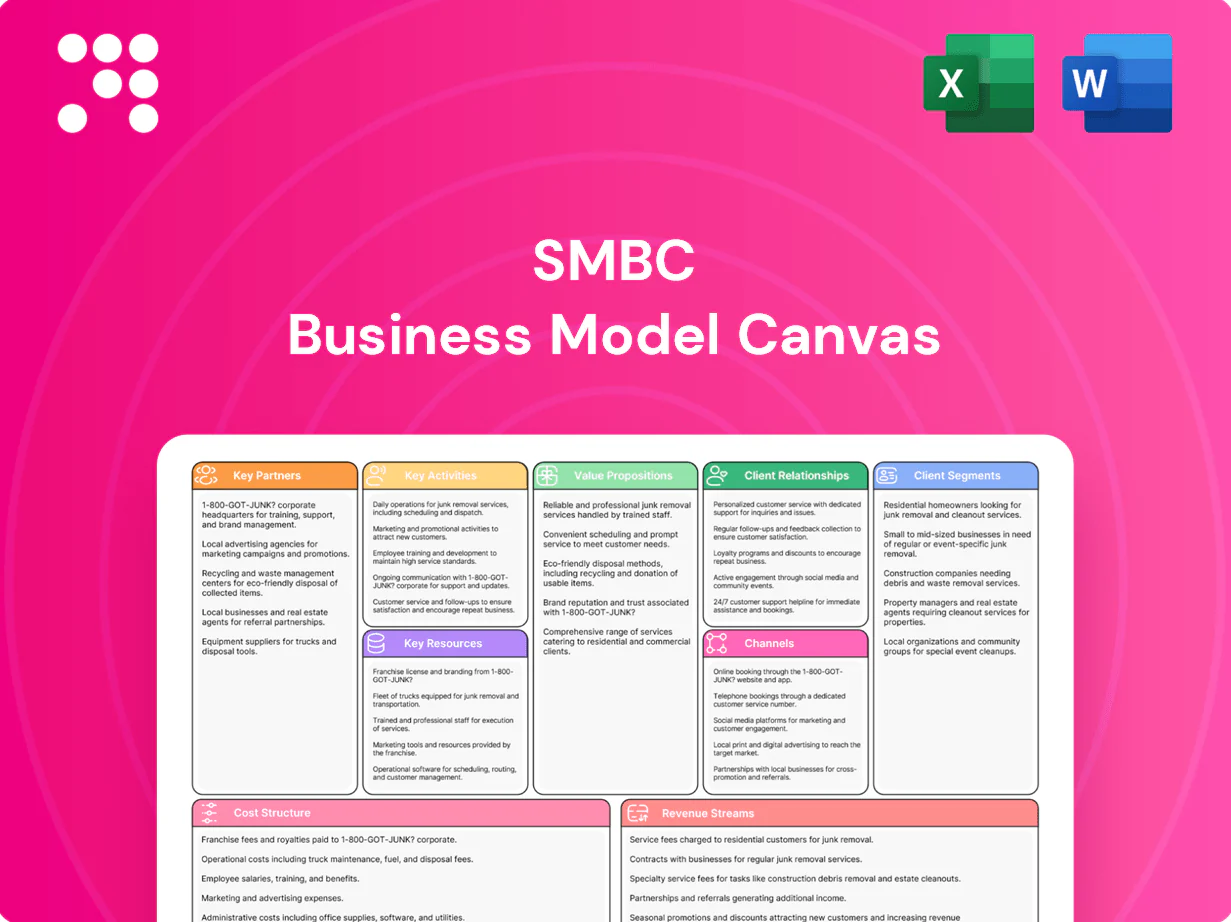

SMBC Business Model Canvas

Unlock the strategic blueprint of a major bank with a concise Business Model Canvas

Unlock the full strategic blueprint behind SMBC’s business model in our comprehensive Business Model Canvas. This concise, actionable report reveals how SMBC creates value, captures market share, and manages risks across all nine blocks. Ideal for investors, consultants, and founders seeking a ready-to-use, downloadable template—purchase the full Canvas to benchmark strategy and drive decisions.

