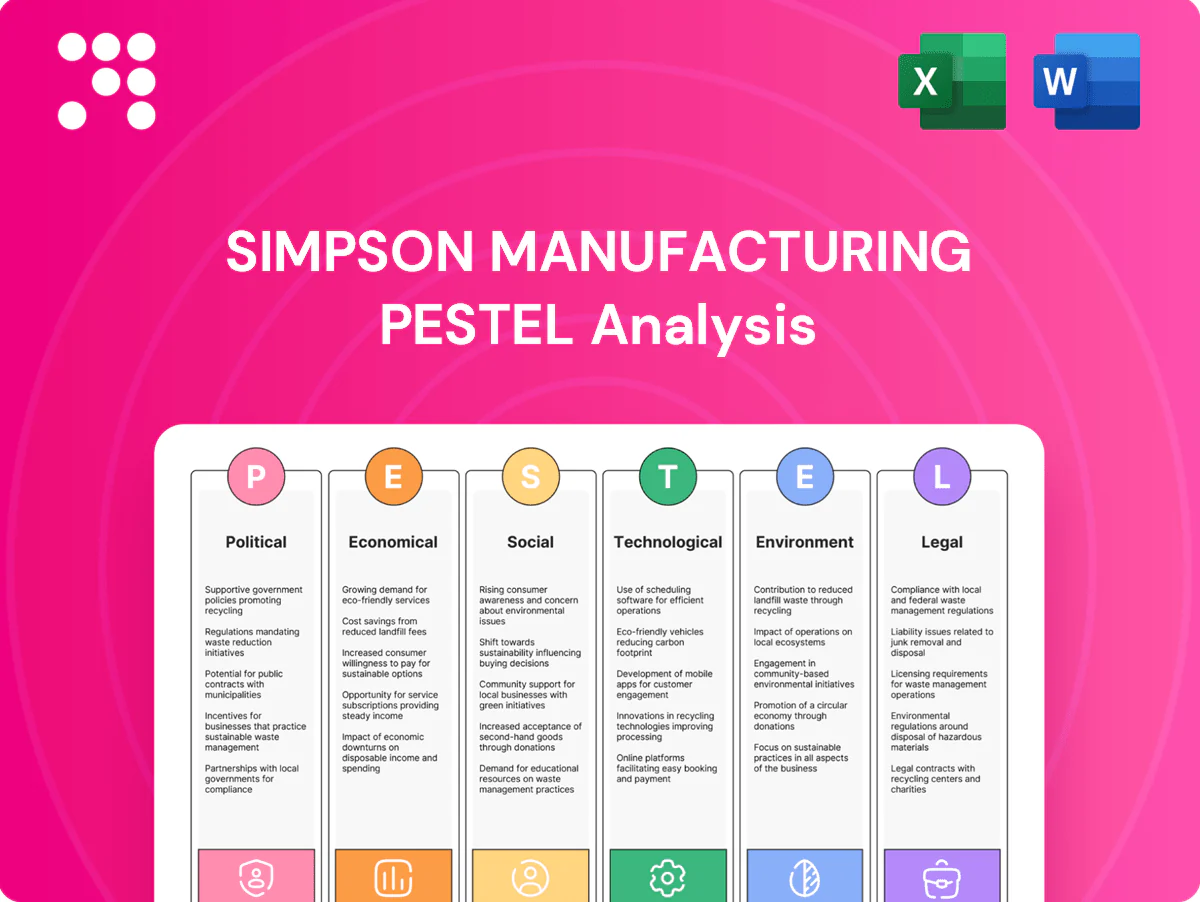

Simpson Manufacturing PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, and evolving sustainability rules are reshaping Simpson Manufacturing’s prospects in our concise PESTLE snapshot. This expert-ready analysis highlights risks and opportunities you can act on immediately. Buy the full PESTLE to access the complete deep-dive, editable insights and strategic recommendations.

Political factors

Building codes and public policy

Government adoption and periodic updates to seismic and wind-resistance codes directly expand demand for Simpson Manufacturing’s structural connectors, as jurisdictions implement newer ICC I-Codes that are revised on a three-year cycle. Alignment with FEMA guidance and international standards (eg ISO/EN structural norms) shapes product specifications and market entry requirements. Proactive engagement with code councils and ICC committees can secure favorable inclusion of proprietary solutions into model codes, supporting long-term revenue stability.

