Skyworth SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Skyworth shows strong product innovation and expanding global TV and smart-home reach, yet faces supply-chain strain and intense competition; our SWOT highlights strategic risks and opportunit ies for growth. Unlock detailed, research-backed findings, financial context, and tactical recommendations. Purchase the full SWOT for a ready-to-use Word report and editable Excel matrix to inform investment or strategic decisions.

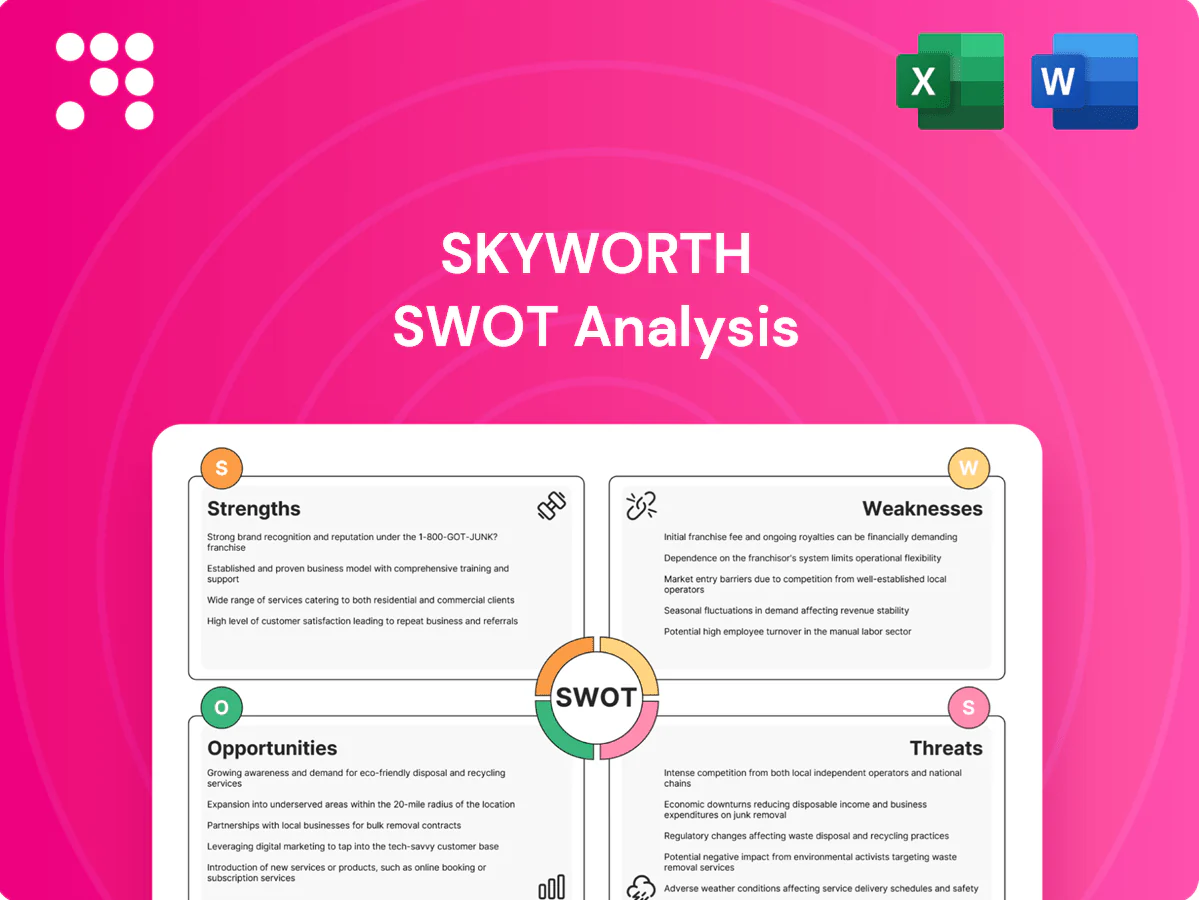

Strengths

Diversified consumer electronics portfolio

Skyworth’s diversified lineup across TVs, set-top boxes, appliances, displays, automotive electronics and security systems cuts dependence on any single category, supporting cross-selling that boosts channel ties and retailer shelf space; this portfolio helped Skyworth deliver RMB 41.2 billion revenue in 2024 and maintain a top-8 global TV shipment position (~10 million units), smoothing revenue through product cycles and regional demand swings.

