Bank SinoPac PESTLE Analysis

Your Competitive Advantage Starts with This Report

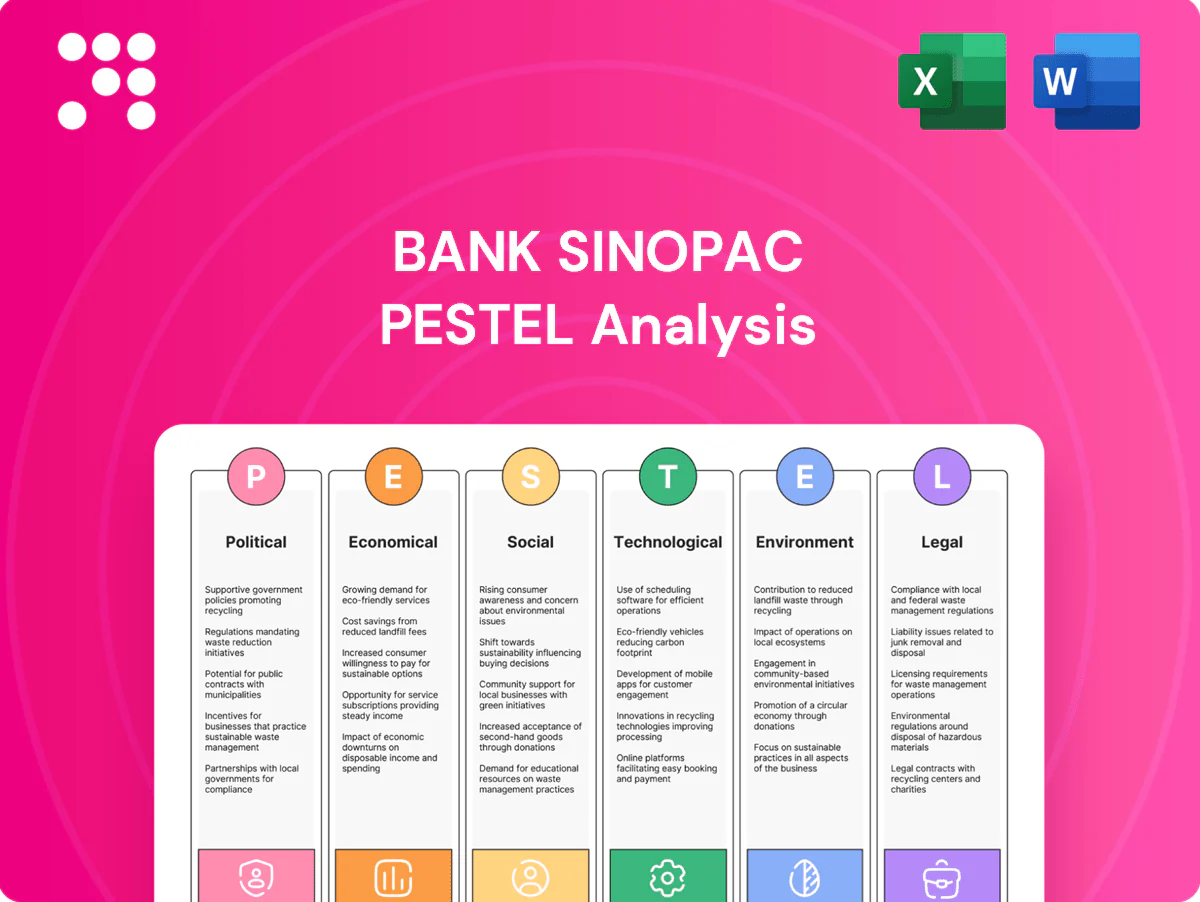

Explore how political, economic, social, technological, legal, and environmental forces are shaping Bank SinoPac’s strategy and risk profile in our targeted PESTLE Analysis. This concise brief highlights key external drivers and investment implications to inform smarter decisions. Purchase the full report for the complete, editable deep-dive and actionable recommendations.

Political factors

Regulatory stability in Taiwan

The Central Bank of the Republic of China (established 1924) and the Financial Supervisory Commission (established 2004) provide a relatively predictable policy environment for commercial banks, supporting long-term planning for deposits, lending and wealth products. Periodic macroprudential tweaks have in recent years influenced mortgage and consumer credit growth. Proactive compliance and early policy monitoring reduce operational disruption.

