Sinotruk Hong Kong Porter's Five Forces Analysis

From Overview to Strategy Blueprint

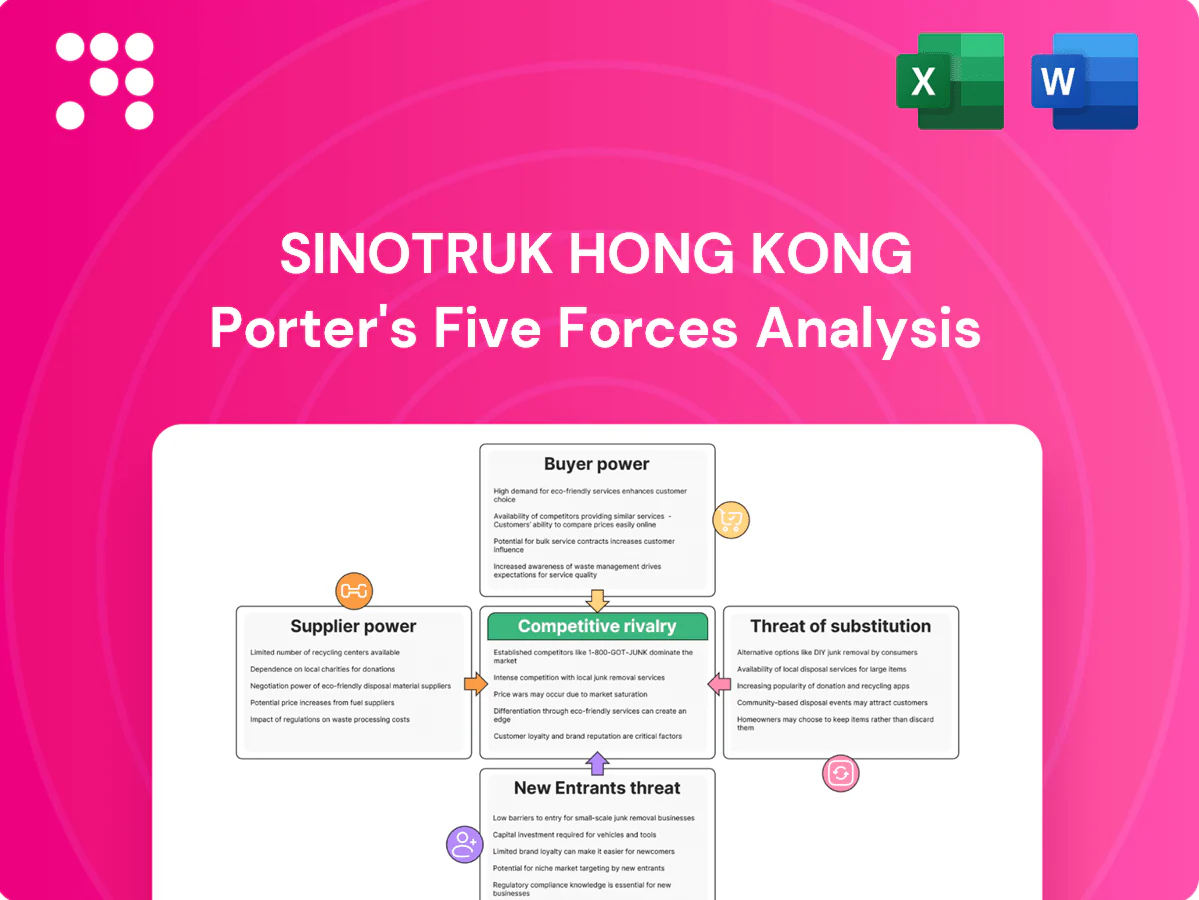

Sinotruk Hong Kong operates within a dynamic heavy-duty truck market, facing significant competitive pressures from established global players and emerging domestic manufacturers. Understanding the intensity of rivalry, the bargaining power of buyers and suppliers, and the threats of new entrants and substitutes is crucial for navigating this landscape.

The complete report reveals the real forces shaping Sinotruk Hong Kong’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Highly specialized components

For critical systems like advanced engine management, braking, or safety technologies, Sinotruk Hong Kong may depend on a limited number of global suppliers. For example, in 2024, the global automotive supplier market saw consolidation, with key players in specialized electronics and powertrain components holding substantial market share.

These suppliers, possessing unique technological expertise and intellectual property, can wield significant pricing power over Sinotruk. This reliance on specialized parts can create bottlenecks or increase costs if alternatives are not readily available, impacting Sinotruk's production efficiency and profitability.

Commodity raw materials price fluctuations

Commodity raw materials like steel and rubber, essential for Sinotruk's heavy-duty trucks, are readily available from numerous suppliers. However, their prices can swing significantly due to global supply and demand dynamics.

In 2024, steel prices experienced notable fluctuations, with benchmarks like hot-rolled coil seeing a roughly 15% increase in the first half of the year before stabilizing. Similarly, natural rubber prices, crucial for tires, saw a 10% rise in early 2024 driven by weather concerns in key producing regions.