Manufacturing scale and OEM/ODM capabilities

Skyworth’s ability to produce under its own brand and as an OEM/ODM drives factory utilization—supporting annual TV output of over 10 million units and consolidated revenue that exceeded RMB 30 billion in 2024. OEM/ODM contracts supply steady baseline orders and increase customer stickiness, with partner business representing a substantial share of volumes. Scale enables Skyworth to negotiate component costs more aggressively and shorten time-to-market for new models, improving gross margin resilience.

R&D in display and smart device integration

Core strengths in TV and display engineering — reflected in Skyworth’s >12 million TV shipments in 2023 — sustain competitive image quality and feature sets across price tiers.

Deep integration of connectivity and software in smart TVs and appliances raises user value and supports growing IoT services and aftermarket software monetization.

In-house engineering shortens iteration cycles on panels, backlights and image-processing, accelerating product refresh cadence and time-to-market.

Global distribution network

Skyworth’s global distribution network spans 100+ countries and regions, diversifying geopolitical and macro risk by spreading revenue streams across Asia, Europe, the Americas and Africa; 2024 group revenue reached RMB 37.2 billion, underpinning channel investments. Multi-channel routes—retail, e-commerce and B2B—boost market reach and helped grow overseas sales share in 2024. Localized product specs and certifications ensure compliance with country standards and faster market entry.

- Global footprint: 100+ countries/regions

- 2024 revenue: RMB 37.2 billion

- Channels: retail, e-commerce, B2B

- Localized specs & certifications

Value-oriented brand positioning

Skyworths value-oriented price-to-performance mix has driven share gains in price-sensitive segments, supporting expansion in emerging markets; Omdia ranked Skyworth among the top six global TV vendors by shipments in 2024, with an estimated ~6% global TV market share. This strong value branding appeals to cost-conscious consumers and drives volume, improving economies of scale and lowering unit costs.

- price-to-performance

- emerging-markets

- volume-driven-economies

Diversified electronics: RMB 37.2bn revenue, ~10m TVs, ~6% global TV share

Skyworth’s diversified portfolio (TVs, appliances, automotive, security) and strong value positioning drove RMB 37.2 billion revenue in 2024 and ~6% global TV share; TV shipments were ~10 million in 2024, smoothing cycles. OEM/ODM plus in-house R&D sustain annual TV output >10 million and faster product refresh, while a 100+ country footprint diversifies geopolitical risk.

| Metric | Period | Value |

|---|---|---|

| Revenue | 2024 | RMB 37.2 billion |

| TV shipments | 2024 | ~10 million units |

| Global TV share | 2024 | ~6% |

| Footprint | 2024 | 100+ countries |

| OEM/ODM output | Annual | >10 million units |

What is included in the product

Examines the strengths, weaknesses, opportunities, and threats shaping Skyworth’s competitive position and strategic prospects in consumer electronics and smart TV markets.

Provides a concise, visual SWOT matrix tailored to Skyworth for rapid strategic alignment and easy inclusion in reports and stakeholder briefings.

Weaknesses

Exposure to commoditized hardware markets

Skyworth's core TVs, appliances and basic displays compete in commoditized segments where global TV shipments hovered around 200 million units in 2024, driving intense price-based competition. This commoditization has pressured gross margins across OEMs, pushing many panel-and-hardware players to low-single-digit margin bands and raising break-even volumes. Without strong software, recurring services or ecosystem lock-in, differentiation is difficult and margin recovery remains constrained.

