Sintokogio Porter's Five Forces Analysis

From Overview to Strategy Blueprint

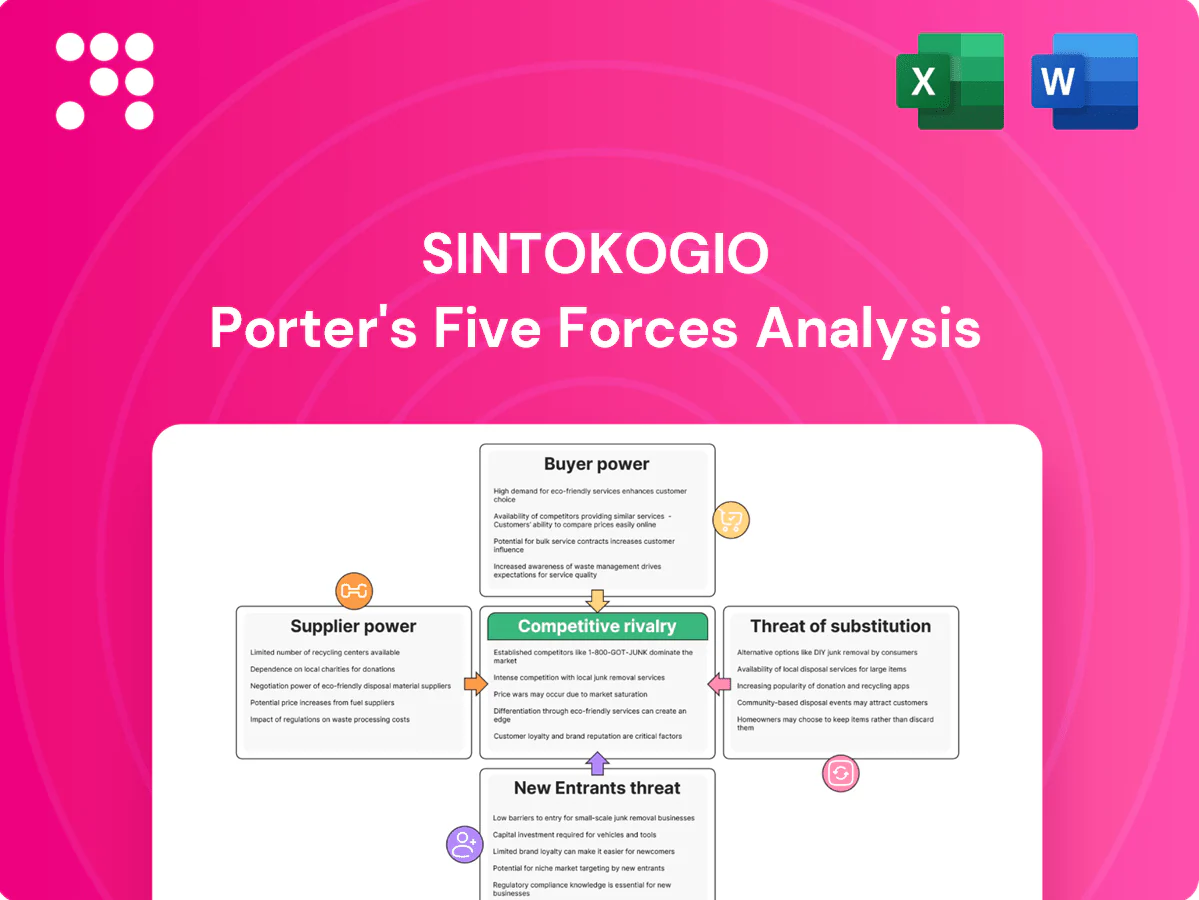

Sintokogio faces moderate buyer power, concentrated suppliers for specialized components, and steady rivalry driven by precision engineering and cost pressures; barriers to entry are modest but technical know‑how raises the bar, while substitutes remain limited. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sintokogio’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component reliance

Controls, sensors, PLCs and high-spec motors are concentrated among a few global suppliers, with the top vendors accounting for roughly 60–70% of industrial automation revenue in 2024. This concentration raises switching costs and keeps lead times elevated (commonly 8–16 weeks in 2024), increasing project timing risk. Long-term framework agreements can dampen annual price swings (historically up to ~15%) but do not remove supply concentration. Design-for-multi-vendor architectures materially rebalance supplier power by lowering single-supplier dependency.

