Smulders Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Smulders Group faces moderate supplier power and capital-intensive barriers that limit new entrants, while buyer concentration and project-based competition heighten price sensitivity; substitute threats are low but technological shifts pose strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smulders Group’s competitive dynamics and actionable insights in detail.

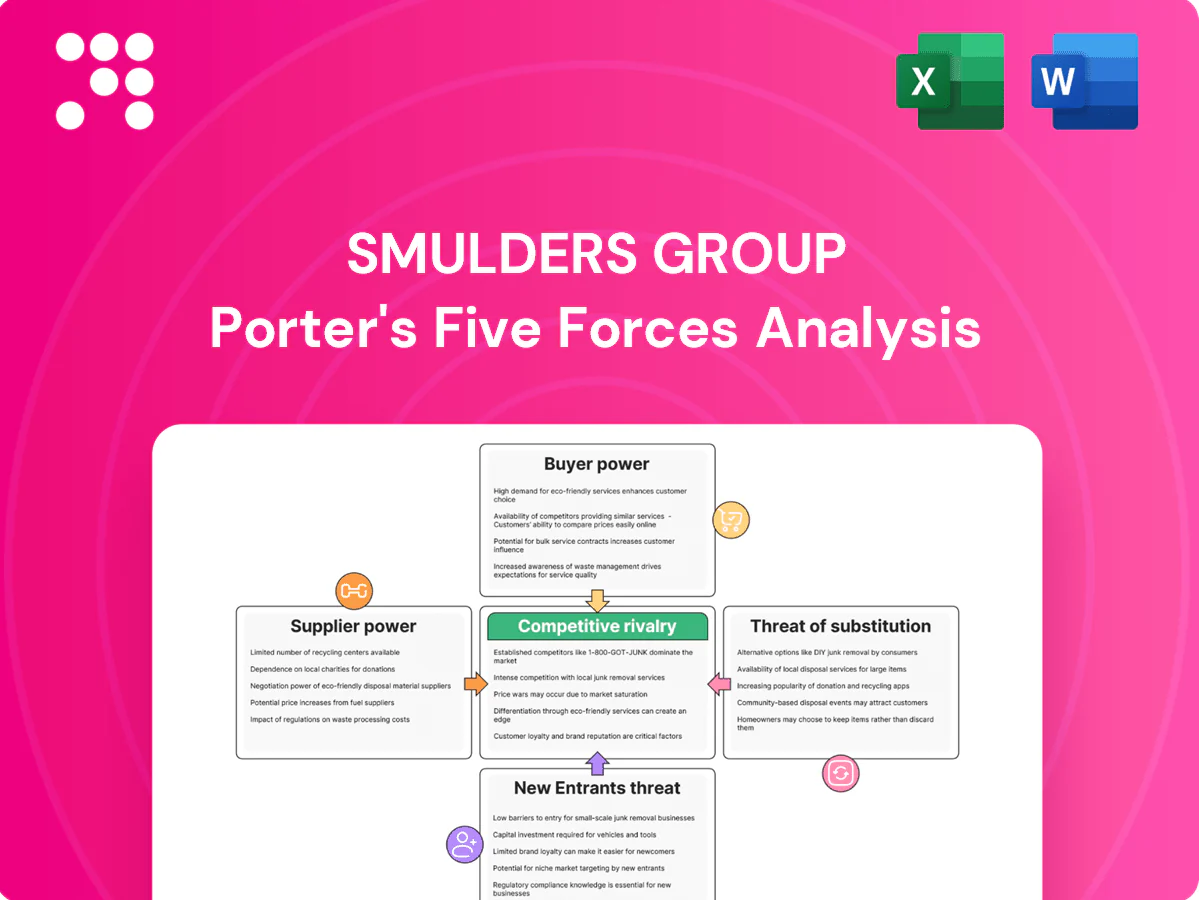

Suppliers Bargaining Power

Concentrated steel plate and forging sources

Offshore-grade heavy plate, flanges and castings are sourced from a narrow set of qualified mills and forges, giving suppliers outsized leverage; in 2024 mill lead times often exceed 30 weeks and allocation tightens during major wind build-outs. Dual-qualification and frame agreements can reduce exposure, but switching suppliers is slow. Smulders’ Eiffage Metal volume helps negotiate better terms yet cannot eliminate cyclical scarcity. Suppliers retain notable bargaining power.