Brand equity lagging premium incumbents

In developed markets Skyworth faces entrenched premium incumbents (Samsung, LG) that capture the majority of high-end shelf space and consumer mindshare, limiting Skyworth’s premium perception and pricing power. Premium panels and OLED models typically command ASPs roughly 2–3x mainstream LCD sets, capping Skyworth’s ability to lift overall ASPs without heavier R&D and product differentiation. Shifting preferences requires significantly higher marketing spend and channel investments to close perception gaps.

Limited proprietary software ecosystem

Reliance on third-party OS platforms like Google TV or Roku limits Skyworths control over UX, data access and update cadence, constraining differentiation. Platform owners can unilaterally change terms, features or monetisation—Google/Apple app-store fees are set at 15% for many developers—exposing device OEMs to margin shifts. Low services revenue means lower lifetime value per device and less recurring cash flow.

Component cost and FX sensitivity

Panel, semiconductor and logistics cost swings have compressed Skyworth margins in recent years as spot panel and chip market volatility persisted into 2024, and freight-rate spikes raised per-unit costs; currency moves further increased import costs and affected export pricing power. Hedging reduces exposure but cannot fully eliminate earnings volatility across sourcing and sales currencies.

- High component price sensitivity

- FX impacts import/export margins

- Hedging mitigates but not removes risk

Operational complexity from broad lineup

Managing a broad lineup across TVs, home appliances and smart devices increases supply-chain and inventory risks as parts and SKUs multiply, raising carrying costs and stock-out exposure.

Product lifecycle management and after-sales support grow more demanding across geographies, stretching warranty, logistics and service networks.

Complexity can dilute focus and R&D resources, slowing innovation cadence and raising per‑unit development costs.

- Supply-chain fragmentation

- Higher after-sales burden

- R&D resource dilution

Commoditized TV market, platform fees and supply volatility squeeze margins

Skyworth competes in commoditized TV/appliance markets (global TV shipments ~200 million in 2024), pressuring margins. Entrenched premium rivals and 2–3x ASP gap for OLED limit premium mix lift. Reliance on third-party OSes reduces UX/data control and faces app-store fees (~15%). Component, freight and FX volatility compressed margins and raised break-even volumes.

| Weakness | Metric | 2024 |

|---|---|---|

| Market commoditization | Global TV shipments | ~200M |

| Platform dependence | App-store fee | ~15% |

Preview the Actual Deliverable

Skyworth SWOT Analysis

This is the actual Skyworth SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy to unlock the complete, editable version. The file is structured, actionable, and ready for immediate use after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Skyworth shows strong product innovation and expanding global TV and smart-home reach, yet faces supply-chain strain and intense competition; our SWOT highlights strategic risks and opportunit ies for growth. Unlock detailed, research-backed findings, financial context, and tactical recommendations. Purchase the full SWOT for a ready-to-use Word report and editable Excel matrix to inform investment or strategic decisions.

Strengths

Diversified consumer electronics portfolio

Skyworth’s diversified lineup across TVs, set-top boxes, appliances, displays, automotive electronics and security systems cuts dependence on any single category, supporting cross-selling that boosts channel ties and retailer shelf space; this portfolio helped Skyworth deliver RMB 41.2 billion revenue in 2024 and maintain a top-8 global TV shipment position (~10 million units), smoothing revenue through product cycles and regional demand swings.

Manufacturing scale and OEM/ODM capabilities

Skyworth’s ability to produce under its own brand and as an OEM/ODM drives factory utilization—supporting annual TV output of over 10 million units and consolidated revenue that exceeded RMB 30 billion in 2024. OEM/ODM contracts supply steady baseline orders and increase customer stickiness, with partner business representing a substantial share of volumes. Scale enables Skyworth to negotiate component costs more aggressively and shorten time-to-market for new models, improving gross margin resilience.

R&D in display and smart device integration

Core strengths in TV and display engineering — reflected in Skyworth’s >12 million TV shipments in 2023 — sustain competitive image quality and feature sets across price tiers.

Deep integration of connectivity and software in smart TVs and appliances raises user value and supports growing IoT services and aftermarket software monetization.