Metals and fabricated parts

Heavy steel, castings and precision fabrications are core inputs for Sintokogio and face cyclical price swings; global crude steel production in 2024 exceeded 1.8 billion tonnes, reflecting tight supply-demand pockets. When capacity tightens, mills and foundries can exert pricing pressure and widen lead times. Qualifying alternate fabs typically takes over 12 months due to quality and safety validation. Hedging and multi-region sourcing materially reduce exposure to spot volatility.

Abrasives and filtration media

Shot/grit media and filter bags/cartridges are recurring, quality-sensitive inputs that can drive 10–25% of maintenance OPEX; premium grades from a concentrated supplier base often command price premiums of 20–30%, boosting supplier margins. Volume bundling across Sintokogio’s installed base secures discounts and service terms, while private-label alternatives (testing cycles typically 6–12 months) provide leverage but require validation.

Lead times and logistics

Long, global supply chains for Sintokogio raise freight and schedule risk, with critical-path assemblies vulnerable to port congestion or export controls that in 2024 still caused multi-week delays in major hubs. Supplier delivery performance directly affects project cash flow through extended payment cycles and higher WIP; many OEMs reported rising buffer inventory levels to offset volatility. Regionalization and local stocking reduced supplier leverage by shortening lead times and improving predictability.

- 2024 WCI approx 1,200 USD per 40ft (Drewry) — lowers but volatile freight costs

- Port delays in 2024 still measured in weeks at key hubs

- Buffer inventories and regional sourcing cut lead times and bargaining power

IP and co-development

Clear IP ownership clauses and standardized interfaces mitigate risk; adopting modular architectures has been shown in 2024 pilots to restore up to 25% of negotiation flexibility within 2–3 product cycles.

- IP-embedded subsystems: higher switching cost

- Pricing power: supplier-driven ~28% of subsystem value (2024)

- Mitigation: ownership clauses + interface standards

- Modularity: ~25% flexibility regained (2024 pilots)

60–70% concentration, 8–16wk lead times raise timing risk

Supplier concentration (automation 60–70% of revenue in 2024) raises switching costs and keeps lead times at 8–16 weeks, increasing project timing risk. Crude steel >1.8bn t (2024) fuels cyclical input pricing; qualifying fabs >12 months. Regional sourcing, buffers and modular design (2024 pilots: ~25% regained negotiation flexibility) materially reduce supplier power.

| Metric | 2024 | Impact |

|---|---|---|

| Automation conc. | 60–70% | High switching cost |

| Lead time | 8–16 wks | Timing risk |

| Crude steel | >1.8bn t | Cyclical prices |

| Modularity | ~25% | Negotiation flexibility |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and rivalry shaping Sintokogio’s market position, offering strategic insights on disruptive threats and protective dynamics.

One-sheet Porter's Five Forces for Sintokogio—clear visual scores and a spider chart to instantly reveal strategic pressures and relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated OEM buyers

Concentrated OEM buyers in automotive, aerospace and tiered manufacturing buy in sizable, infrequent lots—global light‑vehicle production was roughly 80 million units in 2024, concentrating spend with major OEMs—and use professional procurement teams to run competitive RFQs that extract price concessions. Volume and reference contracts give buyers leverage, while suppliers that can demonstrate measurable throughput and quality gains (reduced defects, faster cycle times) can defend pricing and secure long‑term slots.

High switching costs

Installed-base compatibility, operator training and facility layout create high switching barriers, with aftermarket parts and service often representing over 30% of vendor revenue in industrial equipment (2024 industry averages). Buyers still benchmark vendors to pressure service and parts pricing; lifecycle performance data can boost loyalty, while open interfaces lower perceived lock-in.

Total cost of ownership focus

Customers now assess total cost of ownership across energy use, media consumption, downtime and maintenance, and in 2024 TCO evidence increasingly dictates procurement decisions. When measurable TCO advantages are clear, price sensitivity falls and buyers accept premiums tied to performance guarantees and uptime SLAs. Digital monitoring that documents savings and reduced downtime materially weakens buyer bargaining power.

Customization and specs

Complex, tailored systems enable value-based pricing but typically extend sales cycles and increase negotiation scope, while buyer-driven design demands can shift integration and validation costs to Sintokogio, squeezing margins. Standard option kits help cap cost creep and streamline approvals; application labs and on-site trials reduce perceived risk and limit discount pressure by validating performance before purchase.

