Smulders Group PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Our concise PESTLE for Smulders Group highlights key political, economic, social, technological, legal and environmental forces shaping its offshore and renewable-energy operations. Use these insights to anticipate risks and spot growth opportunities. Purchase the full analysis for in-depth, ready-to-use strategic intelligence.

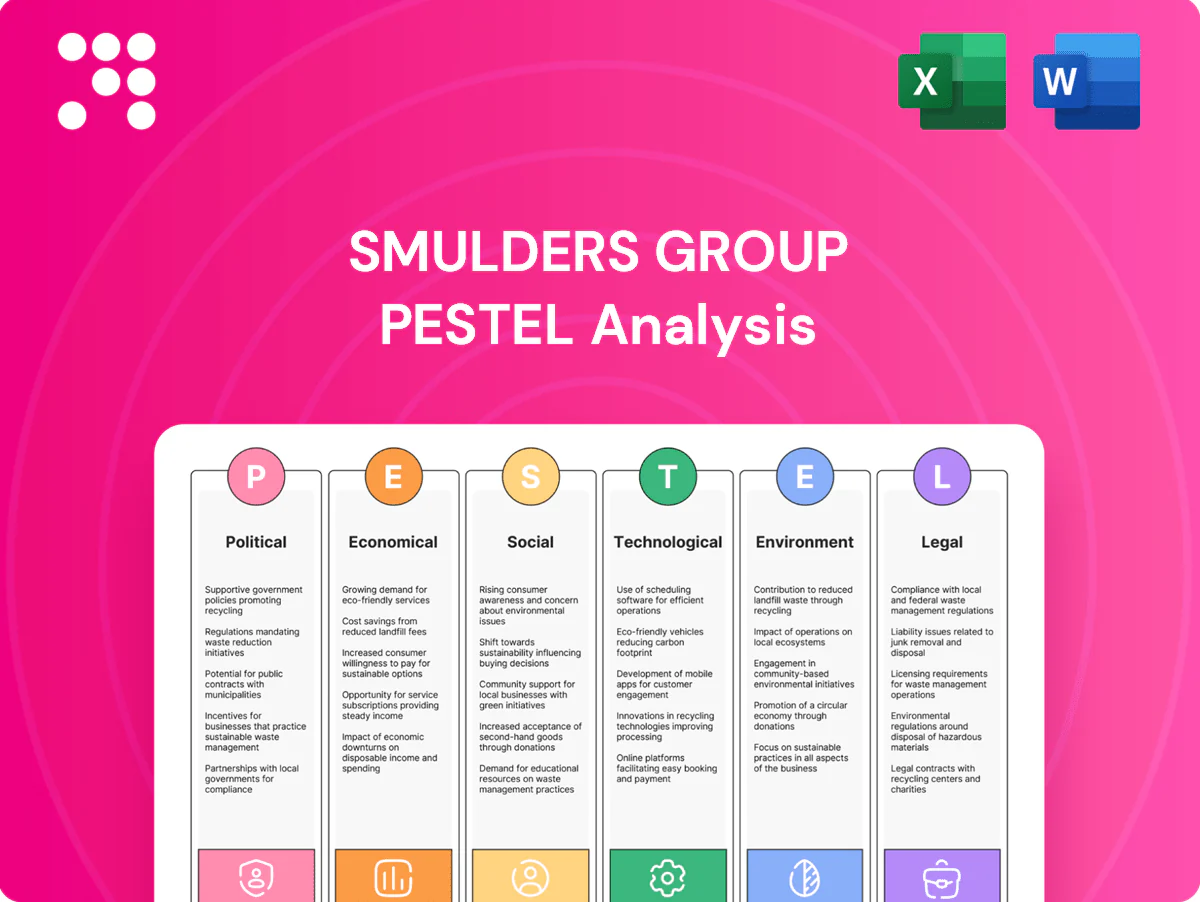

Political factors

EU energy transition policy tailwinds

EU offshore targets of 60 GW by 2030 and 300 GW by 2050, plus the UK 50 GW 2030 goal, create multi‑year pipelines for foundations and substations that underpin Smulders’ orderbook. National industrial policies and local‑content rules steer regional fabrication and siting of Smulders’ capacity. Policy stability de‑risks capex but election cycles can delay auctions; close alignment with Eiffage Metal and trade associations improves anticipation of shifts.

