Sinopec Porter's Five Forces Analysis

Don't Miss the Bigger Picture

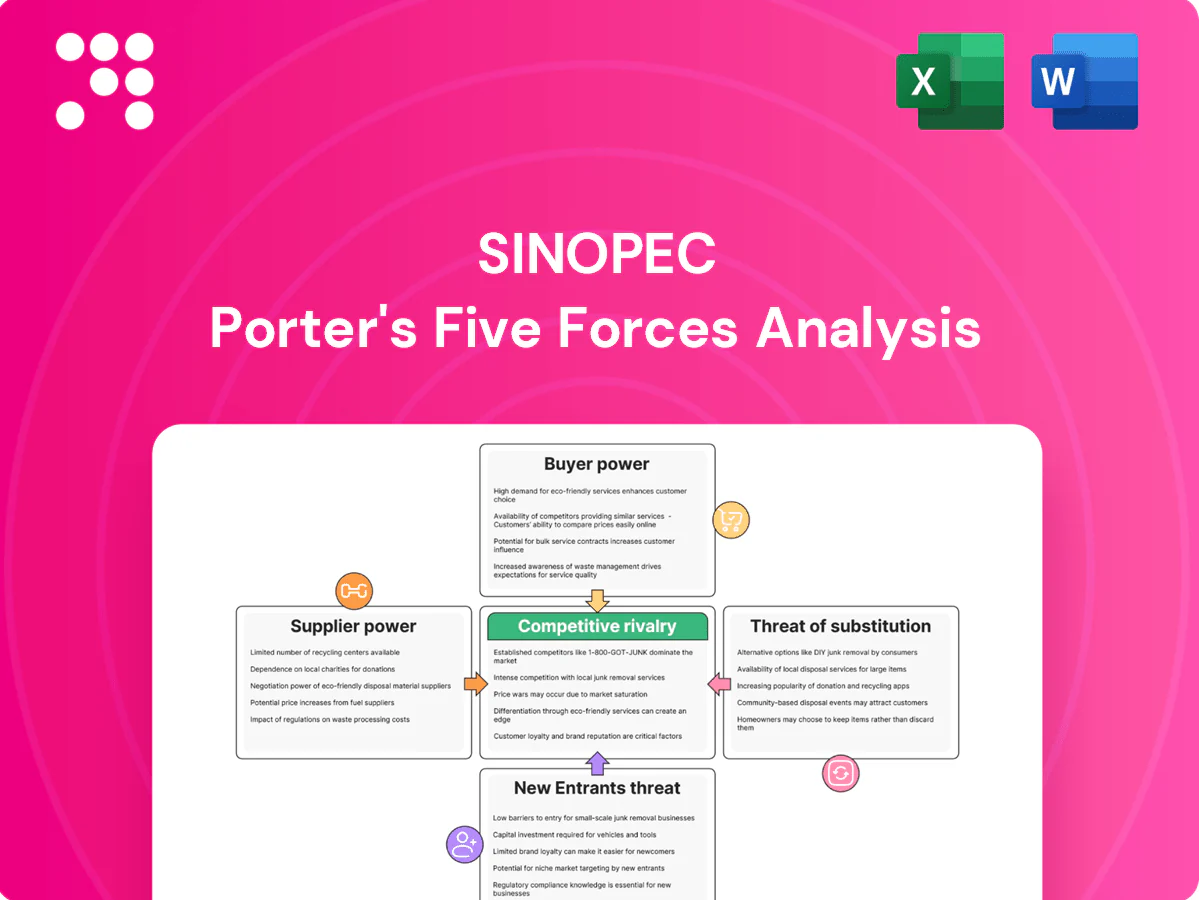

Sinopec faces intense competitive rivalry and significant supplier bargaining power due to upstream oil markets, while buyer power and substitute threats shift with renewable adoption and refining margins. Regulatory and capital barriers temper new entrants but geopolitical risks heighten external pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sinopec’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated crude and gas sources

Upstream crude and gas supply is concentrated: OPEC+ accounted for about 45% of global oil output in 2024 and national oil companies hold roughly 80% of proved hydrocarbon reserves, giving suppliers strong leverage on benchmark-linked pricing and volumes. Sinopec reduces risk via long-term contracts and diversified sourcing, but geopolitical exposure remains. Supply shocks can curtail refining runs and compress margin capture.

