmacy Agreements set remuneration, location rules and service funding within the multi-billion-dollar PBS framework, directly shaping pharmacy viability. Changes to CPA terms materially affect Sigma’s banner partners’ profitability and store footprint across thousands of community sites. Stability provides more predictable demand for wholesale and retail channels, while renegotiations create planning risk. Sigma reduces exposure through early scenario planning with banner owners.

Federal–state health priorities

Variations in state hospital funding and procurement policies drive institutional sales for Sigma, especially as Australia spends roughly 10% of GDP on health and serves ~26 million people. Federal emphasis on primary care and vaccination programs (millions vaccinated annually) increases service-led volumes. Political focus on regional health unlocks targeted grants for distribution resilience, and alignment with public health campaigns strengthens brand standing.

Supply chain sovereignty

Canberra’s 2024 push for medicine security prioritises local stockholding and strategic reserves, prompting incentives and possible mandates for higher safety stocks and real-time reporting that could increase working capital by an estimated low-double-digit percentage for distributors.

Higher inventory requirements may deepen customer ties as Sigma can market itself as a national resilience partner, leveraging its pharmacy network and logistics to capture government and retail contracts.

- policy: 2024 federal focus on medicine security

- impact: safety-stock rise → working capital up (low-double-digit %)

- opportunity: stronger ties with government & pharmacies

- positioning: Sigma as supply partner for national resilience

Trade and import dynamics

Free trade agreements and tariff settings materially affect Sigma Healthcare’s landed cost for generics and OTC lines, altering gross margins and retail pricing flexibility.

Geopolitical tensions and supply-chain disruptions in China and India have previously interrupted API and finished-goods flows, while export controls or domestic priority allocations can be triggered during shortages.

Diversified sourcing, inventory buffers and active policy engagement with regulators mitigate procurement shocks and protect continuity of supply.

- trade: FTAs/tariffs influence landed cost

- geopolitics: China/India supply risk

- controls: export/priority rules in shortages

- mitigation: diversification & policy engagement

PBS spend anchors wholesale volumes while price cuts and medicine‑security lift working capital

Commonwealth PBS (~AUD 11bn spend; ~240m scripts p.a.) drives Sigma’s wholesale volumes, margins and community pharmacy demand.

Price disclosure and statutory cuts compress distributor rebates, shaving points off already slim margins.

2024 medicine‑security push increases mandated safety stocks (estimated low‑double‑digit % rise in working capital) and reporting requirements.

State hospital procurement, FTAs and China/India supply risks affect landed costs and institutional sales, creating both risk and contracting opportunities.

| Policy | Impact | Data | Opportunity |

|---|---|---|---|

| PBS/CPA | Volume/margin | AUD 11bn; 240m scripts | Stable demand |

| Medicine security 2024 | Higher inventory | Working capital +low‑double‑digit % | Govt contracts |