Quality certifications and traceability requirements

In 2024 Smulders' reliance on DNV/ISO/NORSOK specs forces use of certified inputs, narrowing substitution options. Non-conformities trigger documented rework and delay penalties that raise supplier stickiness and add measurable project risk. Rigorous documentation and traceability systems embed suppliers into Smulders' QA processes. These factors increase switching costs and strengthen supplier bargaining positions.

Specialized welding consumables and coatings

Qualified welding wires, fluxes and corrosion coatings for offshore fabrications are niche and tightly audited, with approval gates that limit alternative sourcing.

Vendor changes trigger requalification, procedure updates and trials that commonly take weeks and can materially delay fixed-delivery offshore schedules.

Any supply disruption risks schedule slippage and penalties, while suppliers gain leverage via approval control and typical 12-month warranty obligations.

Heavy-lift logistics and port services

Skilled subcontractors and fabrication capacity

Peak-load welding, NDT and assembly for Smulders depend heavily on accredited subcontractors; in 2024 these specialist crews faced EU day-rate pressure, reported up roughly 15% year-on-year, driven by skilled-trade shortages and tight fabrication capacity. Training and retention investments cut but do not eliminate external reliance, and subcontractors routinely prioritize higher-margin projects, constraining Smulders bargaining leverage.

- Subcontractor dependence: high

- Day-rate rise 2024: ~15%

- Vacancy/shortage: elevated in EU hubs

- Retention reduces but not removes risk

- Supplier prioritization increases pricing pressure

Suppliers tighten: >30 weeks, +15%, +20%

Suppliers hold strong leverage: offshore plate lead-times >30 weeks (2024) and certified inputs narrow alternatives; switching triggers requalification and delays. Specialist crews saw day-rates +15% YoY (2024), raising subcontractor power. Heavy-lift/vessel charter premiums surged ~20% (2024), keeping logistics suppliers influential despite long-term bookings.

| Metric | 2024 |

|---|---|

| Mill lead-time | >30 weeks |

| Welding crew day-rate | +15% YoY |

| Vessel charter premium | ~+20% |

| Warranty | 12 months |

What is included in the product

Tailored Porter's Five Forces analysis for Smulders Group uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic insights to protect market share and profitability.

A clear one-sheet summary of Smulders Group's five competitive forces—ideal for quick strategic decisions; customize pressure levels with updated market or regulatory inputs and export a spider chart or clean layout ready for pitch decks or boardroom slides.

Customers Bargaining Power

Highly concentrated utility and EPC buyers

Offshore wind developers and EPCs are few and large—top players like Ørsted, RWE, Equinor, Iberdrola and Vattenfall dominate global project pipelines—enabling tough negotiations. Framework tenders routinely pit fabricators on price and delivery, while buyers bundle multi-year pipelines (commonly 3–7 years) to extract steeper discounts. This concentration materially heightens buyer power over margins for fabricators like Smulders.

Stringent delivery and LD regimes

Contracts routinely include liquidated damages—market practice in 2024 is ~0.5–1.0% of contract value per week, capped at 5–10%—for delays and quality shortfalls. Schedule adherence is vital to vessel campaigns and grid milestones, where a week’s slip can trigger substantial LDs and knock-on vessel cost overruns. Risk is increasingly shifted to fabricators, raising commercial pressure as buyers actively use LDs to enforce performance and pricing discipline.

Design standardization and should-cost transparency

Repeatable designs and detailed BOMs let buyers benchmark costs across yards, forcing Smulders to defend margins. Commodity steel (Platts HRC ~€850/t in 2024) and freight signals (Baltic Dry Index ~1,200 avg in 2024) feed robust should-cost models. That transparency compresses bid spreads to low single-digit percentages, so value-add must come from productivity gains and risk management rather than opaque pricing.