Infrastructure spending priorities

National and local infrastructure bills, notably the 2021 Infrastructure Investment and Jobs Act totaling 1.2 trillion dollars with roughly 550 billion in new federal investments, drive non-residential construction cycles and order timing. Funding streams for resilient infrastructure raise demand for high-performance fasteners and connectors used in bridges and utilities. Clear visibility into multi-year budget pipelines enables Simpson to plan capacity and position inventory to capture contract-led growth.

Trade policy and tariffs

Section 232 tariffs (25% on steel, 10% on aluminum) continue to raise Simpson Manufacturing’s input costs and compress pricing power on fabricated metal products. Shifts in US–China and US–EU trade relations, antidumping duties and quotas alter sourcing economics and can force supplier changes. Diversified procurement and localizing production reduce exposure to tariff-driven volatility.

“Buy America”/local content rules

Buy America and local content rules boost demand for domestic manufacturing footprints, increasing Simpson Manufacturings competitiveness for federally funded projects tied to the Bipartisan Infrastructure Law (BIL), which includes about 550 billion dollars in new infrastructure investment.

Compliance determines eligibility for public projects and inclusion on procurement lists, making supply-chain localization a strategic priority for revenue capture from public-sector spending.

Robust certification and documentation systems are now critical to qualify for contracts and avoid debarment or bid disqualification.

- Tag: BIL_550B

- Tag: Domestic_Footprint

- Tag: Procurement_Eligibility

- Tag: Certification_Required

Geopolitical supply chain stability

Regional conflicts and sanctions since 2022 have disrupted metals, coatings and logistics, raising reroute and insurance costs; freight volatility remained elevated into 2023–24. Political risk in key supplier countries lengthened lead times and increased input costs for manufacturers like Simpson. Multi-sourcing and nearshoring reduced exposure, with nearshore sourcing up about 15% in manufacturing by 2024.

- Sanctions-driven supply shocks

- Longer lead times, higher costs

- Multi-sourcing & nearshoring mitigate risk (~15% rise)

Code updates, Buy America and FEMA lift connector demand; IIJA 550B

Code updates on a three-year ICC cycle and FEMA alignment drive demand for Simpson’s connectors; IIJA/BIL (2021) added ~550B in new infrastructure funding supporting nonresidential demand. Section 232 tariffs (25% steel, 10% Al) and 2022+ sanctions raised input costs; nearshoring rose ~15% by 2024 to mitigate risk. Buy America/local content increases federal contract eligibility and favors domestic capacity.

| Factor | Metric |

|---|---|

| IIJA/BIL | ~550B new |

| Tariffs | Steel 25% / Al 10% |

| Nearshoring | +15% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Simpson Manufacturing across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed insights and forward‑looking scenarios to identify risks and opportunities for executives, investors and strategists.

Concise, visually segmented Simpson Manufacturing PESTLE summary streamlines external risk assessment for meetings and presentations, is easily editable for local context or notes, and produces a shareable slide-ready format to align teams and support strategic planning.

Economic factors

Housing starts and renovation cycles

Residential construction volume is Simpson Manufacturings primary demand driver: US housing starts ran near a 1.45 million annualized pace in 2024 (US Census Bureau), while US home-improvement spending was roughly $480 billion in 2024 (JCHS/market estimates). New builds and R&R cycles correlate tightly with connector and fastener sales, so tracking building permits, starts and homeowner equity levels directly informs Simpson sales forecasts.

Interest rates and credit availability

Higher mortgage and construction financing costs—with the Fed funds rate at 5.25–5.50% and 30‑year mortgage rates near 7% in mid‑2025—have suppressed project starts, while potential rate cuts could unlock pent‑up residential and commercial demand; Simpson can use hedging and flexible pricing to manage rate‑driven margin volatility.

Raw material and freight costs

Steel HRC averaged about $900/ton in mid-2025 and LME zinc near $3,100/ton, while US industrial electricity ran ~$0.081/kWh (EIA 2024); these inputs directly compress or expand gross margins for Simpson. Ocean spot rates Shanghai–LA fell toward $1,300/FEU in early 2025 and US truckload spot rates rose ~7% YoY in 2024, pushing delivered cost and service variability. Long-term supply contracts and 60–90‑day inventory buffers have been used to stabilize input economics.