Cross-strait geopolitical risk

Heightened Taiwan–China tensions raise risk premiums and market volatility, pressuring funding costs, FX flows and client risk appetite; China and Hong Kong still account for about 41% of Taiwan exports (2024), amplifying spillovers. Business continuity, liquidity buffers and scenario planning are critical given Taiwan’s foreign-exchange reserves of roughly USD 530–540bn (2024). Diversifying revenue and counterparties mitigates concentration risk.

Government industrial policies

Government push for semiconductors, green energy and strategic manufacturing is raising corporate credit demand; Taiwan's foundry lead—TSMC controls roughly half of global contract chip production—drives large capex financing needs. The 20% renewable electricity target for 2025 focuses green project lending and subsidized deals that Bank SinoPac can align with for loans and ECM mandates. Public–private programs create fee pools but require policy literacy and targeted risk assessment to avoid overexposure to cyclical clusters.

International relations and trade

Shifts in trade agreements reshape corporate clients’ financing needs as Taiwan remains export-dependent, with exports near 60–65% of GDP, increasing demand for trade lines and FX hedging.

Sanctions regimes and AML rules have tightened cross-border payments and correspondent banking after a 2021 ADB estimate of a global trade finance gap around 1.7 trillion USD.

Bank SinoPac must adapt international services to changing corridors and enforce robust KYC in trade finance to prevent compliance breaches and de-risk correspondent relationships.

- exports_share_gdp: ~60–65%

- global_trade_finance_gap: ~1.7T_USD

- priority: strengthened_KYC_and_sanctions_screening

Public sector stimulus and social programs

Public sector stimulus and social programs in Taiwan bolster SME and consumer lending, with SMEs comprising about 98% of enterprises and Taiwan population ~23.5 million, so government measures can materially expand Bank SinoPac’s loan book and fee income; participation in government-backed schemes increases community impact and reputational capital while requiring pricing that reflects guarantee coverage and program terms.

- Operational readiness speeds deployment and client satisfaction

- Pricing must mirror guarantee structures and tenure

- High SME share (~98%) magnifies policy effects

Regulatory predictability and macroprudential tweaks shape credit; Taiwan tensions boost FX, lending

Predictable regulator framework (CBC, FSC) supports planning but macroprudential tweaks affect mortgage/consumer credit; compliance shortens disruption. Taiwan–China tensions raise funding and FX volatility; FX reserves ~USD 535bn (2024). Policy push into semiconductors and green energy (TSMC ~50% foundry; 20% renewables target 2025) drives corporate lending demand.

| Indicator | Value |

|---|---|

| FX reserves | ~USD 535bn (2024) |

| Exports share GDP | 60–65% |

| China/HK share exports | ~41% (2024) |

| TSMC foundry share | ~50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank SinoPac across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed insights, forward-looking scenarios and actionable implications for executives, investors and strategists.

A concise, visually segmented PESTLE overview of Bank SinoPac that distills external risks and opportunities for quick inclusion in presentations or planning sessions, with editable notes for team-specific context and easy sharing across devices.

Economic factors

Interest rate cycle impact

Policy rate moves (US fed funds 5.25–5.50% in 2024–25) drive Bank SinoPac’s NIM via loan repricing timing; slower deposit repricing raises deposit beta and compresses spreads. Active deposit beta management is vital to protect margins. Hedging and balance-sheet duration strategies stabilize earnings, and stress tests should model sharp 200–300 bps rate shocks.

Export-driven cyclicality

Taiwan’s economy, with exports roughly two-thirds of GDP, is tightly tied to global tech and trade cycles. Semiconductor dominance (TSMC >50% global foundry share) makes downturns cut corporate borrowing and fee income, while recoveries lift lending and transaction fees. Sectoral diversification and working-capital products aligned to inventory and receivable swings help smooth Bank SinoPac’s revenue.

