Sims Metal Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

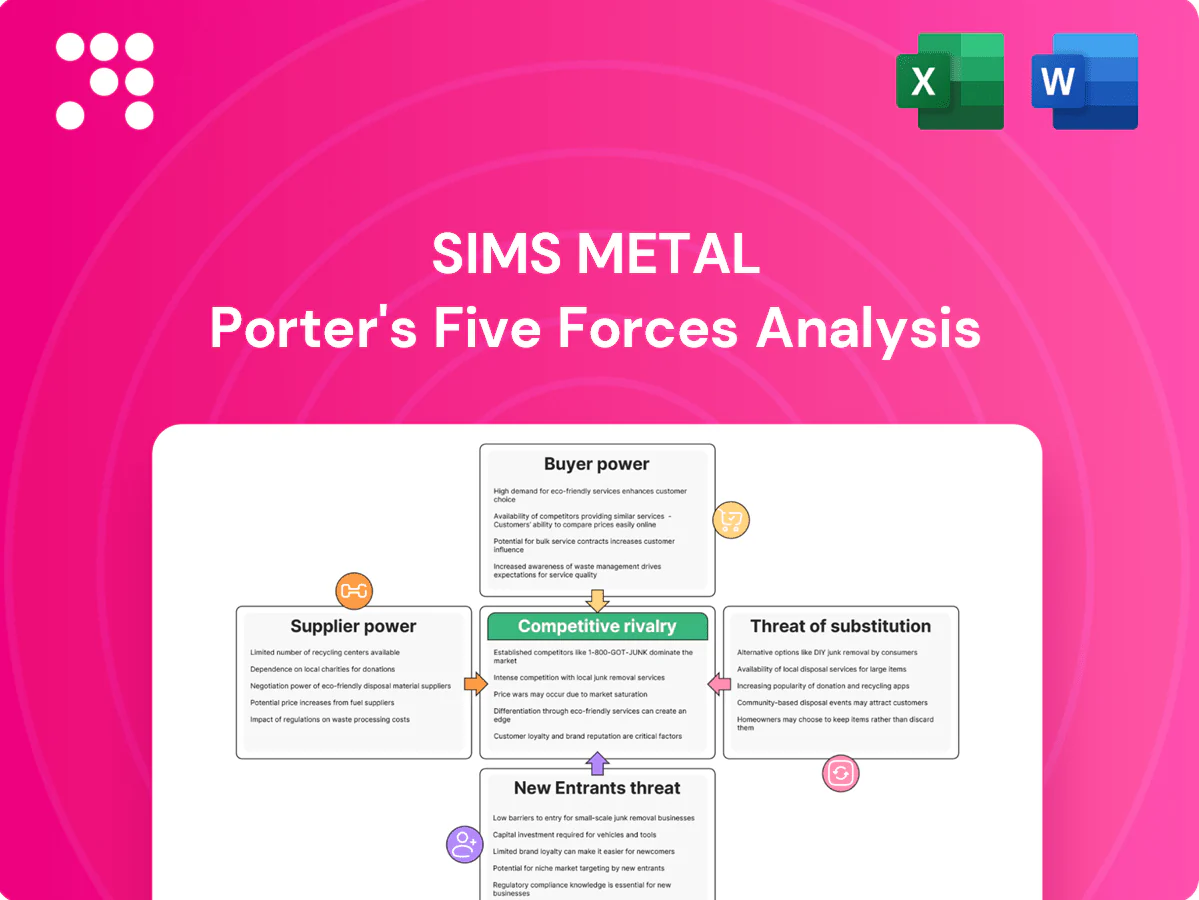

Sims Metal’s Porter's Five Forces snapshot highlights competitive intensity, buyer and supplier leverage, substitute risks, and barriers to entry across global scrap and recycling markets. This concise view teases strategic vulnerabilities and opportunities—unlock the full report for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Fragmented scrap sources

Supply is dispersed across households, dealers, demolition firms and industrial generators, with global ferrous scrap trade around 110 million tonnes in 2023–24, limiting coordinated pricing leverage and supporting Sims’ procurement terms.

