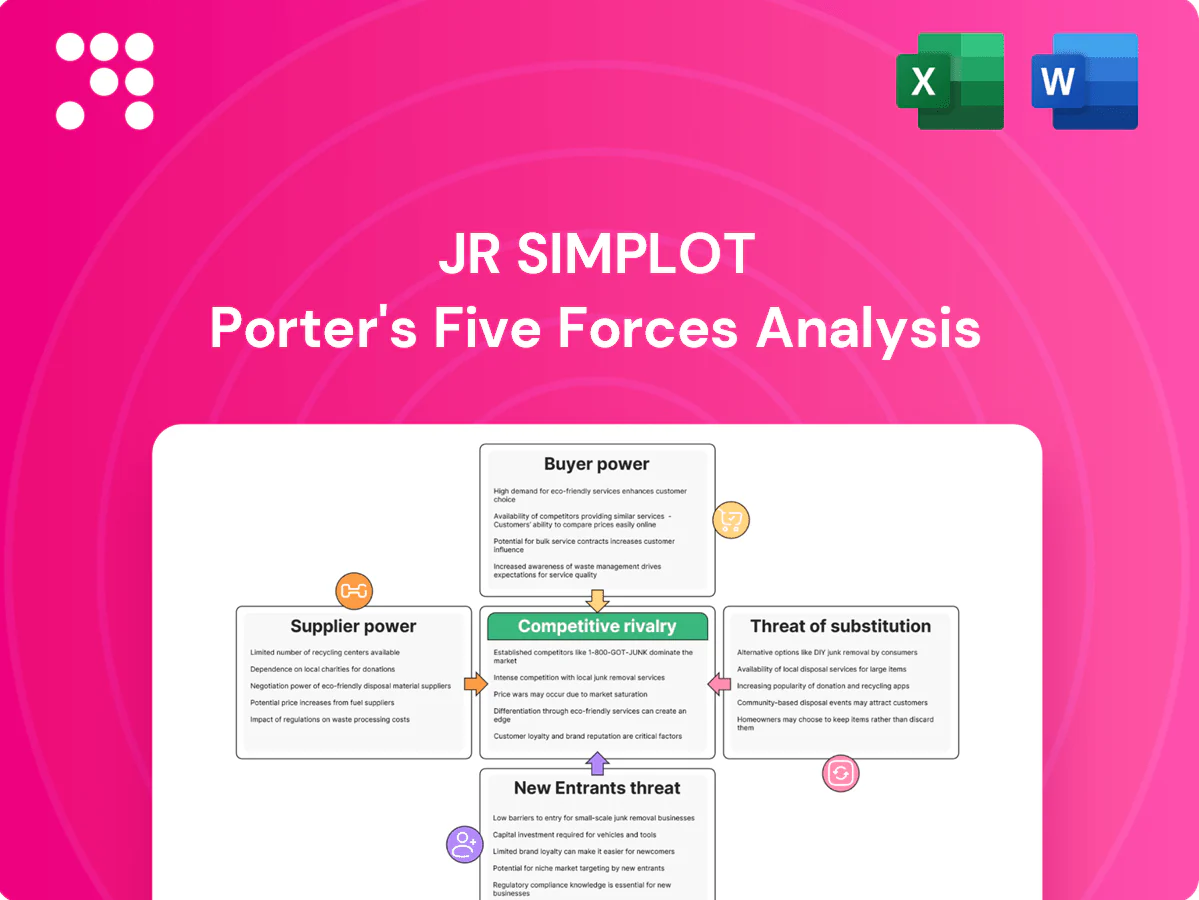

JR Simplot Porter's Five Forces Analysis

From Overview to Strategy Blueprint

JR Simplot faces moderate supplier power for fertilizers and seeds, high buyer power in commoditized potato markets, and significant rivalry from global agribusiness and private labels; barriers to entry are medium due to capital intensity but low-tech substitutes pose limited threat. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JR Simplot’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consolidated potato growers

Simplot sources potatoes from large grower networks in Idaho and the Pacific Northwest, regions that supply roughly 30% of US potatoes, giving some growers scale and bargaining leverage. Multi-year contracts smooth spot volatility but embed pricing formulas that can be disadvantageous if input costs spike. Weather-driven yield shortfalls (drought/flood cycles) periodically tighten supply and boost grower power. Simplot’s investment in storage and agronomy services reduces that supplier leverage.