What is included in the product

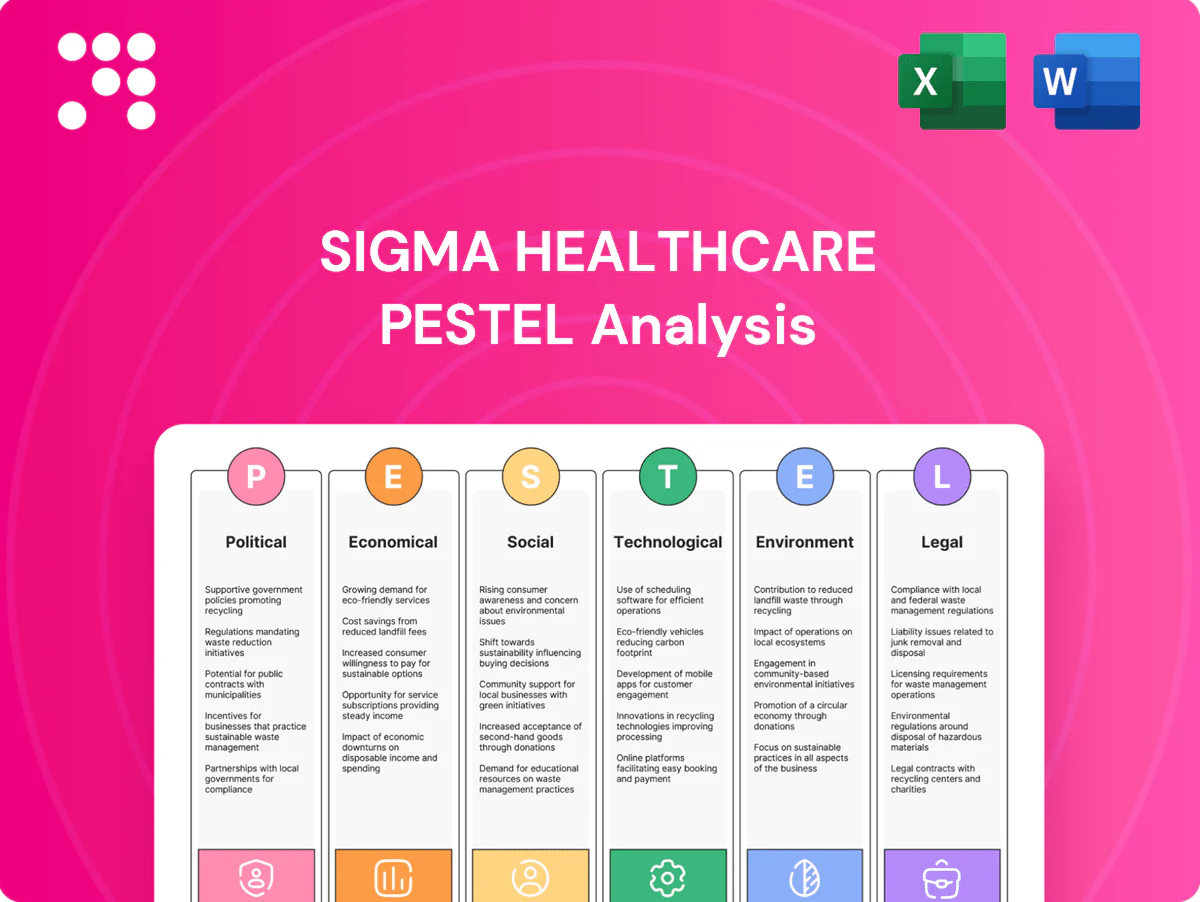

Explores how macro-environmental factors uniquely affect Sigma Healthcare across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed, region- and industry-specific analysis. Designed to help executives, investors and advisors identify risks, opportunities and scenario-driven strategic responses.

A concise, visually segmented Sigma Healthcare PESTLE summary that distills external risks and opportunities for rapid reference in meetings or presentations. Easily shared and editable for regional or business-line notes, it speeds alignment across teams and supports focused strategic planning.

Economic factors

Inflation and costs

Input inflation — with Australia CPI easing to about 3.5% in 2024 and nominal wage growth near 3.8% — lifts costs for wages, utilities, packaging and freight, squeezing pharmacy margins. Fuel price volatility, driven by 2023–24 crude swings, raises last‑mile and interstate linehaul costs unpredictably. Margin management therefore relies on scale efficiencies and disciplined price pass‑through. Continuous cost‑to‑serve optimisation remains critical to protect gross margins.

Consumer spending cycles

OTC and front‑of‑store sales at Sigma are highly sensitive to discretionary income; during 2024 softer consumer spending saw shifts toward value ranges, with private‑label penetration rising across Australian retail. Economic slowdowns typically move mix away from premium SKUs toward cheaper alternatives while script volumes remain relatively defensive, though average basket size can contract. Sigma’s banners, supporting c.1,500 pharmacies and reporting group revenue near AUD3.9bn in FY24, can lean into promotions and loyalty to protect share.

Interest rates and working capital

Higher interest rates (around 4% in mid-2025) raise inventory carrying costs across Sigma Healthcare’s national DC network, increasing financing needs and working capital days. Extended supplier terms and rising pharmacy credit risk compress cash flow, evident in industry-wide receivable pressures. Efficient SKU rationalization and improved demand forecasting, plus treasury discipline and securitization of receivables, can reduce funding costs and free cash.

Currency and import exposure

Depreciating AUD (around USD0.66 in mid‑2025) raises landed costs for imported medicines and OTCs, pressuring gross margins; Sigma’s hedging programs smooth short‑term COGS volatility but cannot offset sustained currency-driven price increases. Pharmacy contract pricing windows need explicit FX pass‑through clauses to avoid margin erosion, while active supplier renegotiation and alternative sourcing reduce import cost pressure.

