SNAAM Group SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

SNAAM Group’s strategic foothold, operational strengths, and sector-specific risks are only partially revealed here—our full SWOT unpacks competitive advantages, emergent threats, and growth levers with data-driven analysis. Purchase the complete SWOT to receive a professionally written, editable report plus an Excel matrix for planning, pitching, or investing with confidence. Unlock the full picture and act faster.

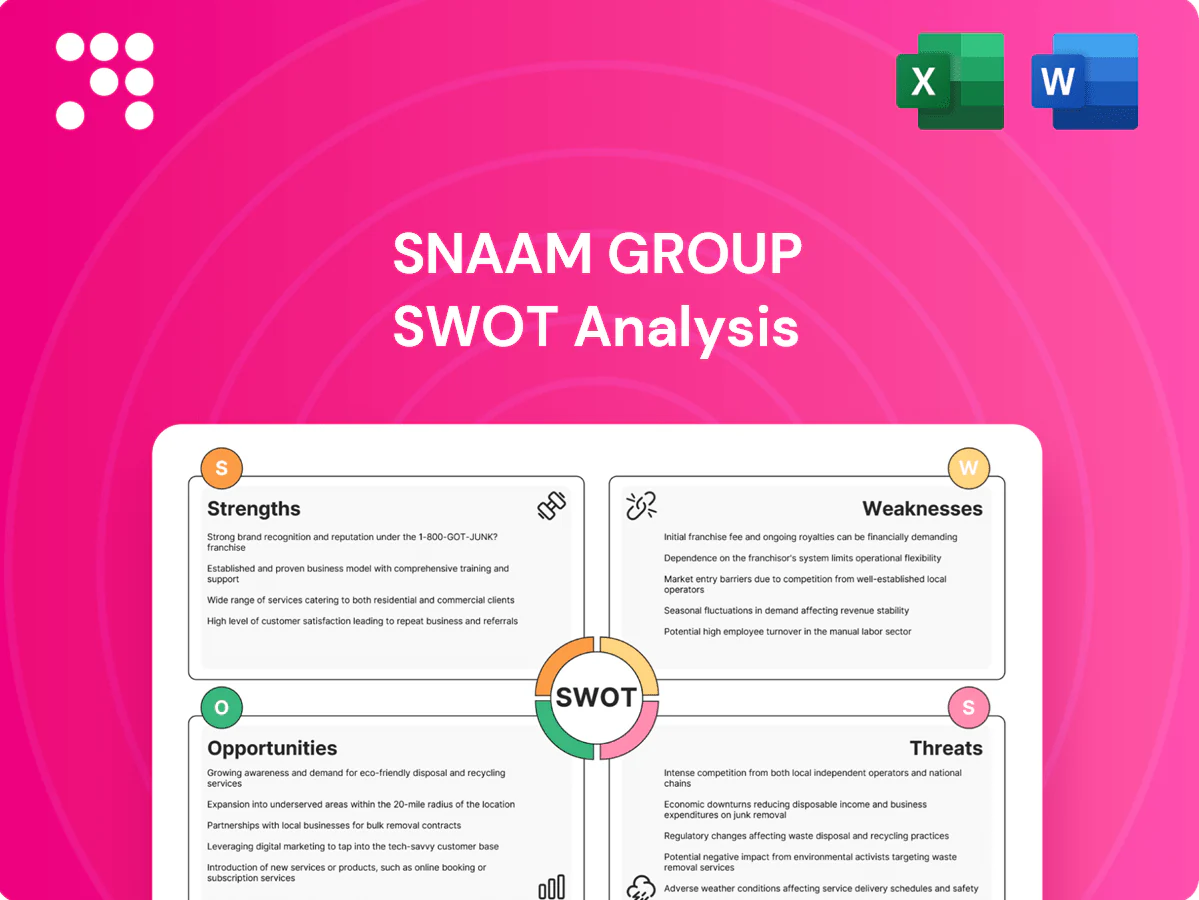

Strengths

Integrated design-to-install capability

End-to-end ownership from engineering to commissioning reduces handoffs and errors, cutting rework that industry studies estimate at 5–10% of project value. It enables faster project cycles and tighter quality control within a global HVAC/filtration market ~USD 240 billion (2023), while clients prefer a single accountable partner for complex deployments and faster, consistent warranty service.

Sector expertise in regulated industries

SNAAM Group's deep experience in food, pharma and manufacturing matches strict GMP/HACCP needs, supporting tailored cleanroom and contamination-control solutions; the global cleanroom market, valued at about USD 4.2 billion in 2023 with ~6% CAGR, underlines demand. Proven familiarity with validation, documentation and audits reduces compliance risk and sales friction, enabling premium pricing and higher contract margins.