Labor market tightness

Skilled labor shortages slow jobsite throughput; 2024 AGC survey found 89% of firms had difficulty filling craft positions, driving delays and higher labor costs.

Time-saving, pre-engineered solutions gain appeal when labor is scarce; training and on-site installation support increase contractor preference.

- Labor squeeze: AGC 2024 — 89% difficulty filling craft roles

- Pre-engineered demand rises with scarce labor

- Training/support boosts product adoption

Currency fluctuations

Currency fluctuations materially affect Simpson Manufacturing’s reported results and import/export competitiveness: a stronger dollar can compress overseas translation revenues while reducing the cost of imported inputs, and a weaker dollar has the opposite effect. The company uses natural hedges via geographically diversified sourcing and local pricing to dampen volatility, while contractual pricing clauses limit short-term FX exposure.

- FX impact: translation vs transaction

- Benefit: lower input costs when USD strong

- Risk: pressured overseas revenues

- Mitigants: natural hedges, pricing localization

Code updates, Buy America and FEMA lift connector demand; IIJA 550B

Residential demand drives Simpson: US housing starts ~1.45M (2024) and home‑improvement ≈$480B (2024); financing costs (30y ≈7% mid‑2025) suppress starts but cuts could reaccelerate. Key inputs—HRC steel ≈$900/ton, LME zinc ≈$3,100/ton, US electricity ≈$0.081/kWh (mid‑2025)—and labor shortages (AGC 89% difficulty 2024) compress margins and pace.

| Metric | Value |

|---|---|

| Housing starts (2024) | 1.45M |

| Home‑improve (2024) | $480B |

| 30y mortgage (mid‑2025) | ~7% |

| HRC steel | $900/ton |

| LME zinc | $3,100/ton |

| Electricity (US) | $0.081/kWh |

| Labor difficulty (AGC 2024) | 89% |

Preview Before You Purchase

Simpson Manufacturing PESTLE Analysis

The preview shown here is the exact Simpson Manufacturing PESTLE Analysis document you’ll receive after purchase—fully formatted and professionally structured. No placeholders or teasers: the content, layout, and analysis are final and ready to download. What you see is the real file delivered immediately upon payment.

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, and evolving sustainability rules are reshaping Simpson Manufacturing’s prospects in our concise PESTLE snapshot. This expert-ready analysis highlights risks and opportunities you can act on immediately. Buy the full PESTLE to access the complete deep-dive, editable insights and strategic recommendations.

Political factors

Building codes and public policy

Government adoption and periodic updates to seismic and wind-resistance codes directly expand demand for Simpson Manufacturing’s structural connectors, as jurisdictions implement newer ICC I-Codes that are revised on a three-year cycle. Alignment with FEMA guidance and international standards (eg ISO/EN structural norms) shapes product specifications and market entry requirements. Proactive engagement with code councils and ICC committees can secure favorable inclusion of proprietary solutions into model codes, supporting long-term revenue stability.

Infrastructure spending priorities

National and local infrastructure bills, notably the 2021 Infrastructure Investment and Jobs Act totaling 1.2 trillion dollars with roughly 550 billion in new federal investments, drive non-residential construction cycles and order timing. Funding streams for resilient infrastructure raise demand for high-performance fasteners and connectors used in bridges and utilities. Clear visibility into multi-year budget pipelines enables Simpson to plan capacity and position inventory to capture contract-led growth.

Trade policy and tariffs

Section 232 tariffs (25% on steel, 10% on aluminum) continue to raise Simpson Manufacturing’s input costs and compress pricing power on fabricated metal products. Shifts in US–China and US–EU trade relations, antidumping duties and quotas alter sourcing economics and can force supplier changes. Diversified procurement and localizing production reduce exposure to tariff-driven volatility.

“Buy America”/local content rules

Buy America and local content rules boost demand for domestic manufacturing footprints, increasing Simpson Manufacturings competitiveness for federally funded projects tied to the Bipartisan Infrastructure Law (BIL), which includes about 550 billion dollars in new infrastructure investment.