- Value pricing vs longer cycles

- Buyer design control raises supplier costs

- Standard kits limit cost creep

- Labs/trials cut discount leverage

Aftermarket leverage

OEM scale forces price pressure; 30%+ aftermarket and 24h SLAs entrench vendors

Concentrated OEM buyers (global light‑vehicle production ~80m units in 2024) exert strong price pressure via RFQs, but demonstrated TCO and uptime reduce sensitivity. Aftermarket/service often >30% of vendor revenue, keeping switching costs high when spare availability and <24h response are delivered. Multi‑year (3–5y) contracts trade price for revenue stability.

| Metric | 2024 |

|---|---|

| Light‑vehicle output | ~80m units |

| Aftermarket share | >30% |

| Service SLAs | <24h response |

| Contract length | 3–5 years |

Full Version Awaits

Sintokogio Porter's Five Forces Analysis

This preview shows the exact Sintokogio Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for immediate download and use. Once you buy, you'll get instant access to this same file.

From Overview to Strategy Blueprint

Sintokogio faces moderate buyer power, concentrated suppliers for specialized components, and steady rivalry driven by precision engineering and cost pressures; barriers to entry are modest but technical know‑how raises the bar, while substitutes remain limited. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sintokogio’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component reliance

Controls, sensors, PLCs and high-spec motors are concentrated among a few global suppliers, with the top vendors accounting for roughly 60–70% of industrial automation revenue in 2024. This concentration raises switching costs and keeps lead times elevated (commonly 8–16 weeks in 2024), increasing project timing risk. Long-term framework agreements can dampen annual price swings (historically up to ~15%) but do not remove supply concentration. Design-for-multi-vendor architectures materially rebalance supplier power by lowering single-supplier dependency.

Metals and fabricated parts

Heavy steel, castings and precision fabrications are core inputs for Sintokogio and face cyclical price swings; global crude steel production in 2024 exceeded 1.8 billion tonnes, reflecting tight supply-demand pockets. When capacity tightens, mills and foundries can exert pricing pressure and widen lead times. Qualifying alternate fabs typically takes over 12 months due to quality and safety validation. Hedging and multi-region sourcing materially reduce exposure to spot volatility.

Abrasives and filtration media

Shot/grit media and filter bags/cartridges are recurring, quality-sensitive inputs that can drive 10–25% of maintenance OPEX; premium grades from a concentrated supplier base often command price premiums of 20–30%, boosting supplier margins. Volume bundling across Sintokogio’s installed base secures discounts and service terms, while private-label alternatives (testing cycles typically 6–12 months) provide leverage but require validation.

Lead times and logistics

Long, global supply chains for Sintokogio raise freight and schedule risk, with critical-path assemblies vulnerable to port congestion or export controls that in 2024 still caused multi-week delays in major hubs. Supplier delivery performance directly affects project cash flow through extended payment cycles and higher WIP; many OEMs reported rising buffer inventory levels to offset volatility. Regionalization and local stocking reduced supplier leverage by shortening lead times and improving predictability.

- 2024 WCI approx 1,200 USD per 40ft (Drewry) — lowers but volatile freight costs

- Port delays in 2024 still measured in weeks at key hubs

- Buffer inventories and regional sourcing cut lead times and bargaining power

IP and co-development

Clear IP ownership clauses and standardized interfaces mitigate risk; adopting modular architectures has been shown in 2024 pilots to restore up to 25% of negotiation flexibility within 2–3 product cycles.

- IP-embedded subsystems: higher switching cost

- Pricing power: supplier-driven ~28% of subsystem value (2024)

- Mitigation: ownership clauses + interface standards

- Modularity: ~25% flexibility regained (2024 pilots)

60–70% concentration, 8–16wk lead times raise timing risk

Supplier concentration (automation 60–70% of revenue in 2024) raises switching costs and keeps lead times at 8–16 weeks, increasing project timing risk. Crude steel >1.8bn t (2024) fuels cyclical input pricing; qualifying fabs >12 months. Regional sourcing, buffers and modular design (2024 pilots: ~25% regained negotiation flexibility) materially reduce supplier power.

| Metric | 2024 | Impact |

|---|---|---|

| Automation conc. | 60–70% | High switching cost |

| Lead time | 8–16 wks | Timing risk |

| Crude steel | >1.8bn t | Cyclical prices |

| Modularity | ~25% | Negotiation flexibility |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and rivalry shaping Sintokogio’s market position, offering strategic insights on disruptive threats and protective dynamics.