Technology and catalyst licensors

Refining and petrochemical units rely on a narrow group of proprietary licensors such as Honeywell UOP, Axens, Lummus and KBR, giving these technology and catalyst providers significant bargaining power due to high switching costs and lengthy qualification timelines.

Sinopec’s substantial in-house R&D and pilot facilities mitigate but do not eliminate dependence on critical licensed processes and specialty catalysts.

License fees, royalty structures and supply terms directly influence project IRRs and plant uptime, making licensors able to materially affect economics and operational continuity.

Oilfield services and equipment

Specialized rigs, subsea equipment and EPC services showed cyclical scarcity in 2024, with high-spec rig utilization near 85% during the upcycle and service firms pushing pricing and tighter terms. Sinopec’s scale and state backing improve its negotiation position—state ownership and integrated supply chains reduced spot spend volatility in 2024. Bottlenecks in ultra-high-end subsea systems persist, though local content strategies have raised domestic sourcing to meaningful levels.

Logistics and storage providers

Pipeline access, port berths and storage tanks are strategic choke points for Sinopec; congestion or limited capacity drives higher fees and tighter scheduling, increasing supplier leverage.

Sinopec’s vertical integration into pipelines and terminals mitigates exposure by securing throughput and storage control.

Despite integration, peak seasonal demand and regional bottlenecks still strain the network and elevate spot logistics costs.

- Chokepoints: pipelines, berths, tanks

- Mitigation: vertical integration into logistics

- Residual risk: seasonal peak congestion

Feedstock quality and compliance

- Feedstock variability increases operating cost and maintenance

- Premiums for preferred grades improve yields, lower fouling

- Refinery complexity adds flexibility but is limited

- Blending and hedging mitigate, not remove, supplier power

Concentration (45%) & tight rigs (85%) push costs

Upstream concentration (OPEC+ ~45% of 2024 output; NOCs ~80% of reserves) and reliance on licensors (UOP, Axens, Lummus, KBR) give suppliers sizable leverage; Sinopec's long-term contracts and integration reduce but do not eliminate exposure. Service tightness (high-spec rig utilization ~85% in 2024) and logistics chokepoints lift costs. Feedstock quality variance raises processing and maintenance spend despite blending and hedging.

| Metric | 2024 | Impact on Sinopec |

|---|---|---|

| OPEC+ share | ~45% | Price/volume leverage |

| NOC reserves | ~80% | Supply control |

| Rig util. | ~85% | Service cost pressure |

What is included in the product

Tailored exclusively for Sinopec, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes and disruptive threats, evaluating how each force shapes pricing, profitability and strategic positioning within the integrated oil & gas market.

One-sheet Porter's Five Forces for Sinopec that highlights supplier, buyer, and competitive pressures at a glance—perfect for quick strategic decisions. Customize intensity, swap data and export slide-ready charts to ease boardroom discussions and integration into broader reports.

Customers Bargaining Power

Industrial and commercial customers

Industrial and commercial customers negotiate hard on volume, quality and delivery, increasingly multi-sourcing to secure margins and continuity; in 2024 these trends remained pronounced across China’s downstream sectors. Sinopec counters with integrated supply, petrochemical feedstock packages and proprietary logistics to lock in contracts and reduce churn. Global price benchmarks such as Platts and ICE in 2024 constrained product differentiation, sustaining buyer leverage.

Retail fuel consumers

Retail fuel demand for Sinopec is highly fragmented and price sensitive, with consumers responding quickly to pump-price changes. China’s NDRC-regulated retail pricing mechanism, with adjustments roughly every 10 working days, caps upside and anchors competitive responses. Sinopec’s nationwide network of over 30,000 service stations and millions of loyalty members improve retention, but low switching costs keep buyer power elevated. Brand and convenience only partially offset this price-driven leverage.