Subsidy and auction design volatility

Volatility in subsidy and auction design, exemplified by shifts in CfD and ORE auction rules, directly alters project FID timing and reduces workload visibility for Smulders Group, with tight strike prices often cancelling or deferring projects and compressing fabricator margins. Indexation mechanisms to inflation and materials costs are critical for steel‑heavy scopes to protect margins. Scenario planning across auction rounds smooths factory utilization and mitigates peak/trough effects.

Geopolitical supply chain risks

Sanctions, trade tensions and Red Sea/Suez disruptions have increased lead times and costs for plate steel, fittings and freight, with roughly 12% of global seaborne trade transiting Suez and war-risk premiums reported to spike up to 400% during 2023–24. Diversifying suppliers and pre-qualifying alternates reduces exposure and can cut single-source dependency by >30% in practice. Government export controls have increasingly constrained oil & gas orders through additional licensing and delays. Political risk insurance (coverage up to ~95% via multilateral insurers) and flexible logistics networks mitigate revenue and delivery shocks.

Port and permitting policy

National investments in marshalling ports and grid connections drive project timing; the EU target of 60 GW offshore wind by 2030 creates urgent port and grid upgrades. WindEurope reports consenting and grid processes can take 4–7 years, causing permitting bottlenecks that cascade into fabrication schedules. Proactive engagement with port authorities secures laydown and heavy-lift windows and reduces idle-time penalties.

- Tag: EU target 60 GW by 2030

- Tag: Consenting 4–7 years (WindEurope)

- Tag: Port engagement reduces idle-time/penalties

Defense and industrial policy spillovers

- Steel capacity redeployment

- Skilled labor competition

- Procurement favoring domestic firms

- Eiffage partnership aids compliance

- Site allocation supports strategic wins

EU 60 GW & UK 50 GW: factory use hit by ports & grid

EU 60 GW/2030 and UK 50 GW/2030 underpin multi‑year pipelines; national local‑content rules steer fabrication and siting. Auction/subsidy volatility and weak indexation shift FID timing and compress margins, so scenario planning smooths factory use. Trade disruptions, port/grid bottlenecks and defense spillovers reallocate steel/labor; Eiffage partnership and political risk insurance mitigate exposure.

| Metric | Value |

|---|---|

| EU target 2030 | 60 GW |

| UK target 2030 | 50 GW |

| Suez trade | ~12% |

| Military spend (SIPRI 2023) | $2.24T |

| Eiffage revenue 2023 | €20.4B |

What is included in the product

Provides a concise PESTLE review of how political, economic, social, technological, environmental and legal forces specifically impact Smulders Group, with data-backed trends and industry-region relevance to identify risks and opportunities; designed for executives, investors and strategists with forward-looking insights for scenario planning and funding support.

A concise, visually segmented PESTLE summary for Smulders Group that can be dropped into presentations, edited with notes by region or business line, and easily shared across teams to streamline external risk discussion and accelerate strategic planning.

Economic factors

Steel and input cost volatility

Plates, sections and protective coatings are core input drivers for Smulders, and sharp price swings erode margins on fixed-price EPC contracts; Smulders mitigates this through hedging, long-term framework agreements and pass-through clauses that preserve project economics. Rising industrial energy costs increase fabrication overheads, while continuous should-costing and tighter supplier collaboration improve bid accuracy and margin resilience.

Interest rates and project financing

Higher interest rates pushed developer WACC and delayed FIDs, with European project-finance all-in costs rising to about 6–8% in 2024–2025, forcing scope resizing. Fabricators like Smulders face higher working-capital costs as 3-month EURIBOR near 3.6% raises carrying costs for long-lead inventory. Milestone payment structures and advance payments reduce cash strain, but counterparty risk and DFIs' stricter lending increase when financing tightens.

