Skyward Specialty Insurance SWOT Analysis

Make Insightful Decisions Backed by Expert Research

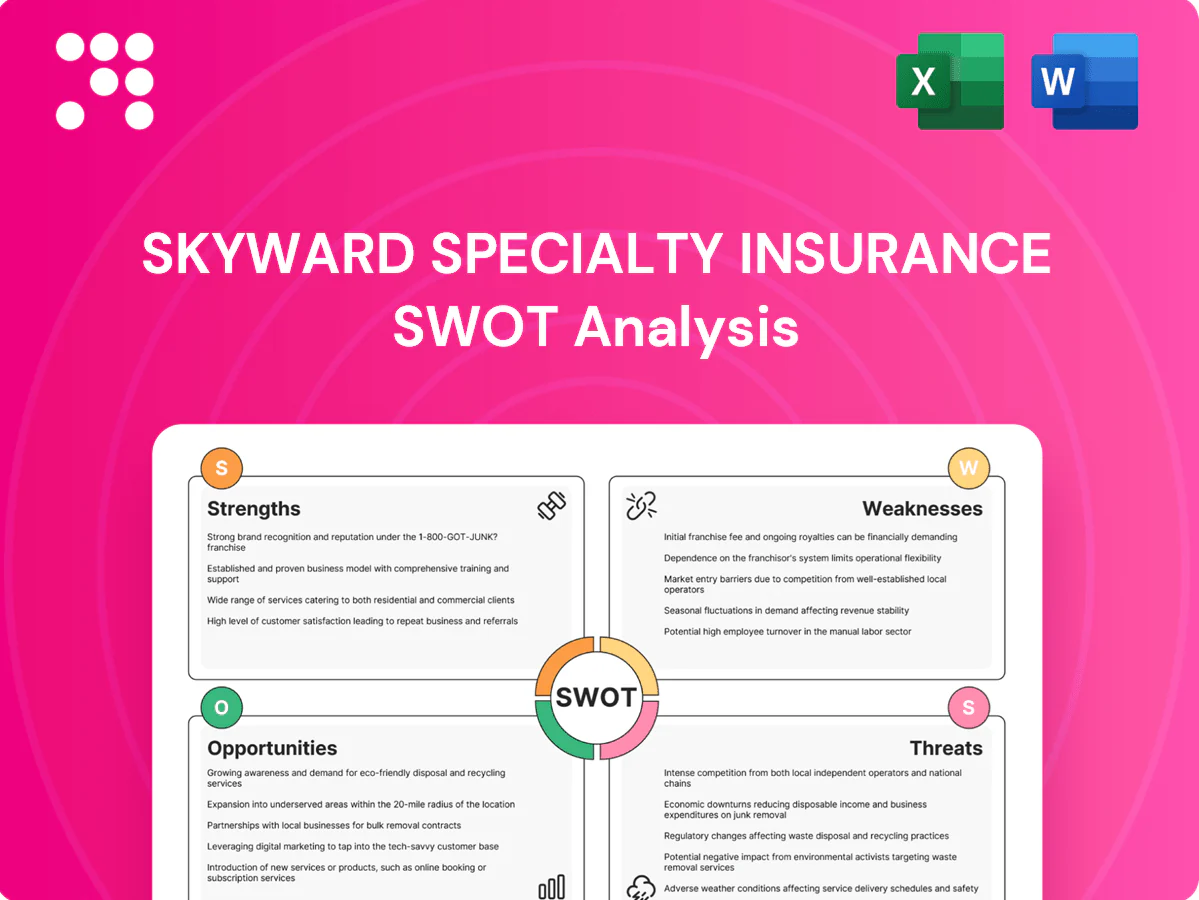

Skyward Specialty Insurance shows niche underwriting expertise, targeted product breadth, and strong reinsurance relationships, yet faces exposure to catastrophe losses and competitive pricing pressure. Our SWOT preview highlights core strengths, vulnerabilities, and growth vectors critical for underwriting and investment decisions. Purchase the full SWOT analysis for a detailed, editable report and Excel matrix to inform strategy and due diligence.

Strengths

Niche underwriting expertise

Deep specialization enables disciplined risk selection in complex, underserved classes, driving loss ratios materially below broad-market peers (2024 specialty median loss ratio ~62% vs broad P&C ~68%).

Diverse specialty product mix

Skyward’s diverse specialty product mix—spanning professional lines, surety, general liability and other commercial segments—lowers concentration risk and allows capacity to be reallocated to higher-return niches during hard/soft cycles. Cross-sell opportunities bolster unit economics and agent stickiness by increasing wallet share and renewal rates. Product breadth enhances resilience by shifting focus to the most attractive pockets as market conditions evolve.

