SiteMinder Porter's Five Forces Analysis

From Overview to Strategy Blueprint

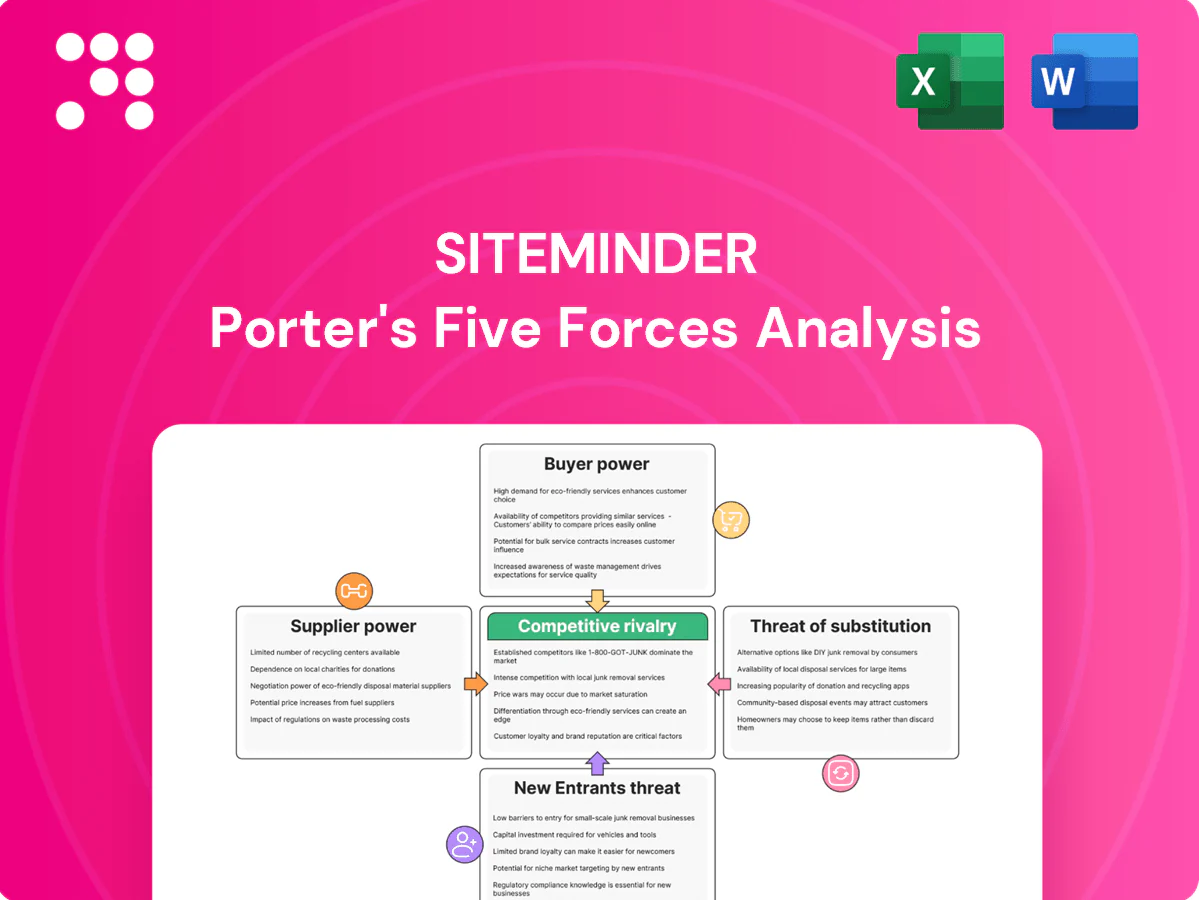

SiteMinder’s Porter's Five Forces snapshot highlights intense buyer power, moderate supplier leverage, low substitute threat, and rising competitive rivalry as distribution shifts online. The full report reveals force-by-force ratings, visuals and concrete business implications. Unlock the complete analysis to inform strategy and investment decisions.

Suppliers Bargaining Power

Concentrated cloud hosting

SiteMinder depends on hyperscale clouds — AWS, Azure and GCP — which together held over 65% of the IaaS market in 2024 (Synergy Research Group), giving those vendors leverage on pricing and contract terms. Reserved instances and multi‑cloud approaches reduce but do not eliminate dependency, while egress fee or SLA changes can directly compress margins and trigger penalty exposure. Vendor ecosystems also shape required security certifications and regional data residency options.