Currency exposure

Multi-country projects generate EUR/GBP/NOK/USD revenue-cost mismatches that can compress margins across Smulders operations. Natural hedges and FX forwards are used to stabilize margins and cash flow. Pricing contracts in the client currency with indexation further reduces exposure. Eiffage group treasury coordination centralizes hedging and optimizes coverage; 2024 average EUR/USD was about 1.09.

Cyclical demand across end-markets

Offshore wind growth is reducing oil & gas cyclicality in Smulders’ order book, supported by the EU target of 60 GW offshore by 2030 which underpins near-term demand; diversification into bridges and industrial steel balances utilisation, while capacity planning avoids peak-bust hiring and modular production enables rapid product mix shifts.

- Offshore: EU 60 GW by 2030

- Diversification: bridges & industrial steel

- Operations: modular production, steady capacity planning

Competition and consolidation

European yards face intense competition from Asian fabricators and new entrants as the EU pushes for 60 GW offshore wind by 2030, raising demand for XXL monopiles and jackets where scale, QA and track record are decisive. Joint-venture models increasingly spread capex and risk on mega-projects, while sector consolidation could improve pricing discipline and margin stability.

- Competition: Asian yards gaining share

- Differentiators: scale, QA, track record

- JV: spreads capex/risk on mega-projects

- Consolidation: supports pricing discipline

EU 60 GW & UK 50 GW: factory use hit by ports & grid

Input-price volatility (steel, coatings) and rising industrial energy pushed fabrication costs up in 2024–25; hedging, pass-throughs and supplier frameworks protect margins. Project finance all-in costs ~6–8% and 3M EURIBOR ~3.6% raise WACC and working-capital costs, slowing FIDs. FX (EUR/USD ~1.09 in 2024) and multi-currency contracts require hedging; EU offshore target 60 GW by 2030 sustains demand.

| Metric | 2024–25 |

|---|---|

| Project finance all-in | 6–8% |

| 3M EURIBOR | ~3.6% |

| EUR/USD avg | ~1.09 |

| EU offshore target | 60 GW by 2030 |

Full Version Awaits

Smulders Group PESTLE Analysis

The preview shown here is the exact Smulders Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers: the content, structure and layout are identical to the downloadable file. You’ll get this final document immediately after checkout.

Your Shortcut to Market Insight Starts Here

Our concise PESTLE for Smulders Group highlights key political, economic, social, technological, legal and environmental forces shaping its offshore and renewable-energy operations. Use these insights to anticipate risks and spot growth opportunities. Purchase the full analysis for in-depth, ready-to-use strategic intelligence.

Political factors

EU energy transition policy tailwinds

EU offshore targets of 60 GW by 2030 and 300 GW by 2050, plus the UK 50 GW 2030 goal, create multi‑year pipelines for foundations and substations that underpin Smulders’ orderbook. National industrial policies and local‑content rules steer regional fabrication and siting of Smulders’ capacity. Policy stability de‑risks capex but election cycles can delay auctions; close alignment with Eiffage Metal and trade associations improves anticipation of shifts.

Subsidy and auction design volatility

Volatility in subsidy and auction design, exemplified by shifts in CfD and ORE auction rules, directly alters project FID timing and reduces workload visibility for Smulders Group, with tight strike prices often cancelling or deferring projects and compressing fabricator margins. Indexation mechanisms to inflation and materials costs are critical for steel‑heavy scopes to protect margins. Scenario planning across auction rounds smooths factory utilization and mitigates peak/trough effects.

Geopolitical supply chain risks

Sanctions, trade tensions and Red Sea/Suez disruptions have increased lead times and costs for plate steel, fittings and freight, with roughly 12% of global seaborne trade transiting Suez and war-risk premiums reported to spike up to 400% during 2023–24. Diversifying suppliers and pre-qualifying alternates reduces exposure and can cut single-source dependency by >30% in practice. Government export controls have increasingly constrained oil & gas orders through additional licensing and delays. Political risk insurance (coverage up to ~95% via multilateral insurers) and flexible logistics networks mitigate revenue and delivery shocks.