Transition to larger foundations and floating

Customers demand XXL monopiles and early floating prototypes, forcing suppliers to invest to buyer-driven specs; heavy capex for qualification and specialized tooling erodes suppliers negotiation power. With the EU aiming for 60 GW offshore wind by 2030, buyers can reallocate awards to yards already capable, increasing purchaser leverage.

- Capex exposure weakens suppliers

- Buyer-driven specs raise investment risk

- Capability-ready yards capture awards

ESG and local content requirements

Developers demand local jobs, low-carbon steel and fully audited supply chains, aligning with the EU Fit for 55 target of 55% emissions reduction by 2030; these requirements shrink suppliers and raise input costs. Buyers embed ESG scoring into procurement to extract price, warranty or timeline concessions, and Smulders’ European footprint mitigates but does not remove buyer leverage.

- Local jobs: increases sourcing constraints

- Low-carbon steel: raises material cost and certification needs

- Audited chains: longer lead times, higher compliance spend

- ESG scoring: used to award concessions

Concentrated buyers squeeze fabricator margins; tenders, LDs and capex shift risk to suppliers

Buyers concentrated (Ørsted, RWE, Equinor, Iberdrola, Vattenfall) drive strong price pressure via multi-year tenders and bundling, compressing fabricator margins. Market-standard liquidated damages (~0.5–1.0%/week, capped 5–10%) and detailed BOMs give purchasers leverage; Platts HRC ~€850/t and BDI ~1,200 (2024) enable should-costing. Capex for XXL monopiles and ESG/local sourcing (EU 60 GW by 2030, Fit for 55: 55% by 2030) further shift risk to suppliers.

| Metric | 2024 Value |

|---|---|

| LDs | 0.5–1.0%/wk; cap 5–10% |

| Platts HRC | €850/t |

| BDI avg | ~1,200 |

| EU target | 60 GW offshore by 2030 |

What You See Is What You Get

Smulders Group Porter's Five Forces Analysis

This Smulders Group Porter's Five Forces analysis delivers a concise, professional assessment of competitive pressures, supplier and buyer dynamics, threat of substitutes, and industry rivalry. The document you see is the same professionally written analysis you'll receive—fully formatted and ready to use. No mockups or placeholders, just the final file. Instant download after purchase.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Smulders Group faces moderate supplier power and capital-intensive barriers that limit new entrants, while buyer concentration and project-based competition heighten price sensitivity; substitute threats are low but technological shifts pose strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smulders Group’s competitive dynamics and actionable insights in detail.

Suppliers Bargaining Power

Concentrated steel plate and forging sources

Offshore-grade heavy plate, flanges and castings are sourced from a narrow set of qualified mills and forges, giving suppliers outsized leverage; in 2024 mill lead times often exceed 30 weeks and allocation tightens during major wind build-outs. Dual-qualification and frame agreements can reduce exposure, but switching suppliers is slow. Smulders’ Eiffage Metal volume helps negotiate better terms yet cannot eliminate cyclical scarcity. Suppliers retain notable bargaining power.

Quality certifications and traceability requirements

In 2024 Smulders' reliance on DNV/ISO/NORSOK specs forces use of certified inputs, narrowing substitution options. Non-conformities trigger documented rework and delay penalties that raise supplier stickiness and add measurable project risk. Rigorous documentation and traceability systems embed suppliers into Smulders' QA processes. These factors increase switching costs and strengthen supplier bargaining positions.

Specialized welding consumables and coatings

Qualified welding wires, fluxes and corrosion coatings for offshore fabrications are niche and tightly audited, with approval gates that limit alternative sourcing.

Vendor changes trigger requalification, procedure updates and trials that commonly take weeks and can materially delay fixed-delivery offshore schedules.

Any supply disruption risks schedule slippage and penalties, while suppliers gain leverage via approval control and typical 12-month warranty obligations.