While Sinotruk's large-scale procurement offers some negotiation power, substantial hikes in these raw material costs directly impact its production expenses and profit margins. This volatility underscores the importance of robust supply chain management, including strategic sourcing and financial hedging instruments, to buffer against adverse price movements and maintain competitive pricing.

In-house production capabilities for core components

Sinotruk's strategic decision to manufacture its own engines and axles significantly curtails its reliance on external suppliers for these critical components. This vertical integration enhances Sinotruk's leverage by providing more control over the quality, cost, and supply chain reliability of these essential parts.

By producing its core components in-house, Sinotruk effectively diminishes the bargaining power of potential third-party engine and axle manufacturers. For instance, in 2024, Sinotruk's engine production capacity reached over 500,000 units annually, a substantial portion of its total vehicle output, demonstrating a strong commitment to internal manufacturing.

Supplier concentration for high-tech parts

The market for certain high-tech components essential for modern trucks, like advanced electronic control units or specialized battery management systems, can be highly concentrated. This means a limited number of suppliers might dominate the production of these critical parts. For instance, in 2024, the global market for automotive semiconductors, a key high-tech component, was estimated to be worth over $60 billion, with a significant portion of advanced chip production concentrated among a few major players.

When Sinotruk Hong Kong relies on these concentrated suppliers for niche or advanced parts, those suppliers gain considerable bargaining power. This can translate into higher prices for components or stricter supply terms, directly impacting Sinotruk's cost of goods sold and potentially its profit margins. For example, a shortage of specific microchips in 2023-2024 led to significant price increases for automotive manufacturers globally.

- Supplier Dominance: A few key manufacturers often control the supply of specialized high-tech automotive components.

- Price Influence: Concentrated suppliers can dictate higher prices for essential advanced parts.

- Supply Chain Risk: Reliance on a few suppliers for critical technology increases vulnerability to supply disruptions.

Switching costs and integration complexity

Switching suppliers for critical components, particularly those deeply integrated into Sinotruk's vehicle platforms, presents significant hurdles. For instance, transitioning from a supplier of advanced engine management systems or proprietary chassis components can necessitate substantial investments in retooling production lines and redesigning vehicle architectures. These integration complexities, coupled with the need for extensive compatibility and performance testing, directly amplify the bargaining power of existing suppliers by making it difficult and costly for Sinotruk to explore alternative sourcing options.

The financial implications of such transitions can be considerable. In 2024, the automotive industry saw average costs for retooling a single production line range from $5 million to $50 million, depending on the complexity of the components involved. For a large manufacturer like Sinotruk, a full component system switch could easily run into hundreds of millions of dollars. This financial barrier reinforces supplier leverage, as the upfront investment required to switch often outweighs the perceived benefits of finding a new supplier, especially if the existing supplier offers competitive pricing and reliable delivery.

- High Retooling Costs: Switching suppliers for integrated systems can demand millions in production line modifications.

- Vehicle Architecture Redesign: New component integration may require costly and time-consuming redesigns of vehicle platforms.

- Extensive Testing Requirements: Ensuring compatibility and performance of new components necessitates rigorous and expensive testing phases.

- Financial Disincentive to Switch: The substantial upfront costs often make it economically unfeasible for Sinotruk to change suppliers readily.

Supplier Power Dynamics: Commodity vs. High-Tech Component Influence

Sinotruk Hong Kong faces moderate bargaining power from suppliers of commodity materials like steel and rubber, as these are widely available. However, price volatility, such as the 15% increase in hot-rolled coil steel prices in early 2024, can still impact costs. The company's vertical integration for engines and axles, with over 500,000 units produced annually in 2024, significantly reduces its reliance on external suppliers for these critical, high-value components, thereby mitigating their bargaining power.

The bargaining power of suppliers is elevated for specialized, high-tech components like advanced electronics and semiconductors, where market concentration is high. For instance, the global automotive semiconductor market, valued over $60 billion in 2024, is dominated by a few key players, leading to potential price increases and supply chain risks, as seen with microchip shortages in 2023-2024.

Switching suppliers for deeply integrated systems, such as engine management or chassis components, is costly for Sinotruk, with retooling expenses ranging from $5 million to $50 million per production line in 2024. These high integration and redesign costs, coupled with extensive testing requirements, strengthen the leverage of existing specialized suppliers.

| Supplier Type | Bargaining Power Level | Key Factors |

| Commodity Materials (Steel, Rubber) | Moderate | Wide availability, but subject to global price fluctuations (e.g., 15% steel price rise in early 2024). |

| Vertically Integrated Components (Engines, Axles) | Low | Sinotruk's in-house production (500,000+ units annually in 2024) reduces reliance. |

| Specialized High-Tech Components (Semiconductors, Electronics) | High | Market concentration (e.g., $60B+ semiconductor market in 2024 dominated by few players), integration complexity, and past shortages. |

What is included in the product

Tailored exclusively for Sinotruk Hong Kong, this analysis dissects the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Gain instant clarity on competitive pressures by visualizing the intensity of each force, enabling proactive strategy adjustments.

