SiteOne Landscape Supply Porter's Five Forces Analysis

Don't Miss the Bigger Picture

SiteOne Landscape Supply faces concentrated supplier and buyer power, regional competitive intensity, and moderate threat from substitutes—pressures that materially shape margins and growth prospects. This snapshot highlights key strategic levers but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for in-depth ratings, charts, and actionable implications. Purchase the complete report to inform investment and strategy decisions.

Suppliers Bargaining Power

Diversified supplier base dilutes leverage

SiteOne sources across numerous manufacturers in irrigation, fertilizer, hardscapes, lighting and nursery inputs, which dilutes any single vendor’s leverage; multi-sourcing and comparable SKUs enable substitution while geographic breadth across the U.S. and Canada lets the company balance regional supply shocks. With FY2024 net sales near $4.0 billion this scale reduces supplier power, though niche specialty items with few makers still retain pricing clout.

Branded manufacturers retain category influence

Top irrigation and lighting brands such as Hunter, Toro and Rain Bird command terms through contractor preference and spec-driven demand, with vendor programs, rebates and MAP policies constraining distributor pricing. SiteOne’s scale—roughly 700 branches and about $6.8 billion revenue in 2024—helps win allocations but it must carry key brands to remain competitive. This dynamic sustains moderate supplier bargaining power.

Logistics, lead times, and seasonality create dependence

Peak-season demand and long lead times for hardscapes and fertilizers heighten SiteOne's reliance on timely supplier deliveries; SiteOne reported net sales of about $6.1 billion in fiscal 2024, concentrating risk during seasonal peaks. Rising freight costs and capacity constraints have shifted margin toward vendors, while weather-driven volatility limits distributor negotiating flexibility. In shortages, supplier allocation practices favor vendors with greater leverage, constraining SiteOne's purchasing power.

Private label and scale rebates counterbalance

SiteOne leverages private label and aggregated purchasing to extract better terms from suppliers, helping sustain fiscal 2024 sales of about $4.6 billion and a retail footprint of over 700 branches. Volume rebates, marketing funds and joint planning with vendors reduce supplier rent-seeking; private brands provide alternatives where specs allow, dampening vendor leverage in commodity-like categories.

- Private label scale: over 700 branches

- Fiscal 2024 sales: ~$4.6B

- Rebates/marketing funds offset supplier power

Specialized/regulated inputs raise switching costs

Specialized inputs like EPA-regulated chemicals, UL-listed code-compliant lighting, and proprietary irrigation controllers often require vendor-tied certifications and training, raising switching costs for SiteOne; compatibility and warranty constraints limit rapid vendor changes, and vendor tech support and service agreements further entrench suppliers. These factors heighten supplier bargaining power in key product lines in 2024.

- EPA and UL certifications drive supplier lock-in

- Warranty/compatibility limit vendor switching

- Vendor tech support embeds relationships

- Increases supplier bargaining power in select lines

Moderate supplier power vs scale: ~$6.1B, ~700 branches

SiteOne faces moderate supplier power: diversified vendor base, private-label scale and ~700 branches counterbalance supplier leverage, but key brands (Toro, Rain Bird) and specialty items (EPA/UL-regulated, proprietary controllers) retain pricing/control, especially during seasonal peaks; FY2024 sales ~ $6.1B amplify purchasing clout but do not eliminate supplier rent-seeking.

| Metric | 2024 |

|---|---|

| Branches | ~700 |

| Net sales | ~$6.1B |

| Supplier power | Moderate |

What is included in the product

Concise Porter's Five Forces analysis for SiteOne Landscape Supply, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and barriers to entry that shape margins and growth. Includes strategic insights on disruptive risks and defensive levers to protect market share and pricing power.

A concise Porter's Five Forces summary tailored to SiteOne—streamlines competitive pressure analysis for faster, confident decisions. Swap in your metrics, visualize threats with a radar view, and copy straight into decks to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Fragmented contractor base limits buyer leverage

Local landscapers and small contractors — estimated at over 1 million firms in the US (2024) — comprise much of SiteOne’s demand, limiting coordinated bargaining and buyer leverage. Many prioritize proximity, inventory breadth and trade credit over small price differences, and service needs plus rapid delivery further reduce price-only switching. This long tail of customers moderates overall buyer power.

