Simmons Bank Business Model Canvas

Bank Strategic Blueprint: Business Model Canvas with Editable Word & Excel Downloads

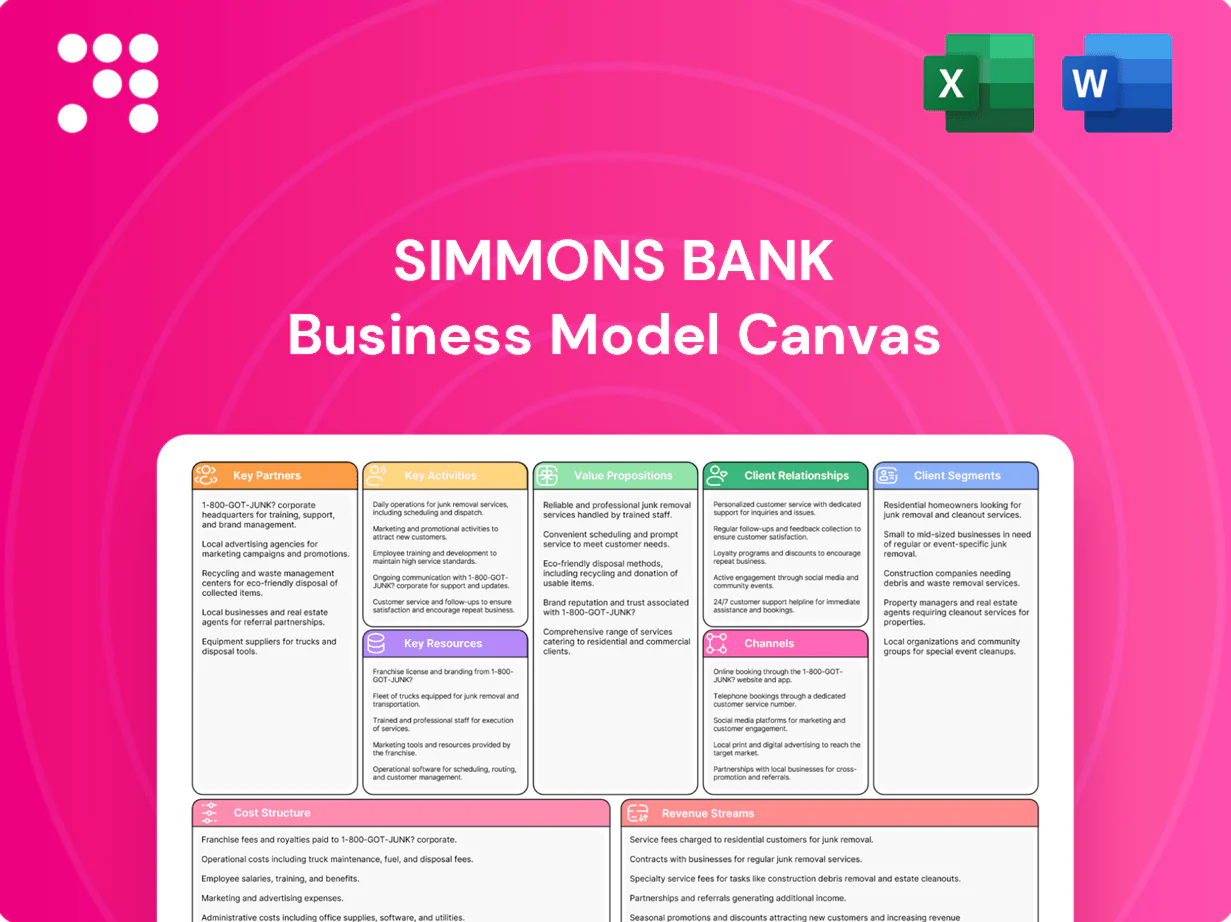

Unlock Simmons Bank's strategic blueprint with the full Business Model Canvas. This concise, company-specific canvas reveals value propositions, customer segments, revenue streams, and cost structure—ideal for investors, consultants, and founders. Download the editable Word & Excel files to benchmark, adapt, and act.

