Sime Darby Porter's Five Forces Analysis

From Overview to Strategy Blueprint

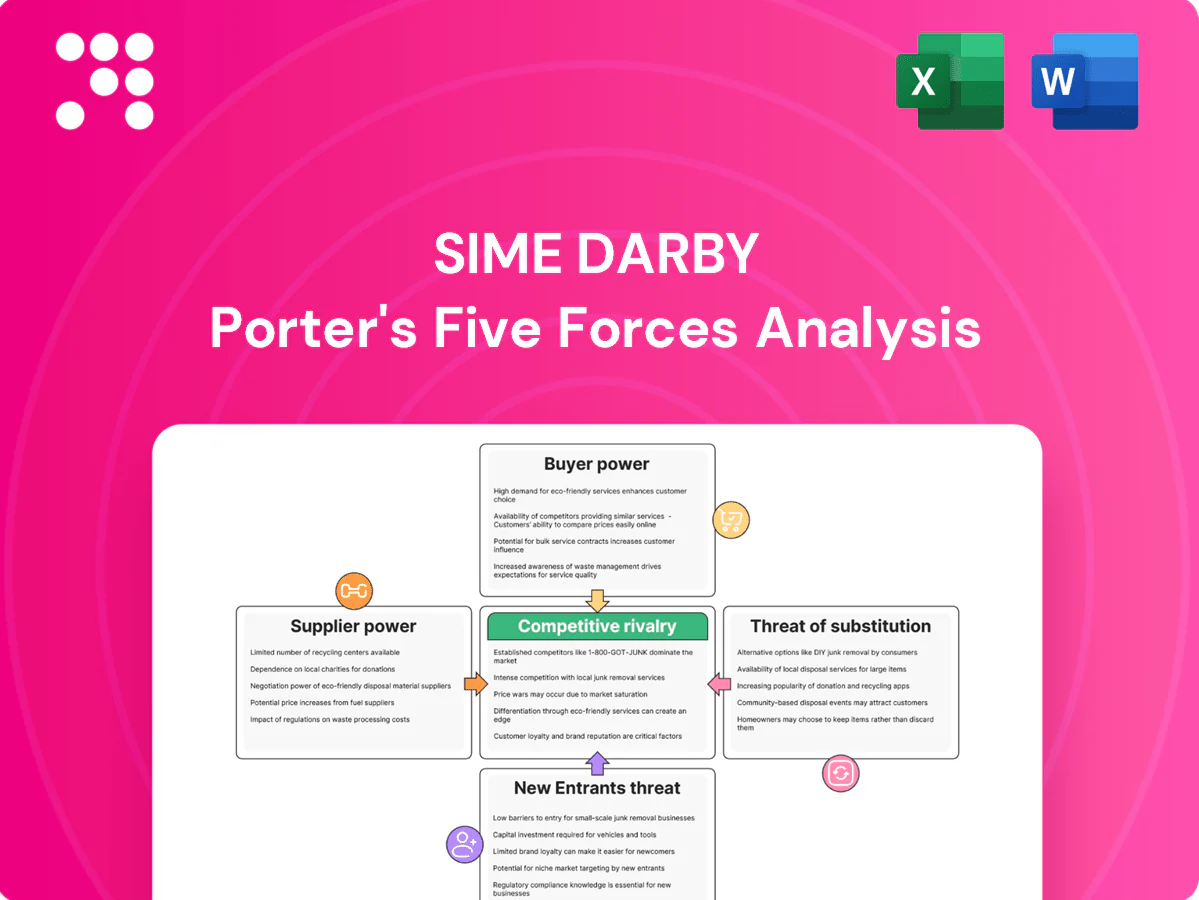

Sime Darby faces varied pressures—from concentrated supplier relationships and buyer bargaining to moderate threat of new entrants and substitutes amid asset-heavy logistics and diversified portfolios. Our snapshot highlights key competitive dynamics and strategic levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

OEM concentration is high

Sime Darby depends on a small set of powerful OEMs such as Caterpillar and major auto brands, limiting its ability to switch suppliers and increasing dependency risk.

Exclusive distributorships give OEMs leverage over pricing, territorial rights and product standards, constraining Sime Darby’s margin and commercial flexibility.