In-house engineering shortens iteration cycles on panels, backlights and image-processing, accelerating product refresh cadence and time-to-market.

Global distribution network

Skyworth’s global distribution network spans 100+ countries and regions, diversifying geopolitical and macro risk by spreading revenue streams across Asia, Europe, the Americas and Africa; 2024 group revenue reached RMB 37.2 billion, underpinning channel investments. Multi-channel routes—retail, e-commerce and B2B—boost market reach and helped grow overseas sales share in 2024. Localized product specs and certifications ensure compliance with country standards and faster market entry.

- Global footprint: 100+ countries/regions

- 2024 revenue: RMB 37.2 billion

- Channels: retail, e-commerce, B2B

- Localized specs & certifications

Value-oriented brand positioning

Skyworths value-oriented price-to-performance mix has driven share gains in price-sensitive segments, supporting expansion in emerging markets; Omdia ranked Skyworth among the top six global TV vendors by shipments in 2024, with an estimated ~6% global TV market share. This strong value branding appeals to cost-conscious consumers and drives volume, improving economies of scale and lowering unit costs.

- price-to-performance

- emerging-markets

- volume-driven-economies

Diversified electronics: RMB 37.2bn revenue, ~10m TVs, ~6% global TV share

Skyworth’s diversified portfolio (TVs, appliances, automotive, security) and strong value positioning drove RMB 37.2 billion revenue in 2024 and ~6% global TV share; TV shipments were ~10 million in 2024, smoothing cycles. OEM/ODM plus in-house R&D sustain annual TV output >10 million and faster product refresh, while a 100+ country footprint diversifies geopolitical risk.

| Metric | Period | Value |

|---|---|---|

| Revenue | 2024 | RMB 37.2 billion |

| TV shipments | 2024 | ~10 million units |

| Global TV share | 2024 | ~6% |

| Footprint | 2024 | 100+ countries |

| OEM/ODM output | Annual | >10 million units |

What is included in the product

Examines the strengths, weaknesses, opportunities, and threats shaping Skyworth’s competitive position and strategic prospects in consumer electronics and smart TV markets.

Provides a concise, visual SWOT matrix tailored to Skyworth for rapid strategic alignment and easy inclusion in reports and stakeholder briefings.

Weaknesses

Exposure to commoditized hardware markets

Skyworth's core TVs, appliances and basic displays compete in commoditized segments where global TV shipments hovered around 200 million units in 2024, driving intense price-based competition. This commoditization has pressured gross margins across OEMs, pushing many panel-and-hardware players to low-single-digit margin bands and raising break-even volumes. Without strong software, recurring services or ecosystem lock-in, differentiation is difficult and margin recovery remains constrained.

Brand equity lagging premium incumbents

In developed markets Skyworth faces entrenched premium incumbents (Samsung, LG) that capture the majority of high-end shelf space and consumer mindshare, limiting Skyworth’s premium perception and pricing power. Premium panels and OLED models typically command ASPs roughly 2–3x mainstream LCD sets, capping Skyworth’s ability to lift overall ASPs without heavier R&D and product differentiation. Shifting preferences requires significantly higher marketing spend and channel investments to close perception gaps.

Limited proprietary software ecosystem

Reliance on third-party OS platforms like Google TV or Roku limits Skyworths control over UX, data access and update cadence, constraining differentiation. Platform owners can unilaterally change terms, features or monetisation—Google/Apple app-store fees are set at 15% for many developers—exposing device OEMs to margin shifts. Low services revenue means lower lifetime value per device and less recurring cash flow.

Component cost and FX sensitivity

Panel, semiconductor and logistics cost swings have compressed Skyworth margins in recent years as spot panel and chip market volatility persisted into 2024, and freight-rate spikes raised per-unit costs; currency moves further increased import costs and affected export pricing power. Hedging reduces exposure but cannot fully eliminate earnings volatility across sourcing and sales currencies.