Property market dynamics

Housing policies and price trends directly shape mortgage growth and credit risk for Bank SinoPac, with LTV/LTI caps constraining origination volumes and lowering risk-weighted assets; prudent underwriting and tighter debt-service assessments mitigate cyclical corrections. Cross-selling protection and investment products helps diversify fee income and stabilize margins amid housing market shifts.

FX volatility and dollar liquidity

NTD/USD moved roughly between 29.5–33.0 since 2022, increasing corporates’ hedging needs and causing swings in banks’ FX trading income. Adequate FX liquidity and collateral channels, supported by Taiwan’s ~550bn USD reserves (2024), are essential. Offering structured hedges deepens client relationships while strict risk limits curb P&L swings in stressed markets.

- FX-volatility: NTD/USD 29.5–33.0

- Reserves: ~550bn USD

- Structured hedges: client retention

- Risk limits: P&L shock absorption

Inflation and household income

Cost-of-living shifts—Taiwan CPI eased to about 1.9% in 2024 (DGBAS)—reshape savings and consumption, pressuring real incomes and boosting fee sensitivity among retail clients. Bank SinoPac must use tailored pricing, value bundles and proactive cross-sell to preserve deposits and cards revenue. Credit scoring models should incorporate updated affordability metrics and frequent income shocks monitoring.

- Inflation: Taiwan CPI ~1.9% (2024, DGBAS)

- Behavior: higher fee sensitivity, lower discretionary spend

- Action: targeted pricing, bundles, dynamic affordability in credit scoring

Regulatory predictability and macroprudential tweaks shape credit; Taiwan tensions boost FX, lending

Policy rates (US fed funds 5.25–5.50% in 2024–25) drive NIM via loan/deposit repricing timing; hedging and duration management plus 200–300bps stress tests protect margins. Taiwan GDP tied to exports (semiconductors; TSMC >50% foundry share) so trade cycles shift loan demand and fees. Housing LTV/LTI caps constrain mortgage growth and credit risk. FX swings (NTD/USD 29.5–33.0) raise hedging demand; reserves ~550bn USD.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (2024–25) |

| Taiwan CPI | ~1.9% (2024) |

| NTD/USD | 29.5–33.0 (since 2022) |

| FX reserves | ~550bn USD (2024) |

| TSMC foundry share | >50% |

Preview the Actual Deliverable

Bank SinoPac PESTLE Analysis

The preview of the Bank SinoPac PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers, delivered exactly as displayed. After payment you’ll be able to download this same, professionally structured file immediately.

Your Competitive Advantage Starts with This Report

Explore how political, economic, social, technological, legal, and environmental forces are shaping Bank SinoPac’s strategy and risk profile in our targeted PESTLE Analysis. This concise brief highlights key external drivers and investment implications to inform smarter decisions. Purchase the full report for the complete, editable deep-dive and actionable recommendations.

Political factors

Regulatory stability in Taiwan

The Central Bank of the Republic of China (established 1924) and the Financial Supervisory Commission (established 2004) provide a relatively predictable policy environment for commercial banks, supporting long-term planning for deposits, lending and wealth products. Periodic macroprudential tweaks have in recent years influenced mortgage and consumer credit growth. Proactive compliance and early policy monitoring reduce operational disruption.

Cross-strait geopolitical risk

Heightened Taiwan–China tensions raise risk premiums and market volatility, pressuring funding costs, FX flows and client risk appetite; China and Hong Kong still account for about 41% of Taiwan exports (2024), amplifying spillovers. Business continuity, liquidity buffers and scenario planning are critical given Taiwan’s foreign-exchange reserves of roughly USD 530–540bn (2024). Diversifying revenue and counterparties mitigates concentration risk.

Government industrial policies

Government push for semiconductors, green energy and strategic manufacturing is raising corporate credit demand; Taiwan's foundry lead—TSMC controls roughly half of global contract chip production—drives large capex financing needs. The 20% renewable electricity target for 2025 focuses green project lending and subsidized deals that Bank SinoPac can align with for loans and ECM mandates. Public–private programs create fee pools but require policy literacy and targeted risk assessment to avoid overexposure to cyclical clusters.

International relations and trade

Shifts in trade agreements reshape corporate clients’ financing needs as Taiwan remains export-dependent, with exports near 60–65% of GDP, increasing demand for trade lines and FX hedging.