Contractual obligations often require Sime Darby to carry inventory, invest in tooling and provide OEM-led training, raising fixed costs and capital intensity across industrial and motors segments.

Brand-driven pricing power

Premium brands enforce minimum advertised pricing and price discipline, constraining Sime Darby dealer margin flexibility. OEM-controlled parts and service specifications preserve captive revenue streams and reduce local pricing autonomy. Warranty and recall policies are dictated upstream, keeping Sime Darby aligned with OEM pricing architectures; global automotive aftermarket valued at USD 419 billion in 2024.

Technology and parts dependency

Proprietary diagnostics, telematics and software lock-in force dependence on OEM updates and licenses, with software and services accounting for over 25% of OEM revenues in 2024, tightening lifecycle control. Genuine parts ecosystems restrict third-party sourcing, and as equipment electrifies and digitizes, supplier control over batteries, power electronics and telematics modules rises, strengthening supplier power over lifecycle economics.

Volume rebates and allocation

OEMs deploy tiered incentives, allocations and model availability to steer dealer behavior, tying access to high-demand units to sales mix and CSI targets in 2024.

In tight supply periods allocation served as a bargaining lever, shifting deliveries across dealer networks and prioritizing those meeting OEM metrics.

Dealers reported margin pressure during demand peaks, with allocation-driven mix changes compressing profitability by an estimated 3–5 percentage points in some markets.

- Allocation reliance

- CSI-linked access

- Tiered rebates

- 3–5pp margin squeeze

Geographic exclusivity trade-offs

Exclusive territories give Sime Darby local protection but concentrate dependence on a single supplier per brand, creating supplier-specific operational risk; renegotiation risk persists at contract renewal (typically every 3–7 years in port concession cycles as of 2024). Compliance with brand CI and capex standards increases capex intensity and limits supplier switching, so the trade-off exchanges market access for structural supplier clout.

- Supplier dependence: single-supplier per brand raises concentration risk

- Renegotiation cadence: 3–7 years (2024 industry norm) drives price/leverage exposure

- Ongoing CI/capex: raises switching costs and strengthens supplier bargaining power

OEM lock-in drives concentration risk and 3–5pp dealer margin squeeze

Sime Darby depends on a few powerful OEMs (eg Caterpillar, major auto brands), limiting switching and raising concentration risk. Exclusive distributorships, CI/capex and allocations constrain pricing and compressed dealer margins by ~3–5pp. OEM lock-in rises as software/services ≈25% of OEM revenue (2024) and global aftermarket ≈USD 419bn (2024). Renegotiations typically occur every 3–7 years.

| Metric | 2024 value | Impact |

|---|---|---|

| OEM software/services | ≈25% | Lifecycle lock-in |

| Automotive aftermarket | USD 419bn | Captive revenue |

| Margin squeeze | 3–5pp | Profit compression |

| Renegotiation cadence | 3–7 yrs | Leverage timing |

What is included in the product

Tailored Porter's Five Forces analysis for Sime Darby uncovering key drivers of competition, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and disruptive threats and substitutes that challenge its market position.

A concise one-sheet Porter’s Five Forces for Sime Darby—visual spider chart and customizable pressure levels relieve decision fatigue by instantly highlighting competitive intensity, with clean, deck-ready layouts for boardrooms or investor packs.

Customers Bargaining Power

Large fleet buyers negotiate hard

Mining, construction, plantations and government fleets aggregate demand through tenders that commonly bundle 100+ units and multi-year contracts (typically 3–5 years), squeezing suppliers on price and uptime; buyers routinely extract discounts in the 5–15% range and demand strict SLA and availability guarantees. Multi-year maintenance deals become battlegrounds where volume and service commitments determine margins, amplifying buyer power in industrial equipment markets.

Retail auto buyers are price-aware

Online listings and financing tools have made pricing highly transparent, with over 70% of buyers researching vehicles online in 2024, tightening negotiation room for Sime Darby Motors. Cross-shopping across brands and dealers compresses margins as shoppers compare offers in real time. Trade-in valuations and bundled servicing increasingly act as levers in deals. Although fragmented, widespread information access raises customer bargaining power.