- FX rate mid‑2025: ~USD0.66

- Hedging: reduces volatility, not structural shifts

- Contracts: require FX pass‑through

- Sourcing: supplier talks/alternates lower risk

Industry consolidation

Pharmacy group mergers shift bargaining power and demand broader service offerings; Chemist Warehouse holds about 30% of Australian pharmacy sales (Roy Morgan 2023). Rising hospital outsourcing and 3PL arrangements are reshaping account structures and contract terms. Scale can lift Sigma’s network utilization and tech ROI, but vigilance on churn risk and differentiated service tiers is essential.

- Consolidation: stronger buyer leverage

- 3PL shift: fewer, larger accounts

- Scale: improved utilization/ROI

- Risk: monitor churn, tiered services

PBS spend anchors wholesale volumes while price cuts and medicine‑security lift working capital

Input inflation (Aust CPI ~3.5% in 2024) and nominal wage growth (~3.8%) squeeze margins while fuel and FX volatility (AUD/USD ~0.66 mid‑2025) raise landed costs; Sigma’s scale and hedging partially mitigate but cannot fully offset sustained pressures. Higher rates (~4% mid‑2025) lift inventory financing costs and working capital needs; consolidation (Chemist Warehouse ~30% 2023) increases buyer leverage.

| Metric | Value |

|---|---|

| Aust CPI 2024 | ~3.5% |

| Wage growth 2024 | ~3.8% |

| FY24 revenue | AUD 3.9bn |

| AUD/USD mid‑2025 | ~0.66 |

| Cash rate mid‑2025 | ~4% |

| CW share (Roy Morgan) | ~30% (2023) |

Preview Before You Purchase

Sigma Healthcare PESTLE Analysis

The Sigma Healthcare PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the final file, with no placeholders or teasers. After checkout you’ll instantly download this finished, professionally structured report.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Sigma Healthcare—three concise sections reveal how political shifts, economic pressures, and tech trends will shape growth and risk. Ideal for investors and strategists seeking actionable insights. Purchase the full report to access the complete, editable breakdown and make informed decisions today.

Political factors

PBS and pricing policy

Commonwealth PBS settings drive about 240 million scripts p.a. and roughly AUD 11 billion in government PBS spending, directly shaping Sigma’s wholesale volumes and margins.

Price disclosure and statutory price reductions have historically compressed distributor rebates and can shave percentage points off slim wholesale margins.

Policy shifts on co‑payments or 60‑day dispensing change order frequency and inventory turns, affecting working capital.

Sigma must pursue active policy advocacy and rapid contract and stocking model adjustments to protect margins and cash flow.

Community Pharmacy Agreements

Successive Community Pharmacy Agreements set remuneration, location rules and service funding within the multi-billion-dollar PBS framework, directly shaping pharmacy viability. Changes to CPA terms materially affect Sigma’s banner partners’ profitability and store footprint across thousands of community sites. Stability provides more predictable demand for wholesale and retail channels, while renegotiations create planning risk. Sigma reduces exposure through early scenario planning with banner owners.

Federal–state health priorities

Variations in state hospital funding and procurement policies drive institutional sales for Sigma, especially as Australia spends roughly 10% of GDP on health and serves ~26 million people. Federal emphasis on primary care and vaccination programs (millions vaccinated annually) increases service-led volumes. Political focus on regional health unlocks targeted grants for distribution resilience, and alignment with public health campaigns strengthens brand standing.

Supply chain sovereignty

Canberra’s 2024 push for medicine security prioritises local stockholding and strategic reserves, prompting incentives and possible mandates for higher safety stocks and real-time reporting that could increase working capital by an estimated low-double-digit percentage for distributors.

Higher inventory requirements may deepen customer ties as Sigma can market itself as a national resilience partner, leveraging its pharmacy network and logistics to capture government and retail contracts.

- policy: 2024 federal focus on medicine security

- impact: safety-stock rise → working capital up (low-double-digit %)

- opportunity: stronger ties with government & pharmacies

- positioning: Sigma as supply partner for national resilience

Trade and import dynamics

Free trade agreements and tariff settings materially affect Sigma Healthcare’s landed cost for generics and OTC lines, altering gross margins and retail pricing flexibility.

Geopolitical tensions and supply-chain disruptions in China and India have previously interrupted API and finished-goods flows, while export controls or domestic priority allocations can be triggered during shortages.