Critical OTA and metasearch APIs

Connectivity to Booking.com (Booking Holdings revenue 2023: 15.07 billion USD) and Expedia (Expedia Group revenue 2023: 11.0 billion USD), plus Google Hotel Ads, is core to a channel manager’s value proposition. API rule changes, certification queues and rate-limit policies grant these platforms leverage over pricing and feature roadmaps. Ongoing compliance and recertification drive recurring engineering cost and resource allocation. Preferential OTA partnerships can steer product priorities and joint-marketing economics.

PMS and payment integrations

Hotels increasingly require deep, bi-directional PMS and payment gateway integrations to support real-time availability, rates and guest data, forcing providers into complex development and certification cycles. Leading PMS vendors and payment partners can impose technical constraints and certification processes that increase implementation costs and time to market. Global card processing fees typically range 1.5–3.5%, directly affecting take-rates and settlement economics. Regional fragmentation of PMS and payments stacks amplifies cumulative supplier bargaining power.

Data, mapping, and content services

Rate mapping, room-type ontologies and image/CDN services are usually sourced from specialized vendors, and their content quality and freshness directly affect conversion so niche suppliers retain leverage; switching risks data mismatches and rework and often needs costly reconciliation. Volume discounts exist, but differentiation still depends on these inputs.

- Specialized sourcing

- Conversion impact

- Switching risk

- Volume discounts vs differentiation

Regulatory and compliance vendors

Regulatory and compliance vendors hold rising supplier power for SiteMinder: GDPR allows fines up to €20 million or 4% of global turnover, PCI-DSS and PSD2 SCA require ongoing assessments and controls, and regional privacy laws mandate audits, tooling, and consultants; certification cycles and mandated controls impose recurring costs and third-party timelines, increasing dependence on specialists and strengthening vendor bargaining as standards tighten.

- GDPR: max fine €20M or 4% global turnover

- PCI-DSS/PSD2: continuous assessments and SCA requirements

- Recurring costs: audits, tooling, consultants drive vendor leverage

Hyperscaler and OTA dominance squeezes margins via API limits, card fees and compliance costs

Hyperscale clouds (AWS/Azure/GCP) held ~65% of IaaS in 2024, concentrating pricing and SLA leverage. Major OTAs (Booking Holdings rev 2023: 15.07B; Expedia 2023: 11.0B) control API access and certification cadence. PMS/payment partners impose integration and card fees (1.5–3.5%), raising implementation and margin pressure. Compliance vendors enforce GDPR/PCI/PSD2 costs (GDPR fine up to €20M or 4% turnover).

| Supplier | Key metric | Impact |

|---|---|---|

| Hyperscalers | 65% IaaS (2024) | Pricing/SLA leverage |

| OTAs | Booking 15.07B; Expedia 11.0B (2023) | API/rate-limit control |

| PMS/Payments | Card fees 1.5–3.5% | Margin & integration cost |

| Compliance | GDPR fine €20M/4% | Recurring audit/tooling costs |

What is included in the product

Tailored Porter's Five Forces analysis for SiteMinder that uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market entry risks to inform strategic positioning and pricing.

A concise Porter's Five Forces template tailored to SiteMinder that quickly surfaces competitive pressures to relieve strategic uncertainty; customize scores, labels and notes to reflect changing market dynamics and drop straight into pitch decks or dashboards.

Customers Bargaining Power

Fragmented but price-sensitive hotels

Independent hotels and small groups face high vendor choice and tight cost scrutiny, often switching between subscription and take-rate models during soft demand; Booking Holdings and Expedia+Vrbo account for roughly 70% of OTA bookings, driving trials of competitors before commitment, and discounting plus bundled offers are now baseline expectations.

Multi-homing across tools

Hotels commonly multi-home across PMS-native distribution, standalone booking engines and web builders, eroding supplier lock-in and strengthening buyer leverage. Vendors face displacement unless they interoperate; SiteMinder reported serving 35,000+ properties, underscoring widespread multi-vendor stacks. The need for feature parity across integrations drives competitive pricing and faster product parity.

