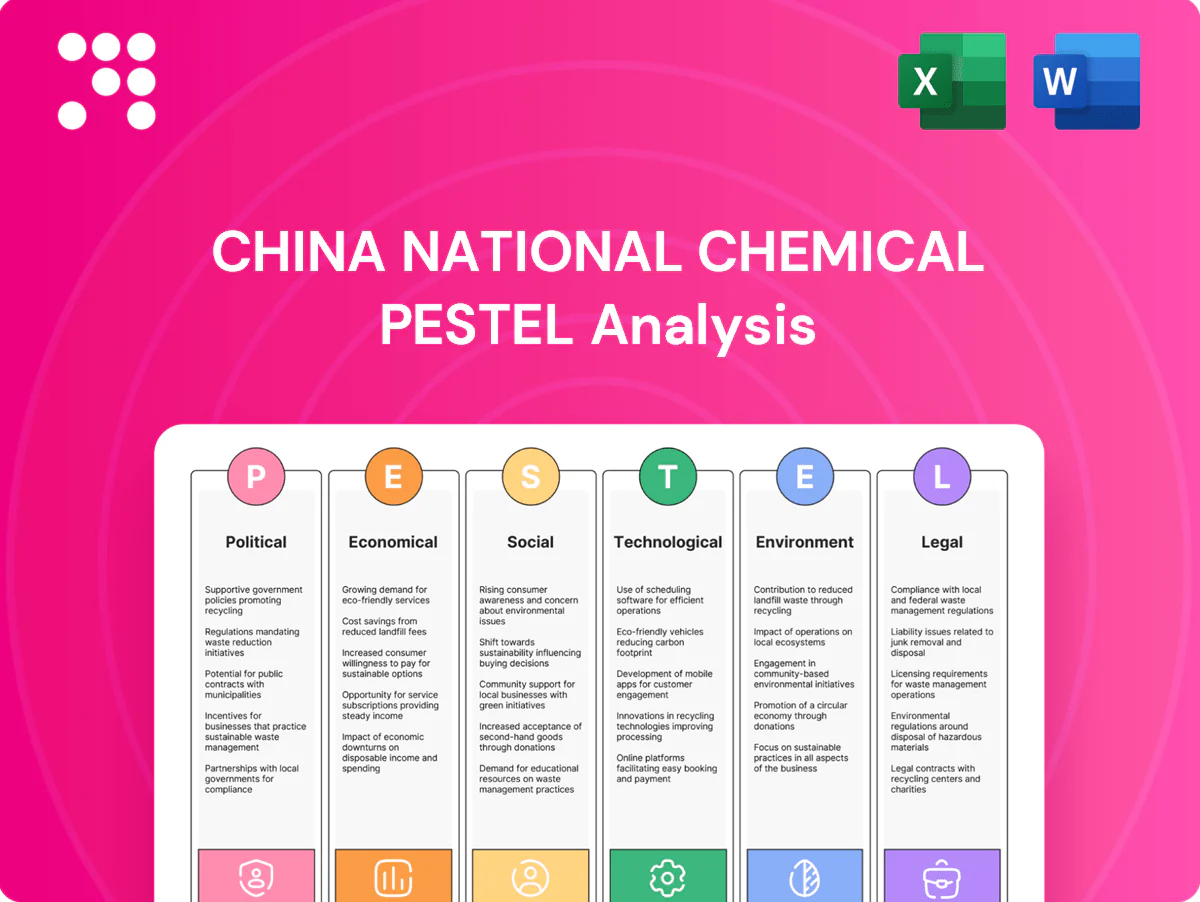

China National Chemical PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the complex external forces shaping China National Chemical with our concise PESTLE analysis—covering regulatory shifts, economic outlook, environmental pressures, and tech disruption. Ideal for investors and strategists who need actionable insight fast. Purchase the full report to access the complete, editable breakdown and make informed decisions today.

Political factors

SOE governance and state directives

As a former centrally managed SOE now under Sinochem Holdings (merger completed in 2021) China National Chemical operates under SASAC oversight, aligning strategy with central industrial policy. Leadership rotations and KPIs track national priorities—self-reliance and grain/food security reiterated in 2024 Central Document No.1—speeding approvals but limiting portfolio pruning. State backing lowers financing spreads yet increases policy-execution obligations.