Phosphate and raw input control

J.R. Simplot owns phosphate mines in southeastern Idaho and integrated fertilizer manufacturing, which reduces dependence on external mineral suppliers and lowers supplier power for key nutrients. Regulatory and environmental costs in mining, including permitting and reclamation obligations that can run into tens of millions of dollars, increase effective input rigidity. Vendors of equipment, reagents and explosives continue to retain negotiation leverage despite vertical integration.

Energy and utilities dependence

Processing plants and cold chains are highly energy intensive, exposing J.R. Simplot to utility and fuel suppliers; U.S. industrial electricity prices vary up to threefold across regions, creating material cost dispersion. Limited substitution during peak demand windows strengthens supplier power, with peak premiums often 20–50% above baseload rates. Active hedging and multi-source fuel contracts can moderate volatility and cap exposure. Plant location locks in exposure to regional utility monopolies and local rate structures.

Packaging and cold-chain vendors

Packaging films, pallets and reefer logistics are concentrated among few specialized vendors, giving suppliers leverage; tight freight and reefers in 2024 further elevated carrier bargaining power, though multi-year logistics contracts and private fleet use mitigate cost exposure and service risk, while port or labor disruptions can spike supplier leverage temporarily.

- Concentrated vendors

- Tight 2024 freight capacity

- Multi-year bids lower risk

- Disruptions spike leverage

Specialty chemicals and equipment OEMs

Processing lines rely on proprietary machinery and spare parts from a handful of OEMs, giving suppliers elevated leverage; switching costs and downtime risk amplify that power and can impose multi-week outages. Preventive maintenance programs and dual-sourcing of consumables reduce dependence, while vendor-managed inventory arrangements (increasingly adopted across food processors) help rebalance bargaining. JR Simplot reported roughly $3.5 billion revenue in 2023, underscoring scale-sensitive supply risks.

- Few OEMs: concentrated supplier base

- High switching cost: downtime risk

- Mitigation: preventive maintenance, dual-sourcing

- Leverage: vendor-managed inventory

Moderate-high supplier power; 30% potato exposure; energy spreads up to 3x

Simplot faces moderate-to-high supplier power: regional growers (Idaho/PacNW ~30% US potatoes) and concentrated OEMs/packaging vendors raise leverage, while vertical integration in phosphate mining and storage/agronomy lowers it. Energy price dispersion (up to 3x) and 2024 tight freight amplify risk; multi-year contracts, hedging and dual-sourcing partially mitigate exposure.

| Metric | Value |

|---|---|

| Revenue (2023) | $3.5bn |

| Idaho/PacNW potato share | ~30% |

| Energy price spread | up to 3x |

What is included in the product

Tailored Porter's Five Forces analysis for JR Simplot that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitute threats, and strategic recommendations to protect margins and inform investor or management decisions.

A concise one-sheet Porter's Five Forces for J.R. Simplot—instantly reveals competitive pressures and strategic levers to relieve decision-making pain points.

Customers Bargaining Power

Concentrated QSR chains

Global QSR leaders buy fries in volumes measured in millions of pounds annually, giving them outsized price and specification power over suppliers like JR Simplot. Vendor qualification lists and approved-supplier programs narrow buyer options and raise switching costs for producers. Long-term supply contracts, commonly spanning 3–5 years, stabilize volumes but compress supplier margins. Contractual performance penalties and operational audits further increase buyer leverage.

Retailers and private label

Retailers and club channels can pit Simplot branded products against private label—top four U.S. grocery retailers control roughly 60% of the market and private label reached about 18% of grocery sales in 2024, strengthening buyer leverage. Control of shelf space lets buyers demand prominent placement and promotional funding, with trade promotions often exceeding 10% of CPG revenue, pressuring margins. Product differentiation via cuts, coatings and innovation reduces direct comparability and lessens price-only competition.

Farm customers for fertilizer

Row-crop farmers are highly price-sensitive and can switch nutrient suppliers in a market worth roughly $25 billion annually in U.S. crop nutrients; seasonal buying windows and co-op bargaining (co-ops account for a large share of retail supply) amplify customer leverage. Simplot’s local distribution and agronomy services create stickiness by bundling advice and logistics. Commodity cycles matter: urea and MAP prices were roughly 50–60% below 2022 peaks by end-2024, swinging willingness to pay.