Diverse product portfolio

Diverse portfolio—dust collectors, filtration units, and custom systems—expands addressable use cases across manufacturing, mining, and power, supporting resilience as the industrial dust collector market targets about 6% CAGR to 2030. Cross-selling and modular upgrades boost customer lifetime value and aftermarket revenue. Standardized cores with configurable options balance cost and customization, cushioning demand swings across segments.

Focus on air quality and safety outcomes

SNAAM Group ties a clear value proposition to worker health, productivity and regulatory compliance, framing air quality as an operational KPI rather than just equipment. Measured KPIs such as HEPA filter capture efficiency (99.97% at 0.3 μm) and PM2.5 reduction targets aligned with WHO 2021 guideline (5 μg/m3) support robust ROI and EHS case-making. Safety-first messaging directly resonates with EHS and operations leaders and differentiates outcome-focused solutions from commodity hardware vendors.

- Value: worker health → productivity, compliance

- KPIs: HEPA 99.97% capture; PM2.5 target 5 μg/m3

- Audience: EHS & operations alignment

- Edge: outcome-driven vs commodity hardware

Field service and lifecycle support

Installation, maintenance and scheduled filter replacement create steady, recurring revenue streams; the field service management market is growing at roughly a 10% CAGR through 2030, underpinning long-term service monetization. Ongoing performance monitoring and tune-ups sustain system efficiency and reduce churn, while close service relationships boost retention and referrals. Service feedback loops directly inform product improvements and lower R&D cycles.

- Recurring revenue from installs/filters

- 10% CAGR FSM market to 2030

- Monitoring sustains efficiency

- Service drives retention/referrals

- Feedback accelerates product improvement

End-to-end HVAC filtration cuts rework 5-10% and targets USD 240bn market

End-to-end ownership reduces rework (industry 5–10% of project value) and accelerates cycles in a ~USD 240bn HVAC/filtration market (2023). Cleanroom expertise targets USD 4.2bn market (2023, ~6% CAGR), enabling premium margins via compliance. Recurring service (filters/installation) taps FSM market ~10% CAGR to 2030, supporting steady aftermarket revenue.

| Metric | Value |

|---|---|

| HVAC/filtration market | ~USD 240bn (2023) |

| Cleanroom market | USD 4.2bn (2023), ~6% CAGR |

| HEPA efficiency | 99.97% @ 0.3 μm |

| FSM CAGR | ~10% to 2030 |

| Typical rework | 5–10% project value |

What is included in the product

Provides a concise SWOT overview of SNAAM Group, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic positioning, growth priorities, and risk mitigation.

Provides a concise SNAAM Group SWOT matrix for fast, visual strategy alignment across business units, enabling leaders to spot strategic gaps quickly. Ideal for executives and teams needing a compact, decision-ready overview to prioritize initiatives and communicate priorities efficiently.

Weaknesses

Customization-heavy delivery model

Engineering-heavy, customization-first delivery compresses margins (custom project gross margins often 10–18% vs 20–35% for standardized SKUs), extends lead times by 30–60%, and raises working-capital needs by 20–40% due to bespoke components; scope creep without strict project controls is common, and scalability lags behind standardized manufacturing.

Exposure to capex cycles

Industrial customers commonly defer ventilation upgrades in downturns, causing project revenue to become lumpy and quarterly bookings to swing, with cashflow timing tied to milestone billing that typically creates 30–90 day receivable lags. Budget freezes in pharma and food plants often pause awards, compressing forecast accuracy and increasing working capital strain. Such capex sensitivity can drive pronounced volatility in order intake and margin visibility.

Potential geographic concentration

Limited geographic footprint heightens dependency on local demand and networks, concentrating revenue risk in core regions.

Expanding beyond these areas raises logistics and on-site commissioning costs, eroding margins on distant projects.

Service response times often lag in remote markets, while market entry faces certification and vendor-approval delays that slow scaling.

Aftermarket dependency on consumables

Aftermarket dependence on consumables exposes SNAAM to price erosion as generics and private-label entrants — which captured about 25% of filter sales in 2024 — push prices down; survey data in 2024 shows 62% of buyers dual-source consumables to reduce cost. Managing inventory across dozens of sizes and media increases working capital and SKU complexity, and client use of subpar consumables can degrade perceived system performance.

Brand visibility versus global incumbents

SNAAM Group's brand visibility lags versus global incumbents that dominate engineered air solutions, where 2024 procurement surveys report over 60% of complex tenders shortlist legacy vendors with global references. Bid lists and client RFPs often favor suppliers with multiregional case studies, and winning such contracts demands extensive credentials and certifications. Marketing spend and channel reach are constrained versus multinational peers, limiting lead generation.