Partnerships

Payment networks and card processors

Partners like Visa and Mastercard and card processors enable issuance, acceptance and settlement, with the two networks accounting for over 80% of US card transaction volume in 2024; this scale expands merchant acceptance and drives interchange revenue for Simmons Bank. Co-brand and rewards partners lift card spend and retention. Robust SLAs and advanced fraud tools cut chargebacks and losses, protecting net fee income.

Core banking, fintech, and digital vendors

Core systems, cloud providers, and fintech integrations power Simmons Bank’s account servicing, digital banking, and payments, enabling real-time processing and mobile-first delivery. APIs accelerate feature rollout and lower unit costs, shortening integration cycles and supporting faster product launches. Cybersecurity and fraud partners mitigate risk—IBM reported a 2023 average data breach cost of $4.45 million—while vendor roadmaps enable scalability and regulatory change readiness.

Secondary market and mortgage investors

Agencies and private investors provided primary liquidity for mortgage originations, buying roughly 70% of loans in 2024 via whole-loan sales and securitizations, enabling Simmons Bank to convert originations to cash. Pipeline hedging partners manage rate risk on funded and forward-delivered loans, reducing margin volatility. Third-party servicing platforms handle post-close customer experience, and together these relationships stabilize margins across rate cycles.

SBA, USDA, and public program alliances

Simmons Bank leverages SBA, USDA and public program alliances to expand credit for small business and agriculture across its Mid-South footprint, reducing lender risk through government loan guarantees that lower loss severity and increase lending capacity. Preferred lender status accelerates approvals, deepening community impact and supporting regional economic resilience.

- SBA/USDA guarantees: lower credit loss

- Preferred lender: faster approvals

- Expanded capacity for small biz & ag lending

- Stronger Mid-South community impact

Community organizations and referral partners

Local chambers, realtors, auto dealers, and CPAs drive core lead flow for Simmons Bank, converting community referrals into deposit and loan relationships; financial education partners increase brand trust and improve inclusion; employer groups extend payroll services and HSA relationships, deepening product share; these networks anchor local market share and customer loyalty.

- referral channels: chambers, realtors, dealers, CPAs

- trust: financial education partners

- employee links: payroll & HSA via employers

- outcome: sustained local market share & loyalty

Card networks, cloud & APIs fuel payments; investors buy ~70% of loans

Card networks and processors (Visa/Mastercard >80% US card volume in 2024) drive acceptance and interchange. Core systems, cloud and fintech APIs enable real-time digital delivery while cybersecurity limits losses (avg breach cost $4.45M in 2023). Agencies/private buyers purchased ~70% of loans in 2024, and SBA/USDA guarantees expand small‑business and agricultural lending capacity.

| Partner | Role | 2024 metric |

|---|---|---|

| Visa/Mastercard | Acceptance, interchange | >80% US volume |

| Agencies/Investors | Liquidity | ~70% loans bought |

| SBA/USDA | Guaranteed lending | Preferred lender status |

| Cybersecurity vendors | Risk mitigation | Avg breach cost $4.45M (2023) |

What is included in the product

A comprehensive Business Model Canvas for Simmons Bank detailing customer segments, channels, value propositions, revenue and cost structures across the 9 classic BMC blocks, reflecting real-world operations and strategic priorities. Ideal for presentations, investor discussions and internal strategy with linked SWOT and competitive-advantage insights.

High-level view of Simmons Bank’s business model with editable cells, streamlining analysis and easing stakeholder alignment for faster decision-making.

Activities

Loan origination, underwriting, and portfolio management

Source, evaluate, and price real estate, commercial, and agricultural credits across origination channels, supporting a loan portfolio that totaled $18.2 billion as of year-end 2024; underwriting combines cash‑flow, collateral valuation, and covenant design to price risk-adjusted returns. Monitor collateral, covenants, and performance with monthly surveillance, adjust risk grades, and work out problem loans to keep nonperforming assets low (NPL ratio 0.45% in 2024). Optimize mix for yield, duration, and regulatory capital to target ROA/ROE and CET1 ratios aligned with supervisory guidance.