Foodservice distributors

Foodservice distributors aggregate thousands of independent restaurants and in 2024 the top three (Sysco, US Foods, Performance Food Group) controlled roughly 70% of the US distribution market, giving them strong leverage to negotiate rebates (commonly 1–3%) and volume-based concessions. Their dense route networks increase pressure on pass-through pricing and allow margin compression; co-developed SKUs and service-level guarantees are routinely used to trade margin for loyalty, while extended credit terms serve as a key negotiation lever.

- Aggregation: top 3 ≈70% (2024)

- Rebates: typically 1–3%

- Route density: enables pass-through leverage

- Co-developed SKUs: margin for loyalty

- Credit terms: strategic negotiation tool

Specification and quality requirements

Strict cut, color and texture specifications increase rejection risk and thus strengthen buyer bargaining power; in 2024 major retail chains enforced tighter specs, accelerating audits and chargebacks. Compliance investments create supplier-specific sunk costs in equipment and testing, while data sharing and yield-optimization programs can align incentives and reduce disputes. Failures to meet specs prompt rapid volume reallocation to rivals, often within 30 days.

- Rejection risk ↑ strengthens buyer leverage

- Compliance = supplier sunk costs

- Data sharing → incentive alignment

- Spec failures → rapid reallocation (≈30 days)

Buyers' power and promos squeeze food margins as nutrient costs fall 50–60%

Large QSRs, retailers and top distributors (top 3 ≈70% distribution share) exert strong price and spec power, using 3–5 year contracts, rebates (1–3%) and trade promos (>10% of CPG revenue) to compress Simplot margins; private label ≈18% of grocery sales (2024). Farmers/co-ops and seasonal buying plus nutrient prices ~50–60% below 2022 peaks by end-2024 tilt negotiation dynamics.

| Buyer | 2024 stat | Impact |

|---|---|---|

| Distributors | Top3 ≈70% | High leverage |

| Retail | Private label ≈18% | Promo pressure |

| Farmers | Nutrient prices -50–60% | Price sensitivity |

Preview Before You Purchase

JR Simplot Porter's Five Forces Analysis

This preview displays the exact JR Simplot Porter's Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The file is the full, professionally formatted report, ready for immediate download and use the moment you buy. Purchase grants instant access to this identical document for your strategic or investment needs.

From Overview to Strategy Blueprint

JR Simplot faces moderate supplier power for fertilizers and seeds, high buyer power in commoditized potato markets, and significant rivalry from global agribusiness and private labels; barriers to entry are medium due to capital intensity but low-tech substitutes pose limited threat. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JR Simplot’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consolidated potato growers

Simplot sources potatoes from large grower networks in Idaho and the Pacific Northwest, regions that supply roughly 30% of US potatoes, giving some growers scale and bargaining leverage. Multi-year contracts smooth spot volatility but embed pricing formulas that can be disadvantageous if input costs spike. Weather-driven yield shortfalls (drought/flood cycles) periodically tighten supply and boost grower power. Simplot’s investment in storage and agronomy services reduces that supplier leverage.

Phosphate and raw input control

J.R. Simplot owns phosphate mines in southeastern Idaho and integrated fertilizer manufacturing, which reduces dependence on external mineral suppliers and lowers supplier power for key nutrients. Regulatory and environmental costs in mining, including permitting and reclamation obligations that can run into tens of millions of dollars, increase effective input rigidity. Vendors of equipment, reagents and explosives continue to retain negotiation leverage despite vertical integration.

Energy and utilities dependence

Processing plants and cold chains are highly energy intensive, exposing J.R. Simplot to utility and fuel suppliers; U.S. industrial electricity prices vary up to threefold across regions, creating material cost dispersion. Limited substitution during peak demand windows strengthens supplier power, with peak premiums often 20–50% above baseload rates. Active hedging and multi-source fuel contracts can moderate volatility and cap exposure. Plant location locks in exposure to regional utility monopolies and local rate structures.

Packaging and cold-chain vendors

Packaging films, pallets and reefer logistics are concentrated among few specialized vendors, giving suppliers leverage; tight freight and reefers in 2024 further elevated carrier bargaining power, though multi-year logistics contracts and private fleet use mitigate cost exposure and service risk, while port or labor disruptions can spike supplier leverage temporarily.