Port and permitting policy

National investments in marshalling ports and grid connections drive project timing; the EU target of 60 GW offshore wind by 2030 creates urgent port and grid upgrades. WindEurope reports consenting and grid processes can take 4–7 years, causing permitting bottlenecks that cascade into fabrication schedules. Proactive engagement with port authorities secures laydown and heavy-lift windows and reduces idle-time penalties.

- Tag: EU target 60 GW by 2030

- Tag: Consenting 4–7 years (WindEurope)

- Tag: Port engagement reduces idle-time/penalties

Defense and industrial policy spillovers

- Steel capacity redeployment

- Skilled labor competition

- Procurement favoring domestic firms

- Eiffage partnership aids compliance

- Site allocation supports strategic wins

EU 60 GW & UK 50 GW: factory use hit by ports & grid

EU 60 GW/2030 and UK 50 GW/2030 underpin multi‑year pipelines; national local‑content rules steer fabrication and siting. Auction/subsidy volatility and weak indexation shift FID timing and compress margins, so scenario planning smooths factory use. Trade disruptions, port/grid bottlenecks and defense spillovers reallocate steel/labor; Eiffage partnership and political risk insurance mitigate exposure.

| Metric | Value |

|---|---|

| EU target 2030 | 60 GW |

| UK target 2030 | 50 GW |

| Suez trade | ~12% |

| Military spend (SIPRI 2023) | $2.24T |

| Eiffage revenue 2023 | €20.4B |

What is included in the product

Provides a concise PESTLE review of how political, economic, social, technological, environmental and legal forces specifically impact Smulders Group, with data-backed trends and industry-region relevance to identify risks and opportunities; designed for executives, investors and strategists with forward-looking insights for scenario planning and funding support.

A concise, visually segmented PESTLE summary for Smulders Group that can be dropped into presentations, edited with notes by region or business line, and easily shared across teams to streamline external risk discussion and accelerate strategic planning.

Economic factors

Steel and input cost volatility

Plates, sections and protective coatings are core input drivers for Smulders, and sharp price swings erode margins on fixed-price EPC contracts; Smulders mitigates this through hedging, long-term framework agreements and pass-through clauses that preserve project economics. Rising industrial energy costs increase fabrication overheads, while continuous should-costing and tighter supplier collaboration improve bid accuracy and margin resilience.

Interest rates and project financing

Higher interest rates pushed developer WACC and delayed FIDs, with European project-finance all-in costs rising to about 6–8% in 2024–2025, forcing scope resizing. Fabricators like Smulders face higher working-capital costs as 3-month EURIBOR near 3.6% raises carrying costs for long-lead inventory. Milestone payment structures and advance payments reduce cash strain, but counterparty risk and DFIs' stricter lending increase when financing tightens.

Currency exposure

Multi-country projects generate EUR/GBP/NOK/USD revenue-cost mismatches that can compress margins across Smulders operations. Natural hedges and FX forwards are used to stabilize margins and cash flow. Pricing contracts in the client currency with indexation further reduces exposure. Eiffage group treasury coordination centralizes hedging and optimizes coverage; 2024 average EUR/USD was about 1.09.

Cyclical demand across end-markets

Offshore wind growth is reducing oil & gas cyclicality in Smulders’ order book, supported by the EU target of 60 GW offshore by 2030 which underpins near-term demand; diversification into bridges and industrial steel balances utilisation, while capacity planning avoids peak-bust hiring and modular production enables rapid product mix shifts.

- Offshore: EU 60 GW by 2030

- Diversification: bridges & industrial steel

- Operations: modular production, steady capacity planning

Competition and consolidation

European yards face intense competition from Asian fabricators and new entrants as the EU pushes for 60 GW offshore wind by 2030, raising demand for XXL monopiles and jackets where scale, QA and track record are decisive. Joint-venture models increasingly spread capex and risk on mega-projects, while sector consolidation could improve pricing discipline and margin stability.