Deposit gathering and liquidity management

Simmons focuses on acquiring stable, low-cost consumer and commercial deposits to fund lending while navigating a 2024 fed funds range near 5.25–5.50%. Treasury manages cash, securities and contingent liquidity lines and monitors wholesale funding metrics; banks target LCR ≥100% under Basel III norms. Funds transfer pricing is optimized to align product-level profitability and transfer pricing signals. Stress testing ensures resiliency under severe scenarios.

Risk, compliance, and financial controls

Operate BSA/AML, KYC, and fraud-prevention frameworks tied to regulatory reporting and audit readiness, with model risk governance overseeing validation and scenario testing. Calibrate allowance for credit losses through portfolio-level stress testing and forward-looking metrics. Maintain robust lending and operations policies, periodic control reviews, and escalation protocols to ensure compliance and financial control.

Digital product development and operations

Digital product development focuses on enhancing online and mobile banking, payments, and card features while targeting 99.99% uptime, robust cybersecurity, and incident-response SLAs under 60 minutes; data analytics drive personalization and UX improvements with typical engagement uplifts near 15% and integration of fintech partners via secure APIs.

- 99.99% uptime target

- Incident response SLA under 60 minutes

- ~15% engagement uplift from personalization

- Secure API integrations with 25+ fintech partners

Relationship management and sales

- Client segments: retail, business, commercial, wealth

- Cross-sell: treasury, cards, advisory

- Approach: tailored pricing and proactive outreach

- Scale: ~300 branches; ~$60B assets (2024)

Real, commercial & ag lending: $18.2B loans, NPL 0.45%, assets $60B

Source, underwrite, and price real estate, commercial and ag loans; loan portfolio $18.2B (YE2024) with NPL 0.45%. Fund via low‑cost deposits; assets ~$60B and ~300 branches; manage liquidity (LCR≥100%) amid 2024 fed funds ~5.25–5.50%. Operate BSA/AML, stress testing, and digital ops (99.99% uptime, incident SLA <60m) with 25+ fintech integrations.

| Metric | 2024 |

|---|---|

| Loans | $18.2B |

| Assets | $60B |

| NPL | 0.45% |

| Branches | ~300 |

| Uptime | 99.99% |

| Incident SLA | <60m |

| Fintech partners | 25+ |

| Fed funds | 5.25–5.50% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Simmons Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview shows the real, editable file formatted for immediate use. Upon purchase you'll download the complete Word and Excel versions with all content intact.

Bank Strategic Blueprint: Business Model Canvas with Editable Word & Excel Downloads

Unlock Simmons Bank's strategic blueprint with the full Business Model Canvas. This concise, company-specific canvas reveals value propositions, customer segments, revenue streams, and cost structure—ideal for investors, consultants, and founders. Download the editable Word & Excel files to benchmark, adapt, and act.

Partnerships

Payment networks and card processors

Partners like Visa and Mastercard and card processors enable issuance, acceptance and settlement, with the two networks accounting for over 80% of US card transaction volume in 2024; this scale expands merchant acceptance and drives interchange revenue for Simmons Bank. Co-brand and rewards partners lift card spend and retention. Robust SLAs and advanced fraud tools cut chargebacks and losses, protecting net fee income.

Core banking, fintech, and digital vendors

Core systems, cloud providers, and fintech integrations power Simmons Bank’s account servicing, digital banking, and payments, enabling real-time processing and mobile-first delivery. APIs accelerate feature rollout and lower unit costs, shortening integration cycles and supporting faster product launches. Cybersecurity and fraud partners mitigate risk—IBM reported a 2023 average data breach cost of $4.45 million—while vendor roadmaps enable scalability and regulatory change readiness.

Secondary market and mortgage investors

Agencies and private investors provided primary liquidity for mortgage originations, buying roughly 70% of loans in 2024 via whole-loan sales and securitizations, enabling Simmons Bank to convert originations to cash. Pipeline hedging partners manage rate risk on funded and forward-delivered loans, reducing margin volatility. Third-party servicing platforms handle post-close customer experience, and together these relationships stabilize margins across rate cycles.