Geopolitical trade and sanctions exposure

Agrochemicals and advanced materials face rising tariff and export-control risks in US and EU markets, constraining China National Chemical’s access to key end markets. Sanctions screening and counterparties’ de-risking can disrupt cross-border M&A and fragment supply chains, delaying deals and raising compliance costs. Overseas assets must navigate shifting geopolitical sentiments that can impair valuations and market access. Rapid diplomatic shifts can quickly change licensing, customs and reporting burdens.

Rural revitalization and food security agendas

China’s Rural Revitalization and 14th Five-Year Plan (2021–2025) explicitly prioritizes yield resilience and input efficiency, underpinning sustained crop‑protection demand as Beijing targets roughly 95% grain self‑sufficiency; subsidies and extension services often channel support to domestic formulations, bolstering market share for local firms. However, procurement guidance and price caps can compress margins, while tighter green‑agriculture standards and revised pesticide registration rules increasingly determine licensing and market access.

Belt and Road market access

BRI corridors open growth in emerging markets for rubber and chemicals across 149 participating countries, supported by vehicles like the $40 billion Silk Road Fund; this expands downstream demand and project pipelines. Local political risk and currency controls complicate repatriation and working capital, raising FX and sovereign-credit exposure. Government-to-government projects can accelerate entry but increase sovereign risk, so proactive stakeholder engagement is essential to maintain social license abroad.

- BRI reach: 149 countries

- Finance enabler: Silk Road Fund $40 billion

- Risk: currency controls, repatriation issues

- Trade-off: G2G speeds entry but adds sovereign risk

- Mitigation: stakeholder engagement for social license

Industrial policy on strategic materials

China's industrial policy prioritizes upstream security in specialties, batteries and advanced materials, channeling state-backed projects and subsidies into high-end chemical value chains.

Beijing enforces export controls and allocation policies for critical minerals—China produced about 64% of global rare-earth oxides in 2023 (USGS) and accounted for roughly 77% of global lithium-ion battery cell capacity in 2022 (IEA); incentives and quotas favor localization and reduce import dependence.

State control eases approvals; export controls and green rules squeeze agrochemical margins

State control via SASAC/Sinochem (post‑2021) aligns China National Chemical with industrial policy, speeding approvals but constraining divestitures. Export controls, US/EU restrictions and sanctions screening raise compliance costs and can block M&A. Rural Revitalization and 14th FYP sustain agrochem demand while price controls and greener regs squeeze margins.

| Metric | Value |

|---|---|

| BRI countries | 149 |

| Silk Road Fund | $40bn |

| Rare‑earth share (2023, USGS) | 64% |

| Battery cell capacity (2022, IEA) | ~77% |

What is included in the product

Explores how external macro-environmental factors uniquely affect China National Chemical across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and examples tied to its chemicals, agriculture and materials businesses. Designed for executives and investors, the analysis highlights regulatory risks, supply-chain and energy trends, sustainability pressures and strategic opportunities for scenario planning.

Condensed PESTLE analysis of China National Chemical that distills regulatory, economic, social, technological, environmental and legal risks into a single, shareable summary—ideal for fast alignment in meetings, slide decks, or risk workshops.

Economic factors

Cyclical demand and commodity price swings

Feedstock volatility—Brent crude averaged about $86/bbl in 2024—along with naphtha and natural gas swings drives sharp margin variability across CNCC’s petrochemical chains. Agrochemical sales remain seasonal and weather-dependent, peaking in planting seasons and stressing working capital. Rubber and specialty materials track China auto and construction cycles (passenger vehicle sales ~27M in 2024), amplifying cyclicality. Active hedging and flexible production planning are essential to stabilize EBITDA.

Post-merger scale and synergies

Post-merger scale from the ChemChina–Sinochem tie-up created significant purchasing power and logistics efficiencies, with the combined group delivering roughly RMB 600 billion in annual revenue by 2023, enabling volume discounts and consolidated freight savings. Consolidation can lower SG&A and improve capacity utilization across agrochemicals and petrochemical plants. Integration risk centers on overlapping brands and complex ERP harmonization across thousands of SKUs and sites. Realizing procurement and R&D synergies underpins targeted ROIC uplift through centralized sourcing and joint platform R&D.