Broker and program administrator network

Skyward’s broker and program administrator network leverages strong distribution partnerships to expand reach into targeted niches cost-effectively; MGAs and program managers accounted for roughly 10% of US P&C premiums in 2023, underscoring scale. These partners deliver curated books with embedded expertise, accelerate speed-to-market and pipeline visibility, and enable data feedback loops to refine underwriting.

Customized coverage and risk solutions

Skyward Specialty Insurance leverages tailored policy forms and risk management services to compete on value rather than price, addressing exposures standard forms miss and enabling more precise risk selection aligned with insureds’ operations, which drives higher client satisfaction and renewal rates.

- Tailored forms

- Risk management services

- Improved risk selection

- Higher satisfaction & renewals

Relationship-driven operating model

Skyward Specialty’s relationship-driven operating model focuses on long-term producer and client ties that stabilize submissions and improve flow quality; trusted partnerships encourage more complete data sharing, yielding better underwriting outcomes and loss selection.

- Supports pricing discipline in soft markets

- Enhances data completeness for underwriting

- Reinforces reliable claims-handling perceptions

Specialty P&C: Lower Loss Ratios, Higher Returns, and MGA-Driven Distribution Edge

Deep specialization yields disciplined risk selection and loss ratios materially below peers (2024 specialty median ~62% vs broad P&C ~68%).

Diverse specialty mix reduces concentration and enables reallocation to higher-return niches while supporting cross-sell and stronger unit economics.

Broker/MGA distribution (MGAs ~10% of US P&C premiums in 2023) plus tailored forms improve underwriting, client satisfaction and renewals.

| Metric | Value |

|---|---|

| 2024 specialty median loss ratio | ~62% |

| 2024 broad P&C median loss ratio | ~68% |

| MGAs share of US P&C (2023) | ~10% |

What is included in the product

Provides a concise SWOT overview of Skyward Specialty Insurance, highlighting core strengths and operational weaknesses while mapping market opportunities and external threats that shape its strategic positioning.

Provides a focused SWOT matrix tailored to Skyward Specialty Insurance for rapid identification of strategic risks and opportunities, enabling executives and teams to align response plans and simplify stakeholder briefings.

Weaknesses

Scale relative to major carriers

Smaller scale limits Skyward Specialty’s ability to absorb fixed costs and weakens negotiating leverage with brokers and reinsurers, often resulting in higher per-policy expense ratios. Elevated reinsurance pricing pressures underwriting margins and can force tighter capacity or higher premiums. Constrained capital availability may slow rapid deployment of capacity and reduces diversification across catastrophe and long-tail portfolios.

Distribution concentration risk

Reliance on select brokers and program administrators creates dependency; the top four brokers—Marsh, Aon, Willis Towers Watson and Gallagher—control roughly 65% of global brokerage revenue, concentrating placement power. Loss of a key partner could materially reduce premium volume and distribution reach. Conflicts over commission or underwriting control may arise, while monitoring delegated authority increases compliance and oversight costs.

Exposure to niche volatility

Specialty niches can swing quickly with regulatory or litigation shifts, exposing Skyward to concentrated tail risk in areas like cyber or professional liability. Smaller premium bases magnify loss-ratio volatility: a single $50m loss against $200m of earned premium would lift loss ratio by 25 percentage points. Data scarcity in emerging classes hinders pricing—cyber premiums rose about 30% in 2023—and fast niche growth risks adverse selection.

Operational complexity from customization

Bespoke coverage drives policy administration variability and friction, as nonstandard wordings and modules require more manual review and bespoke workflows. Complex endorsements raise error risk and extend underwriting and issuance cycle times, while claims handling needs specialized adjuster expertise for niche exposures. Without rigorous process design this can elevate expense ratios and slow responsiveness.

- Administration variability

- Higher endorsement error risk

- Specialized adjuster dependency

- Upward pressure on expense ratios

Reserve and long-tail uncertainty

Reserve and long-tail uncertainty is pronounced in Skyward Specialty's professional lines and select casualty portfolios where latent severity and social inflation trends have driven adverse development industry-wide; limited vintage data in newer programs amplifies this uncertainty and forces materially conservative reserves that can suppress reported ROE during growth phases.