Quality and contamination risk

Inconsistent scrap quality raises processing costs and yield uncertainty, with contamination often cutting recovered metal yields by up to 10% and increasing downstream processing costs; cleaner, presorted material commanded premiums of around 10–15% in 2024. Sims mitigates supplier power via global scale, onsite testing and pricing differentials, and has increased investments in sorting technology—reducing reliance on supplier diligence.

Logistics and proximity

In 2024 transport costs kept scrap largely regional, giving nearby suppliers leverage as hauling often dominates margin. Local scarcity within tight radii can sharply elevate supplier power. Sims’ dense facility network and mobile shears in 2024 improved reach and sourcing optionality. Back-to-back logistics and route optimization reduced supplier bargaining strength by lowering empty miles and turnaround time.

Industrial contract suppliers

Industrial contract suppliers—large manufacturers and demolition primes—lock multi-year scrap offtakes, concentrating volume and increasing supplier bargaining power. Sims mitigates this through bundled services (bins, pickups, reporting) and price indexation clauses, which lower spot exposure but compress margins during cyclical booms. Contract stickiness secures flow yet limits upside in tight markets.

- Volume concentration raises supplier leverage

- Service bundles reduce churn and sustain contracts

- Price indexation shifts market risk but caps upside

- Long-term contracts lower spot volatility, compress margins in booms

Regulatory and ESG factors

Stricter 2024 regulatory and ESG regimes, notably the EU CSRD phased in from 2024, raise supplier compliance costs for hazardous streams like e-waste, shrinking the pool of approved vendors and increasing their bargaining power.

Sims’ established compliance and traceability infrastructure attracts top-tier suppliers, lets the company set higher standards, and uses certifications to formalize terms and limit opportunism.

- CSRD 2024: tighter supply‑chain disclosures

- Approved suppliers: smaller, higher‑value pool

- Certifications: contractual leverage, reduced opportunism

Dispersed 110 Mt scrap, 10–15% clean premiums boost supplier leverage

Supply is dispersed (global ferrous scrap ~110 Mt in 2023–24), limiting coordinated pricing. Contamination cuts yields up to 10% while clean scrap earned 10–15% premiums in 2024, raising supplier leverage. Regional transport gives local suppliers short‑term power; Sims’ network, contracts and CSRD‑led approved vendor lists (2024) mitigate but also concentrate supply.

| Metric | 2023–24 value | Impact |

|---|---|---|

| Global ferrous scrap | 110 Mt | Limits coordinated pricing |

| Yield loss (contamination) | Up to 10% | Raises processing costs |

| Clean scrap premium | 10–15% | Increases supplier pricing power |

| CSRD effect | 2024 | Shrinks approved vendor pool |

What is included in the product

Tailored exclusively for Sims Metal, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market-entry barriers that shape pricing and profitability. It also identifies disruptive threats, substitutes, and strategic levers to protect market share and inform investor or strategic materials.

A concise one-sheet Porter’s Five Forces for Sims Metal that visualizes competitive pressure with a spider chart, customizable for market shifts and regulatory scenarios—ready to copy into pitch decks or integrate into Excel dashboards without macros.

Customers Bargaining Power

Concentrated mill buyers

Steel mills, foundries and smelters buy scrap in large batches and are price‑sophisticated, with top regional mill groups accounting for roughly 70% of demand concentration, boosting their leverage on grades and specs. Index‑linked pricing (e.g., benchmark scrap and steel indices) ties Sims margins to market benchmarks. Sims competes by offering reliability, consistent quality and volume assurance, supporting long‑term mill contracts.

Price transparency

Price transparency is high as 2024 saw daily spot and monthly averages published by SteelBenchmarker, S&P Global Platts and LME-related steel reporting, making headline spreads visible to customers. Buyers can switch suppliers when spreads widen, raising bargaining power. Sims defends margins by competing on logistics, quality and timeliness beyond price. Hedging and blending strategies stabilize supply cost and protect customer relationships during volatility.