Partnerships

Global correspondent and syndication banks

SMFG partners with global correspondent and syndication banks to enable cross-border payments, trade finance, and syndicated lending, broadening access to markets where it lacks physical presence. These relationships expand balance-sheet capacity and diversify deal flow by co-underwriting transactions and sharing risk. Shared underwriting reduces capital concentration and enhances client coverage through partner networks.

Payments networks and co-brand partners

Alliances with Visa and Mastercard and merchant partners power SMBC card issuance, acceptance and loyalty ecosystems; Visa and Mastercard together accounted for over 80% of global card transactions in 2024. Co-branded programs deepen customer stickiness and enrich behavioral data for targeting. They unlock interchange and fee income (typical interchange ~1–2%) and expand marketing reach. Joint risk and fraud controls raise portfolio quality and lower loss rates.

Fintechs and technology vendors

Cloud, core-banking, API and AI partners accelerate SMBCs digital transformation, with 2024 industry studies showing fintech collaborations can cut onboarding times by up to 60% and reduce IT run costs around 20%. These partnerships improve KYC/AML, lending analytics and CX while vendor ecosystems shorten time-to-market, and support open banking integrations for corporate and retail clients.

Securities, asset management, and brokerage affiliates

Securities and asset-management affiliates within SMFG deliver full-service capital markets and investment solutions, leveraging combined distribution to boost IPOs, DCM/ECM and structured-product placement; SMFG’s consolidated assets exceed JPY 200 trillion, underpinning scale. Asset-gathering drives recurring fee income and cross-sell into banking, while deep research and execution broaden institutional client value.

- Distribution scale: unified IPO/DCM/ECM origination

- Revenue mix: recurring AM fees + brokerage spreads

- Client value: research-led institutional execution

Regulators and industry consortia

Constructive relationships with regulators secure licenses and ensure compliance, enabling SMBC to operate across jurisdictions while reducing approval delays and regulatory costs. Active participation in industry consortia shapes payments, ESG and digital-asset standards, accelerating interoperability and market-infrastructure upgrades. Demonstrable governance credibility lowers systemic and reputational risk, supporting client confidence and capital access.

- Regulatory access: faster licensing, lower compliance friction

- Standards influence: payments, ESG, digital assets

- Infrastructure: interoperability and market upgrades

- Risk reduction: stronger governance, lower systemic/reputational risk

Correspondent reach, card fees and fintech cuts scale assets past JPY 200T

SMFG leverages correspondent and syndication banks to enable cross-border payments and syndicated lending, expanding reach where it lacks branches and lowering capital concentration; SMFG consolidated assets >JPY 200 trillion (2024).

Card partnerships with Visa/Mastercard (≈80% global transactions 2024) drive interchange (~1–2%) and co-branded acquisition, boosting fee income and customer data.

Cloud, API and fintech allies cut onboarding up to 60% and lower IT run costs ~20%, accelerating digital product rollout and KYC/AML improvements.

| Partner Type | Primary Benefit | 2024 Metric |

|---|---|---|

| Correspondent/Syndication | Market access, risk share | Assets >JPY 200T |

What is included in the product

Comprehensive SMBC Business Model Canvas detailing customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with narratives, competitive advantages and linked SWOT for presentations and investor discussions.

Condenses SMBC’s complex corporate banking strategy into an editable one-page canvas for quick review and alignment. Great for boardrooms, team workshops, or client pitches—saves hours of structuring and makes comparison and collaboration effortless.

Activities

Corporate and retail lending

Origination, underwriting and portfolio management across corporates, SMEs and consumers drive core growth, with cross-sell embedded at origination to lift fee income and lifetime value. Pricing and structuring balance risk-return through cyclical adjustments and sector limits. Active monitoring and stress testing sustain asset quality and capital efficiency; SMBC remains Japan's second-largest bank by assets as of 2024.

Treasury and ALM

As of 2024 SMFG centralizes liquidity, funding mix and interest-rate risk management across the group; securities portfolios (roughly ¥20 trillion) and active hedging support NIM stability, stress testing guides CET1 and liquidity buffers (LCR >100%), while diversified wholesale and deposit funding reduce overall funding costs.