Lifecycle TCO focus

Industrial buyers now drive a lifecycle TCO focus, scrutinizing fuel, parts and downtime and often deferring purchases, choosing used or rental options or stretching maintenance to cut costs; data-driven TCO comparisons amplify pricing pressure on new units and aftersales, elevating buyer leverage well beyond the sticker price.

Financing and bundled solutions

Buyers increasingly use captive and third-party financing to pressure Sime Darby on headline rates and value-added concessions, shifting leverage into the buyer's hands during negotiations.

Bundled warranties, telematics and maintenance contracts are routinely requested as trade-offs, allowing customers to extract non-price concessions and lower total cost of ownership.

Competitive financing offers frequently swing deals across brands, amplifying buyer influence at the deal-structuring stage.

- Financing leverage

- Bundled services

- Telematics & maintenance

- Deal-switching power

Switching across brands and channels

For Sime Darby, switching is easy: Komatsu, Volvo CE and Hitachi remain among the top global suppliers in 2024, while Chinese OEMs such as SANY and XCMG expanded export presence, giving buyers credible alternatives.

In autos, multi-brand showrooms and surge in online used-car platforms broaden choices; customers also shift to rentals or independent workshops after warranty, strengthening buyer leverage across the asset lifecycle.

- Multiple top-tier CE brands present in 2024

- Chinese OEMs increasing export share

- Used-car platforms expanding buyer options

- Post-warranty rental/independent workshop switching

Buyers have leverage: 70% research, 5–15% discounts

Buyers wield strong leverage: industrial tenders (3–5 year bundles) extract 5–15% discounts and strict SLAs, while 2024 data shows over 70% of buyers research online, enabling cross-shopping and deal-switching. Lifecycle TCO, bundled warranties, telematics and captive/third-party financing shift negotiations toward customers, amplified by credible alternatives (Komatsu, Volvo CE, Hitachi, SANY, XCMG).

| Metric | 2024 Value |

|---|---|

| Online research | 70%+ |

| Typical discounts | 5–15% |

| Contract length | 3–5 years |

| Key alternatives | Komatsu, Volvo CE, Hitachi, SANY, XCMG |

Preview the Actual Deliverable

Sime Darby Porter's Five Forces Analysis

This preview shows the exact Sime Darby Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted, comprehensive and ready for immediate download and use. Completing your purchase grants instant access to this identical file.

From Overview to Strategy Blueprint

Sime Darby faces varied pressures—from concentrated supplier relationships and buyer bargaining to moderate threat of new entrants and substitutes amid asset-heavy logistics and diversified portfolios. Our snapshot highlights key competitive dynamics and strategic levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

OEM concentration is high

Sime Darby depends on a small set of powerful OEMs such as Caterpillar and major auto brands, limiting its ability to switch suppliers and increasing dependency risk.

Exclusive distributorships give OEMs leverage over pricing, territorial rights and product standards, constraining Sime Darby’s margin and commercial flexibility.

Contractual obligations often require Sime Darby to carry inventory, invest in tooling and provide OEM-led training, raising fixed costs and capital intensity across industrial and motors segments.

Brand-driven pricing power

Premium brands enforce minimum advertised pricing and price discipline, constraining Sime Darby dealer margin flexibility. OEM-controlled parts and service specifications preserve captive revenue streams and reduce local pricing autonomy. Warranty and recall policies are dictated upstream, keeping Sime Darby aligned with OEM pricing architectures; global automotive aftermarket valued at USD 419 billion in 2024.

Technology and parts dependency

Proprietary diagnostics, telematics and software lock-in force dependence on OEM updates and licenses, with software and services accounting for over 25% of OEM revenues in 2024, tightening lifecycle control. Genuine parts ecosystems restrict third-party sourcing, and as equipment electrifies and digitizes, supplier control over batteries, power electronics and telematics modules rises, strengthening supplier power over lifecycle economics.

Volume rebates and allocation

OEMs deploy tiered incentives, allocations and model availability to steer dealer behavior, tying access to high-demand units to sales mix and CSI targets in 2024.

In tight supply periods allocation served as a bargaining lever, shifting deliveries across dealer networks and prioritizing those meeting OEM metrics.