- Concentrated vendors

- Tight 2024 freight capacity

- Multi-year bids lower risk

- Disruptions spike leverage

Specialty chemicals and equipment OEMs

Processing lines rely on proprietary machinery and spare parts from a handful of OEMs, giving suppliers elevated leverage; switching costs and downtime risk amplify that power and can impose multi-week outages. Preventive maintenance programs and dual-sourcing of consumables reduce dependence, while vendor-managed inventory arrangements (increasingly adopted across food processors) help rebalance bargaining. JR Simplot reported roughly $3.5 billion revenue in 2023, underscoring scale-sensitive supply risks.

- Few OEMs: concentrated supplier base

- High switching cost: downtime risk

- Mitigation: preventive maintenance, dual-sourcing

- Leverage: vendor-managed inventory

Moderate-high supplier power; 30% potato exposure; energy spreads up to 3x

Simplot faces moderate-to-high supplier power: regional growers (Idaho/PacNW ~30% US potatoes) and concentrated OEMs/packaging vendors raise leverage, while vertical integration in phosphate mining and storage/agronomy lowers it. Energy price dispersion (up to 3x) and 2024 tight freight amplify risk; multi-year contracts, hedging and dual-sourcing partially mitigate exposure.

| Metric | Value |

|---|---|

| Revenue (2023) | $3.5bn |

| Idaho/PacNW potato share | ~30% |

| Energy price spread | up to 3x |

What is included in the product

Tailored Porter's Five Forces analysis for JR Simplot that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitute threats, and strategic recommendations to protect margins and inform investor or management decisions.

A concise one-sheet Porter's Five Forces for J.R. Simplot—instantly reveals competitive pressures and strategic levers to relieve decision-making pain points.

Customers Bargaining Power

Concentrated QSR chains

Global QSR leaders buy fries in volumes measured in millions of pounds annually, giving them outsized price and specification power over suppliers like JR Simplot. Vendor qualification lists and approved-supplier programs narrow buyer options and raise switching costs for producers. Long-term supply contracts, commonly spanning 3–5 years, stabilize volumes but compress supplier margins. Contractual performance penalties and operational audits further increase buyer leverage.

Retailers and private label

Retailers and club channels can pit Simplot branded products against private label—top four U.S. grocery retailers control roughly 60% of the market and private label reached about 18% of grocery sales in 2024, strengthening buyer leverage. Control of shelf space lets buyers demand prominent placement and promotional funding, with trade promotions often exceeding 10% of CPG revenue, pressuring margins. Product differentiation via cuts, coatings and innovation reduces direct comparability and lessens price-only competition.

Farm customers for fertilizer

Row-crop farmers are highly price-sensitive and can switch nutrient suppliers in a market worth roughly $25 billion annually in U.S. crop nutrients; seasonal buying windows and co-op bargaining (co-ops account for a large share of retail supply) amplify customer leverage. Simplot’s local distribution and agronomy services create stickiness by bundling advice and logistics. Commodity cycles matter: urea and MAP prices were roughly 50–60% below 2022 peaks by end-2024, swinging willingness to pay.

Foodservice distributors

Foodservice distributors aggregate thousands of independent restaurants and in 2024 the top three (Sysco, US Foods, Performance Food Group) controlled roughly 70% of the US distribution market, giving them strong leverage to negotiate rebates (commonly 1–3%) and volume-based concessions. Their dense route networks increase pressure on pass-through pricing and allow margin compression; co-developed SKUs and service-level guarantees are routinely used to trade margin for loyalty, while extended credit terms serve as a key negotiation lever.

- Aggregation: top 3 ≈70% (2024)

- Rebates: typically 1–3%

- Route density: enables pass-through leverage

- Co-developed SKUs: margin for loyalty

- Credit terms: strategic negotiation tool

Specification and quality requirements

Strict cut, color and texture specifications increase rejection risk and thus strengthen buyer bargaining power; in 2024 major retail chains enforced tighter specs, accelerating audits and chargebacks. Compliance investments create supplier-specific sunk costs in equipment and testing, while data sharing and yield-optimization programs can align incentives and reduce disputes. Failures to meet specs prompt rapid volume reallocation to rivals, often within 30 days.