Moderate switching costs

Migrating channel mappings, rate plans and website assets creates measurable friction for SiteMinder customers but remains manageable given the platform’s over 35,000 hotel customers and 400+ integrations that streamline exports and data portability. Implementation support and API/data-export features can lower barriers further, shortening onboarding from weeks to days for many properties. Short contract durations (monthly–annual common in hotel SaaS) increase churn risk, so references and clear ROI metrics become decisive in renewals.

Enterprise procurement power

Hotel chains and management companies secure volume discounts, SLAs and bespoke integrations, driving strong procurement leverage over vendors like SiteMinder; centralized procurement also enforces strict security and compliance requirements that lengthen sales cycles. Concessions on product roadmaps and elevated support tiers are frequently traded to win enterprise deals, and losing a single large client can materially affect ARR concentration.

- Enterprise deals often demand custom SLAs and integrations

- Centralized procurement adds security/compliance gates

- Roadmap/support concessions common to secure contracts

- High ARR concentration risk from single-account loss

Outcome-based expectations

Buyers demand outcome-based results: many hotels target 10–20% uplift in direct bookings and 3–5% ADR improvement; failure to meet targets often leads to credits or switching providers, increasing churn risk for SiteMinder. Transparent analytics and clear attribution are now mandatory, and this performance focus has steadily strengthened buyer bargaining power through 2024.

- Expectations: 10–20% direct bookings uplift

- Financial targets: 3–5% ADR gains

- Remedies: credits or supplier switch if lagging

- Demand: end-to-end transparent attribution

Independents gain leverage as two OTAs drive ~70% bookings; multi-homing rises

Customers wield strong leverage: independents switch models and Booking Holdings+Expedia/Vrbo drive ~70% OTA bookings. SiteMinder serves 35k+ properties with 400+ integrations, enabling multi-homing and lowering lock-in. Monthly–annual contracts and targets (10–20% direct uplift; 3–5% ADR) raise churn risk.

| Metric | 2024 |

|---|---|

| OTA share | ~70% |

| Properties | 35k+ |

| Integrations | 400+ |

| Targets | 10–20% uplift; 3–5% ADR |

Preview the Actual Deliverable

SiteMinder Porter's Five Forces Analysis

This preview shows the exact SiteMinder Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is professionally written, fully formatted and ready to download and use the moment you buy. You're viewing the final deliverable; instant access is granted to this identical file upon payment.

From Overview to Strategy Blueprint

SiteMinder’s Porter's Five Forces snapshot highlights intense buyer power, moderate supplier leverage, low substitute threat, and rising competitive rivalry as distribution shifts online. The full report reveals force-by-force ratings, visuals and concrete business implications. Unlock the complete analysis to inform strategy and investment decisions.

Suppliers Bargaining Power

Concentrated cloud hosting

SiteMinder depends on hyperscale clouds — AWS, Azure and GCP — which together held over 65% of the IaaS market in 2024 (Synergy Research Group), giving those vendors leverage on pricing and contract terms. Reserved instances and multi‑cloud approaches reduce but do not eliminate dependency, while egress fee or SLA changes can directly compress margins and trigger penalty exposure. Vendor ecosystems also shape required security certifications and regional data residency options.

Critical OTA and metasearch APIs

Connectivity to Booking.com (Booking Holdings revenue 2023: 15.07 billion USD) and Expedia (Expedia Group revenue 2023: 11.0 billion USD), plus Google Hotel Ads, is core to a channel manager’s value proposition. API rule changes, certification queues and rate-limit policies grant these platforms leverage over pricing and feature roadmaps. Ongoing compliance and recertification drive recurring engineering cost and resource allocation. Preferential OTA partnerships can steer product priorities and joint-marketing economics.

PMS and payment integrations

Hotels increasingly require deep, bi-directional PMS and payment gateway integrations to support real-time availability, rates and guest data, forcing providers into complex development and certification cycles. Leading PMS vendors and payment partners can impose technical constraints and certification processes that increase implementation costs and time to market. Global card processing fees typically range 1.5–3.5%, directly affecting take-rates and settlement economics. Regional fragmentation of PMS and payments stacks amplifies cumulative supplier bargaining power.