FX and financing conditions

Revenue booked in diversified currencies exposes CNCC to RMB translation volatility as USD strength persists; rising US rates (federal funds target 5.25–5.50% as of June 2025) increases USD debt servicing for overseas units. SOE status often grants access to lower-cost state financing but draws scrutiny on leverage and contingent liabilities. Active FX hedging and liability matching remain pivotal to protect margins and debt serviceability.

Domestic rebalancing and “dual circulation”

Policy push for dual circulation and import substitution supports higher-value specialty chemicals, aligning with China's 2024 GDP growth of 5.2% (IMF) and industrial upgrading drives; this can widen specialty margins versus commoditized export grades. Slower property and infrastructure activity continues to damp bulk chemical volumes. A portfolio tilt to value-added, consumer-adjacent chemistries reduces exposure to cyclical macro drag.

- Policy: dual circulation, import substitution

- Macro: 2024 GDP 5.2% and weaker property/infrastructure demand

- Strategy: tilt to specialty and consumer-facing chemistries

Global supply-chain reconfiguration

Customers are diversifying sourcing, weighing on China National Chemical export volumes as China accounted for about 28% of global manufacturing output in 2024; nearshoring by multinationals is increasing pressure on China-based production. Building regional hubs in APAC, EMEA and the Americas can defend share and cut logistics risk, while inventory and supplier redundancy push up working capital needs.

- Export risk: diversified buyers

- Nearshoring: pressure on China plants

- Regional hubs: defend share, reduce transit risk

- Working capital: higher inventory and supplier redundancy

State control eases approvals; export controls and green rules squeeze agrochemical margins

Feedstock volatility (Brent ~$86/bbl in 2024) and seasonal agro demand drive margin swings and working-capital strain. Post-merger scale (combined ~RMB 600bn revenue in 2023) cuts procurement and logistics costs but adds integration risk. USD strength and US rates (5.25–5.50% as of Jun 2025) raise FX and debt costs. Policy push to specialty chemistries amid 2024 GDP 5.2% shifts portfolio toward higher-margin segments.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| China GDP 2024 | 5.2% |

| Auto sales 2024 | ~27M |

| Combined revenue 2023 | RMB 600bn |

| US rates Jun 2025 | 5.25–5.50% |

| China manuf share 2024 | 28% |

Preview the Actual Deliverable

China National Chemical PESTLE Analysis

The China National Chemical PESTLE Analysis provides a concise, actionable assessment of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it immediately for strategy, risk assessment, or investor briefing.

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the complex external forces shaping China National Chemical with our concise PESTLE analysis—covering regulatory shifts, economic outlook, environmental pressures, and tech disruption. Ideal for investors and strategists who need actionable insight fast. Purchase the full report to access the complete, editable breakdown and make informed decisions today.

Political factors

SOE governance and state directives

As a former centrally managed SOE now under Sinochem Holdings (merger completed in 2021) China National Chemical operates under SASAC oversight, aligning strategy with central industrial policy. Leadership rotations and KPIs track national priorities—self-reliance and grain/food security reiterated in 2024 Central Document No.1—speeding approvals but limiting portfolio pruning. State backing lowers financing spreads yet increases policy-execution obligations.

Geopolitical trade and sanctions exposure

Agrochemicals and advanced materials face rising tariff and export-control risks in US and EU markets, constraining China National Chemical’s access to key end markets. Sanctions screening and counterparties’ de-risking can disrupt cross-border M&A and fragment supply chains, delaying deals and raising compliance costs. Overseas assets must navigate shifting geopolitical sentiments that can impair valuations and market access. Rapid diplomatic shifts can quickly change licensing, customs and reporting burdens.

Rural revitalization and food security agendas

China’s Rural Revitalization and 14th Five-Year Plan (2021–2025) explicitly prioritizes yield resilience and input efficiency, underpinning sustained crop‑protection demand as Beijing targets roughly 95% grain self‑sufficiency; subsidies and extension services often channel support to domestic formulations, bolstering market share for local firms. However, procurement guidance and price caps can compress margins, while tighter green‑agriculture standards and revised pesticide registration rules increasingly determine licensing and market access.

Belt and Road market access

BRI corridors open growth in emerging markets for rubber and chemicals across 149 participating countries, supported by vehicles like the $40 billion Silk Road Fund; this expands downstream demand and project pipelines. Local political risk and currency controls complicate repatriation and working capital, raising FX and sovereign-credit exposure. Government-to-government projects can accelerate entry but increase sovereign risk, so proactive stakeholder engagement is essential to maintain social license abroad.