Substitution among recyclers

Large industrial buyers frequently dual-source across regional recyclers, limiting price-setting power of any single supplier; switching costs are moderate when material specs are standard. Sims’ 200+ facilities across 15 countries in 2024 reduce supply-disruption risk and raise incumbent advantage. Its value-added services and tailored grades (logistics, processing, certification) increase customer stickiness and blunt substitution pressure.

Demand cyclicality

Demand cyclicality: downcycles in construction and manufacturing weaken buyer urgency, widening customer leverage as mills push for tighter specs and longer payment terms; Sims offsets this by managing mix across ferrous and non‑ferrous and by shifting volumes to export markets, while strict inventory and working‑capital discipline helps soften margin pressure.

- Buyer leverage rises in downcycles

- Mills demand tighter specs, longer terms

- Sims uses mix management and exports

- Inventory/WC discipline cushions margins

ESG-driven procurement

ESG-driven procurement raises the strategic value of low-CO2 recycled metals as buyers prioritize certified, traceable inputs, softening pure price pressure. Sims’ circular-economy credentials improve its negotiating position and allow packaging of data-reporting and compliance services into sales. CSRD phased in 2024 brought ~11,700 companies into enhanced ESG reporting scope, boosting buyer demand for supplier data.

- CSRD 2024: ~11,700 companies in scope

- Traceability/certification moderates price-only bargaining

- Sims bundles reporting/compliance with material supply

Buyers ~70% vs recyclers 200+ sites: price power tempered

Buyers are concentrated—top regional mills account for ~70% of scrap demand—giving large customers strong price leverage, especially in downcycles. High price transparency (daily spot indices) and easy dual-sourcing raise switching power, while Sims’ 200+ facilities in 15 countries, logistics services and low‑CO2 credentials (CSRD scope ~11,700 firms in 2024) blunt pure price pressure.

| Metric | 2024 |

|---|---|

| Mill demand concentration | ~70% |

| Sims footprint | 200+ sites, 15 countries |

| CSRD scope | ~11,700 companies |

Same Document Delivered

Sims Metal Porter's Five Forces Analysis

This preview shows the exact Sims Metal Porter's Five Forces Analysis you'll receive—no mockups or placeholders. The file is fully formatted and ready for download immediately after purchase. What you see here is the final, ready-to-use deliverable for your review and use.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sims Metal’s Porter's Five Forces snapshot highlights competitive intensity, buyer and supplier leverage, substitute risks, and barriers to entry across global scrap and recycling markets. This concise view teases strategic vulnerabilities and opportunities—unlock the full report for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Fragmented scrap sources

Supply is dispersed across households, dealers, demolition firms and industrial generators, with global ferrous scrap trade around 110 million tonnes in 2023–24, limiting coordinated pricing leverage and supporting Sims’ procurement terms.

Quality and contamination risk

Inconsistent scrap quality raises processing costs and yield uncertainty, with contamination often cutting recovered metal yields by up to 10% and increasing downstream processing costs; cleaner, presorted material commanded premiums of around 10–15% in 2024. Sims mitigates supplier power via global scale, onsite testing and pricing differentials, and has increased investments in sorting technology—reducing reliance on supplier diligence.

Logistics and proximity

In 2024 transport costs kept scrap largely regional, giving nearby suppliers leverage as hauling often dominates margin. Local scarcity within tight radii can sharply elevate supplier power. Sims’ dense facility network and mobile shears in 2024 improved reach and sourcing optionality. Back-to-back logistics and route optimization reduced supplier bargaining strength by lowering empty miles and turnaround time.

Industrial contract suppliers

Industrial contract suppliers—large manufacturers and demolition primes—lock multi-year scrap offtakes, concentrating volume and increasing supplier bargaining power. Sims mitigates this through bundled services (bins, pickups, reporting) and price indexation clauses, which lower spot exposure but compress margins during cyclical booms. Contract stickiness secures flow yet limits upside in tight markets.