Sanctions regimes and AML rules have tightened cross-border payments and correspondent banking after a 2021 ADB estimate of a global trade finance gap around 1.7 trillion USD.

Bank SinoPac must adapt international services to changing corridors and enforce robust KYC in trade finance to prevent compliance breaches and de-risk correspondent relationships.

- exports_share_gdp: ~60–65%

- global_trade_finance_gap: ~1.7T_USD

- priority: strengthened_KYC_and_sanctions_screening

Public sector stimulus and social programs

Public sector stimulus and social programs in Taiwan bolster SME and consumer lending, with SMEs comprising about 98% of enterprises and Taiwan population ~23.5 million, so government measures can materially expand Bank SinoPac’s loan book and fee income; participation in government-backed schemes increases community impact and reputational capital while requiring pricing that reflects guarantee coverage and program terms.

- Operational readiness speeds deployment and client satisfaction

- Pricing must mirror guarantee structures and tenure

- High SME share (~98%) magnifies policy effects

Regulatory predictability and macroprudential tweaks shape credit; Taiwan tensions boost FX, lending

Predictable regulator framework (CBC, FSC) supports planning but macroprudential tweaks affect mortgage/consumer credit; compliance shortens disruption. Taiwan–China tensions raise funding and FX volatility; FX reserves ~USD 535bn (2024). Policy push into semiconductors and green energy (TSMC ~50% foundry; 20% renewables target 2025) drives corporate lending demand.

| Indicator | Value |

|---|---|

| FX reserves | ~USD 535bn (2024) |

| Exports share GDP | 60–65% |

| China/HK share exports | ~41% (2024) |

| TSMC foundry share | ~50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank SinoPac across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed insights, forward-looking scenarios and actionable implications for executives, investors and strategists.

A concise, visually segmented PESTLE overview of Bank SinoPac that distills external risks and opportunities for quick inclusion in presentations or planning sessions, with editable notes for team-specific context and easy sharing across devices.

Economic factors

Interest rate cycle impact

Policy rate moves (US fed funds 5.25–5.50% in 2024–25) drive Bank SinoPac’s NIM via loan repricing timing; slower deposit repricing raises deposit beta and compresses spreads. Active deposit beta management is vital to protect margins. Hedging and balance-sheet duration strategies stabilize earnings, and stress tests should model sharp 200–300 bps rate shocks.

Export-driven cyclicality

Taiwan’s economy, with exports roughly two-thirds of GDP, is tightly tied to global tech and trade cycles. Semiconductor dominance (TSMC >50% global foundry share) makes downturns cut corporate borrowing and fee income, while recoveries lift lending and transaction fees. Sectoral diversification and working-capital products aligned to inventory and receivable swings help smooth Bank SinoPac’s revenue.

Property market dynamics

Housing policies and price trends directly shape mortgage growth and credit risk for Bank SinoPac, with LTV/LTI caps constraining origination volumes and lowering risk-weighted assets; prudent underwriting and tighter debt-service assessments mitigate cyclical corrections. Cross-selling protection and investment products helps diversify fee income and stabilize margins amid housing market shifts.

FX volatility and dollar liquidity

NTD/USD moved roughly between 29.5–33.0 since 2022, increasing corporates’ hedging needs and causing swings in banks’ FX trading income. Adequate FX liquidity and collateral channels, supported by Taiwan’s ~550bn USD reserves (2024), are essential. Offering structured hedges deepens client relationships while strict risk limits curb P&L swings in stressed markets.

- FX-volatility: NTD/USD 29.5–33.0

- Reserves: ~550bn USD

- Structured hedges: client retention

- Risk limits: P&L shock absorption

Inflation and household income

Cost-of-living shifts—Taiwan CPI eased to about 1.9% in 2024 (DGBAS)—reshape savings and consumption, pressuring real incomes and boosting fee sensitivity among retail clients. Bank SinoPac must use tailored pricing, value bundles and proactive cross-sell to preserve deposits and cards revenue. Credit scoring models should incorporate updated affordability metrics and frequent income shocks monitoring.