Easily identify and address key threats and opportunities within the commercial vehicle sector, transforming potential pain points into strategic advantages.

Customers Bargaining Power

Large fleet purchases by commercial entities

Sinotruk's customer base primarily includes major logistics, construction, and mining firms. These companies often make large fleet purchases, buying heavy-duty trucks in substantial quantities.

This significant volume grants these customers considerable bargaining power. They can leverage these bulk orders to negotiate better pricing, demand longer warranties, and secure customized contract terms, directly impacting Sinotruk's profitability.

High price sensitivity due to capital expenditure

Customers acquiring heavy-duty trucks face substantial capital expenditures, directly translating to heightened price sensitivity. This significant upfront cost means buyers meticulously evaluate every pricing option available in the market.

Consequently, customers actively compare offerings from different manufacturers, focusing on the total cost of ownership. Factors like fuel efficiency and long-term maintenance costs are rigorously scrutinized, creating persistent downward pressure on Sinotruk's pricing strategies and impacting profitability.

Availability of multiple competitive alternatives

Customers in the heavy-duty truck market, particularly in China, enjoy a significant advantage due to the sheer number of competitive alternatives available. Manufacturers like FAW, Dongfeng, and Shacman are prominent players, offering a diverse range of products that directly compete with Sinotruk. This abundance of choice means customers can readily compare specifications, pricing, and service offerings, putting them in a strong position to negotiate favorable terms.

Increasing adoption of new energy vehicles impacting choices

The increasing adoption of new energy vehicles (NEVs) in the heavy-duty truck (HDT) sector, particularly in China, is significantly shifting the bargaining power towards customers. As more NEV HDT models enter the market and their total cost of ownership becomes more competitive, buyers have a wider array of choices. This greater selection empowers them to negotiate better terms, as they are less dependent on any single traditional manufacturer.

In 2023, China's NEV HDT sales saw substantial growth, with some reports indicating a near doubling compared to the previous year, reaching hundreds of thousands of units. This surge means that customers now have access to a broader range of technologies and pricing structures. For instance, the availability of government subsidies and the improving charging infrastructure further enhance the appeal of NEVs, giving customers more leverage when considering their fleet upgrades or replacements.

- Increased NEV HDT Market Share: In 2023, NEV HDTs accounted for a notable percentage of total HDT sales in China, offering a tangible alternative to diesel.

- Total Cost of Ownership (TCO) Advantage: Lower energy costs and reduced maintenance for NEVs are making them increasingly attractive, giving customers more negotiating power based on long-term savings.

- Technological Advancements: Continuous improvements in battery technology and charging speeds for NEV HDTs provide customers with more confidence and options, reducing reliance on established diesel truck brands.

- Customer Choice and Negotiation: The expanding range of NEV HDT manufacturers and models directly translates to enhanced customer bargaining power, as they can compare offerings and demand more favorable terms.

Importance of after-sales service and network

Customers' bargaining power is significantly influenced by the importance they place on after-sales service and the availability of a strong support network. While competitive pricing remains a key consideration, buyers increasingly value reliable maintenance, readily available spare parts, and extensive service coverage to minimize operational downtime.

Sinotruk has invested in building a global service infrastructure to address these customer needs. As of recent data, the company operates 246 service stations and maintains 217 parts supply networks across the globe, demonstrating a commitment to customer support and aiming to foster loyalty through dependable service.

However, this focus on after-sales can also empower customers. If Sinotruk's service quality is perceived as inadequate or if competitors offer demonstrably superior support and a more accessible network, customers gain leverage. This can lead to increased price sensitivity or a shift in preference towards rivals who better meet their service expectations.

- After-Sales Importance: Customers prioritize operational uptime, making robust after-sales service and spare parts availability critical purchasing factors.

- Sinotruk's Network: The company supports its global customer base with 246 service stations and 217 parts supply networks.

- Customer Leverage: A decline in service quality or superior competitor offerings can significantly increase customer bargaining power.

Customer Power Shapes Heavy-Duty Truck Market

The bargaining power of Sinotruk's customers is substantial due to their significant purchase volumes and the intense competition in the heavy-duty truck market. Factors like price sensitivity, the availability of numerous alternatives, and the growing appeal of new energy vehicles (NEVs) all contribute to this leverage. Furthermore, the critical importance of reliable after-sales service means that any perceived weakness in Sinotruk's support network can further empower buyers to negotiate more favorable terms.

| Factor | Impact on Bargaining Power | Supporting Data/Context |

|---|---|---|

| Purchase Volume | High | Major logistics, construction, and mining firms make large fleet purchases. |

| Availability of Alternatives | High | Strong competition from FAW, Dongfeng, Shacman in China. |

| Price Sensitivity | High | Significant capital expenditure on heavy-duty trucks drives meticulous price evaluation. |

| New Energy Vehicle (NEV) Adoption | Increasing | China's NEV HDT sales nearly doubled in 2023, offering more choices and potentially lower TCO. |

| After-Sales Service Importance | High | Sinotruk operates 246 global service stations and 217 parts supply networks, but service quality is a key negotiation point. |

Full Version Awaits

Sinotruk Hong Kong Porter's Five Forces Analysis

This preview reveals the complete Sinotruk Hong Kong Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape. You're viewing the exact, professionally formatted document you'll receive instantly upon purchase, ensuring no surprises. This detailed analysis is ready for immediate use, providing actionable insights into the industry's dynamics.