Diversified sourcing, inventory buffers and active policy engagement with regulators mitigate procurement shocks and protect continuity of supply.

- trade: FTAs/tariffs influence landed cost

- geopolitics: China/India supply risk

- controls: export/priority rules in shortages

- mitigation: diversification & policy engagement

PBS spend anchors wholesale volumes while price cuts and medicine‑security lift working capital

Commonwealth PBS (~AUD 11bn spend; ~240m scripts p.a.) drives Sigma’s wholesale volumes, margins and community pharmacy demand.

Price disclosure and statutory cuts compress distributor rebates, shaving points off already slim margins.

2024 medicine‑security push increases mandated safety stocks (estimated low‑double‑digit % rise in working capital) and reporting requirements.

State hospital procurement, FTAs and China/India supply risks affect landed costs and institutional sales, creating both risk and contracting opportunities.

| Policy | Impact | Data | Opportunity |

|---|---|---|---|

| PBS/CPA | Volume/margin | AUD 11bn; 240m scripts | Stable demand |

| Medicine security 2024 | Higher inventory | Working capital +low‑double‑digit % | Govt contracts |

What is included in the product

Explores how macro-environmental factors uniquely affect Sigma Healthcare across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed, region- and industry-specific analysis. Designed to help executives, investors and advisors identify risks, opportunities and scenario-driven strategic responses.

A concise, visually segmented Sigma Healthcare PESTLE summary that distills external risks and opportunities for rapid reference in meetings or presentations. Easily shared and editable for regional or business-line notes, it speeds alignment across teams and supports focused strategic planning.

Economic factors

Inflation and costs

Input inflation — with Australia CPI easing to about 3.5% in 2024 and nominal wage growth near 3.8% — lifts costs for wages, utilities, packaging and freight, squeezing pharmacy margins. Fuel price volatility, driven by 2023–24 crude swings, raises last‑mile and interstate linehaul costs unpredictably. Margin management therefore relies on scale efficiencies and disciplined price pass‑through. Continuous cost‑to‑serve optimisation remains critical to protect gross margins.

Consumer spending cycles

OTC and front‑of‑store sales at Sigma are highly sensitive to discretionary income; during 2024 softer consumer spending saw shifts toward value ranges, with private‑label penetration rising across Australian retail. Economic slowdowns typically move mix away from premium SKUs toward cheaper alternatives while script volumes remain relatively defensive, though average basket size can contract. Sigma’s banners, supporting c.1,500 pharmacies and reporting group revenue near AUD3.9bn in FY24, can lean into promotions and loyalty to protect share.

Interest rates and working capital

Higher interest rates (around 4% in mid-2025) raise inventory carrying costs across Sigma Healthcare’s national DC network, increasing financing needs and working capital days. Extended supplier terms and rising pharmacy credit risk compress cash flow, evident in industry-wide receivable pressures. Efficient SKU rationalization and improved demand forecasting, plus treasury discipline and securitization of receivables, can reduce funding costs and free cash.

Currency and import exposure

Depreciating AUD (around USD0.66 in mid‑2025) raises landed costs for imported medicines and OTCs, pressuring gross margins; Sigma’s hedging programs smooth short‑term COGS volatility but cannot offset sustained currency-driven price increases. Pharmacy contract pricing windows need explicit FX pass‑through clauses to avoid margin erosion, while active supplier renegotiation and alternative sourcing reduce import cost pressure.

- FX rate mid‑2025: ~USD0.66

- Hedging: reduces volatility, not structural shifts

- Contracts: require FX pass‑through

- Sourcing: supplier talks/alternates lower risk

Industry consolidation

Pharmacy group mergers shift bargaining power and demand broader service offerings; Chemist Warehouse holds about 30% of Australian pharmacy sales (Roy Morgan 2023). Rising hospital outsourcing and 3PL arrangements are reshaping account structures and contract terms. Scale can lift Sigma’s network utilization and tech ROI, but vigilance on churn risk and differentiated service tiers is essential.