- Competition: Asian yards gaining share

- Differentiators: scale, QA, track record

- JV: spreads capex/risk on mega-projects

- Consolidation: supports pricing discipline

EU 60 GW & UK 50 GW: factory use hit by ports & grid

Input-price volatility (steel, coatings) and rising industrial energy pushed fabrication costs up in 2024–25; hedging, pass-throughs and supplier frameworks protect margins. Project finance all-in costs ~6–8% and 3M EURIBOR ~3.6% raise WACC and working-capital costs, slowing FIDs. FX (EUR/USD ~1.09 in 2024) and multi-currency contracts require hedging; EU offshore target 60 GW by 2030 sustains demand.

| Metric | 2024–25 |

|---|---|

| Project finance all-in | 6–8% |

| 3M EURIBOR | ~3.6% |

| EUR/USD avg | ~1.09 |

| EU offshore target | 60 GW by 2030 |

Full Version Awaits

Smulders Group PESTLE Analysis

The preview shown here is the exact Smulders Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers: the content, structure and layout are identical to the downloadable file. You’ll get this final document immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Our concise PESTLE for Smulders Group highlights key political, economic, social, technological, legal and environmental forces shaping its offshore and renewable-energy operations. Use these insights to anticipate risks and spot growth opportunities. Purchase the full analysis for in-depth, ready-to-use strategic intelligence.

Political factors

EU energy transition policy tailwinds

EU offshore targets of 60 GW by 2030 and 300 GW by 2050, plus the UK 50 GW 2030 goal, create multi‑year pipelines for foundations and substations that underpin Smulders’ orderbook. National industrial policies and local‑content rules steer regional fabrication and siting of Smulders’ capacity. Policy stability de‑risks capex but election cycles can delay auctions; close alignment with Eiffage Metal and trade associations improves anticipation of shifts.

Subsidy and auction design volatility

Volatility in subsidy and auction design, exemplified by shifts in CfD and ORE auction rules, directly alters project FID timing and reduces workload visibility for Smulders Group, with tight strike prices often cancelling or deferring projects and compressing fabricator margins. Indexation mechanisms to inflation and materials costs are critical for steel‑heavy scopes to protect margins. Scenario planning across auction rounds smooths factory utilization and mitigates peak/trough effects.

Geopolitical supply chain risks

Sanctions, trade tensions and Red Sea/Suez disruptions have increased lead times and costs for plate steel, fittings and freight, with roughly 12% of global seaborne trade transiting Suez and war-risk premiums reported to spike up to 400% during 2023–24. Diversifying suppliers and pre-qualifying alternates reduces exposure and can cut single-source dependency by >30% in practice. Government export controls have increasingly constrained oil & gas orders through additional licensing and delays. Political risk insurance (coverage up to ~95% via multilateral insurers) and flexible logistics networks mitigate revenue and delivery shocks.

Port and permitting policy

National investments in marshalling ports and grid connections drive project timing; the EU target of 60 GW offshore wind by 2030 creates urgent port and grid upgrades. WindEurope reports consenting and grid processes can take 4–7 years, causing permitting bottlenecks that cascade into fabrication schedules. Proactive engagement with port authorities secures laydown and heavy-lift windows and reduces idle-time penalties.

- Tag: EU target 60 GW by 2030

- Tag: Consenting 4–7 years (WindEurope)

- Tag: Port engagement reduces idle-time/penalties

Defense and industrial policy spillovers

- Steel capacity redeployment

- Skilled labor competition

- Procurement favoring domestic firms

- Eiffage partnership aids compliance

- Site allocation supports strategic wins

EU 60 GW & UK 50 GW: factory use hit by ports & grid

EU 60 GW/2030 and UK 50 GW/2030 underpin multi‑year pipelines; national local‑content rules steer fabrication and siting. Auction/subsidy volatility and weak indexation shift FID timing and compress margins, so scenario planning smooths factory use. Trade disruptions, port/grid bottlenecks and defense spillovers reallocate steel/labor; Eiffage partnership and political risk insurance mitigate exposure.