- Volume concentration raises supplier leverage

- Service bundles reduce churn and sustain contracts

- Price indexation shifts market risk but caps upside

- Long-term contracts lower spot volatility, compress margins in booms

Regulatory and ESG factors

Stricter 2024 regulatory and ESG regimes, notably the EU CSRD phased in from 2024, raise supplier compliance costs for hazardous streams like e-waste, shrinking the pool of approved vendors and increasing their bargaining power.

Sims’ established compliance and traceability infrastructure attracts top-tier suppliers, lets the company set higher standards, and uses certifications to formalize terms and limit opportunism.

- CSRD 2024: tighter supply‑chain disclosures

- Approved suppliers: smaller, higher‑value pool

- Certifications: contractual leverage, reduced opportunism

Dispersed 110 Mt scrap, 10–15% clean premiums boost supplier leverage

Supply is dispersed (global ferrous scrap ~110 Mt in 2023–24), limiting coordinated pricing. Contamination cuts yields up to 10% while clean scrap earned 10–15% premiums in 2024, raising supplier leverage. Regional transport gives local suppliers short‑term power; Sims’ network, contracts and CSRD‑led approved vendor lists (2024) mitigate but also concentrate supply.

| Metric | 2023–24 value | Impact |

|---|---|---|

| Global ferrous scrap | 110 Mt | Limits coordinated pricing |

| Yield loss (contamination) | Up to 10% | Raises processing costs |

| Clean scrap premium | 10–15% | Increases supplier pricing power |

| CSRD effect | 2024 | Shrinks approved vendor pool |

What is included in the product

Tailored exclusively for Sims Metal, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market-entry barriers that shape pricing and profitability. It also identifies disruptive threats, substitutes, and strategic levers to protect market share and inform investor or strategic materials.

A concise one-sheet Porter’s Five Forces for Sims Metal that visualizes competitive pressure with a spider chart, customizable for market shifts and regulatory scenarios—ready to copy into pitch decks or integrate into Excel dashboards without macros.

Customers Bargaining Power

Concentrated mill buyers

Steel mills, foundries and smelters buy scrap in large batches and are price‑sophisticated, with top regional mill groups accounting for roughly 70% of demand concentration, boosting their leverage on grades and specs. Index‑linked pricing (e.g., benchmark scrap and steel indices) ties Sims margins to market benchmarks. Sims competes by offering reliability, consistent quality and volume assurance, supporting long‑term mill contracts.

Price transparency

Price transparency is high as 2024 saw daily spot and monthly averages published by SteelBenchmarker, S&P Global Platts and LME-related steel reporting, making headline spreads visible to customers. Buyers can switch suppliers when spreads widen, raising bargaining power. Sims defends margins by competing on logistics, quality and timeliness beyond price. Hedging and blending strategies stabilize supply cost and protect customer relationships during volatility.

Substitution among recyclers

Large industrial buyers frequently dual-source across regional recyclers, limiting price-setting power of any single supplier; switching costs are moderate when material specs are standard. Sims’ 200+ facilities across 15 countries in 2024 reduce supply-disruption risk and raise incumbent advantage. Its value-added services and tailored grades (logistics, processing, certification) increase customer stickiness and blunt substitution pressure.

Demand cyclicality

Demand cyclicality: downcycles in construction and manufacturing weaken buyer urgency, widening customer leverage as mills push for tighter specs and longer payment terms; Sims offsets this by managing mix across ferrous and non‑ferrous and by shifting volumes to export markets, while strict inventory and working‑capital discipline helps soften margin pressure.

- Buyer leverage rises in downcycles

- Mills demand tighter specs, longer terms

- Sims uses mix management and exports

- Inventory/WC discipline cushions margins

ESG-driven procurement

ESG-driven procurement raises the strategic value of low-CO2 recycled metals as buyers prioritize certified, traceable inputs, softening pure price pressure. Sims’ circular-economy credentials improve its negotiating position and allow packaging of data-reporting and compliance services into sales. CSRD phased in 2024 brought ~11,700 companies into enhanced ESG reporting scope, boosting buyer demand for supplier data.