SBA, USDA, and public program alliances

Simmons Bank leverages SBA, USDA and public program alliances to expand credit for small business and agriculture across its Mid-South footprint, reducing lender risk through government loan guarantees that lower loss severity and increase lending capacity. Preferred lender status accelerates approvals, deepening community impact and supporting regional economic resilience.

- SBA/USDA guarantees: lower credit loss

- Preferred lender: faster approvals

- Expanded capacity for small biz & ag lending

- Stronger Mid-South community impact

Community organizations and referral partners

Local chambers, realtors, auto dealers, and CPAs drive core lead flow for Simmons Bank, converting community referrals into deposit and loan relationships; financial education partners increase brand trust and improve inclusion; employer groups extend payroll services and HSA relationships, deepening product share; these networks anchor local market share and customer loyalty.

- referral channels: chambers, realtors, dealers, CPAs

- trust: financial education partners

- employee links: payroll & HSA via employers

- outcome: sustained local market share & loyalty

Card networks, cloud & APIs fuel payments; investors buy ~70% of loans

Card networks and processors (Visa/Mastercard >80% US card volume in 2024) drive acceptance and interchange. Core systems, cloud and fintech APIs enable real-time digital delivery while cybersecurity limits losses (avg breach cost $4.45M in 2023). Agencies/private buyers purchased ~70% of loans in 2024, and SBA/USDA guarantees expand small‑business and agricultural lending capacity.

| Partner | Role | 2024 metric |

|---|---|---|

| Visa/Mastercard | Acceptance, interchange | >80% US volume |

| Agencies/Investors | Liquidity | ~70% loans bought |

| SBA/USDA | Guaranteed lending | Preferred lender status |

| Cybersecurity vendors | Risk mitigation | Avg breach cost $4.45M (2023) |

What is included in the product

A comprehensive Business Model Canvas for Simmons Bank detailing customer segments, channels, value propositions, revenue and cost structures across the 9 classic BMC blocks, reflecting real-world operations and strategic priorities. Ideal for presentations, investor discussions and internal strategy with linked SWOT and competitive-advantage insights.

High-level view of Simmons Bank’s business model with editable cells, streamlining analysis and easing stakeholder alignment for faster decision-making.

Activities

Loan origination, underwriting, and portfolio management

Source, evaluate, and price real estate, commercial, and agricultural credits across origination channels, supporting a loan portfolio that totaled $18.2 billion as of year-end 2024; underwriting combines cash‑flow, collateral valuation, and covenant design to price risk-adjusted returns. Monitor collateral, covenants, and performance with monthly surveillance, adjust risk grades, and work out problem loans to keep nonperforming assets low (NPL ratio 0.45% in 2024). Optimize mix for yield, duration, and regulatory capital to target ROA/ROE and CET1 ratios aligned with supervisory guidance.

Deposit gathering and liquidity management

Simmons focuses on acquiring stable, low-cost consumer and commercial deposits to fund lending while navigating a 2024 fed funds range near 5.25–5.50%. Treasury manages cash, securities and contingent liquidity lines and monitors wholesale funding metrics; banks target LCR ≥100% under Basel III norms. Funds transfer pricing is optimized to align product-level profitability and transfer pricing signals. Stress testing ensures resiliency under severe scenarios.

Risk, compliance, and financial controls

Operate BSA/AML, KYC, and fraud-prevention frameworks tied to regulatory reporting and audit readiness, with model risk governance overseeing validation and scenario testing. Calibrate allowance for credit losses through portfolio-level stress testing and forward-looking metrics. Maintain robust lending and operations policies, periodic control reviews, and escalation protocols to ensure compliance and financial control.

Digital product development and operations

Digital product development focuses on enhancing online and mobile banking, payments, and card features while targeting 99.99% uptime, robust cybersecurity, and incident-response SLAs under 60 minutes; data analytics drive personalization and UX improvements with typical engagement uplifts near 15% and integration of fintech partners via secure APIs.