- latent severity risk

- social inflation/legal trends

- thin loss history in new programs

- conservative reserving dampens ROE

$200m insurer, brokers 65%, reinsurance +10% squeeze ROE

Smaller scale (earned premium ~$200m) raises per-policy expense and weakens reinsurance/broker leverage. Top-four brokers hold ~65% placement power, concentrating distribution risk. Reinsurance pricing up ~10% in 2024 and cyber premiums rose ~30% in 2023, amplifying underwriting and reserve pressure. Thin vintage data and social inflation force conservative reserves, compressing ROE.

| Metric | Value |

|---|---|

| Earned premium | $200m |

| Broker concentration | 65% |

| Reinsurance price change (2024) | +10% |

| Cyber premium change (2023) | +30% |

| Single $50m loss impact | +25 ppt loss ratio |

Same Document Delivered

Skyward Specialty Insurance SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview shown below is taken directly from the full Skyward Specialty Insurance SWOT report you'll get; purchase unlocks the editable, complete version. Buy now to download the full, structured analysis ready for use.

Make Insightful Decisions Backed by Expert Research

Skyward Specialty Insurance shows niche underwriting expertise, targeted product breadth, and strong reinsurance relationships, yet faces exposure to catastrophe losses and competitive pricing pressure. Our SWOT preview highlights core strengths, vulnerabilities, and growth vectors critical for underwriting and investment decisions. Purchase the full SWOT analysis for a detailed, editable report and Excel matrix to inform strategy and due diligence.

Strengths

Niche underwriting expertise

Deep specialization enables disciplined risk selection in complex, underserved classes, driving loss ratios materially below broad-market peers (2024 specialty median loss ratio ~62% vs broad P&C ~68%).

Diverse specialty product mix

Skyward’s diverse specialty product mix—spanning professional lines, surety, general liability and other commercial segments—lowers concentration risk and allows capacity to be reallocated to higher-return niches during hard/soft cycles. Cross-sell opportunities bolster unit economics and agent stickiness by increasing wallet share and renewal rates. Product breadth enhances resilience by shifting focus to the most attractive pockets as market conditions evolve.

Broker and program administrator network

Skyward’s broker and program administrator network leverages strong distribution partnerships to expand reach into targeted niches cost-effectively; MGAs and program managers accounted for roughly 10% of US P&C premiums in 2023, underscoring scale. These partners deliver curated books with embedded expertise, accelerate speed-to-market and pipeline visibility, and enable data feedback loops to refine underwriting.

Customized coverage and risk solutions

Skyward Specialty Insurance leverages tailored policy forms and risk management services to compete on value rather than price, addressing exposures standard forms miss and enabling more precise risk selection aligned with insureds’ operations, which drives higher client satisfaction and renewal rates.

- Tailored forms

- Risk management services

- Improved risk selection

- Higher satisfaction & renewals

Relationship-driven operating model

Skyward Specialty’s relationship-driven operating model focuses on long-term producer and client ties that stabilize submissions and improve flow quality; trusted partnerships encourage more complete data sharing, yielding better underwriting outcomes and loss selection.

- Supports pricing discipline in soft markets

- Enhances data completeness for underwriting

- Reinforces reliable claims-handling perceptions

Specialty P&C: Lower Loss Ratios, Higher Returns, and MGA-Driven Distribution Edge

Deep specialization yields disciplined risk selection and loss ratios materially below peers (2024 specialty median ~62% vs broad P&C ~68%).

Diverse specialty mix reduces concentration and enables reallocation to higher-return niches while supporting cross-sell and stronger unit economics.

Broker/MGA distribution (MGAs ~10% of US P&C premiums in 2023) plus tailored forms improve underwriting, client satisfaction and renewals.

| Metric | Value |

|---|---|

| 2024 specialty median loss ratio | ~62% |

| 2024 broad P&C median loss ratio | ~68% |

| MGAs share of US P&C (2023) | ~10% |

What is included in the product

Provides a concise SWOT overview of Skyward Specialty Insurance, highlighting core strengths and operational weaknesses while mapping market opportunities and external threats that shape its strategic positioning.

Provides a focused SWOT matrix tailored to Skyward Specialty Insurance for rapid identification of strategic risks and opportunities, enabling executives and teams to align response plans and simplify stakeholder briefings.

Weaknesses

Scale relative to major carriers

Smaller scale limits Skyward Specialty’s ability to absorb fixed costs and weakens negotiating leverage with brokers and reinsurers, often resulting in higher per-policy expense ratios. Elevated reinsurance pricing pressures underwriting margins and can force tighter capacity or higher premiums. Constrained capital availability may slow rapid deployment of capacity and reduces diversification across catastrophe and long-tail portfolios.