Heavy-lift logistics and port services

Skilled subcontractors and fabrication capacity

Peak-load welding, NDT and assembly for Smulders depend heavily on accredited subcontractors; in 2024 these specialist crews faced EU day-rate pressure, reported up roughly 15% year-on-year, driven by skilled-trade shortages and tight fabrication capacity. Training and retention investments cut but do not eliminate external reliance, and subcontractors routinely prioritize higher-margin projects, constraining Smulders bargaining leverage.

- Subcontractor dependence: high

- Day-rate rise 2024: ~15%

- Vacancy/shortage: elevated in EU hubs

- Retention reduces but not removes risk

- Supplier prioritization increases pricing pressure

Suppliers tighten: >30 weeks, +15%, +20%

Suppliers hold strong leverage: offshore plate lead-times >30 weeks (2024) and certified inputs narrow alternatives; switching triggers requalification and delays. Specialist crews saw day-rates +15% YoY (2024), raising subcontractor power. Heavy-lift/vessel charter premiums surged ~20% (2024), keeping logistics suppliers influential despite long-term bookings.

| Metric | 2024 |

|---|---|

| Mill lead-time | >30 weeks |

| Welding crew day-rate | +15% YoY |

| Vessel charter premium | ~+20% |

| Warranty | 12 months |

What is included in the product

Tailored Porter's Five Forces analysis for Smulders Group uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic insights to protect market share and profitability.

A clear one-sheet summary of Smulders Group's five competitive forces—ideal for quick strategic decisions; customize pressure levels with updated market or regulatory inputs and export a spider chart or clean layout ready for pitch decks or boardroom slides.

Customers Bargaining Power

Highly concentrated utility and EPC buyers

Offshore wind developers and EPCs are few and large—top players like Ørsted, RWE, Equinor, Iberdrola and Vattenfall dominate global project pipelines—enabling tough negotiations. Framework tenders routinely pit fabricators on price and delivery, while buyers bundle multi-year pipelines (commonly 3–7 years) to extract steeper discounts. This concentration materially heightens buyer power over margins for fabricators like Smulders.

Stringent delivery and LD regimes

Contracts routinely include liquidated damages—market practice in 2024 is ~0.5–1.0% of contract value per week, capped at 5–10%—for delays and quality shortfalls. Schedule adherence is vital to vessel campaigns and grid milestones, where a week’s slip can trigger substantial LDs and knock-on vessel cost overruns. Risk is increasingly shifted to fabricators, raising commercial pressure as buyers actively use LDs to enforce performance and pricing discipline.

Design standardization and should-cost transparency

Repeatable designs and detailed BOMs let buyers benchmark costs across yards, forcing Smulders to defend margins. Commodity steel (Platts HRC ~€850/t in 2024) and freight signals (Baltic Dry Index ~1,200 avg in 2024) feed robust should-cost models. That transparency compresses bid spreads to low single-digit percentages, so value-add must come from productivity gains and risk management rather than opaque pricing.

Transition to larger foundations and floating

Customers demand XXL monopiles and early floating prototypes, forcing suppliers to invest to buyer-driven specs; heavy capex for qualification and specialized tooling erodes suppliers negotiation power. With the EU aiming for 60 GW offshore wind by 2030, buyers can reallocate awards to yards already capable, increasing purchaser leverage.

- Capex exposure weakens suppliers

- Buyer-driven specs raise investment risk

- Capability-ready yards capture awards

ESG and local content requirements

Developers demand local jobs, low-carbon steel and fully audited supply chains, aligning with the EU Fit for 55 target of 55% emissions reduction by 2030; these requirements shrink suppliers and raise input costs. Buyers embed ESG scoring into procurement to extract price, warranty or timeline concessions, and Smulders’ European footprint mitigates but does not remove buyer leverage.