From Overview to Strategy Blueprint

Sinotruk Hong Kong operates within a dynamic heavy-duty truck market, facing significant competitive pressures from established global players and emerging domestic manufacturers. Understanding the intensity of rivalry, the bargaining power of buyers and suppliers, and the threats of new entrants and substitutes is crucial for navigating this landscape.

The complete report reveals the real forces shaping Sinotruk Hong Kong’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Highly specialized components

For critical systems like advanced engine management, braking, or safety technologies, Sinotruk Hong Kong may depend on a limited number of global suppliers. For example, in 2024, the global automotive supplier market saw consolidation, with key players in specialized electronics and powertrain components holding substantial market share.

These suppliers, possessing unique technological expertise and intellectual property, can wield significant pricing power over Sinotruk. This reliance on specialized parts can create bottlenecks or increase costs if alternatives are not readily available, impacting Sinotruk's production efficiency and profitability.

Commodity raw materials price fluctuations

Commodity raw materials like steel and rubber, essential for Sinotruk's heavy-duty trucks, are readily available from numerous suppliers. However, their prices can swing significantly due to global supply and demand dynamics.

In 2024, steel prices experienced notable fluctuations, with benchmarks like hot-rolled coil seeing a roughly 15% increase in the first half of the year before stabilizing. Similarly, natural rubber prices, crucial for tires, saw a 10% rise in early 2024 driven by weather concerns in key producing regions.

While Sinotruk's large-scale procurement offers some negotiation power, substantial hikes in these raw material costs directly impact its production expenses and profit margins. This volatility underscores the importance of robust supply chain management, including strategic sourcing and financial hedging instruments, to buffer against adverse price movements and maintain competitive pricing.

In-house production capabilities for core components

Sinotruk's strategic decision to manufacture its own engines and axles significantly curtails its reliance on external suppliers for these critical components. This vertical integration enhances Sinotruk's leverage by providing more control over the quality, cost, and supply chain reliability of these essential parts.

By producing its core components in-house, Sinotruk effectively diminishes the bargaining power of potential third-party engine and axle manufacturers. For instance, in 2024, Sinotruk's engine production capacity reached over 500,000 units annually, a substantial portion of its total vehicle output, demonstrating a strong commitment to internal manufacturing.

Supplier concentration for high-tech parts

The market for certain high-tech components essential for modern trucks, like advanced electronic control units or specialized battery management systems, can be highly concentrated. This means a limited number of suppliers might dominate the production of these critical parts. For instance, in 2024, the global market for automotive semiconductors, a key high-tech component, was estimated to be worth over $60 billion, with a significant portion of advanced chip production concentrated among a few major players.

When Sinotruk Hong Kong relies on these concentrated suppliers for niche or advanced parts, those suppliers gain considerable bargaining power. This can translate into higher prices for components or stricter supply terms, directly impacting Sinotruk's cost of goods sold and potentially its profit margins. For example, a shortage of specific microchips in 2023-2024 led to significant price increases for automotive manufacturers globally.

- Supplier Dominance: A few key manufacturers often control the supply of specialized high-tech automotive components.

- Price Influence: Concentrated suppliers can dictate higher prices for essential advanced parts.

- Supply Chain Risk: Reliance on a few suppliers for critical technology increases vulnerability to supply disruptions.

Switching costs and integration complexity

Switching suppliers for critical components, particularly those deeply integrated into Sinotruk's vehicle platforms, presents significant hurdles. For instance, transitioning from a supplier of advanced engine management systems or proprietary chassis components can necessitate substantial investments in retooling production lines and redesigning vehicle architectures. These integration complexities, coupled with the need for extensive compatibility and performance testing, directly amplify the bargaining power of existing suppliers by making it difficult and costly for Sinotruk to explore alternative sourcing options.

The financial implications of such transitions can be considerable. In 2024, the automotive industry saw average costs for retooling a single production line range from $5 million to $50 million, depending on the complexity of the components involved. For a large manufacturer like Sinotruk, a full component system switch could easily run into hundreds of millions of dollars. This financial barrier reinforces supplier leverage, as the upfront investment required to switch often outweighs the perceived benefits of finding a new supplier, especially if the existing supplier offers competitive pricing and reliable delivery.