Compliance determines eligibility for public projects and inclusion on procurement lists, making supply-chain localization a strategic priority for revenue capture from public-sector spending.

Robust certification and documentation systems are now critical to qualify for contracts and avoid debarment or bid disqualification.

- Tag: BIL_550B

- Tag: Domestic_Footprint

- Tag: Procurement_Eligibility

- Tag: Certification_Required

Geopolitical supply chain stability

Regional conflicts and sanctions since 2022 have disrupted metals, coatings and logistics, raising reroute and insurance costs; freight volatility remained elevated into 2023–24. Political risk in key supplier countries lengthened lead times and increased input costs for manufacturers like Simpson. Multi-sourcing and nearshoring reduced exposure, with nearshore sourcing up about 15% in manufacturing by 2024.

- Sanctions-driven supply shocks

- Longer lead times, higher costs

- Multi-sourcing & nearshoring mitigate risk (~15% rise)

Code updates, Buy America and FEMA lift connector demand; IIJA 550B

Code updates on a three-year ICC cycle and FEMA alignment drive demand for Simpson’s connectors; IIJA/BIL (2021) added ~550B in new infrastructure funding supporting nonresidential demand. Section 232 tariffs (25% steel, 10% Al) and 2022+ sanctions raised input costs; nearshoring rose ~15% by 2024 to mitigate risk. Buy America/local content increases federal contract eligibility and favors domestic capacity.

| Factor | Metric |

|---|---|

| IIJA/BIL | ~550B new |

| Tariffs | Steel 25% / Al 10% |

| Nearshoring | +15% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Simpson Manufacturing across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed insights and forward‑looking scenarios to identify risks and opportunities for executives, investors and strategists.

Concise, visually segmented Simpson Manufacturing PESTLE summary streamlines external risk assessment for meetings and presentations, is easily editable for local context or notes, and produces a shareable slide-ready format to align teams and support strategic planning.

Economic factors

Housing starts and renovation cycles

Residential construction volume is Simpson Manufacturings primary demand driver: US housing starts ran near a 1.45 million annualized pace in 2024 (US Census Bureau), while US home-improvement spending was roughly $480 billion in 2024 (JCHS/market estimates). New builds and R&R cycles correlate tightly with connector and fastener sales, so tracking building permits, starts and homeowner equity levels directly informs Simpson sales forecasts.

Interest rates and credit availability

Higher mortgage and construction financing costs—with the Fed funds rate at 5.25–5.50% and 30‑year mortgage rates near 7% in mid‑2025—have suppressed project starts, while potential rate cuts could unlock pent‑up residential and commercial demand; Simpson can use hedging and flexible pricing to manage rate‑driven margin volatility.

Raw material and freight costs

Steel HRC averaged about $900/ton in mid-2025 and LME zinc near $3,100/ton, while US industrial electricity ran ~$0.081/kWh (EIA 2024); these inputs directly compress or expand gross margins for Simpson. Ocean spot rates Shanghai–LA fell toward $1,300/FEU in early 2025 and US truckload spot rates rose ~7% YoY in 2024, pushing delivered cost and service variability. Long-term supply contracts and 60–90‑day inventory buffers have been used to stabilize input economics.

Labor market tightness

Skilled labor shortages slow jobsite throughput; 2024 AGC survey found 89% of firms had difficulty filling craft positions, driving delays and higher labor costs.

Time-saving, pre-engineered solutions gain appeal when labor is scarce; training and on-site installation support increase contractor preference.

- Labor squeeze: AGC 2024 — 89% difficulty filling craft roles

- Pre-engineered demand rises with scarce labor

- Training/support boosts product adoption

Currency fluctuations

Currency fluctuations materially affect Simpson Manufacturing’s reported results and import/export competitiveness: a stronger dollar can compress overseas translation revenues while reducing the cost of imported inputs, and a weaker dollar has the opposite effect. The company uses natural hedges via geographically diversified sourcing and local pricing to dampen volatility, while contractual pricing clauses limit short-term FX exposure.