- BRI reach: 149 countries

- Finance enabler: Silk Road Fund $40 billion

- Risk: currency controls, repatriation issues

- Trade-off: G2G speeds entry but adds sovereign risk

- Mitigation: stakeholder engagement for social license

Industrial policy on strategic materials

China's industrial policy prioritizes upstream security in specialties, batteries and advanced materials, channeling state-backed projects and subsidies into high-end chemical value chains.

Beijing enforces export controls and allocation policies for critical minerals—China produced about 64% of global rare-earth oxides in 2023 (USGS) and accounted for roughly 77% of global lithium-ion battery cell capacity in 2022 (IEA); incentives and quotas favor localization and reduce import dependence.

State control eases approvals; export controls and green rules squeeze agrochemical margins

State control via SASAC/Sinochem (post‑2021) aligns China National Chemical with industrial policy, speeding approvals but constraining divestitures. Export controls, US/EU restrictions and sanctions screening raise compliance costs and can block M&A. Rural Revitalization and 14th FYP sustain agrochem demand while price controls and greener regs squeeze margins.

| Metric | Value |

|---|---|

| BRI countries | 149 |

| Silk Road Fund | $40bn |

| Rare‑earth share (2023, USGS) | 64% |

| Battery cell capacity (2022, IEA) | ~77% |

What is included in the product

Explores how external macro-environmental factors uniquely affect China National Chemical across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and examples tied to its chemicals, agriculture and materials businesses. Designed for executives and investors, the analysis highlights regulatory risks, supply-chain and energy trends, sustainability pressures and strategic opportunities for scenario planning.

Condensed PESTLE analysis of China National Chemical that distills regulatory, economic, social, technological, environmental and legal risks into a single, shareable summary—ideal for fast alignment in meetings, slide decks, or risk workshops.

Economic factors

Cyclical demand and commodity price swings

Feedstock volatility—Brent crude averaged about $86/bbl in 2024—along with naphtha and natural gas swings drives sharp margin variability across CNCC’s petrochemical chains. Agrochemical sales remain seasonal and weather-dependent, peaking in planting seasons and stressing working capital. Rubber and specialty materials track China auto and construction cycles (passenger vehicle sales ~27M in 2024), amplifying cyclicality. Active hedging and flexible production planning are essential to stabilize EBITDA.

Post-merger scale and synergies

Post-merger scale from the ChemChina–Sinochem tie-up created significant purchasing power and logistics efficiencies, with the combined group delivering roughly RMB 600 billion in annual revenue by 2023, enabling volume discounts and consolidated freight savings. Consolidation can lower SG&A and improve capacity utilization across agrochemicals and petrochemical plants. Integration risk centers on overlapping brands and complex ERP harmonization across thousands of SKUs and sites. Realizing procurement and R&D synergies underpins targeted ROIC uplift through centralized sourcing and joint platform R&D.

FX and financing conditions

Revenue booked in diversified currencies exposes CNCC to RMB translation volatility as USD strength persists; rising US rates (federal funds target 5.25–5.50% as of June 2025) increases USD debt servicing for overseas units. SOE status often grants access to lower-cost state financing but draws scrutiny on leverage and contingent liabilities. Active FX hedging and liability matching remain pivotal to protect margins and debt serviceability.

Domestic rebalancing and “dual circulation”

Policy push for dual circulation and import substitution supports higher-value specialty chemicals, aligning with China's 2024 GDP growth of 5.2% (IMF) and industrial upgrading drives; this can widen specialty margins versus commoditized export grades. Slower property and infrastructure activity continues to damp bulk chemical volumes. A portfolio tilt to value-added, consumer-adjacent chemistries reduces exposure to cyclical macro drag.

- Policy: dual circulation, import substitution

- Macro: 2024 GDP 5.2% and weaker property/infrastructure demand

- Strategy: tilt to specialty and consumer-facing chemistries

Global supply-chain reconfiguration

Customers are diversifying sourcing, weighing on China National Chemical export volumes as China accounted for about 28% of global manufacturing output in 2024; nearshoring by multinationals is increasing pressure on China-based production. Building regional hubs in APAC, EMEA and the Americas can defend share and cut logistics risk, while inventory and supplier redundancy push up working capital needs.