Large nationals and bid work press pricing

National maintenance firms and large installers centralize procurement, demanding volume discounts that compress margins; SiteOne reported roughly $6.0 billion in FY2024 sales, highlighting exposure to these accounts. Competitive project bids require transparent quotes and enable multi-sourcing across regions, leading to double-digit negotiated discounts in many contracts and higher customer bargaining power with tighter margins.

Price sensitivity in commodity categories

Fertilizers, pipe and basic fittings at SiteOne face intense price sensitivity in 2024 as commodity SKUs are readily compared and substituted; buyers routinely switch equivalent-spec products to shave costs. Promotions and rebates — frequently used in 2024 trade programs — further tilt purchasing toward lower-cost suppliers, elevating buyer leverage in these commoditized lines and pressuring margin recovery for distributors; SiteOne reported approximately $5.4 billion in net sales in FY2024.

Service bundling and credit reduce switching

Service bundling — design support, training, jobsite delivery and business solutions — embeds SiteOne into contractor workflows, and with a 2024 branch network exceeding 700 locations these services make switching operationally costly. Trade credit and dedicated account management, part of their commercial offering, increase receivable stickiness. Custom takeoffs and spec assistance create perceived switching costs that temper buyer power.

- Design support: integrated into workflows

- Trade credit: strengthens account retention

- Custom takeoffs: perceived switching costs

- 700+ branches (2024): local presence boosts stickiness

Omnichannel transparency increases options

Omnichannel transparency increases options: online catalogs and competitor e-commerce reveal pricing and availability in real time, enabling customers to compare SiteOne (about 700 locations) with retail pro desks and regional rivals; digital tools narrow information asymmetry and lift buyer power where online alternatives meet needs.

- Online visibility: real-time price/stock comparisons

- Channels: retail pro desks, regional rivals, e-commerce

- Effect: higher buyer leverage when online substitutes suffice

Fragmented landscaper demand limits buyer power; 700+ branches raise switching costs

Local landscapers (>1M US firms) limit coordinated buyer power; convenience, inventory breadth and trade credit reduce price-only switching. National installers extract volume discounts; SiteOne reported ~$6.0B FY2024 sales. Commoditized SKUs face high price sensitivity; omnichannel visibility and 700+ branches raise comparison but service bundling creates switching costs.