- Consolidation: stronger buyer leverage

- 3PL shift: fewer, larger accounts

- Scale: improved utilization/ROI

- Risk: monitor churn, tiered services

PBS spend anchors wholesale volumes while price cuts and medicine‑security lift working capital

Input inflation (Aust CPI ~3.5% in 2024) and nominal wage growth (~3.8%) squeeze margins while fuel and FX volatility (AUD/USD ~0.66 mid‑2025) raise landed costs; Sigma’s scale and hedging partially mitigate but cannot fully offset sustained pressures. Higher rates (~4% mid‑2025) lift inventory financing costs and working capital needs; consolidation (Chemist Warehouse ~30% 2023) increases buyer leverage.

| Metric | Value |

|---|---|

| Aust CPI 2024 | ~3.5% |

| Wage growth 2024 | ~3.8% |

| FY24 revenue | AUD 3.9bn |

| AUD/USD mid‑2025 | ~0.66 |

| Cash rate mid‑2025 | ~4% |

| CW share (Roy Morgan) | ~30% (2023) |

Preview Before You Purchase

Sigma Healthcare PESTLE Analysis

The Sigma Healthcare PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the final file, with no placeholders or teasers. After checkout you’ll instantly download this finished, professionally structured report.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Sigma Healthcare—three concise sections reveal how political shifts, economic pressures, and tech trends will shape growth and risk. Ideal for investors and strategists seeking actionable insights. Purchase the full report to access the complete, editable breakdown and make informed decisions today.

Political factors

PBS and pricing policy

Commonwealth PBS settings drive about 240 million scripts p.a. and roughly AUD 11 billion in government PBS spending, directly shaping Sigma’s wholesale volumes and margins.

Price disclosure and statutory price reductions have historically compressed distributor rebates and can shave percentage points off slim wholesale margins.

Policy shifts on co‑payments or 60‑day dispensing change order frequency and inventory turns, affecting working capital.

Sigma must pursue active policy advocacy and rapid contract and stocking model adjustments to protect margins and cash flow.

Community Pharmacy Agreements

Successive Community Pharmacy Agreements set remuneration, location rules and service funding within the multi-billion-dollar PBS framework, directly shaping pharmacy viability. Changes to CPA terms materially affect Sigma’s banner partners’ profitability and store footprint across thousands of community sites. Stability provides more predictable demand for wholesale and retail channels, while renegotiations create planning risk. Sigma reduces exposure through early scenario planning with banner owners.

Federal–state health priorities

Variations in state hospital funding and procurement policies drive institutional sales for Sigma, especially as Australia spends roughly 10% of GDP on health and serves ~26 million people. Federal emphasis on primary care and vaccination programs (millions vaccinated annually) increases service-led volumes. Political focus on regional health unlocks targeted grants for distribution resilience, and alignment with public health campaigns strengthens brand standing.

Supply chain sovereignty

Canberra’s 2024 push for medicine security prioritises local stockholding and strategic reserves, prompting incentives and possible mandates for higher safety stocks and real-time reporting that could increase working capital by an estimated low-double-digit percentage for distributors.

Higher inventory requirements may deepen customer ties as Sigma can market itself as a national resilience partner, leveraging its pharmacy network and logistics to capture government and retail contracts.

- policy: 2024 federal focus on medicine security

- impact: safety-stock rise → working capital up (low-double-digit %)

- opportunity: stronger ties with government & pharmacies

- positioning: Sigma as supply partner for national resilience

Trade and import dynamics

Free trade agreements and tariff settings materially affect Sigma Healthcare’s landed cost for generics and OTC lines, altering gross margins and retail pricing flexibility.

Geopolitical tensions and supply-chain disruptions in China and India have previously interrupted API and finished-goods flows, while export controls or domestic priority allocations can be triggered during shortages.

Diversified sourcing, inventory buffers and active policy engagement with regulators mitigate procurement shocks and protect continuity of supply.

- trade: FTAs/tariffs influence landed cost

- geopolitics: China/India supply risk

- controls: export/priority rules in shortages

- mitigation: diversification & policy engagement

PBS spend anchors wholesale volumes while price cuts and medicine‑security lift working capital

Commonwealth PBS (~AUD 11bn spend; ~240m scripts p.a.) drives Sigma’s wholesale volumes, margins and community pharmacy demand.

Price disclosure and statutory cuts compress distributor rebates, shaving points off already slim margins.

2024 medicine‑security push increases mandated safety stocks (estimated low‑double‑digit % rise in working capital) and reporting requirements.