- Rejection risk ↑ strengthens buyer leverage

- Compliance = supplier sunk costs

- Data sharing → incentive alignment

- Spec failures → rapid reallocation (≈30 days)

Buyers' power and promos squeeze food margins as nutrient costs fall 50–60%

Large QSRs, retailers and top distributors (top 3 ≈70% distribution share) exert strong price and spec power, using 3–5 year contracts, rebates (1–3%) and trade promos (>10% of CPG revenue) to compress Simplot margins; private label ≈18% of grocery sales (2024). Farmers/co-ops and seasonal buying plus nutrient prices ~50–60% below 2022 peaks by end-2024 tilt negotiation dynamics.

| Buyer | 2024 stat | Impact |

|---|---|---|

| Distributors | Top3 ≈70% | High leverage |

| Retail | Private label ≈18% | Promo pressure |

| Farmers | Nutrient prices -50–60% | Price sensitivity |

Preview Before You Purchase

JR Simplot Porter's Five Forces Analysis

This preview displays the exact JR Simplot Porter's Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The file is the full, professionally formatted report, ready for immediate download and use the moment you buy. Purchase grants instant access to this identical document for your strategic or investment needs.

Description

From Overview to Strategy Blueprint

JR Simplot faces moderate supplier power for fertilizers and seeds, high buyer power in commoditized potato markets, and significant rivalry from global agribusiness and private labels; barriers to entry are medium due to capital intensity but low-tech substitutes pose limited threat. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore JR Simplot’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Consolidated potato growers

Simplot sources potatoes from large grower networks in Idaho and the Pacific Northwest, regions that supply roughly 30% of US potatoes, giving some growers scale and bargaining leverage. Multi-year contracts smooth spot volatility but embed pricing formulas that can be disadvantageous if input costs spike. Weather-driven yield shortfalls (drought/flood cycles) periodically tighten supply and boost grower power. Simplot’s investment in storage and agronomy services reduces that supplier leverage.

Phosphate and raw input control

J.R. Simplot owns phosphate mines in southeastern Idaho and integrated fertilizer manufacturing, which reduces dependence on external mineral suppliers and lowers supplier power for key nutrients. Regulatory and environmental costs in mining, including permitting and reclamation obligations that can run into tens of millions of dollars, increase effective input rigidity. Vendors of equipment, reagents and explosives continue to retain negotiation leverage despite vertical integration.

Energy and utilities dependence

Processing plants and cold chains are highly energy intensive, exposing J.R. Simplot to utility and fuel suppliers; U.S. industrial electricity prices vary up to threefold across regions, creating material cost dispersion. Limited substitution during peak demand windows strengthens supplier power, with peak premiums often 20–50% above baseload rates. Active hedging and multi-source fuel contracts can moderate volatility and cap exposure. Plant location locks in exposure to regional utility monopolies and local rate structures.

Packaging and cold-chain vendors

Packaging films, pallets and reefer logistics are concentrated among few specialized vendors, giving suppliers leverage; tight freight and reefers in 2024 further elevated carrier bargaining power, though multi-year logistics contracts and private fleet use mitigate cost exposure and service risk, while port or labor disruptions can spike supplier leverage temporarily.

- Concentrated vendors

- Tight 2024 freight capacity

- Multi-year bids lower risk

- Disruptions spike leverage

Specialty chemicals and equipment OEMs

Processing lines rely on proprietary machinery and spare parts from a handful of OEMs, giving suppliers elevated leverage; switching costs and downtime risk amplify that power and can impose multi-week outages. Preventive maintenance programs and dual-sourcing of consumables reduce dependence, while vendor-managed inventory arrangements (increasingly adopted across food processors) help rebalance bargaining. JR Simplot reported roughly $3.5 billion revenue in 2023, underscoring scale-sensitive supply risks.

- Few OEMs: concentrated supplier base

- High switching cost: downtime risk

- Mitigation: preventive maintenance, dual-sourcing

- Leverage: vendor-managed inventory

Moderate-high supplier power; 30% potato exposure; energy spreads up to 3x

Simplot faces moderate-to-high supplier power: regional growers (Idaho/PacNW ~30% US potatoes) and concentrated OEMs/packaging vendors raise leverage, while vertical integration in phosphate mining and storage/agronomy lowers it. Energy price dispersion (up to 3x) and 2024 tight freight amplify risk; multi-year contracts, hedging and dual-sourcing partially mitigate exposure.

| Metric | Value |

|---|---|

| Revenue (2023) | $3.5bn |

| Idaho/PacNW potato share | ~30% |

| Energy price spread | up to 3x |

What is included in the product

Tailored Porter's Five Forces analysis for JR Simplot that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitute threats, and strategic recommendations to protect margins and inform investor or management decisions.