| Metric | 2024 |

|---|---|

| FY2024 Sales | $6.0B |

| Net sales (commodities) | $5.4B |

| Branches | 700+ |

| US landscaper firms | >1M |

Same Document Delivered

SiteOne Landscape Supply Porter's Five Forces Analysis

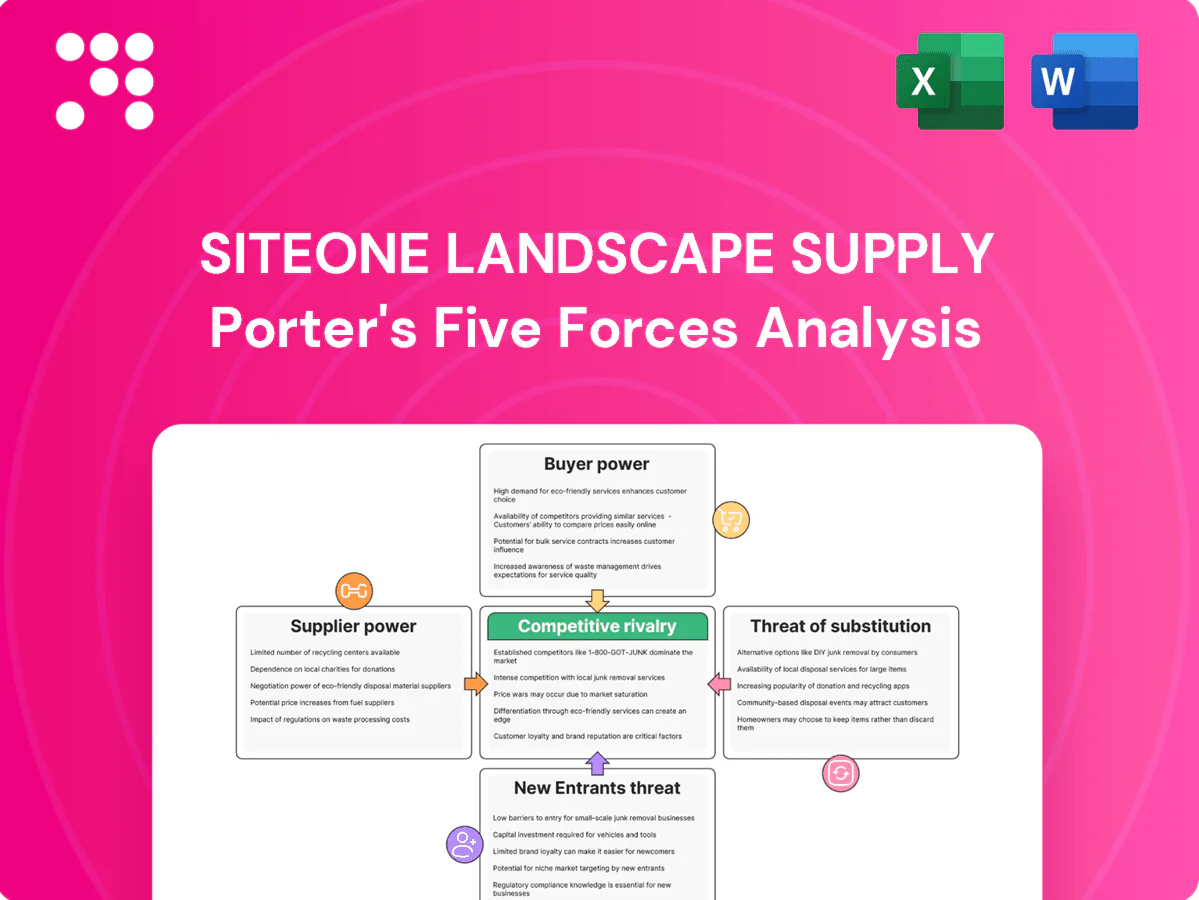

This Porter’s Five Forces analysis of SiteOne Landscape Supply evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products, offering clear insights on pricing pressure and margin risks. It highlights strategic implications for growth, supplier management, and differentiation. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, ready to use.

Don't Miss the Bigger Picture

SiteOne Landscape Supply faces concentrated supplier and buyer power, regional competitive intensity, and moderate threat from substitutes—pressures that materially shape margins and growth prospects. This snapshot highlights key strategic levers but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for in-depth ratings, charts, and actionable implications. Purchase the complete report to inform investment and strategy decisions.

Suppliers Bargaining Power

Diversified supplier base dilutes leverage

SiteOne sources across numerous manufacturers in irrigation, fertilizer, hardscapes, lighting and nursery inputs, which dilutes any single vendor’s leverage; multi-sourcing and comparable SKUs enable substitution while geographic breadth across the U.S. and Canada lets the company balance regional supply shocks. With FY2024 net sales near $4.0 billion this scale reduces supplier power, though niche specialty items with few makers still retain pricing clout.

Branded manufacturers retain category influence

Top irrigation and lighting brands such as Hunter, Toro and Rain Bird command terms through contractor preference and spec-driven demand, with vendor programs, rebates and MAP policies constraining distributor pricing. SiteOne’s scale—roughly 700 branches and about $6.8 billion revenue in 2024—helps win allocations but it must carry key brands to remain competitive. This dynamic sustains moderate supplier bargaining power.

Logistics, lead times, and seasonality create dependence

Peak-season demand and long lead times for hardscapes and fertilizers heighten SiteOne's reliance on timely supplier deliveries; SiteOne reported net sales of about $6.1 billion in fiscal 2024, concentrating risk during seasonal peaks. Rising freight costs and capacity constraints have shifted margin toward vendors, while weather-driven volatility limits distributor negotiating flexibility. In shortages, supplier allocation practices favor vendors with greater leverage, constraining SiteOne's purchasing power.