One-sheet Porter's Five Forces for Sintokogio—clear visual scores and a spider chart to instantly reveal strategic pressures and relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated OEM buyers

Concentrated OEM buyers in automotive, aerospace and tiered manufacturing buy in sizable, infrequent lots—global light‑vehicle production was roughly 80 million units in 2024, concentrating spend with major OEMs—and use professional procurement teams to run competitive RFQs that extract price concessions. Volume and reference contracts give buyers leverage, while suppliers that can demonstrate measurable throughput and quality gains (reduced defects, faster cycle times) can defend pricing and secure long‑term slots.

High switching costs

Installed-base compatibility, operator training and facility layout create high switching barriers, with aftermarket parts and service often representing over 30% of vendor revenue in industrial equipment (2024 industry averages). Buyers still benchmark vendors to pressure service and parts pricing; lifecycle performance data can boost loyalty, while open interfaces lower perceived lock-in.

Total cost of ownership focus

Customers now assess total cost of ownership across energy use, media consumption, downtime and maintenance, and in 2024 TCO evidence increasingly dictates procurement decisions. When measurable TCO advantages are clear, price sensitivity falls and buyers accept premiums tied to performance guarantees and uptime SLAs. Digital monitoring that documents savings and reduced downtime materially weakens buyer bargaining power.

Customization and specs

Complex, tailored systems enable value-based pricing but typically extend sales cycles and increase negotiation scope, while buyer-driven design demands can shift integration and validation costs to Sintokogio, squeezing margins. Standard option kits help cap cost creep and streamline approvals; application labs and on-site trials reduce perceived risk and limit discount pressure by validating performance before purchase.

- Value pricing vs longer cycles

- Buyer design control raises supplier costs

- Standard kits limit cost creep

- Labs/trials cut discount leverage

Aftermarket leverage

OEM scale forces price pressure; 30%+ aftermarket and 24h SLAs entrench vendors

Concentrated OEM buyers (global light‑vehicle production ~80m units in 2024) exert strong price pressure via RFQs, but demonstrated TCO and uptime reduce sensitivity. Aftermarket/service often >30% of vendor revenue, keeping switching costs high when spare availability and <24h response are delivered. Multi‑year (3–5y) contracts trade price for revenue stability.

| Metric | 2024 |

|---|---|

| Light‑vehicle output | ~80m units |

| Aftermarket share | >30% |

| Service SLAs | <24h response |

| Contract length | 3–5 years |

Full Version Awaits

Sintokogio Porter's Five Forces Analysis

This preview shows the exact Sintokogio Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for immediate download and use. Once you buy, you'll get instant access to this same file.

Description

From Overview to Strategy Blueprint

Sintokogio faces moderate buyer power, concentrated suppliers for specialized components, and steady rivalry driven by precision engineering and cost pressures; barriers to entry are modest but technical know‑how raises the bar, while substitutes remain limited. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Sintokogio’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized component reliance

Controls, sensors, PLCs and high-spec motors are concentrated among a few global suppliers, with the top vendors accounting for roughly 60–70% of industrial automation revenue in 2024. This concentration raises switching costs and keeps lead times elevated (commonly 8–16 weeks in 2024), increasing project timing risk. Long-term framework agreements can dampen annual price swings (historically up to ~15%) but do not remove supply concentration. Design-for-multi-vendor architectures materially rebalance supplier power by lowering single-supplier dependency.

Metals and fabricated parts

Heavy steel, castings and precision fabrications are core inputs for Sintokogio and face cyclical price swings; global crude steel production in 2024 exceeded 1.8 billion tonnes, reflecting tight supply-demand pockets. When capacity tightens, mills and foundries can exert pricing pressure and widen lead times. Qualifying alternate fabs typically takes over 12 months due to quality and safety validation. Hedging and multi-region sourcing materially reduce exposure to spot volatility.

Abrasives and filtration media

Shot/grit media and filter bags/cartridges are recurring, quality-sensitive inputs that can drive 10–25% of maintenance OPEX; premium grades from a concentrated supplier base often command price premiums of 20–30%, boosting supplier margins. Volume bundling across Sintokogio’s installed base secures discounts and service terms, while private-label alternatives (testing cycles typically 6–12 months) provide leverage but require validation.