- FX impact: translation vs transaction

- Benefit: lower input costs when USD strong

- Risk: pressured overseas revenues

- Mitigants: natural hedges, pricing localization

Code updates, Buy America and FEMA lift connector demand; IIJA 550B

Residential demand drives Simpson: US housing starts ~1.45M (2024) and home‑improvement ≈$480B (2024); financing costs (30y ≈7% mid‑2025) suppress starts but cuts could reaccelerate. Key inputs—HRC steel ≈$900/ton, LME zinc ≈$3,100/ton, US electricity ≈$0.081/kWh (mid‑2025)—and labor shortages (AGC 89% difficulty 2024) compress margins and pace.

| Metric | Value |

|---|---|

| Housing starts (2024) | 1.45M |

| Home‑improve (2024) | $480B |

| 30y mortgage (mid‑2025) | ~7% |

| HRC steel | $900/ton |

| LME zinc | $3,100/ton |

| Electricity (US) | $0.081/kWh |

| Labor difficulty (AGC 2024) | 89% |

Preview Before You Purchase

Simpson Manufacturing PESTLE Analysis

The preview shown here is the exact Simpson Manufacturing PESTLE Analysis document you’ll receive after purchase—fully formatted and professionally structured. No placeholders or teasers: the content, layout, and analysis are final and ready to download. What you see is the real file delivered immediately upon payment.

Description

Your Shortcut to Market Insight Starts Here

Discover how political shifts, supply-chain economics, and evolving sustainability rules are reshaping Simpson Manufacturing’s prospects in our concise PESTLE snapshot. This expert-ready analysis highlights risks and opportunities you can act on immediately. Buy the full PESTLE to access the complete deep-dive, editable insights and strategic recommendations.

Political factors

Building codes and public policy

Government adoption and periodic updates to seismic and wind-resistance codes directly expand demand for Simpson Manufacturing’s structural connectors, as jurisdictions implement newer ICC I-Codes that are revised on a three-year cycle. Alignment with FEMA guidance and international standards (eg ISO/EN structural norms) shapes product specifications and market entry requirements. Proactive engagement with code councils and ICC committees can secure favorable inclusion of proprietary solutions into model codes, supporting long-term revenue stability.

Infrastructure spending priorities

National and local infrastructure bills, notably the 2021 Infrastructure Investment and Jobs Act totaling 1.2 trillion dollars with roughly 550 billion in new federal investments, drive non-residential construction cycles and order timing. Funding streams for resilient infrastructure raise demand for high-performance fasteners and connectors used in bridges and utilities. Clear visibility into multi-year budget pipelines enables Simpson to plan capacity and position inventory to capture contract-led growth.

Trade policy and tariffs

Section 232 tariffs (25% on steel, 10% on aluminum) continue to raise Simpson Manufacturing’s input costs and compress pricing power on fabricated metal products. Shifts in US–China and US–EU trade relations, antidumping duties and quotas alter sourcing economics and can force supplier changes. Diversified procurement and localizing production reduce exposure to tariff-driven volatility.

“Buy America”/local content rules

Buy America and local content rules boost demand for domestic manufacturing footprints, increasing Simpson Manufacturings competitiveness for federally funded projects tied to the Bipartisan Infrastructure Law (BIL), which includes about 550 billion dollars in new infrastructure investment.

Compliance determines eligibility for public projects and inclusion on procurement lists, making supply-chain localization a strategic priority for revenue capture from public-sector spending.

Robust certification and documentation systems are now critical to qualify for contracts and avoid debarment or bid disqualification.

- Tag: BIL_550B

- Tag: Domestic_Footprint

- Tag: Procurement_Eligibility

- Tag: Certification_Required

Geopolitical supply chain stability

Regional conflicts and sanctions since 2022 have disrupted metals, coatings and logistics, raising reroute and insurance costs; freight volatility remained elevated into 2023–24. Political risk in key supplier countries lengthened lead times and increased input costs for manufacturers like Simpson. Multi-sourcing and nearshoring reduced exposure, with nearshore sourcing up about 15% in manufacturing by 2024.