- Local jobs: increases sourcing constraints

- Low-carbon steel: raises material cost and certification needs

- Audited chains: longer lead times, higher compliance spend

- ESG scoring: used to award concessions

Concentrated buyers squeeze fabricator margins; tenders, LDs and capex shift risk to suppliers

Buyers concentrated (Ørsted, RWE, Equinor, Iberdrola, Vattenfall) drive strong price pressure via multi-year tenders and bundling, compressing fabricator margins. Market-standard liquidated damages (~0.5–1.0%/week, capped 5–10%) and detailed BOMs give purchasers leverage; Platts HRC ~€850/t and BDI ~1,200 (2024) enable should-costing. Capex for XXL monopiles and ESG/local sourcing (EU 60 GW by 2030, Fit for 55: 55% by 2030) further shift risk to suppliers.

| Metric | 2024 Value |

|---|---|

| LDs | 0.5–1.0%/wk; cap 5–10% |

| Platts HRC | €850/t |

| BDI avg | ~1,200 |

| EU target | 60 GW offshore by 2030 |

What You See Is What You Get

Smulders Group Porter's Five Forces Analysis

This Smulders Group Porter's Five Forces analysis delivers a concise, professional assessment of competitive pressures, supplier and buyer dynamics, threat of substitutes, and industry rivalry. The document you see is the same professionally written analysis you'll receive—fully formatted and ready to use. No mockups or placeholders, just the final file. Instant download after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Smulders Group faces moderate supplier power and capital-intensive barriers that limit new entrants, while buyer concentration and project-based competition heighten price sensitivity; substitute threats are low but technological shifts pose strategic risks. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Smulders Group’s competitive dynamics and actionable insights in detail.

Suppliers Bargaining Power

Concentrated steel plate and forging sources

Offshore-grade heavy plate, flanges and castings are sourced from a narrow set of qualified mills and forges, giving suppliers outsized leverage; in 2024 mill lead times often exceed 30 weeks and allocation tightens during major wind build-outs. Dual-qualification and frame agreements can reduce exposure, but switching suppliers is slow. Smulders’ Eiffage Metal volume helps negotiate better terms yet cannot eliminate cyclical scarcity. Suppliers retain notable bargaining power.

Quality certifications and traceability requirements

In 2024 Smulders' reliance on DNV/ISO/NORSOK specs forces use of certified inputs, narrowing substitution options. Non-conformities trigger documented rework and delay penalties that raise supplier stickiness and add measurable project risk. Rigorous documentation and traceability systems embed suppliers into Smulders' QA processes. These factors increase switching costs and strengthen supplier bargaining positions.

Specialized welding consumables and coatings

Qualified welding wires, fluxes and corrosion coatings for offshore fabrications are niche and tightly audited, with approval gates that limit alternative sourcing.

Vendor changes trigger requalification, procedure updates and trials that commonly take weeks and can materially delay fixed-delivery offshore schedules.

Any supply disruption risks schedule slippage and penalties, while suppliers gain leverage via approval control and typical 12-month warranty obligations.

Heavy-lift logistics and port services

Skilled subcontractors and fabrication capacity

Peak-load welding, NDT and assembly for Smulders depend heavily on accredited subcontractors; in 2024 these specialist crews faced EU day-rate pressure, reported up roughly 15% year-on-year, driven by skilled-trade shortages and tight fabrication capacity. Training and retention investments cut but do not eliminate external reliance, and subcontractors routinely prioritize higher-margin projects, constraining Smulders bargaining leverage.

- Subcontractor dependence: high

- Day-rate rise 2024: ~15%

- Vacancy/shortage: elevated in EU hubs

- Retention reduces but not removes risk

- Supplier prioritization increases pricing pressure

Suppliers tighten: >30 weeks, +15%, +20%

Suppliers hold strong leverage: offshore plate lead-times >30 weeks (2024) and certified inputs narrow alternatives; switching triggers requalification and delays. Specialist crews saw day-rates +15% YoY (2024), raising subcontractor power. Heavy-lift/vessel charter premiums surged ~20% (2024), keeping logistics suppliers influential despite long-term bookings.

| Metric | 2024 |

|---|---|

| Mill lead-time | >30 weeks |

| Welding crew day-rate | +15% YoY |

| Vessel charter premium | ~+20% |

| Warranty | 12 months |

What is included in the product

Tailored Porter's Five Forces analysis for Smulders Group uncovering competitive intensity, buyer/supplier power, entry barriers, substitutes and disruptive threats, with strategic insights to protect market share and profitability.