Investment banking and markets

Investment banking and markets at SMBC deliver advisory, ECM/DCM and syndicated-loan solutions to support strategic client transactions, underpinning deal flow in 2024 as SMBC Group reported total assets above ¥170 trillion in FY2024. Markets desks offer FX, rates, credit and commodities solutions for corporates and institutions. Risk warehousing and distribution balance client service with capital usage, while research and execution deepen institutional relationships.

Payments and cards operations

Payments and cards operations — issuing, acquiring and settlement — drive SMBC fee income and build transaction data assets that enable risk-based pricing and merchant insights. Robust fraud prevention and chargeback management preserve margins and reduce loss rates. Network routing and cross-border optimization increase acceptance and lower settlement costs while loyalty programs boost retention and cardholder spend.

Risk, compliance, and digital transformation

Credit, market, operational and compliance risk frameworks protect SMBC’s franchise, embedding limits, stress testing and governance into lending and trading activities.

AML/KYC, sanctions screening and conduct controls meet global standards and are continuously updated to address cross-border compliance risks.

In 2024 digital programs modernized core systems and channels while expanded data and AI capabilities improved decisioning and customer personalization.

- Risk frameworks: limits, stress tests, governance

- Compliance: AML/KYC, sanctions, conduct

- Digital 2024: core modernization, omnichannel

- Data & AI: decisioning, personalization

Origination growth, ¥20T & >100% LCR support NIM

Origination, underwriting and portfolio management across corporates, SMEs and consumers drive growth with cross-sell at origination; pricing/structuring and active stress testing preserve asset quality. Group liquidity, ¥20 trillion securities portfolio and hedging support NIM stability; LCR >100% and diversified funding lower costs. Investment banking, markets and payments fuel fees; digital, data and AI enhance decisioning and personalization.

| Metric | 2024 |

|---|---|

| Total assets (SMFG) | Above ¥170 trillion |

| Securities portfolio (SMBC) | ≈ ¥20 trillion |

| LCR | >100% |

| Bank ranking (Japan) | 2nd by assets |

What You See Is What You Get

Business Model Canvas

The SMBC Business Model Canvas shown here is the exact file you’ll receive—no mockups or samples. When you purchase, you’ll get this same complete, editable document ready for presentation and use in Word and Excel formats. What you preview is what you’ll own.

Unlock the strategic blueprint of a major bank with a concise Business Model Canvas

Unlock the full strategic blueprint behind SMBC’s business model in our comprehensive Business Model Canvas. This concise, actionable report reveals how SMBC creates value, captures market share, and manages risks across all nine blocks. Ideal for investors, consultants, and founders seeking a ready-to-use, downloadable template—purchase the full Canvas to benchmark strategy and drive decisions.

Partnerships

Global correspondent and syndication banks

SMFG partners with global correspondent and syndication banks to enable cross-border payments, trade finance, and syndicated lending, broadening access to markets where it lacks physical presence. These relationships expand balance-sheet capacity and diversify deal flow by co-underwriting transactions and sharing risk. Shared underwriting reduces capital concentration and enhances client coverage through partner networks.

Payments networks and co-brand partners

Alliances with Visa and Mastercard and merchant partners power SMBC card issuance, acceptance and loyalty ecosystems; Visa and Mastercard together accounted for over 80% of global card transactions in 2024. Co-branded programs deepen customer stickiness and enrich behavioral data for targeting. They unlock interchange and fee income (typical interchange ~1–2%) and expand marketing reach. Joint risk and fraud controls raise portfolio quality and lower loss rates.

Fintechs and technology vendors

Cloud, core-banking, API and AI partners accelerate SMBCs digital transformation, with 2024 industry studies showing fintech collaborations can cut onboarding times by up to 60% and reduce IT run costs around 20%. These partnerships improve KYC/AML, lending analytics and CX while vendor ecosystems shorten time-to-market, and support open banking integrations for corporate and retail clients.