- High component price sensitivity

- FX impacts import/export margins

- Hedging mitigates but not removes risk

Operational complexity from broad lineup

Managing a broad lineup across TVs, home appliances and smart devices increases supply-chain and inventory risks as parts and SKUs multiply, raising carrying costs and stock-out exposure.

Product lifecycle management and after-sales support grow more demanding across geographies, stretching warranty, logistics and service networks.

Complexity can dilute focus and R&D resources, slowing innovation cadence and raising per‑unit development costs.

- Supply-chain fragmentation

- Higher after-sales burden

- R&D resource dilution

Commoditized TV market, platform fees and supply volatility squeeze margins

Skyworth competes in commoditized TV/appliance markets (global TV shipments ~200 million in 2024), pressuring margins. Entrenched premium rivals and 2–3x ASP gap for OLED limit premium mix lift. Reliance on third-party OSes reduces UX/data control and faces app-store fees (~15%). Component, freight and FX volatility compressed margins and raised break-even volumes.

| Weakness | Metric | 2024 |

|---|---|---|

| Market commoditization | Global TV shipments | ~200M |

| Platform dependence | App-store fee | ~15% |

Preview the Actual Deliverable

Skyworth SWOT Analysis

This is the actual Skyworth SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy to unlock the complete, editable version. The file is structured, actionable, and ready for immediate use after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Skyworth shows strong product innovation and expanding global TV and smart-home reach, yet faces supply-chain strain and intense competition; our SWOT highlights strategic risks and opportunit ies for growth. Unlock detailed, research-backed findings, financial context, and tactical recommendations. Purchase the full SWOT for a ready-to-use Word report and editable Excel matrix to inform investment or strategic decisions.

Strengths

Diversified consumer electronics portfolio

Skyworth’s diversified lineup across TVs, set-top boxes, appliances, displays, automotive electronics and security systems cuts dependence on any single category, supporting cross-selling that boosts channel ties and retailer shelf space; this portfolio helped Skyworth deliver RMB 41.2 billion revenue in 2024 and maintain a top-8 global TV shipment position (~10 million units), smoothing revenue through product cycles and regional demand swings.

Manufacturing scale and OEM/ODM capabilities

Skyworth’s ability to produce under its own brand and as an OEM/ODM drives factory utilization—supporting annual TV output of over 10 million units and consolidated revenue that exceeded RMB 30 billion in 2024. OEM/ODM contracts supply steady baseline orders and increase customer stickiness, with partner business representing a substantial share of volumes. Scale enables Skyworth to negotiate component costs more aggressively and shorten time-to-market for new models, improving gross margin resilience.

R&D in display and smart device integration

Core strengths in TV and display engineering — reflected in Skyworth’s >12 million TV shipments in 2023 — sustain competitive image quality and feature sets across price tiers.

Deep integration of connectivity and software in smart TVs and appliances raises user value and supports growing IoT services and aftermarket software monetization.

In-house engineering shortens iteration cycles on panels, backlights and image-processing, accelerating product refresh cadence and time-to-market.

Global distribution network

Skyworth’s global distribution network spans 100+ countries and regions, diversifying geopolitical and macro risk by spreading revenue streams across Asia, Europe, the Americas and Africa; 2024 group revenue reached RMB 37.2 billion, underpinning channel investments. Multi-channel routes—retail, e-commerce and B2B—boost market reach and helped grow overseas sales share in 2024. Localized product specs and certifications ensure compliance with country standards and faster market entry.

- Global footprint: 100+ countries/regions

- 2024 revenue: RMB 37.2 billion

- Channels: retail, e-commerce, B2B

- Localized specs & certifications

Value-oriented brand positioning

Skyworths value-oriented price-to-performance mix has driven share gains in price-sensitive segments, supporting expansion in emerging markets; Omdia ranked Skyworth among the top six global TV vendors by shipments in 2024, with an estimated ~6% global TV market share. This strong value branding appeals to cost-conscious consumers and drives volume, improving economies of scale and lowering unit costs.