Chemical converters and OEMs

Downstream chemical converters and OEMs wield meaningful bargaining power because formulations can be redesigned or grades switched to alternative suppliers, while global commodity benchmarks such as Platts naphtha and propylene spreads intensify price pressure on Sinopec. Sinopec counters churn with technical service, stabilized quality and application support, and long-term offtake contracts that lock volumes even as margins remain competitive. In 2024 Sinopec emphasized contract sales to secure volume stability amidst volatile spot spreads.

International traders and export markets

When exporting, Sinopec meets sophisticated buyers with strong market intelligence and rapid access to alternatives; China imported roughly 11 million barrels per day of crude in 2024, intensifying buyer leverage. Freight, FX swings and short arbitrage windows can shift negotiating power within days, while certification and EU/US compliance add transactional friction. Competitive tendering routinely compresses spot and contract margins.

- Buyer sophistication: high

- Freight/FX volatility: immediate impact

- Compliance burden: raises costs

- Tendering: margin pressure

Government and public sector

Government policy on energy security and affordability shapes end-prices and allocation for Sinopec, with regulators using caps and subsidies that increase buyer surplus; Brent averaged about 86 USD/bbl in 2024, constraining retail margin pass-through. Sinopec must balance compliance and commercial returns, raising buyer power in regulated segments and limiting pricing flexibility.

- Policy pressure: energy security targets raise state procurement influence

- Regulatory tools: caps/subsidies boost buyer surplus

- Impact: tighter margins and higher customer bargaining power

Buyers multi-source; downstream price-sensitive — China crude ~11 mbpd, Brent 86 USD/bbl

Industrial buyers multi-source and press margins; 2024 downstream demand remained price-sensitive. Retail is fragmented—Sinopec operates >30,000 stations and NDRC adjusts prices ~every 10 working days, but low switching costs persist. Export buyers are sophisticated; China crude imports ~11 mbpd in 2024. Regulatory price caps and Brent ~86 USD/bbl in 2024 limit pass-through.

| Metric | 2024 |

|---|---|

| Stations | 30,000+ |

| China crude imports | ~11 mbpd |

| Brent avg | 86 USD/bbl |

Full Version Awaits

Sinopec Porter's Five Forces Analysis

This Sinopec Porter's Five Forces analysis delivers a concise, professional assessment of industry rivalry, supplier and buyer power, threat of entrants, and substitutes with implications for strategy and valuation. You're viewing the exact document you'll receive upon purchase—fully formatted and ready to download. No placeholders, no samples; this preview equals the final deliverable.

Don't Miss the Bigger Picture

Sinopec faces intense competitive rivalry and significant supplier bargaining power due to upstream oil markets, while buyer power and substitute threats shift with renewable adoption and refining margins. Regulatory and capital barriers temper new entrants but geopolitical risks heighten external pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sinopec’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated crude and gas sources

Upstream crude and gas supply is concentrated: OPEC+ accounted for about 45% of global oil output in 2024 and national oil companies hold roughly 80% of proved hydrocarbon reserves, giving suppliers strong leverage on benchmark-linked pricing and volumes. Sinopec reduces risk via long-term contracts and diversified sourcing, but geopolitical exposure remains. Supply shocks can curtail refining runs and compress margin capture.

Technology and catalyst licensors

Refining and petrochemical units rely on a narrow group of proprietary licensors such as Honeywell UOP, Axens, Lummus and KBR, giving these technology and catalyst providers significant bargaining power due to high switching costs and lengthy qualification timelines.

Sinopec’s substantial in-house R&D and pilot facilities mitigate but do not eliminate dependence on critical licensed processes and specialty catalysts.

License fees, royalty structures and supply terms directly influence project IRRs and plant uptime, making licensors able to materially affect economics and operational continuity.

Oilfield services and equipment

Specialized rigs, subsea equipment and EPC services showed cyclical scarcity in 2024, with high-spec rig utilization near 85% during the upcycle and service firms pushing pricing and tighter terms. Sinopec’s scale and state backing improve its negotiation position—state ownership and integrated supply chains reduced spot spend volatility in 2024. Bottlenecks in ultra-high-end subsea systems persist, though local content strategies have raised domestic sourcing to meaningful levels.

Logistics and storage providers

Pipeline access, port berths and storage tanks are strategic choke points for Sinopec; congestion or limited capacity drives higher fees and tighter scheduling, increasing supplier leverage.