Private label and scale rebates counterbalance

SiteOne leverages private label and aggregated purchasing to extract better terms from suppliers, helping sustain fiscal 2024 sales of about $4.6 billion and a retail footprint of over 700 branches. Volume rebates, marketing funds and joint planning with vendors reduce supplier rent-seeking; private brands provide alternatives where specs allow, dampening vendor leverage in commodity-like categories.

- Private label scale: over 700 branches

- Fiscal 2024 sales: ~$4.6B

- Rebates/marketing funds offset supplier power

Specialized/regulated inputs raise switching costs

Specialized inputs like EPA-regulated chemicals, UL-listed code-compliant lighting, and proprietary irrigation controllers often require vendor-tied certifications and training, raising switching costs for SiteOne; compatibility and warranty constraints limit rapid vendor changes, and vendor tech support and service agreements further entrench suppliers. These factors heighten supplier bargaining power in key product lines in 2024.

- EPA and UL certifications drive supplier lock-in

- Warranty/compatibility limit vendor switching

- Vendor tech support embeds relationships

- Increases supplier bargaining power in select lines

Moderate supplier power vs scale: ~$6.1B, ~700 branches

SiteOne faces moderate supplier power: diversified vendor base, private-label scale and ~700 branches counterbalance supplier leverage, but key brands (Toro, Rain Bird) and specialty items (EPA/UL-regulated, proprietary controllers) retain pricing/control, especially during seasonal peaks; FY2024 sales ~ $6.1B amplify purchasing clout but do not eliminate supplier rent-seeking.

| Metric | 2024 |

|---|---|

| Branches | ~700 |

| Net sales | ~$6.1B |

| Supplier power | Moderate |

What is included in the product

Concise Porter's Five Forces analysis for SiteOne Landscape Supply, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and barriers to entry that shape margins and growth. Includes strategic insights on disruptive risks and defensive levers to protect market share and pricing power.

A concise Porter's Five Forces summary tailored to SiteOne—streamlines competitive pressure analysis for faster, confident decisions. Swap in your metrics, visualize threats with a radar view, and copy straight into decks to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Fragmented contractor base limits buyer leverage

Local landscapers and small contractors — estimated at over 1 million firms in the US (2024) — comprise much of SiteOne’s demand, limiting coordinated bargaining and buyer leverage. Many prioritize proximity, inventory breadth and trade credit over small price differences, and service needs plus rapid delivery further reduce price-only switching. This long tail of customers moderates overall buyer power.

Large nationals and bid work press pricing

National maintenance firms and large installers centralize procurement, demanding volume discounts that compress margins; SiteOne reported roughly $6.0 billion in FY2024 sales, highlighting exposure to these accounts. Competitive project bids require transparent quotes and enable multi-sourcing across regions, leading to double-digit negotiated discounts in many contracts and higher customer bargaining power with tighter margins.

Price sensitivity in commodity categories

Fertilizers, pipe and basic fittings at SiteOne face intense price sensitivity in 2024 as commodity SKUs are readily compared and substituted; buyers routinely switch equivalent-spec products to shave costs. Promotions and rebates — frequently used in 2024 trade programs — further tilt purchasing toward lower-cost suppliers, elevating buyer leverage in these commoditized lines and pressuring margin recovery for distributors; SiteOne reported approximately $5.4 billion in net sales in FY2024.

Service bundling and credit reduce switching

Service bundling — design support, training, jobsite delivery and business solutions — embeds SiteOne into contractor workflows, and with a 2024 branch network exceeding 700 locations these services make switching operationally costly. Trade credit and dedicated account management, part of their commercial offering, increase receivable stickiness. Custom takeoffs and spec assistance create perceived switching costs that temper buyer power.

- Design support: integrated into workflows

- Trade credit: strengthens account retention

- Custom takeoffs: perceived switching costs

- 700+ branches (2024): local presence boosts stickiness

Omnichannel transparency increases options

Omnichannel transparency increases options: online catalogs and competitor e-commerce reveal pricing and availability in real time, enabling customers to compare SiteOne (about 700 locations) with retail pro desks and regional rivals; digital tools narrow information asymmetry and lift buyer power where online alternatives meet needs.