A clear one-sheet summary of Smulders Group's five competitive forces—ideal for quick strategic decisions; customize pressure levels with updated market or regulatory inputs and export a spider chart or clean layout ready for pitch decks or boardroom slides.

Customers Bargaining Power

Highly concentrated utility and EPC buyers

Offshore wind developers and EPCs are few and large—top players like Ørsted, RWE, Equinor, Iberdrola and Vattenfall dominate global project pipelines—enabling tough negotiations. Framework tenders routinely pit fabricators on price and delivery, while buyers bundle multi-year pipelines (commonly 3–7 years) to extract steeper discounts. This concentration materially heightens buyer power over margins for fabricators like Smulders.

Stringent delivery and LD regimes

Contracts routinely include liquidated damages—market practice in 2024 is ~0.5–1.0% of contract value per week, capped at 5–10%—for delays and quality shortfalls. Schedule adherence is vital to vessel campaigns and grid milestones, where a week’s slip can trigger substantial LDs and knock-on vessel cost overruns. Risk is increasingly shifted to fabricators, raising commercial pressure as buyers actively use LDs to enforce performance and pricing discipline.

Design standardization and should-cost transparency

Repeatable designs and detailed BOMs let buyers benchmark costs across yards, forcing Smulders to defend margins. Commodity steel (Platts HRC ~€850/t in 2024) and freight signals (Baltic Dry Index ~1,200 avg in 2024) feed robust should-cost models. That transparency compresses bid spreads to low single-digit percentages, so value-add must come from productivity gains and risk management rather than opaque pricing.

Transition to larger foundations and floating

Customers demand XXL monopiles and early floating prototypes, forcing suppliers to invest to buyer-driven specs; heavy capex for qualification and specialized tooling erodes suppliers negotiation power. With the EU aiming for 60 GW offshore wind by 2030, buyers can reallocate awards to yards already capable, increasing purchaser leverage.

- Capex exposure weakens suppliers

- Buyer-driven specs raise investment risk

- Capability-ready yards capture awards

ESG and local content requirements

Developers demand local jobs, low-carbon steel and fully audited supply chains, aligning with the EU Fit for 55 target of 55% emissions reduction by 2030; these requirements shrink suppliers and raise input costs. Buyers embed ESG scoring into procurement to extract price, warranty or timeline concessions, and Smulders’ European footprint mitigates but does not remove buyer leverage.

- Local jobs: increases sourcing constraints

- Low-carbon steel: raises material cost and certification needs

- Audited chains: longer lead times, higher compliance spend

- ESG scoring: used to award concessions

Concentrated buyers squeeze fabricator margins; tenders, LDs and capex shift risk to suppliers

Buyers concentrated (Ørsted, RWE, Equinor, Iberdrola, Vattenfall) drive strong price pressure via multi-year tenders and bundling, compressing fabricator margins. Market-standard liquidated damages (~0.5–1.0%/week, capped 5–10%) and detailed BOMs give purchasers leverage; Platts HRC ~€850/t and BDI ~1,200 (2024) enable should-costing. Capex for XXL monopiles and ESG/local sourcing (EU 60 GW by 2030, Fit for 55: 55% by 2030) further shift risk to suppliers.

| Metric | 2024 Value |

|---|---|

| LDs | 0.5–1.0%/wk; cap 5–10% |

| Platts HRC | €850/t |

| BDI avg | ~1,200 |

| EU target | 60 GW offshore by 2030 |

What You See Is What You Get

Smulders Group Porter's Five Forces Analysis

This Smulders Group Porter's Five Forces analysis delivers a concise, professional assessment of competitive pressures, supplier and buyer dynamics, threat of substitutes, and industry rivalry. The document you see is the same professionally written analysis you'll receive—fully formatted and ready to use. No mockups or placeholders, just the final file. Instant download after purchase.