- price-to-performance

- emerging-markets

- volume-driven-economies

Diversified electronics: RMB 37.2bn revenue, ~10m TVs, ~6% global TV share

Skyworth’s diversified portfolio (TVs, appliances, automotive, security) and strong value positioning drove RMB 37.2 billion revenue in 2024 and ~6% global TV share; TV shipments were ~10 million in 2024, smoothing cycles. OEM/ODM plus in-house R&D sustain annual TV output >10 million and faster product refresh, while a 100+ country footprint diversifies geopolitical risk.

| Metric | Period | Value |

|---|---|---|

| Revenue | 2024 | RMB 37.2 billion |

| TV shipments | 2024 | ~10 million units |

| Global TV share | 2024 | ~6% |

| Footprint | 2024 | 100+ countries |

| OEM/ODM output | Annual | >10 million units |

What is included in the product

Examines the strengths, weaknesses, opportunities, and threats shaping Skyworth’s competitive position and strategic prospects in consumer electronics and smart TV markets.

Provides a concise, visual SWOT matrix tailored to Skyworth for rapid strategic alignment and easy inclusion in reports and stakeholder briefings.

Weaknesses

Exposure to commoditized hardware markets

Skyworth's core TVs, appliances and basic displays compete in commoditized segments where global TV shipments hovered around 200 million units in 2024, driving intense price-based competition. This commoditization has pressured gross margins across OEMs, pushing many panel-and-hardware players to low-single-digit margin bands and raising break-even volumes. Without strong software, recurring services or ecosystem lock-in, differentiation is difficult and margin recovery remains constrained.

Brand equity lagging premium incumbents

In developed markets Skyworth faces entrenched premium incumbents (Samsung, LG) that capture the majority of high-end shelf space and consumer mindshare, limiting Skyworth’s premium perception and pricing power. Premium panels and OLED models typically command ASPs roughly 2–3x mainstream LCD sets, capping Skyworth’s ability to lift overall ASPs without heavier R&D and product differentiation. Shifting preferences requires significantly higher marketing spend and channel investments to close perception gaps.

Limited proprietary software ecosystem

Reliance on third-party OS platforms like Google TV or Roku limits Skyworths control over UX, data access and update cadence, constraining differentiation. Platform owners can unilaterally change terms, features or monetisation—Google/Apple app-store fees are set at 15% for many developers—exposing device OEMs to margin shifts. Low services revenue means lower lifetime value per device and less recurring cash flow.

Component cost and FX sensitivity

Panel, semiconductor and logistics cost swings have compressed Skyworth margins in recent years as spot panel and chip market volatility persisted into 2024, and freight-rate spikes raised per-unit costs; currency moves further increased import costs and affected export pricing power. Hedging reduces exposure but cannot fully eliminate earnings volatility across sourcing and sales currencies.

- High component price sensitivity

- FX impacts import/export margins

- Hedging mitigates but not removes risk

Operational complexity from broad lineup

Managing a broad lineup across TVs, home appliances and smart devices increases supply-chain and inventory risks as parts and SKUs multiply, raising carrying costs and stock-out exposure.

Product lifecycle management and after-sales support grow more demanding across geographies, stretching warranty, logistics and service networks.

Complexity can dilute focus and R&D resources, slowing innovation cadence and raising per‑unit development costs.

- Supply-chain fragmentation

- Higher after-sales burden

- R&D resource dilution

Commoditized TV market, platform fees and supply volatility squeeze margins

Skyworth competes in commoditized TV/appliance markets (global TV shipments ~200 million in 2024), pressuring margins. Entrenched premium rivals and 2–3x ASP gap for OLED limit premium mix lift. Reliance on third-party OSes reduces UX/data control and faces app-store fees (~15%). Component, freight and FX volatility compressed margins and raised break-even volumes.

| Weakness | Metric | 2024 |

|---|---|---|

| Market commoditization | Global TV shipments | ~200M |

| Platform dependence | App-store fee | ~15% |

Preview the Actual Deliverable

Skyworth SWOT Analysis

This is the actual Skyworth SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy to unlock the complete, editable version. The file is structured, actionable, and ready for immediate use after checkout.