- Online visibility: real-time price/stock comparisons

- Channels: retail pro desks, regional rivals, e-commerce

- Effect: higher buyer leverage when online substitutes suffice

Fragmented landscaper demand limits buyer power; 700+ branches raise switching costs

Local landscapers (>1M US firms) limit coordinated buyer power; convenience, inventory breadth and trade credit reduce price-only switching. National installers extract volume discounts; SiteOne reported ~$6.0B FY2024 sales. Commoditized SKUs face high price sensitivity; omnichannel visibility and 700+ branches raise comparison but service bundling creates switching costs.

| Metric | 2024 |

|---|---|

| FY2024 Sales | $6.0B |

| Net sales (commodities) | $5.4B |

| Branches | 700+ |

| US landscaper firms | >1M |

Same Document Delivered

SiteOne Landscape Supply Porter's Five Forces Analysis

This Porter’s Five Forces analysis of SiteOne Landscape Supply evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products, offering clear insights on pricing pressure and margin risks. It highlights strategic implications for growth, supplier management, and differentiation. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, ready to use.

Description

Don't Miss the Bigger Picture

SiteOne Landscape Supply faces concentrated supplier and buyer power, regional competitive intensity, and moderate threat from substitutes—pressures that materially shape margins and growth prospects. This snapshot highlights key strategic levers but omits force-by-force ratings and visuals. Unlock the full Porter's Five Forces Analysis for in-depth ratings, charts, and actionable implications. Purchase the complete report to inform investment and strategy decisions.

Suppliers Bargaining Power

Diversified supplier base dilutes leverage

SiteOne sources across numerous manufacturers in irrigation, fertilizer, hardscapes, lighting and nursery inputs, which dilutes any single vendor’s leverage; multi-sourcing and comparable SKUs enable substitution while geographic breadth across the U.S. and Canada lets the company balance regional supply shocks. With FY2024 net sales near $4.0 billion this scale reduces supplier power, though niche specialty items with few makers still retain pricing clout.

Branded manufacturers retain category influence

Top irrigation and lighting brands such as Hunter, Toro and Rain Bird command terms through contractor preference and spec-driven demand, with vendor programs, rebates and MAP policies constraining distributor pricing. SiteOne’s scale—roughly 700 branches and about $6.8 billion revenue in 2024—helps win allocations but it must carry key brands to remain competitive. This dynamic sustains moderate supplier bargaining power.

Logistics, lead times, and seasonality create dependence

Peak-season demand and long lead times for hardscapes and fertilizers heighten SiteOne's reliance on timely supplier deliveries; SiteOne reported net sales of about $6.1 billion in fiscal 2024, concentrating risk during seasonal peaks. Rising freight costs and capacity constraints have shifted margin toward vendors, while weather-driven volatility limits distributor negotiating flexibility. In shortages, supplier allocation practices favor vendors with greater leverage, constraining SiteOne's purchasing power.

Private label and scale rebates counterbalance

SiteOne leverages private label and aggregated purchasing to extract better terms from suppliers, helping sustain fiscal 2024 sales of about $4.6 billion and a retail footprint of over 700 branches. Volume rebates, marketing funds and joint planning with vendors reduce supplier rent-seeking; private brands provide alternatives where specs allow, dampening vendor leverage in commodity-like categories.

- Private label scale: over 700 branches

- Fiscal 2024 sales: ~$4.6B

- Rebates/marketing funds offset supplier power

Specialized/regulated inputs raise switching costs

Specialized inputs like EPA-regulated chemicals, UL-listed code-compliant lighting, and proprietary irrigation controllers often require vendor-tied certifications and training, raising switching costs for SiteOne; compatibility and warranty constraints limit rapid vendor changes, and vendor tech support and service agreements further entrench suppliers. These factors heighten supplier bargaining power in key product lines in 2024.