Sinopec’s vertical integration into pipelines and terminals mitigates exposure by securing throughput and storage control.

Despite integration, peak seasonal demand and regional bottlenecks still strain the network and elevate spot logistics costs.

- Chokepoints: pipelines, berths, tanks

- Mitigation: vertical integration into logistics

- Residual risk: seasonal peak congestion

Feedstock quality and compliance

- Feedstock variability increases operating cost and maintenance

- Premiums for preferred grades improve yields, lower fouling

- Refinery complexity adds flexibility but is limited

- Blending and hedging mitigate, not remove, supplier power

Concentration (45%) & tight rigs (85%) push costs

Upstream concentration (OPEC+ ~45% of 2024 output; NOCs ~80% of reserves) and reliance on licensors (UOP, Axens, Lummus, KBR) give suppliers sizable leverage; Sinopec's long-term contracts and integration reduce but do not eliminate exposure. Service tightness (high-spec rig utilization ~85% in 2024) and logistics chokepoints lift costs. Feedstock quality variance raises processing and maintenance spend despite blending and hedging.

| Metric | 2024 | Impact on Sinopec |

|---|---|---|

| OPEC+ share | ~45% | Price/volume leverage |

| NOC reserves | ~80% | Supply control |

| Rig util. | ~85% | Service cost pressure |

What is included in the product

Tailored exclusively for Sinopec, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes and disruptive threats, evaluating how each force shapes pricing, profitability and strategic positioning within the integrated oil & gas market.

One-sheet Porter's Five Forces for Sinopec that highlights supplier, buyer, and competitive pressures at a glance—perfect for quick strategic decisions. Customize intensity, swap data and export slide-ready charts to ease boardroom discussions and integration into broader reports.

Customers Bargaining Power

Industrial and commercial customers

Industrial and commercial customers negotiate hard on volume, quality and delivery, increasingly multi-sourcing to secure margins and continuity; in 2024 these trends remained pronounced across China’s downstream sectors. Sinopec counters with integrated supply, petrochemical feedstock packages and proprietary logistics to lock in contracts and reduce churn. Global price benchmarks such as Platts and ICE in 2024 constrained product differentiation, sustaining buyer leverage.

Retail fuel consumers

Retail fuel demand for Sinopec is highly fragmented and price sensitive, with consumers responding quickly to pump-price changes. China’s NDRC-regulated retail pricing mechanism, with adjustments roughly every 10 working days, caps upside and anchors competitive responses. Sinopec’s nationwide network of over 30,000 service stations and millions of loyalty members improve retention, but low switching costs keep buyer power elevated. Brand and convenience only partially offset this price-driven leverage.

Chemical converters and OEMs

Downstream chemical converters and OEMs wield meaningful bargaining power because formulations can be redesigned or grades switched to alternative suppliers, while global commodity benchmarks such as Platts naphtha and propylene spreads intensify price pressure on Sinopec. Sinopec counters churn with technical service, stabilized quality and application support, and long-term offtake contracts that lock volumes even as margins remain competitive. In 2024 Sinopec emphasized contract sales to secure volume stability amidst volatile spot spreads.

International traders and export markets

When exporting, Sinopec meets sophisticated buyers with strong market intelligence and rapid access to alternatives; China imported roughly 11 million barrels per day of crude in 2024, intensifying buyer leverage. Freight, FX swings and short arbitrage windows can shift negotiating power within days, while certification and EU/US compliance add transactional friction. Competitive tendering routinely compresses spot and contract margins.

- Buyer sophistication: high

- Freight/FX volatility: immediate impact

- Compliance burden: raises costs

- Tendering: margin pressure

Government and public sector

Government policy on energy security and affordability shapes end-prices and allocation for Sinopec, with regulators using caps and subsidies that increase buyer surplus; Brent averaged about 86 USD/bbl in 2024, constraining retail margin pass-through. Sinopec must balance compliance and commercial returns, raising buyer power in regulated segments and limiting pricing flexibility.