- Export risk: diversified buyers

- Nearshoring: pressure on China plants

- Regional hubs: defend share, reduce transit risk

- Working capital: higher inventory and supplier redundancy

State control eases approvals; export controls and green rules squeeze agrochemical margins

Feedstock volatility (Brent ~$86/bbl in 2024) and seasonal agro demand drive margin swings and working-capital strain. Post-merger scale (combined ~RMB 600bn revenue in 2023) cuts procurement and logistics costs but adds integration risk. USD strength and US rates (5.25–5.50% as of Jun 2025) raise FX and debt costs. Policy push to specialty chemistries amid 2024 GDP 5.2% shifts portfolio toward higher-margin segments.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| China GDP 2024 | 5.2% |

| Auto sales 2024 | ~27M |

| Combined revenue 2023 | RMB 600bn |

| US rates Jun 2025 | 5.25–5.50% |

| China manuf share 2024 | 28% |

Preview the Actual Deliverable

China National Chemical PESTLE Analysis

The China National Chemical PESTLE Analysis provides a concise, actionable assessment of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it immediately for strategy, risk assessment, or investor briefing.

Description

Plan Smarter. Present Sharper. Compete Stronger.

Navigate the complex external forces shaping China National Chemical with our concise PESTLE analysis—covering regulatory shifts, economic outlook, environmental pressures, and tech disruption. Ideal for investors and strategists who need actionable insight fast. Purchase the full report to access the complete, editable breakdown and make informed decisions today.

Political factors

SOE governance and state directives

As a former centrally managed SOE now under Sinochem Holdings (merger completed in 2021) China National Chemical operates under SASAC oversight, aligning strategy with central industrial policy. Leadership rotations and KPIs track national priorities—self-reliance and grain/food security reiterated in 2024 Central Document No.1—speeding approvals but limiting portfolio pruning. State backing lowers financing spreads yet increases policy-execution obligations.

Geopolitical trade and sanctions exposure

Agrochemicals and advanced materials face rising tariff and export-control risks in US and EU markets, constraining China National Chemical’s access to key end markets. Sanctions screening and counterparties’ de-risking can disrupt cross-border M&A and fragment supply chains, delaying deals and raising compliance costs. Overseas assets must navigate shifting geopolitical sentiments that can impair valuations and market access. Rapid diplomatic shifts can quickly change licensing, customs and reporting burdens.

Rural revitalization and food security agendas

China’s Rural Revitalization and 14th Five-Year Plan (2021–2025) explicitly prioritizes yield resilience and input efficiency, underpinning sustained crop‑protection demand as Beijing targets roughly 95% grain self‑sufficiency; subsidies and extension services often channel support to domestic formulations, bolstering market share for local firms. However, procurement guidance and price caps can compress margins, while tighter green‑agriculture standards and revised pesticide registration rules increasingly determine licensing and market access.

Belt and Road market access

BRI corridors open growth in emerging markets for rubber and chemicals across 149 participating countries, supported by vehicles like the $40 billion Silk Road Fund; this expands downstream demand and project pipelines. Local political risk and currency controls complicate repatriation and working capital, raising FX and sovereign-credit exposure. Government-to-government projects can accelerate entry but increase sovereign risk, so proactive stakeholder engagement is essential to maintain social license abroad.

- BRI reach: 149 countries

- Finance enabler: Silk Road Fund $40 billion

- Risk: currency controls, repatriation issues

- Trade-off: G2G speeds entry but adds sovereign risk

- Mitigation: stakeholder engagement for social license

Industrial policy on strategic materials

China's industrial policy prioritizes upstream security in specialties, batteries and advanced materials, channeling state-backed projects and subsidies into high-end chemical value chains.

Beijing enforces export controls and allocation policies for critical minerals—China produced about 64% of global rare-earth oxides in 2023 (USGS) and accounted for roughly 77% of global lithium-ion battery cell capacity in 2022 (IEA); incentives and quotas favor localization and reduce import dependence.

State control eases approvals; export controls and green rules squeeze agrochemical margins

State control via SASAC/Sinochem (post‑2021) aligns China National Chemical with industrial policy, speeding approvals but constraining divestitures. Export controls, US/EU restrictions and sanctions screening raise compliance costs and can block M&A. Rural Revitalization and 14th FYP sustain agrochem demand while price controls and greener regs squeeze margins.

| Metric | Value |

|---|---|

| BRI countries | 149 |

| Silk Road Fund | $40bn |

| Rare‑earth share (2023, USGS) | 64% |

| Battery cell capacity (2022, IEA) | ~77% |

What is included in the product

Explores how external macro-environmental factors uniquely affect China National Chemical across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven subpoints and examples tied to its chemicals, agriculture and materials businesses. Designed for executives and investors, the analysis highlights regulatory risks, supply-chain and energy trends, sustainability pressures and strategic opportunities for scenario planning.