Dealers reported margin pressure during demand peaks, with allocation-driven mix changes compressing profitability by an estimated 3–5 percentage points in some markets.

- Allocation reliance

- CSI-linked access

- Tiered rebates

- 3–5pp margin squeeze

Geographic exclusivity trade-offs

Exclusive territories give Sime Darby local protection but concentrate dependence on a single supplier per brand, creating supplier-specific operational risk; renegotiation risk persists at contract renewal (typically every 3–7 years in port concession cycles as of 2024). Compliance with brand CI and capex standards increases capex intensity and limits supplier switching, so the trade-off exchanges market access for structural supplier clout.

- Supplier dependence: single-supplier per brand raises concentration risk

- Renegotiation cadence: 3–7 years (2024 industry norm) drives price/leverage exposure

- Ongoing CI/capex: raises switching costs and strengthens supplier bargaining power

OEM lock-in drives concentration risk and 3–5pp dealer margin squeeze

Sime Darby depends on a few powerful OEMs (eg Caterpillar, major auto brands), limiting switching and raising concentration risk. Exclusive distributorships, CI/capex and allocations constrain pricing and compressed dealer margins by ~3–5pp. OEM lock-in rises as software/services ≈25% of OEM revenue (2024) and global aftermarket ≈USD 419bn (2024). Renegotiations typically occur every 3–7 years.

| Metric | 2024 value | Impact |

|---|---|---|

| OEM software/services | ≈25% | Lifecycle lock-in |

| Automotive aftermarket | USD 419bn | Captive revenue |

| Margin squeeze | 3–5pp | Profit compression |

| Renegotiation cadence | 3–7 yrs | Leverage timing |

What is included in the product

Tailored Porter's Five Forces analysis for Sime Darby uncovering key drivers of competition, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and disruptive threats and substitutes that challenge its market position.

A concise one-sheet Porter’s Five Forces for Sime Darby—visual spider chart and customizable pressure levels relieve decision fatigue by instantly highlighting competitive intensity, with clean, deck-ready layouts for boardrooms or investor packs.

Customers Bargaining Power

Large fleet buyers negotiate hard

Mining, construction, plantations and government fleets aggregate demand through tenders that commonly bundle 100+ units and multi-year contracts (typically 3–5 years), squeezing suppliers on price and uptime; buyers routinely extract discounts in the 5–15% range and demand strict SLA and availability guarantees. Multi-year maintenance deals become battlegrounds where volume and service commitments determine margins, amplifying buyer power in industrial equipment markets.

Retail auto buyers are price-aware

Online listings and financing tools have made pricing highly transparent, with over 70% of buyers researching vehicles online in 2024, tightening negotiation room for Sime Darby Motors. Cross-shopping across brands and dealers compresses margins as shoppers compare offers in real time. Trade-in valuations and bundled servicing increasingly act as levers in deals. Although fragmented, widespread information access raises customer bargaining power.

Lifecycle TCO focus

Industrial buyers now drive a lifecycle TCO focus, scrutinizing fuel, parts and downtime and often deferring purchases, choosing used or rental options or stretching maintenance to cut costs; data-driven TCO comparisons amplify pricing pressure on new units and aftersales, elevating buyer leverage well beyond the sticker price.

Financing and bundled solutions

Buyers increasingly use captive and third-party financing to pressure Sime Darby on headline rates and value-added concessions, shifting leverage into the buyer's hands during negotiations.

Bundled warranties, telematics and maintenance contracts are routinely requested as trade-offs, allowing customers to extract non-price concessions and lower total cost of ownership.

Competitive financing offers frequently swing deals across brands, amplifying buyer influence at the deal-structuring stage.

- Financing leverage

- Bundled services

- Telematics & maintenance

- Deal-switching power

Switching across brands and channels

For Sime Darby, switching is easy: Komatsu, Volvo CE and Hitachi remain among the top global suppliers in 2024, while Chinese OEMs such as SANY and XCMG expanded export presence, giving buyers credible alternatives.

In autos, multi-brand showrooms and surge in online used-car platforms broaden choices; customers also shift to rentals or independent workshops after warranty, strengthening buyer leverage across the asset lifecycle.