Distribution concentration risk

Reliance on select brokers and program administrators creates dependency; the top four brokers—Marsh, Aon, Willis Towers Watson and Gallagher—control roughly 65% of global brokerage revenue, concentrating placement power. Loss of a key partner could materially reduce premium volume and distribution reach. Conflicts over commission or underwriting control may arise, while monitoring delegated authority increases compliance and oversight costs.

Exposure to niche volatility

Specialty niches can swing quickly with regulatory or litigation shifts, exposing Skyward to concentrated tail risk in areas like cyber or professional liability. Smaller premium bases magnify loss-ratio volatility: a single $50m loss against $200m of earned premium would lift loss ratio by 25 percentage points. Data scarcity in emerging classes hinders pricing—cyber premiums rose about 30% in 2023—and fast niche growth risks adverse selection.

Operational complexity from customization

Bespoke coverage drives policy administration variability and friction, as nonstandard wordings and modules require more manual review and bespoke workflows. Complex endorsements raise error risk and extend underwriting and issuance cycle times, while claims handling needs specialized adjuster expertise for niche exposures. Without rigorous process design this can elevate expense ratios and slow responsiveness.

- Administration variability

- Higher endorsement error risk

- Specialized adjuster dependency

- Upward pressure on expense ratios

Reserve and long-tail uncertainty

Reserve and long-tail uncertainty is pronounced in Skyward Specialty's professional lines and select casualty portfolios where latent severity and social inflation trends have driven adverse development industry-wide; limited vintage data in newer programs amplifies this uncertainty and forces materially conservative reserves that can suppress reported ROE during growth phases.

- latent severity risk

- social inflation/legal trends

- thin loss history in new programs

- conservative reserving dampens ROE

$200m insurer, brokers 65%, reinsurance +10% squeeze ROE

Smaller scale (earned premium ~$200m) raises per-policy expense and weakens reinsurance/broker leverage. Top-four brokers hold ~65% placement power, concentrating distribution risk. Reinsurance pricing up ~10% in 2024 and cyber premiums rose ~30% in 2023, amplifying underwriting and reserve pressure. Thin vintage data and social inflation force conservative reserves, compressing ROE.

| Metric | Value |

|---|---|

| Earned premium | $200m |

| Broker concentration | 65% |

| Reinsurance price change (2024) | +10% |

| Cyber premium change (2023) | +30% |

| Single $50m loss impact | +25 ppt loss ratio |

Same Document Delivered

Skyward Specialty Insurance SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview shown below is taken directly from the full Skyward Specialty Insurance SWOT report you'll get; purchase unlocks the editable, complete version. Buy now to download the full, structured analysis ready for use.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Skyward Specialty Insurance shows niche underwriting expertise, targeted product breadth, and strong reinsurance relationships, yet faces exposure to catastrophe losses and competitive pricing pressure. Our SWOT preview highlights core strengths, vulnerabilities, and growth vectors critical for underwriting and investment decisions. Purchase the full SWOT analysis for a detailed, editable report and Excel matrix to inform strategy and due diligence.

Strengths

Niche underwriting expertise

Deep specialization enables disciplined risk selection in complex, underserved classes, driving loss ratios materially below broad-market peers (2024 specialty median loss ratio ~62% vs broad P&C ~68%).

Diverse specialty product mix

Skyward’s diverse specialty product mix—spanning professional lines, surety, general liability and other commercial segments—lowers concentration risk and allows capacity to be reallocated to higher-return niches during hard/soft cycles. Cross-sell opportunities bolster unit economics and agent stickiness by increasing wallet share and renewal rates. Product breadth enhances resilience by shifting focus to the most attractive pockets as market conditions evolve.

Broker and program administrator network

Skyward’s broker and program administrator network leverages strong distribution partnerships to expand reach into targeted niches cost-effectively; MGAs and program managers accounted for roughly 10% of US P&C premiums in 2023, underscoring scale. These partners deliver curated books with embedded expertise, accelerate speed-to-market and pipeline visibility, and enable data feedback loops to refine underwriting.

Customized coverage and risk solutions

Skyward Specialty Insurance leverages tailored policy forms and risk management services to compete on value rather than price, addressing exposures standard forms miss and enabling more precise risk selection aligned with insureds’ operations, which drives higher client satisfaction and renewal rates.