- Inflation: Taiwan CPI ~1.9% (2024, DGBAS)

- Behavior: higher fee sensitivity, lower discretionary spend

- Action: targeted pricing, bundles, dynamic affordability in credit scoring

Regulatory predictability and macroprudential tweaks shape credit; Taiwan tensions boost FX, lending

Policy rates (US fed funds 5.25–5.50% in 2024–25) drive NIM via loan/deposit repricing timing; hedging and duration management plus 200–300bps stress tests protect margins. Taiwan GDP tied to exports (semiconductors; TSMC >50% foundry share) so trade cycles shift loan demand and fees. Housing LTV/LTI caps constrain mortgage growth and credit risk. FX swings (NTD/USD 29.5–33.0) raise hedging demand; reserves ~550bn USD.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (2024–25) |

| Taiwan CPI | ~1.9% (2024) |

| NTD/USD | 29.5–33.0 (since 2022) |

| FX reserves | ~550bn USD (2024) |

| TSMC foundry share | >50% |

Preview the Actual Deliverable

Bank SinoPac PESTLE Analysis

The preview of the Bank SinoPac PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers, delivered exactly as displayed. After payment you’ll be able to download this same, professionally structured file immediately.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Explore how political, economic, social, technological, legal, and environmental forces are shaping Bank SinoPac’s strategy and risk profile in our targeted PESTLE Analysis. This concise brief highlights key external drivers and investment implications to inform smarter decisions. Purchase the full report for the complete, editable deep-dive and actionable recommendations.

Political factors

Regulatory stability in Taiwan

The Central Bank of the Republic of China (established 1924) and the Financial Supervisory Commission (established 2004) provide a relatively predictable policy environment for commercial banks, supporting long-term planning for deposits, lending and wealth products. Periodic macroprudential tweaks have in recent years influenced mortgage and consumer credit growth. Proactive compliance and early policy monitoring reduce operational disruption.

Cross-strait geopolitical risk

Heightened Taiwan–China tensions raise risk premiums and market volatility, pressuring funding costs, FX flows and client risk appetite; China and Hong Kong still account for about 41% of Taiwan exports (2024), amplifying spillovers. Business continuity, liquidity buffers and scenario planning are critical given Taiwan’s foreign-exchange reserves of roughly USD 530–540bn (2024). Diversifying revenue and counterparties mitigates concentration risk.

Government industrial policies

Government push for semiconductors, green energy and strategic manufacturing is raising corporate credit demand; Taiwan's foundry lead—TSMC controls roughly half of global contract chip production—drives large capex financing needs. The 20% renewable electricity target for 2025 focuses green project lending and subsidized deals that Bank SinoPac can align with for loans and ECM mandates. Public–private programs create fee pools but require policy literacy and targeted risk assessment to avoid overexposure to cyclical clusters.

International relations and trade

Shifts in trade agreements reshape corporate clients’ financing needs as Taiwan remains export-dependent, with exports near 60–65% of GDP, increasing demand for trade lines and FX hedging.

Sanctions regimes and AML rules have tightened cross-border payments and correspondent banking after a 2021 ADB estimate of a global trade finance gap around 1.7 trillion USD.

Bank SinoPac must adapt international services to changing corridors and enforce robust KYC in trade finance to prevent compliance breaches and de-risk correspondent relationships.

- exports_share_gdp: ~60–65%

- global_trade_finance_gap: ~1.7T_USD

- priority: strengthened_KYC_and_sanctions_screening

Public sector stimulus and social programs

Public sector stimulus and social programs in Taiwan bolster SME and consumer lending, with SMEs comprising about 98% of enterprises and Taiwan population ~23.5 million, so government measures can materially expand Bank SinoPac’s loan book and fee income; participation in government-backed schemes increases community impact and reputational capital while requiring pricing that reflects guarantee coverage and program terms.