- CSRD 2024: ~11,700 companies in scope

- Traceability/certification moderates price-only bargaining

- Sims bundles reporting/compliance with material supply

Buyers ~70% vs recyclers 200+ sites: price power tempered

Buyers are concentrated—top regional mills account for ~70% of scrap demand—giving large customers strong price leverage, especially in downcycles. High price transparency (daily spot indices) and easy dual-sourcing raise switching power, while Sims’ 200+ facilities in 15 countries, logistics services and low‑CO2 credentials (CSRD scope ~11,700 firms in 2024) blunt pure price pressure.

| Metric | 2024 |

|---|---|

| Mill demand concentration | ~70% |

| Sims footprint | 200+ sites, 15 countries |

| CSRD scope | ~11,700 companies |

Same Document Delivered

Sims Metal Porter's Five Forces Analysis

This preview shows the exact Sims Metal Porter's Five Forces Analysis you'll receive—no mockups or placeholders. The file is fully formatted and ready for download immediately after purchase. What you see here is the final, ready-to-use deliverable for your review and use.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Sims Metal’s Porter's Five Forces snapshot highlights competitive intensity, buyer and supplier leverage, substitute risks, and barriers to entry across global scrap and recycling markets. This concise view teases strategic vulnerabilities and opportunities—unlock the full report for force-by-force ratings, visuals, and actionable insights to inform investment or strategy.

Suppliers Bargaining Power

Fragmented scrap sources

Supply is dispersed across households, dealers, demolition firms and industrial generators, with global ferrous scrap trade around 110 million tonnes in 2023–24, limiting coordinated pricing leverage and supporting Sims’ procurement terms.

Quality and contamination risk

Inconsistent scrap quality raises processing costs and yield uncertainty, with contamination often cutting recovered metal yields by up to 10% and increasing downstream processing costs; cleaner, presorted material commanded premiums of around 10–15% in 2024. Sims mitigates supplier power via global scale, onsite testing and pricing differentials, and has increased investments in sorting technology—reducing reliance on supplier diligence.

Logistics and proximity

In 2024 transport costs kept scrap largely regional, giving nearby suppliers leverage as hauling often dominates margin. Local scarcity within tight radii can sharply elevate supplier power. Sims’ dense facility network and mobile shears in 2024 improved reach and sourcing optionality. Back-to-back logistics and route optimization reduced supplier bargaining strength by lowering empty miles and turnaround time.

Industrial contract suppliers

Industrial contract suppliers—large manufacturers and demolition primes—lock multi-year scrap offtakes, concentrating volume and increasing supplier bargaining power. Sims mitigates this through bundled services (bins, pickups, reporting) and price indexation clauses, which lower spot exposure but compress margins during cyclical booms. Contract stickiness secures flow yet limits upside in tight markets.

- Volume concentration raises supplier leverage

- Service bundles reduce churn and sustain contracts

- Price indexation shifts market risk but caps upside

- Long-term contracts lower spot volatility, compress margins in booms

Regulatory and ESG factors

Stricter 2024 regulatory and ESG regimes, notably the EU CSRD phased in from 2024, raise supplier compliance costs for hazardous streams like e-waste, shrinking the pool of approved vendors and increasing their bargaining power.

Sims’ established compliance and traceability infrastructure attracts top-tier suppliers, lets the company set higher standards, and uses certifications to formalize terms and limit opportunism.

- CSRD 2024: tighter supply‑chain disclosures

- Approved suppliers: smaller, higher‑value pool

- Certifications: contractual leverage, reduced opportunism

Dispersed 110 Mt scrap, 10–15% clean premiums boost supplier leverage

Supply is dispersed (global ferrous scrap ~110 Mt in 2023–24), limiting coordinated pricing. Contamination cuts yields up to 10% while clean scrap earned 10–15% premiums in 2024, raising supplier leverage. Regional transport gives local suppliers short‑term power; Sims’ network, contracts and CSRD‑led approved vendor lists (2024) mitigate but also concentrate supply.