Securities, asset management, and brokerage affiliates

Securities and asset-management affiliates within SMFG deliver full-service capital markets and investment solutions, leveraging combined distribution to boost IPOs, DCM/ECM and structured-product placement; SMFG’s consolidated assets exceed JPY 200 trillion, underpinning scale. Asset-gathering drives recurring fee income and cross-sell into banking, while deep research and execution broaden institutional client value.

- Distribution scale: unified IPO/DCM/ECM origination

- Revenue mix: recurring AM fees + brokerage spreads

- Client value: research-led institutional execution

Regulators and industry consortia

Constructive relationships with regulators secure licenses and ensure compliance, enabling SMBC to operate across jurisdictions while reducing approval delays and regulatory costs. Active participation in industry consortia shapes payments, ESG and digital-asset standards, accelerating interoperability and market-infrastructure upgrades. Demonstrable governance credibility lowers systemic and reputational risk, supporting client confidence and capital access.

- Regulatory access: faster licensing, lower compliance friction

- Standards influence: payments, ESG, digital assets

- Infrastructure: interoperability and market upgrades

- Risk reduction: stronger governance, lower systemic/reputational risk

Correspondent reach, card fees and fintech cuts scale assets past JPY 200T

SMFG leverages correspondent and syndication banks to enable cross-border payments and syndicated lending, expanding reach where it lacks branches and lowering capital concentration; SMFG consolidated assets >JPY 200 trillion (2024).

Card partnerships with Visa/Mastercard (≈80% global transactions 2024) drive interchange (~1–2%) and co-branded acquisition, boosting fee income and customer data.

Cloud, API and fintech allies cut onboarding up to 60% and lower IT run costs ~20%, accelerating digital product rollout and KYC/AML improvements.

| Partner Type | Primary Benefit | 2024 Metric |

|---|---|---|

| Correspondent/Syndication | Market access, risk share | Assets >JPY 200T |

What is included in the product

Comprehensive SMBC Business Model Canvas detailing customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with narratives, competitive advantages and linked SWOT for presentations and investor discussions.

Condenses SMBC’s complex corporate banking strategy into an editable one-page canvas for quick review and alignment. Great for boardrooms, team workshops, or client pitches—saves hours of structuring and makes comparison and collaboration effortless.

Activities

Corporate and retail lending

Origination, underwriting and portfolio management across corporates, SMEs and consumers drive core growth, with cross-sell embedded at origination to lift fee income and lifetime value. Pricing and structuring balance risk-return through cyclical adjustments and sector limits. Active monitoring and stress testing sustain asset quality and capital efficiency; SMBC remains Japan's second-largest bank by assets as of 2024.

Treasury and ALM

As of 2024 SMFG centralizes liquidity, funding mix and interest-rate risk management across the group; securities portfolios (roughly ¥20 trillion) and active hedging support NIM stability, stress testing guides CET1 and liquidity buffers (LCR >100%), while diversified wholesale and deposit funding reduce overall funding costs.

Investment banking and markets

Investment banking and markets at SMBC deliver advisory, ECM/DCM and syndicated-loan solutions to support strategic client transactions, underpinning deal flow in 2024 as SMBC Group reported total assets above ¥170 trillion in FY2024. Markets desks offer FX, rates, credit and commodities solutions for corporates and institutions. Risk warehousing and distribution balance client service with capital usage, while research and execution deepen institutional relationships.

Payments and cards operations

Payments and cards operations — issuing, acquiring and settlement — drive SMBC fee income and build transaction data assets that enable risk-based pricing and merchant insights. Robust fraud prevention and chargeback management preserve margins and reduce loss rates. Network routing and cross-border optimization increase acceptance and lower settlement costs while loyalty programs boost retention and cardholder spend.

Risk, compliance, and digital transformation

Credit, market, operational and compliance risk frameworks protect SMBC’s franchise, embedding limits, stress testing and governance into lending and trading activities.

AML/KYC, sanctions screening and conduct controls meet global standards and are continuously updated to address cross-border compliance risks.

In 2024 digital programs modernized core systems and channels while expanded data and AI capabilities improved decisioning and customer personalization.