- Operational readiness speeds deployment and client satisfaction

- Pricing must mirror guarantee structures and tenure

- High SME share (~98%) magnifies policy effects

Regulatory predictability and macroprudential tweaks shape credit; Taiwan tensions boost FX, lending

Predictable regulator framework (CBC, FSC) supports planning but macroprudential tweaks affect mortgage/consumer credit; compliance shortens disruption. Taiwan–China tensions raise funding and FX volatility; FX reserves ~USD 535bn (2024). Policy push into semiconductors and green energy (TSMC ~50% foundry; 20% renewables target 2025) drives corporate lending demand.

| Indicator | Value |

|---|---|

| FX reserves | ~USD 535bn (2024) |

| Exports share GDP | 60–65% |

| China/HK share exports | ~41% (2024) |

| TSMC foundry share | ~50% |

What is included in the product

Explores how macro-environmental factors uniquely affect Bank SinoPac across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-backed insights, forward-looking scenarios and actionable implications for executives, investors and strategists.

A concise, visually segmented PESTLE overview of Bank SinoPac that distills external risks and opportunities for quick inclusion in presentations or planning sessions, with editable notes for team-specific context and easy sharing across devices.

Economic factors

Interest rate cycle impact

Policy rate moves (US fed funds 5.25–5.50% in 2024–25) drive Bank SinoPac’s NIM via loan repricing timing; slower deposit repricing raises deposit beta and compresses spreads. Active deposit beta management is vital to protect margins. Hedging and balance-sheet duration strategies stabilize earnings, and stress tests should model sharp 200–300 bps rate shocks.

Export-driven cyclicality

Taiwan’s economy, with exports roughly two-thirds of GDP, is tightly tied to global tech and trade cycles. Semiconductor dominance (TSMC >50% global foundry share) makes downturns cut corporate borrowing and fee income, while recoveries lift lending and transaction fees. Sectoral diversification and working-capital products aligned to inventory and receivable swings help smooth Bank SinoPac’s revenue.

Property market dynamics

Housing policies and price trends directly shape mortgage growth and credit risk for Bank SinoPac, with LTV/LTI caps constraining origination volumes and lowering risk-weighted assets; prudent underwriting and tighter debt-service assessments mitigate cyclical corrections. Cross-selling protection and investment products helps diversify fee income and stabilize margins amid housing market shifts.

FX volatility and dollar liquidity

NTD/USD moved roughly between 29.5–33.0 since 2022, increasing corporates’ hedging needs and causing swings in banks’ FX trading income. Adequate FX liquidity and collateral channels, supported by Taiwan’s ~550bn USD reserves (2024), are essential. Offering structured hedges deepens client relationships while strict risk limits curb P&L swings in stressed markets.

- FX-volatility: NTD/USD 29.5–33.0

- Reserves: ~550bn USD

- Structured hedges: client retention

- Risk limits: P&L shock absorption

Inflation and household income

Cost-of-living shifts—Taiwan CPI eased to about 1.9% in 2024 (DGBAS)—reshape savings and consumption, pressuring real incomes and boosting fee sensitivity among retail clients. Bank SinoPac must use tailored pricing, value bundles and proactive cross-sell to preserve deposits and cards revenue. Credit scoring models should incorporate updated affordability metrics and frequent income shocks monitoring.

- Inflation: Taiwan CPI ~1.9% (2024, DGBAS)

- Behavior: higher fee sensitivity, lower discretionary spend

- Action: targeted pricing, bundles, dynamic affordability in credit scoring

Regulatory predictability and macroprudential tweaks shape credit; Taiwan tensions boost FX, lending

Policy rates (US fed funds 5.25–5.50% in 2024–25) drive NIM via loan/deposit repricing timing; hedging and duration management plus 200–300bps stress tests protect margins. Taiwan GDP tied to exports (semiconductors; TSMC >50% foundry share) so trade cycles shift loan demand and fees. Housing LTV/LTI caps constrain mortgage growth and credit risk. FX swings (NTD/USD 29.5–33.0) raise hedging demand; reserves ~550bn USD.

| Metric | Value |

|---|---|

| Fed funds | 5.25–5.50% (2024–25) |

| Taiwan CPI | ~1.9% (2024) |

| NTD/USD | 29.5–33.0 (since 2022) |

| FX reserves | ~550bn USD (2024) |

| TSMC foundry share | >50% |

Preview the Actual Deliverable

Bank SinoPac PESTLE Analysis

The preview of the Bank SinoPac PESTLE Analysis shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product with no placeholders or teasers, delivered exactly as displayed. After payment you’ll be able to download this same, professionally structured file immediately.