Data, mapping, and content services

Rate mapping, room-type ontologies and image/CDN services are usually sourced from specialized vendors, and their content quality and freshness directly affect conversion so niche suppliers retain leverage; switching risks data mismatches and rework and often needs costly reconciliation. Volume discounts exist, but differentiation still depends on these inputs.

- Specialized sourcing

- Conversion impact

- Switching risk

- Volume discounts vs differentiation

Regulatory and compliance vendors

Regulatory and compliance vendors hold rising supplier power for SiteMinder: GDPR allows fines up to €20 million or 4% of global turnover, PCI-DSS and PSD2 SCA require ongoing assessments and controls, and regional privacy laws mandate audits, tooling, and consultants; certification cycles and mandated controls impose recurring costs and third-party timelines, increasing dependence on specialists and strengthening vendor bargaining as standards tighten.

- GDPR: max fine €20M or 4% global turnover

- PCI-DSS/PSD2: continuous assessments and SCA requirements

- Recurring costs: audits, tooling, consultants drive vendor leverage

Hyperscaler and OTA dominance squeezes margins via API limits, card fees and compliance costs

Hyperscale clouds (AWS/Azure/GCP) held ~65% of IaaS in 2024, concentrating pricing and SLA leverage. Major OTAs (Booking Holdings rev 2023: 15.07B; Expedia 2023: 11.0B) control API access and certification cadence. PMS/payment partners impose integration and card fees (1.5–3.5%), raising implementation and margin pressure. Compliance vendors enforce GDPR/PCI/PSD2 costs (GDPR fine up to €20M or 4% turnover).

| Supplier | Key metric | Impact |

|---|---|---|

| Hyperscalers | 65% IaaS (2024) | Pricing/SLA leverage |

| OTAs | Booking 15.07B; Expedia 11.0B (2023) | API/rate-limit control |

| PMS/Payments | Card fees 1.5–3.5% | Margin & integration cost |

| Compliance | GDPR fine €20M/4% | Recurring audit/tooling costs |

What is included in the product

Tailored Porter's Five Forces analysis for SiteMinder that uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market entry risks to inform strategic positioning and pricing.

A concise Porter's Five Forces template tailored to SiteMinder that quickly surfaces competitive pressures to relieve strategic uncertainty; customize scores, labels and notes to reflect changing market dynamics and drop straight into pitch decks or dashboards.

Customers Bargaining Power

Fragmented but price-sensitive hotels

Independent hotels and small groups face high vendor choice and tight cost scrutiny, often switching between subscription and take-rate models during soft demand; Booking Holdings and Expedia+Vrbo account for roughly 70% of OTA bookings, driving trials of competitors before commitment, and discounting plus bundled offers are now baseline expectations.

Multi-homing across tools

Hotels commonly multi-home across PMS-native distribution, standalone booking engines and web builders, eroding supplier lock-in and strengthening buyer leverage. Vendors face displacement unless they interoperate; SiteMinder reported serving 35,000+ properties, underscoring widespread multi-vendor stacks. The need for feature parity across integrations drives competitive pricing and faster product parity.

Moderate switching costs

Migrating channel mappings, rate plans and website assets creates measurable friction for SiteMinder customers but remains manageable given the platform’s over 35,000 hotel customers and 400+ integrations that streamline exports and data portability. Implementation support and API/data-export features can lower barriers further, shortening onboarding from weeks to days for many properties. Short contract durations (monthly–annual common in hotel SaaS) increase churn risk, so references and clear ROI metrics become decisive in renewals.

Enterprise procurement power

Hotel chains and management companies secure volume discounts, SLAs and bespoke integrations, driving strong procurement leverage over vendors like SiteMinder; centralized procurement also enforces strict security and compliance requirements that lengthen sales cycles. Concessions on product roadmaps and elevated support tiers are frequently traded to win enterprise deals, and losing a single large client can materially affect ARR concentration.

- Enterprise deals often demand custom SLAs and integrations

- Centralized procurement adds security/compliance gates

- Roadmap/support concessions common to secure contracts

- High ARR concentration risk from single-account loss

Outcome-based expectations

Buyers demand outcome-based results: many hotels target 10–20% uplift in direct bookings and 3–5% ADR improvement; failure to meet targets often leads to credits or switching providers, increasing churn risk for SiteMinder. Transparent analytics and clear attribution are now mandatory, and this performance focus has steadily strengthened buyer bargaining power through 2024.