- High Retooling Costs: Switching suppliers for integrated systems can demand millions in production line modifications.

- Vehicle Architecture Redesign: New component integration may require costly and time-consuming redesigns of vehicle platforms.

- Extensive Testing Requirements: Ensuring compatibility and performance of new components necessitates rigorous and expensive testing phases.

- Financial Disincentive to Switch: The substantial upfront costs often make it economically unfeasible for Sinotruk to change suppliers readily.

Supplier Power Dynamics: Commodity vs. High-Tech Component Influence

Sinotruk Hong Kong faces moderate bargaining power from suppliers of commodity materials like steel and rubber, as these are widely available. However, price volatility, such as the 15% increase in hot-rolled coil steel prices in early 2024, can still impact costs. The company's vertical integration for engines and axles, with over 500,000 units produced annually in 2024, significantly reduces its reliance on external suppliers for these critical, high-value components, thereby mitigating their bargaining power.

The bargaining power of suppliers is elevated for specialized, high-tech components like advanced electronics and semiconductors, where market concentration is high. For instance, the global automotive semiconductor market, valued over $60 billion in 2024, is dominated by a few key players, leading to potential price increases and supply chain risks, as seen with microchip shortages in 2023-2024.

Switching suppliers for deeply integrated systems, such as engine management or chassis components, is costly for Sinotruk, with retooling expenses ranging from $5 million to $50 million per production line in 2024. These high integration and redesign costs, coupled with extensive testing requirements, strengthen the leverage of existing specialized suppliers.

| Supplier Type | Bargaining Power Level | Key Factors |

| Commodity Materials (Steel, Rubber) | Moderate | Wide availability, but subject to global price fluctuations (e.g., 15% steel price rise in early 2024). |

| Vertically Integrated Components (Engines, Axles) | Low | Sinotruk's in-house production (500,000+ units annually in 2024) reduces reliance. |

| Specialized High-Tech Components (Semiconductors, Electronics) | High | Market concentration (e.g., $60B+ semiconductor market in 2024 dominated by few players), integration complexity, and past shortages. |

What is included in the product

Tailored exclusively for Sinotruk Hong Kong, this analysis dissects the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Gain instant clarity on competitive pressures by visualizing the intensity of each force, enabling proactive strategy adjustments.

Easily identify and address key threats and opportunities within the commercial vehicle sector, transforming potential pain points into strategic advantages.

Customers Bargaining Power

Large fleet purchases by commercial entities

Sinotruk's customer base primarily includes major logistics, construction, and mining firms. These companies often make large fleet purchases, buying heavy-duty trucks in substantial quantities.

This significant volume grants these customers considerable bargaining power. They can leverage these bulk orders to negotiate better pricing, demand longer warranties, and secure customized contract terms, directly impacting Sinotruk's profitability.

High price sensitivity due to capital expenditure

Customers acquiring heavy-duty trucks face substantial capital expenditures, directly translating to heightened price sensitivity. This significant upfront cost means buyers meticulously evaluate every pricing option available in the market.

Consequently, customers actively compare offerings from different manufacturers, focusing on the total cost of ownership. Factors like fuel efficiency and long-term maintenance costs are rigorously scrutinized, creating persistent downward pressure on Sinotruk's pricing strategies and impacting profitability.

Availability of multiple competitive alternatives

Customers in the heavy-duty truck market, particularly in China, enjoy a significant advantage due to the sheer number of competitive alternatives available. Manufacturers like FAW, Dongfeng, and Shacman are prominent players, offering a diverse range of products that directly compete with Sinotruk. This abundance of choice means customers can readily compare specifications, pricing, and service offerings, putting them in a strong position to negotiate favorable terms.

Increasing adoption of new energy vehicles impacting choices

The increasing adoption of new energy vehicles (NEVs) in the heavy-duty truck (HDT) sector, particularly in China, is significantly shifting the bargaining power towards customers. As more NEV HDT models enter the market and their total cost of ownership becomes more competitive, buyers have a wider array of choices. This greater selection empowers them to negotiate better terms, as they are less dependent on any single traditional manufacturer.

In 2023, China's NEV HDT sales saw substantial growth, with some reports indicating a near doubling compared to the previous year, reaching hundreds of thousands of units. This surge means that customers now have access to a broader range of technologies and pricing structures. For instance, the availability of government subsidies and the improving charging infrastructure further enhance the appeal of NEVs, giving customers more leverage when considering their fleet upgrades or replacements.

- Increased NEV HDT Market Share: In 2023, NEV HDTs accounted for a notable percentage of total HDT sales in China, offering a tangible alternative to diesel.

- Total Cost of Ownership (TCO) Advantage: Lower energy costs and reduced maintenance for NEVs are making them increasingly attractive, giving customers more negotiating power based on long-term savings.

- Technological Advancements: Continuous improvements in battery technology and charging speeds for NEV HDTs provide customers with more confidence and options, reducing reliance on established diesel truck brands.