Condensed PESTLE analysis of China National Chemical that distills regulatory, economic, social, technological, environmental and legal risks into a single, shareable summary—ideal for fast alignment in meetings, slide decks, or risk workshops.

Economic factors

Cyclical demand and commodity price swings

Feedstock volatility—Brent crude averaged about $86/bbl in 2024—along with naphtha and natural gas swings drives sharp margin variability across CNCC’s petrochemical chains. Agrochemical sales remain seasonal and weather-dependent, peaking in planting seasons and stressing working capital. Rubber and specialty materials track China auto and construction cycles (passenger vehicle sales ~27M in 2024), amplifying cyclicality. Active hedging and flexible production planning are essential to stabilize EBITDA.

Post-merger scale and synergies

Post-merger scale from the ChemChina–Sinochem tie-up created significant purchasing power and logistics efficiencies, with the combined group delivering roughly RMB 600 billion in annual revenue by 2023, enabling volume discounts and consolidated freight savings. Consolidation can lower SG&A and improve capacity utilization across agrochemicals and petrochemical plants. Integration risk centers on overlapping brands and complex ERP harmonization across thousands of SKUs and sites. Realizing procurement and R&D synergies underpins targeted ROIC uplift through centralized sourcing and joint platform R&D.

FX and financing conditions

Revenue booked in diversified currencies exposes CNCC to RMB translation volatility as USD strength persists; rising US rates (federal funds target 5.25–5.50% as of June 2025) increases USD debt servicing for overseas units. SOE status often grants access to lower-cost state financing but draws scrutiny on leverage and contingent liabilities. Active FX hedging and liability matching remain pivotal to protect margins and debt serviceability.

Domestic rebalancing and “dual circulation”

Policy push for dual circulation and import substitution supports higher-value specialty chemicals, aligning with China's 2024 GDP growth of 5.2% (IMF) and industrial upgrading drives; this can widen specialty margins versus commoditized export grades. Slower property and infrastructure activity continues to damp bulk chemical volumes. A portfolio tilt to value-added, consumer-adjacent chemistries reduces exposure to cyclical macro drag.

- Policy: dual circulation, import substitution

- Macro: 2024 GDP 5.2% and weaker property/infrastructure demand

- Strategy: tilt to specialty and consumer-facing chemistries

Global supply-chain reconfiguration

Customers are diversifying sourcing, weighing on China National Chemical export volumes as China accounted for about 28% of global manufacturing output in 2024; nearshoring by multinationals is increasing pressure on China-based production. Building regional hubs in APAC, EMEA and the Americas can defend share and cut logistics risk, while inventory and supplier redundancy push up working capital needs.

- Export risk: diversified buyers

- Nearshoring: pressure on China plants

- Regional hubs: defend share, reduce transit risk

- Working capital: higher inventory and supplier redundancy

State control eases approvals; export controls and green rules squeeze agrochemical margins

Feedstock volatility (Brent ~$86/bbl in 2024) and seasonal agro demand drive margin swings and working-capital strain. Post-merger scale (combined ~RMB 600bn revenue in 2023) cuts procurement and logistics costs but adds integration risk. USD strength and US rates (5.25–5.50% as of Jun 2025) raise FX and debt costs. Policy push to specialty chemistries amid 2024 GDP 5.2% shifts portfolio toward higher-margin segments.

| Metric | Value |

|---|---|

| Brent 2024 | $86/bbl |

| China GDP 2024 | 5.2% |

| Auto sales 2024 | ~27M |

| Combined revenue 2023 | RMB 600bn |

| US rates Jun 2025 | 5.25–5.50% |

| China manuf share 2024 | 28% |

Preview the Actual Deliverable

China National Chemical PESTLE Analysis

The China National Chemical PESTLE Analysis provides a concise, actionable assessment of political, economic, social, technological, legal and environmental factors affecting the company. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it immediately for strategy, risk assessment, or investor briefing.