- 99.99% uptime target

- Incident response SLA under 60 minutes

- ~15% engagement uplift from personalization

- Secure API integrations with 25+ fintech partners

Relationship management and sales

- Client segments: retail, business, commercial, wealth

- Cross-sell: treasury, cards, advisory

- Approach: tailored pricing and proactive outreach

- Scale: ~300 branches; ~$60B assets (2024)

Real, commercial & ag lending: $18.2B loans, NPL 0.45%, assets $60B

Source, underwrite, and price real estate, commercial and ag loans; loan portfolio $18.2B (YE2024) with NPL 0.45%. Fund via low‑cost deposits; assets ~$60B and ~300 branches; manage liquidity (LCR≥100%) amid 2024 fed funds ~5.25–5.50%. Operate BSA/AML, stress testing, and digital ops (99.99% uptime, incident SLA <60m) with 25+ fintech integrations.

| Metric | 2024 |

|---|---|

| Loans | $18.2B |

| Assets | $60B |

| NPL | 0.45% |

| Branches | ~300 |

| Uptime | 99.99% |

| Incident SLA | <60m |

| Fintech partners | 25+ |

| Fed funds | 5.25–5.50% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Simmons Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview shows the real, editable file formatted for immediate use. Upon purchase you'll download the complete Word and Excel versions with all content intact.

Original: $10.00

-65%$10.00

$3.50Description

Bank Strategic Blueprint: Business Model Canvas with Editable Word & Excel Downloads

Unlock Simmons Bank's strategic blueprint with the full Business Model Canvas. This concise, company-specific canvas reveals value propositions, customer segments, revenue streams, and cost structure—ideal for investors, consultants, and founders. Download the editable Word & Excel files to benchmark, adapt, and act.

Partnerships

Payment networks and card processors

Partners like Visa and Mastercard and card processors enable issuance, acceptance and settlement, with the two networks accounting for over 80% of US card transaction volume in 2024; this scale expands merchant acceptance and drives interchange revenue for Simmons Bank. Co-brand and rewards partners lift card spend and retention. Robust SLAs and advanced fraud tools cut chargebacks and losses, protecting net fee income.

Core banking, fintech, and digital vendors

Core systems, cloud providers, and fintech integrations power Simmons Bank’s account servicing, digital banking, and payments, enabling real-time processing and mobile-first delivery. APIs accelerate feature rollout and lower unit costs, shortening integration cycles and supporting faster product launches. Cybersecurity and fraud partners mitigate risk—IBM reported a 2023 average data breach cost of $4.45 million—while vendor roadmaps enable scalability and regulatory change readiness.

Secondary market and mortgage investors

Agencies and private investors provided primary liquidity for mortgage originations, buying roughly 70% of loans in 2024 via whole-loan sales and securitizations, enabling Simmons Bank to convert originations to cash. Pipeline hedging partners manage rate risk on funded and forward-delivered loans, reducing margin volatility. Third-party servicing platforms handle post-close customer experience, and together these relationships stabilize margins across rate cycles.

SBA, USDA, and public program alliances

Simmons Bank leverages SBA, USDA and public program alliances to expand credit for small business and agriculture across its Mid-South footprint, reducing lender risk through government loan guarantees that lower loss severity and increase lending capacity. Preferred lender status accelerates approvals, deepening community impact and supporting regional economic resilience.

- SBA/USDA guarantees: lower credit loss

- Preferred lender: faster approvals

- Expanded capacity for small biz & ag lending

- Stronger Mid-South community impact

Community organizations and referral partners

Local chambers, realtors, auto dealers, and CPAs drive core lead flow for Simmons Bank, converting community referrals into deposit and loan relationships; financial education partners increase brand trust and improve inclusion; employer groups extend payroll services and HSA relationships, deepening product share; these networks anchor local market share and customer loyalty.