- Multiple top-tier CE brands present in 2024

- Chinese OEMs increasing export share

- Used-car platforms expanding buyer options

- Post-warranty rental/independent workshop switching

Buyers have leverage: 70% research, 5–15% discounts

Buyers wield strong leverage: industrial tenders (3–5 year bundles) extract 5–15% discounts and strict SLAs, while 2024 data shows over 70% of buyers research online, enabling cross-shopping and deal-switching. Lifecycle TCO, bundled warranties, telematics and captive/third-party financing shift negotiations toward customers, amplified by credible alternatives (Komatsu, Volvo CE, Hitachi, SANY, XCMG).

| Metric | 2024 Value |

|---|---|

| Online research | 70%+ |

| Typical discounts | 5–15% |

| Contract length | 3–5 years |

| Key alternatives | Komatsu, Volvo CE, Hitachi, SANY, XCMG |

Preview the Actual Deliverable

Sime Darby Porter's Five Forces Analysis

This preview shows the exact Sime Darby Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted, comprehensive and ready for immediate download and use. Completing your purchase grants instant access to this identical file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Sime Darby faces varied pressures—from concentrated supplier relationships and buyer bargaining to moderate threat of new entrants and substitutes amid asset-heavy logistics and diversified portfolios. Our snapshot highlights key competitive dynamics and strategic levers. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore detailed ratings, visuals, and actionable insights.

Suppliers Bargaining Power

OEM concentration is high

Sime Darby depends on a small set of powerful OEMs such as Caterpillar and major auto brands, limiting its ability to switch suppliers and increasing dependency risk.

Exclusive distributorships give OEMs leverage over pricing, territorial rights and product standards, constraining Sime Darby’s margin and commercial flexibility.

Contractual obligations often require Sime Darby to carry inventory, invest in tooling and provide OEM-led training, raising fixed costs and capital intensity across industrial and motors segments.

Brand-driven pricing power

Premium brands enforce minimum advertised pricing and price discipline, constraining Sime Darby dealer margin flexibility. OEM-controlled parts and service specifications preserve captive revenue streams and reduce local pricing autonomy. Warranty and recall policies are dictated upstream, keeping Sime Darby aligned with OEM pricing architectures; global automotive aftermarket valued at USD 419 billion in 2024.

Technology and parts dependency

Proprietary diagnostics, telematics and software lock-in force dependence on OEM updates and licenses, with software and services accounting for over 25% of OEM revenues in 2024, tightening lifecycle control. Genuine parts ecosystems restrict third-party sourcing, and as equipment electrifies and digitizes, supplier control over batteries, power electronics and telematics modules rises, strengthening supplier power over lifecycle economics.

Volume rebates and allocation

OEMs deploy tiered incentives, allocations and model availability to steer dealer behavior, tying access to high-demand units to sales mix and CSI targets in 2024.

In tight supply periods allocation served as a bargaining lever, shifting deliveries across dealer networks and prioritizing those meeting OEM metrics.

Dealers reported margin pressure during demand peaks, with allocation-driven mix changes compressing profitability by an estimated 3–5 percentage points in some markets.

- Allocation reliance

- CSI-linked access

- Tiered rebates

- 3–5pp margin squeeze

Geographic exclusivity trade-offs

Exclusive territories give Sime Darby local protection but concentrate dependence on a single supplier per brand, creating supplier-specific operational risk; renegotiation risk persists at contract renewal (typically every 3–7 years in port concession cycles as of 2024). Compliance with brand CI and capex standards increases capex intensity and limits supplier switching, so the trade-off exchanges market access for structural supplier clout.