| Metric | 2023–24 value | Impact |

|---|---|---|

| Global ferrous scrap | 110 Mt | Limits coordinated pricing |

| Yield loss (contamination) | Up to 10% | Raises processing costs |

| Clean scrap premium | 10–15% | Increases supplier pricing power |

| CSRD effect | 2024 | Shrinks approved vendor pool |

What is included in the product

Tailored exclusively for Sims Metal, this Porter's Five Forces analysis uncovers key drivers of competition, buyer and supplier power, and market-entry barriers that shape pricing and profitability. It also identifies disruptive threats, substitutes, and strategic levers to protect market share and inform investor or strategic materials.

A concise one-sheet Porter’s Five Forces for Sims Metal that visualizes competitive pressure with a spider chart, customizable for market shifts and regulatory scenarios—ready to copy into pitch decks or integrate into Excel dashboards without macros.

Customers Bargaining Power

Concentrated mill buyers

Steel mills, foundries and smelters buy scrap in large batches and are price‑sophisticated, with top regional mill groups accounting for roughly 70% of demand concentration, boosting their leverage on grades and specs. Index‑linked pricing (e.g., benchmark scrap and steel indices) ties Sims margins to market benchmarks. Sims competes by offering reliability, consistent quality and volume assurance, supporting long‑term mill contracts.

Price transparency

Price transparency is high as 2024 saw daily spot and monthly averages published by SteelBenchmarker, S&P Global Platts and LME-related steel reporting, making headline spreads visible to customers. Buyers can switch suppliers when spreads widen, raising bargaining power. Sims defends margins by competing on logistics, quality and timeliness beyond price. Hedging and blending strategies stabilize supply cost and protect customer relationships during volatility.

Substitution among recyclers

Large industrial buyers frequently dual-source across regional recyclers, limiting price-setting power of any single supplier; switching costs are moderate when material specs are standard. Sims’ 200+ facilities across 15 countries in 2024 reduce supply-disruption risk and raise incumbent advantage. Its value-added services and tailored grades (logistics, processing, certification) increase customer stickiness and blunt substitution pressure.

Demand cyclicality

Demand cyclicality: downcycles in construction and manufacturing weaken buyer urgency, widening customer leverage as mills push for tighter specs and longer payment terms; Sims offsets this by managing mix across ferrous and non‑ferrous and by shifting volumes to export markets, while strict inventory and working‑capital discipline helps soften margin pressure.

- Buyer leverage rises in downcycles

- Mills demand tighter specs, longer terms

- Sims uses mix management and exports

- Inventory/WC discipline cushions margins

ESG-driven procurement

ESG-driven procurement raises the strategic value of low-CO2 recycled metals as buyers prioritize certified, traceable inputs, softening pure price pressure. Sims’ circular-economy credentials improve its negotiating position and allow packaging of data-reporting and compliance services into sales. CSRD phased in 2024 brought ~11,700 companies into enhanced ESG reporting scope, boosting buyer demand for supplier data.

- CSRD 2024: ~11,700 companies in scope

- Traceability/certification moderates price-only bargaining

- Sims bundles reporting/compliance with material supply

Buyers ~70% vs recyclers 200+ sites: price power tempered

Buyers are concentrated—top regional mills account for ~70% of scrap demand—giving large customers strong price leverage, especially in downcycles. High price transparency (daily spot indices) and easy dual-sourcing raise switching power, while Sims’ 200+ facilities in 15 countries, logistics services and low‑CO2 credentials (CSRD scope ~11,700 firms in 2024) blunt pure price pressure.

| Metric | 2024 |

|---|---|

| Mill demand concentration | ~70% |

| Sims footprint | 200+ sites, 15 countries |

| CSRD scope | ~11,700 companies |

Same Document Delivered

Sims Metal Porter's Five Forces Analysis

This preview shows the exact Sims Metal Porter's Five Forces Analysis you'll receive—no mockups or placeholders. The file is fully formatted and ready for download immediately after purchase. What you see here is the final, ready-to-use deliverable for your review and use.