- Customer Choice and Negotiation: The expanding range of NEV HDT manufacturers and models directly translates to enhanced customer bargaining power, as they can compare offerings and demand more favorable terms.

Importance of after-sales service and network

Customers' bargaining power is significantly influenced by the importance they place on after-sales service and the availability of a strong support network. While competitive pricing remains a key consideration, buyers increasingly value reliable maintenance, readily available spare parts, and extensive service coverage to minimize operational downtime.

Sinotruk has invested in building a global service infrastructure to address these customer needs. As of recent data, the company operates 246 service stations and maintains 217 parts supply networks across the globe, demonstrating a commitment to customer support and aiming to foster loyalty through dependable service.

However, this focus on after-sales can also empower customers. If Sinotruk's service quality is perceived as inadequate or if competitors offer demonstrably superior support and a more accessible network, customers gain leverage. This can lead to increased price sensitivity or a shift in preference towards rivals who better meet their service expectations.

- After-Sales Importance: Customers prioritize operational uptime, making robust after-sales service and spare parts availability critical purchasing factors.

- Sinotruk's Network: The company supports its global customer base with 246 service stations and 217 parts supply networks.

- Customer Leverage: A decline in service quality or superior competitor offerings can significantly increase customer bargaining power.

Customer Power Shapes Heavy-Duty Truck Market

The bargaining power of Sinotruk's customers is substantial due to their significant purchase volumes and the intense competition in the heavy-duty truck market. Factors like price sensitivity, the availability of numerous alternatives, and the growing appeal of new energy vehicles (NEVs) all contribute to this leverage. Furthermore, the critical importance of reliable after-sales service means that any perceived weakness in Sinotruk's support network can further empower buyers to negotiate more favorable terms.

| Factor | Impact on Bargaining Power | Supporting Data/Context |

|---|---|---|

| Purchase Volume | High | Major logistics, construction, and mining firms make large fleet purchases. |

| Availability of Alternatives | High | Strong competition from FAW, Dongfeng, Shacman in China. |

| Price Sensitivity | High | Significant capital expenditure on heavy-duty trucks drives meticulous price evaluation. |

| New Energy Vehicle (NEV) Adoption | Increasing | China's NEV HDT sales nearly doubled in 2023, offering more choices and potentially lower TCO. |

| After-Sales Service Importance | High | Sinotruk operates 246 global service stations and 217 parts supply networks, but service quality is a key negotiation point. |

Full Version Awaits

Sinotruk Hong Kong Porter's Five Forces Analysis

This preview reveals the complete Sinotruk Hong Kong Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape. You're viewing the exact, professionally formatted document you'll receive instantly upon purchase, ensuring no surprises. This detailed analysis is ready for immediate use, providing actionable insights into the industry's dynamics.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Sinotruk Hong Kong operates within a dynamic heavy-duty truck market, facing significant competitive pressures from established global players and emerging domestic manufacturers. Understanding the intensity of rivalry, the bargaining power of buyers and suppliers, and the threats of new entrants and substitutes is crucial for navigating this landscape.

The complete report reveals the real forces shaping Sinotruk Hong Kong’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Highly specialized components

For critical systems like advanced engine management, braking, or safety technologies, Sinotruk Hong Kong may depend on a limited number of global suppliers. For example, in 2024, the global automotive supplier market saw consolidation, with key players in specialized electronics and powertrain components holding substantial market share.

These suppliers, possessing unique technological expertise and intellectual property, can wield significant pricing power over Sinotruk. This reliance on specialized parts can create bottlenecks or increase costs if alternatives are not readily available, impacting Sinotruk's production efficiency and profitability.

Commodity raw materials price fluctuations

Commodity raw materials like steel and rubber, essential for Sinotruk's heavy-duty trucks, are readily available from numerous suppliers. However, their prices can swing significantly due to global supply and demand dynamics.

In 2024, steel prices experienced notable fluctuations, with benchmarks like hot-rolled coil seeing a roughly 15% increase in the first half of the year before stabilizing. Similarly, natural rubber prices, crucial for tires, saw a 10% rise in early 2024 driven by weather concerns in key producing regions.

While Sinotruk's large-scale procurement offers some negotiation power, substantial hikes in these raw material costs directly impact its production expenses and profit margins. This volatility underscores the importance of robust supply chain management, including strategic sourcing and financial hedging instruments, to buffer against adverse price movements and maintain competitive pricing.

In-house production capabilities for core components

Sinotruk's strategic decision to manufacture its own engines and axles significantly curtails its reliance on external suppliers for these critical components. This vertical integration enhances Sinotruk's leverage by providing more control over the quality, cost, and supply chain reliability of these essential parts.

By producing its core components in-house, Sinotruk effectively diminishes the bargaining power of potential third-party engine and axle manufacturers. For instance, in 2024, Sinotruk's engine production capacity reached over 500,000 units annually, a substantial portion of its total vehicle output, demonstrating a strong commitment to internal manufacturing.