- EPA and UL certifications drive supplier lock-in

- Warranty/compatibility limit vendor switching

- Vendor tech support embeds relationships

- Increases supplier bargaining power in select lines

Moderate supplier power vs scale: ~$6.1B, ~700 branches

SiteOne faces moderate supplier power: diversified vendor base, private-label scale and ~700 branches counterbalance supplier leverage, but key brands (Toro, Rain Bird) and specialty items (EPA/UL-regulated, proprietary controllers) retain pricing/control, especially during seasonal peaks; FY2024 sales ~ $6.1B amplify purchasing clout but do not eliminate supplier rent-seeking.

| Metric | 2024 |

|---|---|

| Branches | ~700 |

| Net sales | ~$6.1B |

| Supplier power | Moderate |

What is included in the product

Concise Porter's Five Forces analysis for SiteOne Landscape Supply, uncovering competitive intensity, buyer and supplier power, threat of substitutes, and barriers to entry that shape margins and growth. Includes strategic insights on disruptive risks and defensive levers to protect market share and pricing power.

A concise Porter's Five Forces summary tailored to SiteOne—streamlines competitive pressure analysis for faster, confident decisions. Swap in your metrics, visualize threats with a radar view, and copy straight into decks to relieve strategic analysis bottlenecks.

Customers Bargaining Power

Fragmented contractor base limits buyer leverage

Local landscapers and small contractors — estimated at over 1 million firms in the US (2024) — comprise much of SiteOne’s demand, limiting coordinated bargaining and buyer leverage. Many prioritize proximity, inventory breadth and trade credit over small price differences, and service needs plus rapid delivery further reduce price-only switching. This long tail of customers moderates overall buyer power.

Large nationals and bid work press pricing

National maintenance firms and large installers centralize procurement, demanding volume discounts that compress margins; SiteOne reported roughly $6.0 billion in FY2024 sales, highlighting exposure to these accounts. Competitive project bids require transparent quotes and enable multi-sourcing across regions, leading to double-digit negotiated discounts in many contracts and higher customer bargaining power with tighter margins.

Price sensitivity in commodity categories

Fertilizers, pipe and basic fittings at SiteOne face intense price sensitivity in 2024 as commodity SKUs are readily compared and substituted; buyers routinely switch equivalent-spec products to shave costs. Promotions and rebates — frequently used in 2024 trade programs — further tilt purchasing toward lower-cost suppliers, elevating buyer leverage in these commoditized lines and pressuring margin recovery for distributors; SiteOne reported approximately $5.4 billion in net sales in FY2024.

Service bundling and credit reduce switching

Service bundling — design support, training, jobsite delivery and business solutions — embeds SiteOne into contractor workflows, and with a 2024 branch network exceeding 700 locations these services make switching operationally costly. Trade credit and dedicated account management, part of their commercial offering, increase receivable stickiness. Custom takeoffs and spec assistance create perceived switching costs that temper buyer power.

- Design support: integrated into workflows

- Trade credit: strengthens account retention

- Custom takeoffs: perceived switching costs

- 700+ branches (2024): local presence boosts stickiness

Omnichannel transparency increases options

Omnichannel transparency increases options: online catalogs and competitor e-commerce reveal pricing and availability in real time, enabling customers to compare SiteOne (about 700 locations) with retail pro desks and regional rivals; digital tools narrow information asymmetry and lift buyer power where online alternatives meet needs.

- Online visibility: real-time price/stock comparisons

- Channels: retail pro desks, regional rivals, e-commerce

- Effect: higher buyer leverage when online substitutes suffice

Fragmented landscaper demand limits buyer power; 700+ branches raise switching costs

Local landscapers (>1M US firms) limit coordinated buyer power; convenience, inventory breadth and trade credit reduce price-only switching. National installers extract volume discounts; SiteOne reported ~$6.0B FY2024 sales. Commoditized SKUs face high price sensitivity; omnichannel visibility and 700+ branches raise comparison but service bundling creates switching costs.

| Metric | 2024 |

|---|---|

| FY2024 Sales | $6.0B |

| Net sales (commodities) | $5.4B |

| Branches | 700+ |

| US landscaper firms | >1M |

Same Document Delivered

SiteOne Landscape Supply Porter's Five Forces Analysis

This Porter’s Five Forces analysis of SiteOne Landscape Supply evaluates competitive rivalry, supplier and buyer power, threat of new entrants, and substitute products, offering clear insights on pricing pressure and margin risks. It highlights strategic implications for growth, supplier management, and differentiation. This preview is the exact, fully formatted document you’ll receive immediately after purchase—no placeholders, ready to use.