| Metric | Value |

|---|---|

| EU target 2030 | 60 GW |

| UK target 2030 | 50 GW |

| Suez trade | ~12% |

| Military spend (SIPRI 2023) | $2.24T |

| Eiffage revenue 2023 | €20.4B |

What is included in the product

Provides a concise PESTLE review of how political, economic, social, technological, environmental and legal forces specifically impact Smulders Group, with data-backed trends and industry-region relevance to identify risks and opportunities; designed for executives, investors and strategists with forward-looking insights for scenario planning and funding support.

A concise, visually segmented PESTLE summary for Smulders Group that can be dropped into presentations, edited with notes by region or business line, and easily shared across teams to streamline external risk discussion and accelerate strategic planning.

Economic factors

Steel and input cost volatility

Plates, sections and protective coatings are core input drivers for Smulders, and sharp price swings erode margins on fixed-price EPC contracts; Smulders mitigates this through hedging, long-term framework agreements and pass-through clauses that preserve project economics. Rising industrial energy costs increase fabrication overheads, while continuous should-costing and tighter supplier collaboration improve bid accuracy and margin resilience.

Interest rates and project financing

Higher interest rates pushed developer WACC and delayed FIDs, with European project-finance all-in costs rising to about 6–8% in 2024–2025, forcing scope resizing. Fabricators like Smulders face higher working-capital costs as 3-month EURIBOR near 3.6% raises carrying costs for long-lead inventory. Milestone payment structures and advance payments reduce cash strain, but counterparty risk and DFIs' stricter lending increase when financing tightens.

Currency exposure

Multi-country projects generate EUR/GBP/NOK/USD revenue-cost mismatches that can compress margins across Smulders operations. Natural hedges and FX forwards are used to stabilize margins and cash flow. Pricing contracts in the client currency with indexation further reduces exposure. Eiffage group treasury coordination centralizes hedging and optimizes coverage; 2024 average EUR/USD was about 1.09.

Cyclical demand across end-markets

Offshore wind growth is reducing oil & gas cyclicality in Smulders’ order book, supported by the EU target of 60 GW offshore by 2030 which underpins near-term demand; diversification into bridges and industrial steel balances utilisation, while capacity planning avoids peak-bust hiring and modular production enables rapid product mix shifts.

- Offshore: EU 60 GW by 2030

- Diversification: bridges & industrial steel

- Operations: modular production, steady capacity planning

Competition and consolidation

European yards face intense competition from Asian fabricators and new entrants as the EU pushes for 60 GW offshore wind by 2030, raising demand for XXL monopiles and jackets where scale, QA and track record are decisive. Joint-venture models increasingly spread capex and risk on mega-projects, while sector consolidation could improve pricing discipline and margin stability.

- Competition: Asian yards gaining share

- Differentiators: scale, QA, track record

- JV: spreads capex/risk on mega-projects

- Consolidation: supports pricing discipline

EU 60 GW & UK 50 GW: factory use hit by ports & grid

Input-price volatility (steel, coatings) and rising industrial energy pushed fabrication costs up in 2024–25; hedging, pass-throughs and supplier frameworks protect margins. Project finance all-in costs ~6–8% and 3M EURIBOR ~3.6% raise WACC and working-capital costs, slowing FIDs. FX (EUR/USD ~1.09 in 2024) and multi-currency contracts require hedging; EU offshore target 60 GW by 2030 sustains demand.

| Metric | 2024–25 |

|---|---|

| Project finance all-in | 6–8% |

| 3M EURIBOR | ~3.6% |

| EUR/USD avg | ~1.09 |

| EU offshore target | 60 GW by 2030 |

Full Version Awaits

Smulders Group PESTLE Analysis

The preview shown here is the exact Smulders Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the full political, economic, social, technological, legal and environmental assessment as displayed. No placeholders or teasers: the content, structure and layout are identical to the downloadable file. You’ll get this final document immediately after checkout.