Supplier concentration for high-tech parts

The market for certain high-tech components essential for modern trucks, like advanced electronic control units or specialized battery management systems, can be highly concentrated. This means a limited number of suppliers might dominate the production of these critical parts. For instance, in 2024, the global market for automotive semiconductors, a key high-tech component, was estimated to be worth over $60 billion, with a significant portion of advanced chip production concentrated among a few major players.

When Sinotruk Hong Kong relies on these concentrated suppliers for niche or advanced parts, those suppliers gain considerable bargaining power. This can translate into higher prices for components or stricter supply terms, directly impacting Sinotruk's cost of goods sold and potentially its profit margins. For example, a shortage of specific microchips in 2023-2024 led to significant price increases for automotive manufacturers globally.

- Supplier Dominance: A few key manufacturers often control the supply of specialized high-tech automotive components.

- Price Influence: Concentrated suppliers can dictate higher prices for essential advanced parts.

- Supply Chain Risk: Reliance on a few suppliers for critical technology increases vulnerability to supply disruptions.

Switching costs and integration complexity

Switching suppliers for critical components, particularly those deeply integrated into Sinotruk's vehicle platforms, presents significant hurdles. For instance, transitioning from a supplier of advanced engine management systems or proprietary chassis components can necessitate substantial investments in retooling production lines and redesigning vehicle architectures. These integration complexities, coupled with the need for extensive compatibility and performance testing, directly amplify the bargaining power of existing suppliers by making it difficult and costly for Sinotruk to explore alternative sourcing options.

The financial implications of such transitions can be considerable. In 2024, the automotive industry saw average costs for retooling a single production line range from $5 million to $50 million, depending on the complexity of the components involved. For a large manufacturer like Sinotruk, a full component system switch could easily run into hundreds of millions of dollars. This financial barrier reinforces supplier leverage, as the upfront investment required to switch often outweighs the perceived benefits of finding a new supplier, especially if the existing supplier offers competitive pricing and reliable delivery.

- High Retooling Costs: Switching suppliers for integrated systems can demand millions in production line modifications.

- Vehicle Architecture Redesign: New component integration may require costly and time-consuming redesigns of vehicle platforms.

- Extensive Testing Requirements: Ensuring compatibility and performance of new components necessitates rigorous and expensive testing phases.

- Financial Disincentive to Switch: The substantial upfront costs often make it economically unfeasible for Sinotruk to change suppliers readily.

Supplier Power Dynamics: Commodity vs. High-Tech Component Influence

Sinotruk Hong Kong faces moderate bargaining power from suppliers of commodity materials like steel and rubber, as these are widely available. However, price volatility, such as the 15% increase in hot-rolled coil steel prices in early 2024, can still impact costs. The company's vertical integration for engines and axles, with over 500,000 units produced annually in 2024, significantly reduces its reliance on external suppliers for these critical, high-value components, thereby mitigating their bargaining power.

The bargaining power of suppliers is elevated for specialized, high-tech components like advanced electronics and semiconductors, where market concentration is high. For instance, the global automotive semiconductor market, valued over $60 billion in 2024, is dominated by a few key players, leading to potential price increases and supply chain risks, as seen with microchip shortages in 2023-2024.

Switching suppliers for deeply integrated systems, such as engine management or chassis components, is costly for Sinotruk, with retooling expenses ranging from $5 million to $50 million per production line in 2024. These high integration and redesign costs, coupled with extensive testing requirements, strengthen the leverage of existing specialized suppliers.

| Supplier Type | Bargaining Power Level | Key Factors |

| Commodity Materials (Steel, Rubber) | Moderate | Wide availability, but subject to global price fluctuations (e.g., 15% steel price rise in early 2024). |

| Vertically Integrated Components (Engines, Axles) | Low | Sinotruk's in-house production (500,000+ units annually in 2024) reduces reliance. |

| Specialized High-Tech Components (Semiconductors, Electronics) | High | Market concentration (e.g., $60B+ semiconductor market in 2024 dominated by few players), integration complexity, and past shortages. |

What is included in the product

Tailored exclusively for Sinotruk Hong Kong, this analysis dissects the intensity of rivalry, buyer and supplier power, threat of new entrants, and the impact of substitutes on its market position.

Gain instant clarity on competitive pressures by visualizing the intensity of each force, enabling proactive strategy adjustments.

Easily identify and address key threats and opportunities within the commercial vehicle sector, transforming potential pain points into strategic advantages.

Customers Bargaining Power

Large fleet purchases by commercial entities

Sinotruk's customer base primarily includes major logistics, construction, and mining firms. These companies often make large fleet purchases, buying heavy-duty trucks in substantial quantities.

This significant volume grants these customers considerable bargaining power. They can leverage these bulk orders to negotiate better pricing, demand longer warranties, and secure customized contract terms, directly impacting Sinotruk's profitability.