- Policy pressure: energy security targets raise state procurement influence

- Regulatory tools: caps/subsidies boost buyer surplus

- Impact: tighter margins and higher customer bargaining power

Buyers multi-source; downstream price-sensitive — China crude ~11 mbpd, Brent 86 USD/bbl

Industrial buyers multi-source and press margins; 2024 downstream demand remained price-sensitive. Retail is fragmented—Sinopec operates >30,000 stations and NDRC adjusts prices ~every 10 working days, but low switching costs persist. Export buyers are sophisticated; China crude imports ~11 mbpd in 2024. Regulatory price caps and Brent ~86 USD/bbl in 2024 limit pass-through.

| Metric | 2024 |

|---|---|

| Stations | 30,000+ |

| China crude imports | ~11 mbpd |

| Brent avg | 86 USD/bbl |

Full Version Awaits

Sinopec Porter's Five Forces Analysis

This Sinopec Porter's Five Forces analysis delivers a concise, professional assessment of industry rivalry, supplier and buyer power, threat of entrants, and substitutes with implications for strategy and valuation. You're viewing the exact document you'll receive upon purchase—fully formatted and ready to download. No placeholders, no samples; this preview equals the final deliverable.

Description

Don't Miss the Bigger Picture

Sinopec faces intense competitive rivalry and significant supplier bargaining power due to upstream oil markets, while buyer power and substitute threats shift with renewable adoption and refining margins. Regulatory and capital barriers temper new entrants but geopolitical risks heighten external pressure. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Sinopec’s competitive dynamics in detail.

Suppliers Bargaining Power

Concentrated crude and gas sources

Upstream crude and gas supply is concentrated: OPEC+ accounted for about 45% of global oil output in 2024 and national oil companies hold roughly 80% of proved hydrocarbon reserves, giving suppliers strong leverage on benchmark-linked pricing and volumes. Sinopec reduces risk via long-term contracts and diversified sourcing, but geopolitical exposure remains. Supply shocks can curtail refining runs and compress margin capture.

Technology and catalyst licensors

Refining and petrochemical units rely on a narrow group of proprietary licensors such as Honeywell UOP, Axens, Lummus and KBR, giving these technology and catalyst providers significant bargaining power due to high switching costs and lengthy qualification timelines.

Sinopec’s substantial in-house R&D and pilot facilities mitigate but do not eliminate dependence on critical licensed processes and specialty catalysts.

License fees, royalty structures and supply terms directly influence project IRRs and plant uptime, making licensors able to materially affect economics and operational continuity.

Oilfield services and equipment

Specialized rigs, subsea equipment and EPC services showed cyclical scarcity in 2024, with high-spec rig utilization near 85% during the upcycle and service firms pushing pricing and tighter terms. Sinopec’s scale and state backing improve its negotiation position—state ownership and integrated supply chains reduced spot spend volatility in 2024. Bottlenecks in ultra-high-end subsea systems persist, though local content strategies have raised domestic sourcing to meaningful levels.

Logistics and storage providers

Pipeline access, port berths and storage tanks are strategic choke points for Sinopec; congestion or limited capacity drives higher fees and tighter scheduling, increasing supplier leverage.

Sinopec’s vertical integration into pipelines and terminals mitigates exposure by securing throughput and storage control.

Despite integration, peak seasonal demand and regional bottlenecks still strain the network and elevate spot logistics costs.

- Chokepoints: pipelines, berths, tanks

- Mitigation: vertical integration into logistics

- Residual risk: seasonal peak congestion

Feedstock quality and compliance

- Feedstock variability increases operating cost and maintenance

- Premiums for preferred grades improve yields, lower fouling

- Refinery complexity adds flexibility but is limited

- Blending and hedging mitigate, not remove, supplier power

Concentration (45%) & tight rigs (85%) push costs

Upstream concentration (OPEC+ ~45% of 2024 output; NOCs ~80% of reserves) and reliance on licensors (UOP, Axens, Lummus, KBR) give suppliers sizable leverage; Sinopec's long-term contracts and integration reduce but do not eliminate exposure. Service tightness (high-spec rig utilization ~85% in 2024) and logistics chokepoints lift costs. Feedstock quality variance raises processing and maintenance spend despite blending and hedging.

| Metric | 2024 | Impact on Sinopec |

|---|---|---|

| OPEC+ share | ~45% | Price/volume leverage |

| NOC reserves | ~80% | Supply control |

| Rig util. | ~85% | Service cost pressure |

What is included in the product

Tailored exclusively for Sinopec, this Porter's Five Forces analysis uncovers key drivers of competition, supplier and buyer power, entry barriers, substitutes and disruptive threats, evaluating how each force shapes pricing, profitability and strategic positioning within the integrated oil & gas market.