- Risk frameworks: limits, stress tests, governance

- Compliance: AML/KYC, sanctions, conduct

- Digital 2024: core modernization, omnichannel

- Data & AI: decisioning, personalization

Origination growth, ¥20T & >100% LCR support NIM

Origination, underwriting and portfolio management across corporates, SMEs and consumers drive growth with cross-sell at origination; pricing/structuring and active stress testing preserve asset quality. Group liquidity, ¥20 trillion securities portfolio and hedging support NIM stability; LCR >100% and diversified funding lower costs. Investment banking, markets and payments fuel fees; digital, data and AI enhance decisioning and personalization.

| Metric | 2024 |

|---|---|

| Total assets (SMFG) | Above ¥170 trillion |

| Securities portfolio (SMBC) | ≈ ¥20 trillion |

| LCR | >100% |

| Bank ranking (Japan) | 2nd by assets |

What You See Is What You Get

Business Model Canvas

The SMBC Business Model Canvas shown here is the exact file you’ll receive—no mockups or samples. When you purchase, you’ll get this same complete, editable document ready for presentation and use in Word and Excel formats. What you preview is what you’ll own.

Description

Unlock the strategic blueprint of a major bank with a concise Business Model Canvas

Unlock the full strategic blueprint behind SMBC’s business model in our comprehensive Business Model Canvas. This concise, actionable report reveals how SMBC creates value, captures market share, and manages risks across all nine blocks. Ideal for investors, consultants, and founders seeking a ready-to-use, downloadable template—purchase the full Canvas to benchmark strategy and drive decisions.

Partnerships

Global correspondent and syndication banks

SMFG partners with global correspondent and syndication banks to enable cross-border payments, trade finance, and syndicated lending, broadening access to markets where it lacks physical presence. These relationships expand balance-sheet capacity and diversify deal flow by co-underwriting transactions and sharing risk. Shared underwriting reduces capital concentration and enhances client coverage through partner networks.

Payments networks and co-brand partners

Alliances with Visa and Mastercard and merchant partners power SMBC card issuance, acceptance and loyalty ecosystems; Visa and Mastercard together accounted for over 80% of global card transactions in 2024. Co-branded programs deepen customer stickiness and enrich behavioral data for targeting. They unlock interchange and fee income (typical interchange ~1–2%) and expand marketing reach. Joint risk and fraud controls raise portfolio quality and lower loss rates.

Fintechs and technology vendors

Cloud, core-banking, API and AI partners accelerate SMBCs digital transformation, with 2024 industry studies showing fintech collaborations can cut onboarding times by up to 60% and reduce IT run costs around 20%. These partnerships improve KYC/AML, lending analytics and CX while vendor ecosystems shorten time-to-market, and support open banking integrations for corporate and retail clients.

Securities, asset management, and brokerage affiliates

Securities and asset-management affiliates within SMFG deliver full-service capital markets and investment solutions, leveraging combined distribution to boost IPOs, DCM/ECM and structured-product placement; SMFG’s consolidated assets exceed JPY 200 trillion, underpinning scale. Asset-gathering drives recurring fee income and cross-sell into banking, while deep research and execution broaden institutional client value.

- Distribution scale: unified IPO/DCM/ECM origination

- Revenue mix: recurring AM fees + brokerage spreads

- Client value: research-led institutional execution

Regulators and industry consortia

Constructive relationships with regulators secure licenses and ensure compliance, enabling SMBC to operate across jurisdictions while reducing approval delays and regulatory costs. Active participation in industry consortia shapes payments, ESG and digital-asset standards, accelerating interoperability and market-infrastructure upgrades. Demonstrable governance credibility lowers systemic and reputational risk, supporting client confidence and capital access.

- Regulatory access: faster licensing, lower compliance friction

- Standards influence: payments, ESG, digital assets

- Infrastructure: interoperability and market upgrades

- Risk reduction: stronger governance, lower systemic/reputational risk

Correspondent reach, card fees and fintech cuts scale assets past JPY 200T

SMFG leverages correspondent and syndication banks to enable cross-border payments and syndicated lending, expanding reach where it lacks branches and lowering capital concentration; SMFG consolidated assets >JPY 200 trillion (2024).