A concise one-sheet Porter's Five Forces for J.R. Simplot—instantly reveals competitive pressures and strategic levers to relieve decision-making pain points.

Customers Bargaining Power

Concentrated QSR chains

Global QSR leaders buy fries in volumes measured in millions of pounds annually, giving them outsized price and specification power over suppliers like JR Simplot. Vendor qualification lists and approved-supplier programs narrow buyer options and raise switching costs for producers. Long-term supply contracts, commonly spanning 3–5 years, stabilize volumes but compress supplier margins. Contractual performance penalties and operational audits further increase buyer leverage.

Retailers and private label

Retailers and club channels can pit Simplot branded products against private label—top four U.S. grocery retailers control roughly 60% of the market and private label reached about 18% of grocery sales in 2024, strengthening buyer leverage. Control of shelf space lets buyers demand prominent placement and promotional funding, with trade promotions often exceeding 10% of CPG revenue, pressuring margins. Product differentiation via cuts, coatings and innovation reduces direct comparability and lessens price-only competition.

Farm customers for fertilizer

Row-crop farmers are highly price-sensitive and can switch nutrient suppliers in a market worth roughly $25 billion annually in U.S. crop nutrients; seasonal buying windows and co-op bargaining (co-ops account for a large share of retail supply) amplify customer leverage. Simplot’s local distribution and agronomy services create stickiness by bundling advice and logistics. Commodity cycles matter: urea and MAP prices were roughly 50–60% below 2022 peaks by end-2024, swinging willingness to pay.

Foodservice distributors

Foodservice distributors aggregate thousands of independent restaurants and in 2024 the top three (Sysco, US Foods, Performance Food Group) controlled roughly 70% of the US distribution market, giving them strong leverage to negotiate rebates (commonly 1–3%) and volume-based concessions. Their dense route networks increase pressure on pass-through pricing and allow margin compression; co-developed SKUs and service-level guarantees are routinely used to trade margin for loyalty, while extended credit terms serve as a key negotiation lever.

- Aggregation: top 3 ≈70% (2024)

- Rebates: typically 1–3%

- Route density: enables pass-through leverage

- Co-developed SKUs: margin for loyalty

- Credit terms: strategic negotiation tool

Specification and quality requirements

Strict cut, color and texture specifications increase rejection risk and thus strengthen buyer bargaining power; in 2024 major retail chains enforced tighter specs, accelerating audits and chargebacks. Compliance investments create supplier-specific sunk costs in equipment and testing, while data sharing and yield-optimization programs can align incentives and reduce disputes. Failures to meet specs prompt rapid volume reallocation to rivals, often within 30 days.

- Rejection risk ↑ strengthens buyer leverage

- Compliance = supplier sunk costs

- Data sharing → incentive alignment

- Spec failures → rapid reallocation (≈30 days)

Buyers' power and promos squeeze food margins as nutrient costs fall 50–60%

Large QSRs, retailers and top distributors (top 3 ≈70% distribution share) exert strong price and spec power, using 3–5 year contracts, rebates (1–3%) and trade promos (>10% of CPG revenue) to compress Simplot margins; private label ≈18% of grocery sales (2024). Farmers/co-ops and seasonal buying plus nutrient prices ~50–60% below 2022 peaks by end-2024 tilt negotiation dynamics.

| Buyer | 2024 stat | Impact |

|---|---|---|

| Distributors | Top3 ≈70% | High leverage |

| Retail | Private label ≈18% | Promo pressure |

| Farmers | Nutrient prices -50–60% | Price sensitivity |

Preview Before You Purchase

JR Simplot Porter's Five Forces Analysis

This preview displays the exact JR Simplot Porter's Five Forces analysis you'll receive upon purchase—no placeholders or mockups. The file is the full, professionally formatted report, ready for immediate download and use the moment you buy. Purchase grants instant access to this identical document for your strategic or investment needs.