One-sheet Porter's Five Forces for Sinopec that highlights supplier, buyer, and competitive pressures at a glance—perfect for quick strategic decisions. Customize intensity, swap data and export slide-ready charts to ease boardroom discussions and integration into broader reports.

Customers Bargaining Power

Industrial and commercial customers

Industrial and commercial customers negotiate hard on volume, quality and delivery, increasingly multi-sourcing to secure margins and continuity; in 2024 these trends remained pronounced across China’s downstream sectors. Sinopec counters with integrated supply, petrochemical feedstock packages and proprietary logistics to lock in contracts and reduce churn. Global price benchmarks such as Platts and ICE in 2024 constrained product differentiation, sustaining buyer leverage.

Retail fuel consumers

Retail fuel demand for Sinopec is highly fragmented and price sensitive, with consumers responding quickly to pump-price changes. China’s NDRC-regulated retail pricing mechanism, with adjustments roughly every 10 working days, caps upside and anchors competitive responses. Sinopec’s nationwide network of over 30,000 service stations and millions of loyalty members improve retention, but low switching costs keep buyer power elevated. Brand and convenience only partially offset this price-driven leverage.

Chemical converters and OEMs

Downstream chemical converters and OEMs wield meaningful bargaining power because formulations can be redesigned or grades switched to alternative suppliers, while global commodity benchmarks such as Platts naphtha and propylene spreads intensify price pressure on Sinopec. Sinopec counters churn with technical service, stabilized quality and application support, and long-term offtake contracts that lock volumes even as margins remain competitive. In 2024 Sinopec emphasized contract sales to secure volume stability amidst volatile spot spreads.

International traders and export markets

When exporting, Sinopec meets sophisticated buyers with strong market intelligence and rapid access to alternatives; China imported roughly 11 million barrels per day of crude in 2024, intensifying buyer leverage. Freight, FX swings and short arbitrage windows can shift negotiating power within days, while certification and EU/US compliance add transactional friction. Competitive tendering routinely compresses spot and contract margins.

- Buyer sophistication: high

- Freight/FX volatility: immediate impact

- Compliance burden: raises costs

- Tendering: margin pressure

Government and public sector

Government policy on energy security and affordability shapes end-prices and allocation for Sinopec, with regulators using caps and subsidies that increase buyer surplus; Brent averaged about 86 USD/bbl in 2024, constraining retail margin pass-through. Sinopec must balance compliance and commercial returns, raising buyer power in regulated segments and limiting pricing flexibility.

- Policy pressure: energy security targets raise state procurement influence

- Regulatory tools: caps/subsidies boost buyer surplus

- Impact: tighter margins and higher customer bargaining power

Buyers multi-source; downstream price-sensitive — China crude ~11 mbpd, Brent 86 USD/bbl

Industrial buyers multi-source and press margins; 2024 downstream demand remained price-sensitive. Retail is fragmented—Sinopec operates >30,000 stations and NDRC adjusts prices ~every 10 working days, but low switching costs persist. Export buyers are sophisticated; China crude imports ~11 mbpd in 2024. Regulatory price caps and Brent ~86 USD/bbl in 2024 limit pass-through.

| Metric | 2024 |

|---|---|

| Stations | 30,000+ |

| China crude imports | ~11 mbpd |

| Brent avg | 86 USD/bbl |

Full Version Awaits

Sinopec Porter's Five Forces Analysis

This Sinopec Porter's Five Forces analysis delivers a concise, professional assessment of industry rivalry, supplier and buyer power, threat of entrants, and substitutes with implications for strategy and valuation. You're viewing the exact document you'll receive upon purchase—fully formatted and ready to download. No placeholders, no samples; this preview equals the final deliverable.