Card partnerships with Visa/Mastercard (≈80% global transactions 2024) drive interchange (~1–2%) and co-branded acquisition, boosting fee income and customer data.

Cloud, API and fintech allies cut onboarding up to 60% and lower IT run costs ~20%, accelerating digital product rollout and KYC/AML improvements.

| Partner Type | Primary Benefit | 2024 Metric |

|---|---|---|

| Correspondent/Syndication | Market access, risk share | Assets >JPY 200T |

What is included in the product

Comprehensive SMBC Business Model Canvas detailing customer segments, channels, value propositions and revenue streams across the 9 BMC blocks, with narratives, competitive advantages and linked SWOT for presentations and investor discussions.

Condenses SMBC’s complex corporate banking strategy into an editable one-page canvas for quick review and alignment. Great for boardrooms, team workshops, or client pitches—saves hours of structuring and makes comparison and collaboration effortless.

Activities

Corporate and retail lending

Origination, underwriting and portfolio management across corporates, SMEs and consumers drive core growth, with cross-sell embedded at origination to lift fee income and lifetime value. Pricing and structuring balance risk-return through cyclical adjustments and sector limits. Active monitoring and stress testing sustain asset quality and capital efficiency; SMBC remains Japan's second-largest bank by assets as of 2024.

Treasury and ALM

As of 2024 SMFG centralizes liquidity, funding mix and interest-rate risk management across the group; securities portfolios (roughly ¥20 trillion) and active hedging support NIM stability, stress testing guides CET1 and liquidity buffers (LCR >100%), while diversified wholesale and deposit funding reduce overall funding costs.

Investment banking and markets

Investment banking and markets at SMBC deliver advisory, ECM/DCM and syndicated-loan solutions to support strategic client transactions, underpinning deal flow in 2024 as SMBC Group reported total assets above ¥170 trillion in FY2024. Markets desks offer FX, rates, credit and commodities solutions for corporates and institutions. Risk warehousing and distribution balance client service with capital usage, while research and execution deepen institutional relationships.

Payments and cards operations

Payments and cards operations — issuing, acquiring and settlement — drive SMBC fee income and build transaction data assets that enable risk-based pricing and merchant insights. Robust fraud prevention and chargeback management preserve margins and reduce loss rates. Network routing and cross-border optimization increase acceptance and lower settlement costs while loyalty programs boost retention and cardholder spend.

Risk, compliance, and digital transformation

Credit, market, operational and compliance risk frameworks protect SMBC’s franchise, embedding limits, stress testing and governance into lending and trading activities.

AML/KYC, sanctions screening and conduct controls meet global standards and are continuously updated to address cross-border compliance risks.

In 2024 digital programs modernized core systems and channels while expanded data and AI capabilities improved decisioning and customer personalization.

- Risk frameworks: limits, stress tests, governance

- Compliance: AML/KYC, sanctions, conduct

- Digital 2024: core modernization, omnichannel

- Data & AI: decisioning, personalization

Origination growth, ¥20T & >100% LCR support NIM

Origination, underwriting and portfolio management across corporates, SMEs and consumers drive growth with cross-sell at origination; pricing/structuring and active stress testing preserve asset quality. Group liquidity, ¥20 trillion securities portfolio and hedging support NIM stability; LCR >100% and diversified funding lower costs. Investment banking, markets and payments fuel fees; digital, data and AI enhance decisioning and personalization.

| Metric | 2024 |

|---|---|

| Total assets (SMFG) | Above ¥170 trillion |

| Securities portfolio (SMBC) | ≈ ¥20 trillion |

| LCR | >100% |

| Bank ranking (Japan) | 2nd by assets |

What You See Is What You Get

Business Model Canvas

The SMBC Business Model Canvas shown here is the exact file you’ll receive—no mockups or samples. When you purchase, you’ll get this same complete, editable document ready for presentation and use in Word and Excel formats. What you preview is what you’ll own.