High price sensitivity due to capital expenditure

Customers acquiring heavy-duty trucks face substantial capital expenditures, directly translating to heightened price sensitivity. This significant upfront cost means buyers meticulously evaluate every pricing option available in the market.

Consequently, customers actively compare offerings from different manufacturers, focusing on the total cost of ownership. Factors like fuel efficiency and long-term maintenance costs are rigorously scrutinized, creating persistent downward pressure on Sinotruk's pricing strategies and impacting profitability.

Availability of multiple competitive alternatives

Customers in the heavy-duty truck market, particularly in China, enjoy a significant advantage due to the sheer number of competitive alternatives available. Manufacturers like FAW, Dongfeng, and Shacman are prominent players, offering a diverse range of products that directly compete with Sinotruk. This abundance of choice means customers can readily compare specifications, pricing, and service offerings, putting them in a strong position to negotiate favorable terms.

Increasing adoption of new energy vehicles impacting choices

The increasing adoption of new energy vehicles (NEVs) in the heavy-duty truck (HDT) sector, particularly in China, is significantly shifting the bargaining power towards customers. As more NEV HDT models enter the market and their total cost of ownership becomes more competitive, buyers have a wider array of choices. This greater selection empowers them to negotiate better terms, as they are less dependent on any single traditional manufacturer.

In 2023, China's NEV HDT sales saw substantial growth, with some reports indicating a near doubling compared to the previous year, reaching hundreds of thousands of units. This surge means that customers now have access to a broader range of technologies and pricing structures. For instance, the availability of government subsidies and the improving charging infrastructure further enhance the appeal of NEVs, giving customers more leverage when considering their fleet upgrades or replacements.

- Increased NEV HDT Market Share: In 2023, NEV HDTs accounted for a notable percentage of total HDT sales in China, offering a tangible alternative to diesel.

- Total Cost of Ownership (TCO) Advantage: Lower energy costs and reduced maintenance for NEVs are making them increasingly attractive, giving customers more negotiating power based on long-term savings.

- Technological Advancements: Continuous improvements in battery technology and charging speeds for NEV HDTs provide customers with more confidence and options, reducing reliance on established diesel truck brands.

- Customer Choice and Negotiation: The expanding range of NEV HDT manufacturers and models directly translates to enhanced customer bargaining power, as they can compare offerings and demand more favorable terms.

Importance of after-sales service and network

Customers' bargaining power is significantly influenced by the importance they place on after-sales service and the availability of a strong support network. While competitive pricing remains a key consideration, buyers increasingly value reliable maintenance, readily available spare parts, and extensive service coverage to minimize operational downtime.

Sinotruk has invested in building a global service infrastructure to address these customer needs. As of recent data, the company operates 246 service stations and maintains 217 parts supply networks across the globe, demonstrating a commitment to customer support and aiming to foster loyalty through dependable service.

However, this focus on after-sales can also empower customers. If Sinotruk's service quality is perceived as inadequate or if competitors offer demonstrably superior support and a more accessible network, customers gain leverage. This can lead to increased price sensitivity or a shift in preference towards rivals who better meet their service expectations.

- After-Sales Importance: Customers prioritize operational uptime, making robust after-sales service and spare parts availability critical purchasing factors.

- Sinotruk's Network: The company supports its global customer base with 246 service stations and 217 parts supply networks.

- Customer Leverage: A decline in service quality or superior competitor offerings can significantly increase customer bargaining power.

Customer Power Shapes Heavy-Duty Truck Market

The bargaining power of Sinotruk's customers is substantial due to their significant purchase volumes and the intense competition in the heavy-duty truck market. Factors like price sensitivity, the availability of numerous alternatives, and the growing appeal of new energy vehicles (NEVs) all contribute to this leverage. Furthermore, the critical importance of reliable after-sales service means that any perceived weakness in Sinotruk's support network can further empower buyers to negotiate more favorable terms.

| Factor | Impact on Bargaining Power | Supporting Data/Context |

|---|---|---|

| Purchase Volume | High | Major logistics, construction, and mining firms make large fleet purchases. |

| Availability of Alternatives | High | Strong competition from FAW, Dongfeng, Shacman in China. |

| Price Sensitivity | High | Significant capital expenditure on heavy-duty trucks drives meticulous price evaluation. |

| New Energy Vehicle (NEV) Adoption | Increasing | China's NEV HDT sales nearly doubled in 2023, offering more choices and potentially lower TCO. |

| After-Sales Service Importance | High | Sinotruk operates 246 global service stations and 217 parts supply networks, but service quality is a key negotiation point. |

Full Version Awaits

Sinotruk Hong Kong Porter's Five Forces Analysis

This preview reveals the complete Sinotruk Hong Kong Porter's Five Forces Analysis, offering a thorough examination of the competitive landscape. You're viewing the exact, professionally formatted document you'll receive instantly upon purchase, ensuring no surprises. This detailed analysis is ready for immediate use, providing actionable insights into the industry's dynamics.