- referral channels: chambers, realtors, dealers, CPAs

- trust: financial education partners

- employee links: payroll & HSA via employers

- outcome: sustained local market share & loyalty

Card networks, cloud & APIs fuel payments; investors buy ~70% of loans

Card networks and processors (Visa/Mastercard >80% US card volume in 2024) drive acceptance and interchange. Core systems, cloud and fintech APIs enable real-time digital delivery while cybersecurity limits losses (avg breach cost $4.45M in 2023). Agencies/private buyers purchased ~70% of loans in 2024, and SBA/USDA guarantees expand small‑business and agricultural lending capacity.

| Partner | Role | 2024 metric |

|---|---|---|

| Visa/Mastercard | Acceptance, interchange | >80% US volume |

| Agencies/Investors | Liquidity | ~70% loans bought |

| SBA/USDA | Guaranteed lending | Preferred lender status |

| Cybersecurity vendors | Risk mitigation | Avg breach cost $4.45M (2023) |

What is included in the product

A comprehensive Business Model Canvas for Simmons Bank detailing customer segments, channels, value propositions, revenue and cost structures across the 9 classic BMC blocks, reflecting real-world operations and strategic priorities. Ideal for presentations, investor discussions and internal strategy with linked SWOT and competitive-advantage insights.

High-level view of Simmons Bank’s business model with editable cells, streamlining analysis and easing stakeholder alignment for faster decision-making.

Activities

Loan origination, underwriting, and portfolio management

Source, evaluate, and price real estate, commercial, and agricultural credits across origination channels, supporting a loan portfolio that totaled $18.2 billion as of year-end 2024; underwriting combines cash‑flow, collateral valuation, and covenant design to price risk-adjusted returns. Monitor collateral, covenants, and performance with monthly surveillance, adjust risk grades, and work out problem loans to keep nonperforming assets low (NPL ratio 0.45% in 2024). Optimize mix for yield, duration, and regulatory capital to target ROA/ROE and CET1 ratios aligned with supervisory guidance.

Deposit gathering and liquidity management

Simmons focuses on acquiring stable, low-cost consumer and commercial deposits to fund lending while navigating a 2024 fed funds range near 5.25–5.50%. Treasury manages cash, securities and contingent liquidity lines and monitors wholesale funding metrics; banks target LCR ≥100% under Basel III norms. Funds transfer pricing is optimized to align product-level profitability and transfer pricing signals. Stress testing ensures resiliency under severe scenarios.

Risk, compliance, and financial controls

Operate BSA/AML, KYC, and fraud-prevention frameworks tied to regulatory reporting and audit readiness, with model risk governance overseeing validation and scenario testing. Calibrate allowance for credit losses through portfolio-level stress testing and forward-looking metrics. Maintain robust lending and operations policies, periodic control reviews, and escalation protocols to ensure compliance and financial control.

Digital product development and operations

Digital product development focuses on enhancing online and mobile banking, payments, and card features while targeting 99.99% uptime, robust cybersecurity, and incident-response SLAs under 60 minutes; data analytics drive personalization and UX improvements with typical engagement uplifts near 15% and integration of fintech partners via secure APIs.

- 99.99% uptime target

- Incident response SLA under 60 minutes

- ~15% engagement uplift from personalization

- Secure API integrations with 25+ fintech partners

Relationship management and sales

- Client segments: retail, business, commercial, wealth

- Cross-sell: treasury, cards, advisory

- Approach: tailored pricing and proactive outreach

- Scale: ~300 branches; ~$60B assets (2024)

Real, commercial & ag lending: $18.2B loans, NPL 0.45%, assets $60B

Source, underwrite, and price real estate, commercial and ag loans; loan portfolio $18.2B (YE2024) with NPL 0.45%. Fund via low‑cost deposits; assets ~$60B and ~300 branches; manage liquidity (LCR≥100%) amid 2024 fed funds ~5.25–5.50%. Operate BSA/AML, stress testing, and digital ops (99.99% uptime, incident SLA <60m) with 25+ fintech integrations.

| Metric | 2024 |

|---|---|

| Loans | $18.2B |

| Assets | $60B |

| NPL | 0.45% |

| Branches | ~300 |

| Uptime | 99.99% |

| Incident SLA | <60m |

| Fintech partners | 25+ |

| Fed funds | 5.25–5.50% |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the exact Simmons Bank Business Model Canvas you'll receive after purchase. It's not a mockup—this live preview shows the real, editable file formatted for immediate use. Upon purchase you'll download the complete Word and Excel versions with all content intact.