- Expectations: 10–20% direct bookings uplift

- Financial targets: 3–5% ADR gains

- Remedies: credits or supplier switch if lagging

- Demand: end-to-end transparent attribution

Independents gain leverage as two OTAs drive ~70% bookings; multi-homing rises

Customers wield strong leverage: independents switch models and Booking Holdings+Expedia/Vrbo drive ~70% OTA bookings. SiteMinder serves 35k+ properties with 400+ integrations, enabling multi-homing and lowering lock-in. Monthly–annual contracts and targets (10–20% direct uplift; 3–5% ADR) raise churn risk.

| Metric | 2024 |

|---|---|

| OTA share | ~70% |

| Properties | 35k+ |

| Integrations | 400+ |

| Targets | 10–20% uplift; 3–5% ADR |

Preview the Actual Deliverable

SiteMinder Porter's Five Forces Analysis

This preview shows the exact SiteMinder Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is professionally written, fully formatted and ready to download and use the moment you buy. You're viewing the final deliverable; instant access is granted to this identical file upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

SiteMinder’s Porter's Five Forces snapshot highlights intense buyer power, moderate supplier leverage, low substitute threat, and rising competitive rivalry as distribution shifts online. The full report reveals force-by-force ratings, visuals and concrete business implications. Unlock the complete analysis to inform strategy and investment decisions.

Suppliers Bargaining Power

Concentrated cloud hosting

SiteMinder depends on hyperscale clouds — AWS, Azure and GCP — which together held over 65% of the IaaS market in 2024 (Synergy Research Group), giving those vendors leverage on pricing and contract terms. Reserved instances and multi‑cloud approaches reduce but do not eliminate dependency, while egress fee or SLA changes can directly compress margins and trigger penalty exposure. Vendor ecosystems also shape required security certifications and regional data residency options.

Critical OTA and metasearch APIs

Connectivity to Booking.com (Booking Holdings revenue 2023: 15.07 billion USD) and Expedia (Expedia Group revenue 2023: 11.0 billion USD), plus Google Hotel Ads, is core to a channel manager’s value proposition. API rule changes, certification queues and rate-limit policies grant these platforms leverage over pricing and feature roadmaps. Ongoing compliance and recertification drive recurring engineering cost and resource allocation. Preferential OTA partnerships can steer product priorities and joint-marketing economics.

PMS and payment integrations

Hotels increasingly require deep, bi-directional PMS and payment gateway integrations to support real-time availability, rates and guest data, forcing providers into complex development and certification cycles. Leading PMS vendors and payment partners can impose technical constraints and certification processes that increase implementation costs and time to market. Global card processing fees typically range 1.5–3.5%, directly affecting take-rates and settlement economics. Regional fragmentation of PMS and payments stacks amplifies cumulative supplier bargaining power.

Data, mapping, and content services

Rate mapping, room-type ontologies and image/CDN services are usually sourced from specialized vendors, and their content quality and freshness directly affect conversion so niche suppliers retain leverage; switching risks data mismatches and rework and often needs costly reconciliation. Volume discounts exist, but differentiation still depends on these inputs.

- Specialized sourcing

- Conversion impact

- Switching risk

- Volume discounts vs differentiation

Regulatory and compliance vendors

Regulatory and compliance vendors hold rising supplier power for SiteMinder: GDPR allows fines up to €20 million or 4% of global turnover, PCI-DSS and PSD2 SCA require ongoing assessments and controls, and regional privacy laws mandate audits, tooling, and consultants; certification cycles and mandated controls impose recurring costs and third-party timelines, increasing dependence on specialists and strengthening vendor bargaining as standards tighten.