Lead times and logistics

Long, global supply chains for Sintokogio raise freight and schedule risk, with critical-path assemblies vulnerable to port congestion or export controls that in 2024 still caused multi-week delays in major hubs. Supplier delivery performance directly affects project cash flow through extended payment cycles and higher WIP; many OEMs reported rising buffer inventory levels to offset volatility. Regionalization and local stocking reduced supplier leverage by shortening lead times and improving predictability.

- 2024 WCI approx 1,200 USD per 40ft (Drewry) — lowers but volatile freight costs

- Port delays in 2024 still measured in weeks at key hubs

- Buffer inventories and regional sourcing cut lead times and bargaining power

IP and co-development

Clear IP ownership clauses and standardized interfaces mitigate risk; adopting modular architectures has been shown in 2024 pilots to restore up to 25% of negotiation flexibility within 2–3 product cycles.

- IP-embedded subsystems: higher switching cost

- Pricing power: supplier-driven ~28% of subsystem value (2024)

- Mitigation: ownership clauses + interface standards

- Modularity: ~25% flexibility regained (2024 pilots)

60–70% concentration, 8–16wk lead times raise timing risk

Supplier concentration (automation 60–70% of revenue in 2024) raises switching costs and keeps lead times at 8–16 weeks, increasing project timing risk. Crude steel >1.8bn t (2024) fuels cyclical input pricing; qualifying fabs >12 months. Regional sourcing, buffers and modular design (2024 pilots: ~25% regained negotiation flexibility) materially reduce supplier power.

| Metric | 2024 | Impact |

|---|---|---|

| Automation conc. | 60–70% | High switching cost |

| Lead time | 8–16 wks | Timing risk |

| Crude steel | >1.8bn t | Cyclical prices |

| Modularity | ~25% | Negotiation flexibility |

What is included in the product

Uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and rivalry shaping Sintokogio’s market position, offering strategic insights on disruptive threats and protective dynamics.

One-sheet Porter's Five Forces for Sintokogio—clear visual scores and a spider chart to instantly reveal strategic pressures and relieve analysis bottlenecks.

Customers Bargaining Power

Concentrated OEM buyers

Concentrated OEM buyers in automotive, aerospace and tiered manufacturing buy in sizable, infrequent lots—global light‑vehicle production was roughly 80 million units in 2024, concentrating spend with major OEMs—and use professional procurement teams to run competitive RFQs that extract price concessions. Volume and reference contracts give buyers leverage, while suppliers that can demonstrate measurable throughput and quality gains (reduced defects, faster cycle times) can defend pricing and secure long‑term slots.

High switching costs

Installed-base compatibility, operator training and facility layout create high switching barriers, with aftermarket parts and service often representing over 30% of vendor revenue in industrial equipment (2024 industry averages). Buyers still benchmark vendors to pressure service and parts pricing; lifecycle performance data can boost loyalty, while open interfaces lower perceived lock-in.

Total cost of ownership focus

Customers now assess total cost of ownership across energy use, media consumption, downtime and maintenance, and in 2024 TCO evidence increasingly dictates procurement decisions. When measurable TCO advantages are clear, price sensitivity falls and buyers accept premiums tied to performance guarantees and uptime SLAs. Digital monitoring that documents savings and reduced downtime materially weakens buyer bargaining power.

Customization and specs

Complex, tailored systems enable value-based pricing but typically extend sales cycles and increase negotiation scope, while buyer-driven design demands can shift integration and validation costs to Sintokogio, squeezing margins. Standard option kits help cap cost creep and streamline approvals; application labs and on-site trials reduce perceived risk and limit discount pressure by validating performance before purchase.

- Value pricing vs longer cycles

- Buyer design control raises supplier costs

- Standard kits limit cost creep

- Labs/trials cut discount leverage

Aftermarket leverage

OEM scale forces price pressure; 30%+ aftermarket and 24h SLAs entrench vendors

Concentrated OEM buyers (global light‑vehicle production ~80m units in 2024) exert strong price pressure via RFQs, but demonstrated TCO and uptime reduce sensitivity. Aftermarket/service often >30% of vendor revenue, keeping switching costs high when spare availability and <24h response are delivered. Multi‑year (3–5y) contracts trade price for revenue stability.

| Metric | 2024 |

|---|---|

| Light‑vehicle output | ~80m units |

| Aftermarket share | >30% |

| Service SLAs | <24h response |

| Contract length | 3–5 years |

Full Version Awaits

Sintokogio Porter's Five Forces Analysis

This preview shows the exact Sintokogio Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for immediate download and use. Once you buy, you'll get instant access to this same file.