State hospital procurement, FTAs and China/India supply risks affect landed costs and institutional sales, creating both risk and contracting opportunities.

| Policy | Impact | Data | Opportunity |

|---|---|---|---|

| PBS/CPA | Volume/margin | AUD 11bn; 240m scripts | Stable demand |

| Medicine security 2024 | Higher inventory | Working capital +low‑double‑digit % | Govt contracts |

What is included in the product

Explores how macro-environmental factors uniquely affect Sigma Healthcare across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed, region- and industry-specific analysis. Designed to help executives, investors and advisors identify risks, opportunities and scenario-driven strategic responses.

A concise, visually segmented Sigma Healthcare PESTLE summary that distills external risks and opportunities for rapid reference in meetings or presentations. Easily shared and editable for regional or business-line notes, it speeds alignment across teams and supports focused strategic planning.

Economic factors

Inflation and costs

Input inflation — with Australia CPI easing to about 3.5% in 2024 and nominal wage growth near 3.8% — lifts costs for wages, utilities, packaging and freight, squeezing pharmacy margins. Fuel price volatility, driven by 2023–24 crude swings, raises last‑mile and interstate linehaul costs unpredictably. Margin management therefore relies on scale efficiencies and disciplined price pass‑through. Continuous cost‑to‑serve optimisation remains critical to protect gross margins.

Consumer spending cycles

OTC and front‑of‑store sales at Sigma are highly sensitive to discretionary income; during 2024 softer consumer spending saw shifts toward value ranges, with private‑label penetration rising across Australian retail. Economic slowdowns typically move mix away from premium SKUs toward cheaper alternatives while script volumes remain relatively defensive, though average basket size can contract. Sigma’s banners, supporting c.1,500 pharmacies and reporting group revenue near AUD3.9bn in FY24, can lean into promotions and loyalty to protect share.

Interest rates and working capital

Higher interest rates (around 4% in mid-2025) raise inventory carrying costs across Sigma Healthcare’s national DC network, increasing financing needs and working capital days. Extended supplier terms and rising pharmacy credit risk compress cash flow, evident in industry-wide receivable pressures. Efficient SKU rationalization and improved demand forecasting, plus treasury discipline and securitization of receivables, can reduce funding costs and free cash.

Currency and import exposure

Depreciating AUD (around USD0.66 in mid‑2025) raises landed costs for imported medicines and OTCs, pressuring gross margins; Sigma’s hedging programs smooth short‑term COGS volatility but cannot offset sustained currency-driven price increases. Pharmacy contract pricing windows need explicit FX pass‑through clauses to avoid margin erosion, while active supplier renegotiation and alternative sourcing reduce import cost pressure.

- FX rate mid‑2025: ~USD0.66

- Hedging: reduces volatility, not structural shifts

- Contracts: require FX pass‑through

- Sourcing: supplier talks/alternates lower risk

Industry consolidation

Pharmacy group mergers shift bargaining power and demand broader service offerings; Chemist Warehouse holds about 30% of Australian pharmacy sales (Roy Morgan 2023). Rising hospital outsourcing and 3PL arrangements are reshaping account structures and contract terms. Scale can lift Sigma’s network utilization and tech ROI, but vigilance on churn risk and differentiated service tiers is essential.

- Consolidation: stronger buyer leverage

- 3PL shift: fewer, larger accounts

- Scale: improved utilization/ROI

- Risk: monitor churn, tiered services

PBS spend anchors wholesale volumes while price cuts and medicine‑security lift working capital

Input inflation (Aust CPI ~3.5% in 2024) and nominal wage growth (~3.8%) squeeze margins while fuel and FX volatility (AUD/USD ~0.66 mid‑2025) raise landed costs; Sigma’s scale and hedging partially mitigate but cannot fully offset sustained pressures. Higher rates (~4% mid‑2025) lift inventory financing costs and working capital needs; consolidation (Chemist Warehouse ~30% 2023) increases buyer leverage.

| Metric | Value |

|---|---|

| Aust CPI 2024 | ~3.5% |

| Wage growth 2024 | ~3.8% |

| FY24 revenue | AUD 3.9bn |

| AUD/USD mid‑2025 | ~0.66 |

| Cash rate mid‑2025 | ~4% |

| CW share (Roy Morgan) | ~30% (2023) |

Preview Before You Purchase

Sigma Healthcare PESTLE Analysis

The Sigma Healthcare PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the final file, with no placeholders or teasers. After checkout you’ll instantly download this finished, professionally structured report.