- GDPR: max fine €20M or 4% global turnover

- PCI-DSS/PSD2: continuous assessments and SCA requirements

- Recurring costs: audits, tooling, consultants drive vendor leverage

Hyperscaler and OTA dominance squeezes margins via API limits, card fees and compliance costs

Hyperscale clouds (AWS/Azure/GCP) held ~65% of IaaS in 2024, concentrating pricing and SLA leverage. Major OTAs (Booking Holdings rev 2023: 15.07B; Expedia 2023: 11.0B) control API access and certification cadence. PMS/payment partners impose integration and card fees (1.5–3.5%), raising implementation and margin pressure. Compliance vendors enforce GDPR/PCI/PSD2 costs (GDPR fine up to €20M or 4% turnover).

| Supplier | Key metric | Impact |

|---|---|---|

| Hyperscalers | 65% IaaS (2024) | Pricing/SLA leverage |

| OTAs | Booking 15.07B; Expedia 11.0B (2023) | API/rate-limit control |

| PMS/Payments | Card fees 1.5–3.5% | Margin & integration cost |

| Compliance | GDPR fine €20M/4% | Recurring audit/tooling costs |

What is included in the product

Tailored Porter's Five Forces analysis for SiteMinder that uncovers key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market entry risks to inform strategic positioning and pricing.

A concise Porter's Five Forces template tailored to SiteMinder that quickly surfaces competitive pressures to relieve strategic uncertainty; customize scores, labels and notes to reflect changing market dynamics and drop straight into pitch decks or dashboards.

Customers Bargaining Power

Fragmented but price-sensitive hotels

Independent hotels and small groups face high vendor choice and tight cost scrutiny, often switching between subscription and take-rate models during soft demand; Booking Holdings and Expedia+Vrbo account for roughly 70% of OTA bookings, driving trials of competitors before commitment, and discounting plus bundled offers are now baseline expectations.

Multi-homing across tools

Hotels commonly multi-home across PMS-native distribution, standalone booking engines and web builders, eroding supplier lock-in and strengthening buyer leverage. Vendors face displacement unless they interoperate; SiteMinder reported serving 35,000+ properties, underscoring widespread multi-vendor stacks. The need for feature parity across integrations drives competitive pricing and faster product parity.

Moderate switching costs

Migrating channel mappings, rate plans and website assets creates measurable friction for SiteMinder customers but remains manageable given the platform’s over 35,000 hotel customers and 400+ integrations that streamline exports and data portability. Implementation support and API/data-export features can lower barriers further, shortening onboarding from weeks to days for many properties. Short contract durations (monthly–annual common in hotel SaaS) increase churn risk, so references and clear ROI metrics become decisive in renewals.

Enterprise procurement power

Hotel chains and management companies secure volume discounts, SLAs and bespoke integrations, driving strong procurement leverage over vendors like SiteMinder; centralized procurement also enforces strict security and compliance requirements that lengthen sales cycles. Concessions on product roadmaps and elevated support tiers are frequently traded to win enterprise deals, and losing a single large client can materially affect ARR concentration.

- Enterprise deals often demand custom SLAs and integrations

- Centralized procurement adds security/compliance gates

- Roadmap/support concessions common to secure contracts

- High ARR concentration risk from single-account loss

Outcome-based expectations

Buyers demand outcome-based results: many hotels target 10–20% uplift in direct bookings and 3–5% ADR improvement; failure to meet targets often leads to credits or switching providers, increasing churn risk for SiteMinder. Transparent analytics and clear attribution are now mandatory, and this performance focus has steadily strengthened buyer bargaining power through 2024.

- Expectations: 10–20% direct bookings uplift

- Financial targets: 3–5% ADR gains

- Remedies: credits or supplier switch if lagging

- Demand: end-to-end transparent attribution

Independents gain leverage as two OTAs drive ~70% bookings; multi-homing rises

Customers wield strong leverage: independents switch models and Booking Holdings+Expedia/Vrbo drive ~70% OTA bookings. SiteMinder serves 35k+ properties with 400+ integrations, enabling multi-homing and lowering lock-in. Monthly–annual contracts and targets (10–20% direct uplift; 3–5% ADR) raise churn risk.

| Metric | 2024 |

|---|---|

| OTA share | ~70% |

| Properties | 35k+ |

| Integrations | 400+ |

| Targets | 10–20% uplift; 3–5% ADR |

Preview the Actual Deliverable

SiteMinder Porter's Five Forces Analysis

This preview shows the exact SiteMinder Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The document is professionally written, fully formatted and ready to download and use the moment you buy. You're viewing the final deliverable; instant access is granted to this identical file upon payment.