- Supplier dependence: single-supplier per brand raises concentration risk

- Renegotiation cadence: 3–7 years (2024 industry norm) drives price/leverage exposure

- Ongoing CI/capex: raises switching costs and strengthens supplier bargaining power

OEM lock-in drives concentration risk and 3–5pp dealer margin squeeze

Sime Darby depends on a few powerful OEMs (eg Caterpillar, major auto brands), limiting switching and raising concentration risk. Exclusive distributorships, CI/capex and allocations constrain pricing and compressed dealer margins by ~3–5pp. OEM lock-in rises as software/services ≈25% of OEM revenue (2024) and global aftermarket ≈USD 419bn (2024). Renegotiations typically occur every 3–7 years.

| Metric | 2024 value | Impact |

|---|---|---|

| OEM software/services | ≈25% | Lifecycle lock-in |

| Automotive aftermarket | USD 419bn | Captive revenue |

| Margin squeeze | 3–5pp | Profit compression |

| Renegotiation cadence | 3–7 yrs | Leverage timing |

What is included in the product

Tailored Porter's Five Forces analysis for Sime Darby uncovering key drivers of competition, supplier and buyer influence on pricing and profitability, barriers deterring new entrants, and disruptive threats and substitutes that challenge its market position.

A concise one-sheet Porter’s Five Forces for Sime Darby—visual spider chart and customizable pressure levels relieve decision fatigue by instantly highlighting competitive intensity, with clean, deck-ready layouts for boardrooms or investor packs.

Customers Bargaining Power

Large fleet buyers negotiate hard

Mining, construction, plantations and government fleets aggregate demand through tenders that commonly bundle 100+ units and multi-year contracts (typically 3–5 years), squeezing suppliers on price and uptime; buyers routinely extract discounts in the 5–15% range and demand strict SLA and availability guarantees. Multi-year maintenance deals become battlegrounds where volume and service commitments determine margins, amplifying buyer power in industrial equipment markets.

Retail auto buyers are price-aware

Online listings and financing tools have made pricing highly transparent, with over 70% of buyers researching vehicles online in 2024, tightening negotiation room for Sime Darby Motors. Cross-shopping across brands and dealers compresses margins as shoppers compare offers in real time. Trade-in valuations and bundled servicing increasingly act as levers in deals. Although fragmented, widespread information access raises customer bargaining power.

Lifecycle TCO focus

Industrial buyers now drive a lifecycle TCO focus, scrutinizing fuel, parts and downtime and often deferring purchases, choosing used or rental options or stretching maintenance to cut costs; data-driven TCO comparisons amplify pricing pressure on new units and aftersales, elevating buyer leverage well beyond the sticker price.

Financing and bundled solutions

Buyers increasingly use captive and third-party financing to pressure Sime Darby on headline rates and value-added concessions, shifting leverage into the buyer's hands during negotiations.

Bundled warranties, telematics and maintenance contracts are routinely requested as trade-offs, allowing customers to extract non-price concessions and lower total cost of ownership.

Competitive financing offers frequently swing deals across brands, amplifying buyer influence at the deal-structuring stage.

- Financing leverage

- Bundled services

- Telematics & maintenance

- Deal-switching power

Switching across brands and channels

For Sime Darby, switching is easy: Komatsu, Volvo CE and Hitachi remain among the top global suppliers in 2024, while Chinese OEMs such as SANY and XCMG expanded export presence, giving buyers credible alternatives.

In autos, multi-brand showrooms and surge in online used-car platforms broaden choices; customers also shift to rentals or independent workshops after warranty, strengthening buyer leverage across the asset lifecycle.

- Multiple top-tier CE brands present in 2024

- Chinese OEMs increasing export share

- Used-car platforms expanding buyer options

- Post-warranty rental/independent workshop switching

Buyers have leverage: 70% research, 5–15% discounts

Buyers wield strong leverage: industrial tenders (3–5 year bundles) extract 5–15% discounts and strict SLAs, while 2024 data shows over 70% of buyers research online, enabling cross-shopping and deal-switching. Lifecycle TCO, bundled warranties, telematics and captive/third-party financing shift negotiations toward customers, amplified by credible alternatives (Komatsu, Volvo CE, Hitachi, SANY, XCMG).

| Metric | 2024 Value |

|---|---|

| Online research | 70%+ |

| Typical discounts | 5–15% |

| Contract length | 3–5 years |

| Key alternatives | Komatsu, Volvo CE, Hitachi, SANY, XCMG |

Preview the Actual Deliverable

Sime Darby Porter's Five Forces Analysis

This preview shows the exact Sime Darby Porter's Five Forces analysis you'll receive after purchase—no placeholders or mockups. The full document is professionally formatted, comprehensive and ready for immediate download and use. Completing your purchase grants instant access to this identical file.