- Sanctions-driven supply shocks

- Longer lead times, higher costs

- Multi-sourcing & nearshoring mitigate risk (~15% rise)

Code updates, Buy America and FEMA lift connector demand; IIJA 550B

Code updates on a three-year ICC cycle and FEMA alignment drive demand for Simpson’s connectors; IIJA/BIL (2021) added ~550B in new infrastructure funding supporting nonresidential demand. Section 232 tariffs (25% steel, 10% Al) and 2022+ sanctions raised input costs; nearshoring rose ~15% by 2024 to mitigate risk. Buy America/local content increases federal contract eligibility and favors domestic capacity.

| Factor | Metric |

|---|---|

| IIJA/BIL | ~550B new |

| Tariffs | Steel 25% / Al 10% |

| Nearshoring | +15% (2024) |

What is included in the product

Explores how macro-environmental factors uniquely affect Simpson Manufacturing across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data‑backed insights and forward‑looking scenarios to identify risks and opportunities for executives, investors and strategists.

Concise, visually segmented Simpson Manufacturing PESTLE summary streamlines external risk assessment for meetings and presentations, is easily editable for local context or notes, and produces a shareable slide-ready format to align teams and support strategic planning.

Economic factors

Housing starts and renovation cycles

Residential construction volume is Simpson Manufacturings primary demand driver: US housing starts ran near a 1.45 million annualized pace in 2024 (US Census Bureau), while US home-improvement spending was roughly $480 billion in 2024 (JCHS/market estimates). New builds and R&R cycles correlate tightly with connector and fastener sales, so tracking building permits, starts and homeowner equity levels directly informs Simpson sales forecasts.

Interest rates and credit availability

Higher mortgage and construction financing costs—with the Fed funds rate at 5.25–5.50% and 30‑year mortgage rates near 7% in mid‑2025—have suppressed project starts, while potential rate cuts could unlock pent‑up residential and commercial demand; Simpson can use hedging and flexible pricing to manage rate‑driven margin volatility.

Raw material and freight costs

Steel HRC averaged about $900/ton in mid-2025 and LME zinc near $3,100/ton, while US industrial electricity ran ~$0.081/kWh (EIA 2024); these inputs directly compress or expand gross margins for Simpson. Ocean spot rates Shanghai–LA fell toward $1,300/FEU in early 2025 and US truckload spot rates rose ~7% YoY in 2024, pushing delivered cost and service variability. Long-term supply contracts and 60–90‑day inventory buffers have been used to stabilize input economics.

Labor market tightness

Skilled labor shortages slow jobsite throughput; 2024 AGC survey found 89% of firms had difficulty filling craft positions, driving delays and higher labor costs.

Time-saving, pre-engineered solutions gain appeal when labor is scarce; training and on-site installation support increase contractor preference.

- Labor squeeze: AGC 2024 — 89% difficulty filling craft roles

- Pre-engineered demand rises with scarce labor

- Training/support boosts product adoption

Currency fluctuations

Currency fluctuations materially affect Simpson Manufacturing’s reported results and import/export competitiveness: a stronger dollar can compress overseas translation revenues while reducing the cost of imported inputs, and a weaker dollar has the opposite effect. The company uses natural hedges via geographically diversified sourcing and local pricing to dampen volatility, while contractual pricing clauses limit short-term FX exposure.

- FX impact: translation vs transaction

- Benefit: lower input costs when USD strong

- Risk: pressured overseas revenues

- Mitigants: natural hedges, pricing localization

Code updates, Buy America and FEMA lift connector demand; IIJA 550B

Residential demand drives Simpson: US housing starts ~1.45M (2024) and home‑improvement ≈$480B (2024); financing costs (30y ≈7% mid‑2025) suppress starts but cuts could reaccelerate. Key inputs—HRC steel ≈$900/ton, LME zinc ≈$3,100/ton, US electricity ≈$0.081/kWh (mid‑2025)—and labor shortages (AGC 89% difficulty 2024) compress margins and pace.

| Metric | Value |

|---|---|

| Housing starts (2024) | 1.45M |

| Home‑improve (2024) | $480B |

| 30y mortgage (mid‑2025) | ~7% |

| HRC steel | $900/ton |

| LME zinc | $3,100/ton |

| Electricity (US) | $0.081/kWh |

| Labor difficulty (AGC 2024) | 89% |

Preview Before You Purchase

Simpson Manufacturing PESTLE Analysis

The preview shown here is the exact Simpson Manufacturing PESTLE Analysis document you’ll receive after purchase—fully formatted and professionally structured. No placeholders or teasers: the content, layout, and analysis are final and ready to download. What you see is the real file delivered immediately upon payment.