- Tailored forms

- Risk management services

- Improved risk selection

- Higher satisfaction & renewals

Relationship-driven operating model

Skyward Specialty’s relationship-driven operating model focuses on long-term producer and client ties that stabilize submissions and improve flow quality; trusted partnerships encourage more complete data sharing, yielding better underwriting outcomes and loss selection.

- Supports pricing discipline in soft markets

- Enhances data completeness for underwriting

- Reinforces reliable claims-handling perceptions

Specialty P&C: Lower Loss Ratios, Higher Returns, and MGA-Driven Distribution Edge

Deep specialization yields disciplined risk selection and loss ratios materially below peers (2024 specialty median ~62% vs broad P&C ~68%).

Diverse specialty mix reduces concentration and enables reallocation to higher-return niches while supporting cross-sell and stronger unit economics.

Broker/MGA distribution (MGAs ~10% of US P&C premiums in 2023) plus tailored forms improve underwriting, client satisfaction and renewals.

| Metric | Value |

|---|---|

| 2024 specialty median loss ratio | ~62% |

| 2024 broad P&C median loss ratio | ~68% |

| MGAs share of US P&C (2023) | ~10% |

What is included in the product

Provides a concise SWOT overview of Skyward Specialty Insurance, highlighting core strengths and operational weaknesses while mapping market opportunities and external threats that shape its strategic positioning.

Provides a focused SWOT matrix tailored to Skyward Specialty Insurance for rapid identification of strategic risks and opportunities, enabling executives and teams to align response plans and simplify stakeholder briefings.

Weaknesses

Scale relative to major carriers

Smaller scale limits Skyward Specialty’s ability to absorb fixed costs and weakens negotiating leverage with brokers and reinsurers, often resulting in higher per-policy expense ratios. Elevated reinsurance pricing pressures underwriting margins and can force tighter capacity or higher premiums. Constrained capital availability may slow rapid deployment of capacity and reduces diversification across catastrophe and long-tail portfolios.

Distribution concentration risk

Reliance on select brokers and program administrators creates dependency; the top four brokers—Marsh, Aon, Willis Towers Watson and Gallagher—control roughly 65% of global brokerage revenue, concentrating placement power. Loss of a key partner could materially reduce premium volume and distribution reach. Conflicts over commission or underwriting control may arise, while monitoring delegated authority increases compliance and oversight costs.

Exposure to niche volatility

Specialty niches can swing quickly with regulatory or litigation shifts, exposing Skyward to concentrated tail risk in areas like cyber or professional liability. Smaller premium bases magnify loss-ratio volatility: a single $50m loss against $200m of earned premium would lift loss ratio by 25 percentage points. Data scarcity in emerging classes hinders pricing—cyber premiums rose about 30% in 2023—and fast niche growth risks adverse selection.

Operational complexity from customization

Bespoke coverage drives policy administration variability and friction, as nonstandard wordings and modules require more manual review and bespoke workflows. Complex endorsements raise error risk and extend underwriting and issuance cycle times, while claims handling needs specialized adjuster expertise for niche exposures. Without rigorous process design this can elevate expense ratios and slow responsiveness.

- Administration variability

- Higher endorsement error risk

- Specialized adjuster dependency

- Upward pressure on expense ratios

Reserve and long-tail uncertainty

Reserve and long-tail uncertainty is pronounced in Skyward Specialty's professional lines and select casualty portfolios where latent severity and social inflation trends have driven adverse development industry-wide; limited vintage data in newer programs amplifies this uncertainty and forces materially conservative reserves that can suppress reported ROE during growth phases.

- latent severity risk

- social inflation/legal trends

- thin loss history in new programs

- conservative reserving dampens ROE

$200m insurer, brokers 65%, reinsurance +10% squeeze ROE

Smaller scale (earned premium ~$200m) raises per-policy expense and weakens reinsurance/broker leverage. Top-four brokers hold ~65% placement power, concentrating distribution risk. Reinsurance pricing up ~10% in 2024 and cyber premiums rose ~30% in 2023, amplifying underwriting and reserve pressure. Thin vintage data and social inflation force conservative reserves, compressing ROE.

| Metric | Value |

|---|---|

| Earned premium | $200m |

| Broker concentration | 65% |

| Reinsurance price change (2024) | +10% |

| Cyber premium change (2023) | +30% |

| Single $50m loss impact | +25 ppt loss ratio |

Same Document Delivered

Skyward Specialty Insurance SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview shown below is taken directly from the full Skyward Specialty Insurance SWOT report you'll get; purchase unlocks the editable, complete version. Buy now to download the full, structured analysis ready for use.