- Low brand awareness vs global incumbents

- >60% of tenders shortlist legacy vendors (2024 surveys)

- High credential threshold for complex wins

- Limited marketing spend and channel reach

Engineering-first customization cuts margins to 10-18%, extends lead times

Engineering-first, customization-led delivery compresses project gross margins (10–18% vs 20–35% for standardized SKUs), lengthens lead times 30–60% and raises working capital; demand is lumpy with 30–90 day receivable lags and capex sensitivity. Aftermarket faces 25% generics (2024) and 62% dual-sourcing; brand shortlisting remains >60% for legacy global vendors (2024).

| Metric | Value |

|---|---|

| Custom project GM | 10–18% |

| Standard SKU GM | 20–35% |

| Receivable lag | 30–90 days |

| Generics share (2024) | 25% |

| Dual-source buyers (2024) | 62% |

| Tenders shortlist legacy (2024) | >60% |

Same Document Delivered

SNAAM Group SWOT Analysis

This is the actual SNAAM Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy now to unlock the complete, editable version with in-depth insights.

Go Beyond the Preview—Access the Full Strategic Report

SNAAM Group’s strategic foothold, operational strengths, and sector-specific risks are only partially revealed here—our full SWOT unpacks competitive advantages, emergent threats, and growth levers with data-driven analysis. Purchase the complete SWOT to receive a professionally written, editable report plus an Excel matrix for planning, pitching, or investing with confidence. Unlock the full picture and act faster.

Strengths

Integrated design-to-install capability

End-to-end ownership from engineering to commissioning reduces handoffs and errors, cutting rework that industry studies estimate at 5–10% of project value. It enables faster project cycles and tighter quality control within a global HVAC/filtration market ~USD 240 billion (2023), while clients prefer a single accountable partner for complex deployments and faster, consistent warranty service.

Sector expertise in regulated industries

SNAAM Group's deep experience in food, pharma and manufacturing matches strict GMP/HACCP needs, supporting tailored cleanroom and contamination-control solutions; the global cleanroom market, valued at about USD 4.2 billion in 2023 with ~6% CAGR, underlines demand. Proven familiarity with validation, documentation and audits reduces compliance risk and sales friction, enabling premium pricing and higher contract margins.

Diverse product portfolio

Diverse portfolio—dust collectors, filtration units, and custom systems—expands addressable use cases across manufacturing, mining, and power, supporting resilience as the industrial dust collector market targets about 6% CAGR to 2030. Cross-selling and modular upgrades boost customer lifetime value and aftermarket revenue. Standardized cores with configurable options balance cost and customization, cushioning demand swings across segments.

Focus on air quality and safety outcomes

SNAAM Group ties a clear value proposition to worker health, productivity and regulatory compliance, framing air quality as an operational KPI rather than just equipment. Measured KPIs such as HEPA filter capture efficiency (99.97% at 0.3 μm) and PM2.5 reduction targets aligned with WHO 2021 guideline (5 μg/m3) support robust ROI and EHS case-making. Safety-first messaging directly resonates with EHS and operations leaders and differentiates outcome-focused solutions from commodity hardware vendors.

- Value: worker health → productivity, compliance

- KPIs: HEPA 99.97% capture; PM2.5 target 5 μg/m3

- Audience: EHS & operations alignment

- Edge: outcome-driven vs commodity hardware

Field service and lifecycle support

Installation, maintenance and scheduled filter replacement create steady, recurring revenue streams; the field service management market is growing at roughly a 10% CAGR through 2030, underpinning long-term service monetization. Ongoing performance monitoring and tune-ups sustain system efficiency and reduce churn, while close service relationships boost retention and referrals. Service feedback loops directly inform product improvements and lower R&D cycles.

- Recurring revenue from installs/filters

- 10% CAGR FSM market to 2030

- Monitoring sustains efficiency

- Service drives retention/referrals

- Feedback accelerates product improvement

End-to-end HVAC filtration cuts rework 5-10% and targets USD 240bn market

End-to-end ownership reduces rework (industry 5–10% of project value) and accelerates cycles in a ~USD 240bn HVAC/filtration market (2023). Cleanroom expertise targets USD 4.2bn market (2023, ~6% CAGR), enabling premium margins via compliance. Recurring service (filters/installation) taps FSM market ~10% CAGR to 2030, supporting steady aftermarket revenue.

| Metric | Value |

|---|---|

| HVAC/filtration market | ~USD 240bn (2023) |

| Cleanroom market | USD 4.2bn (2023), ~6% CAGR |

| HEPA efficiency | 99.97% @ 0.3 μm |

| FSM CAGR | ~10% to 2030 |

| Typical rework | 5–10% project value |

What is included in the product

Provides a concise SWOT overview of SNAAM Group, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic positioning, growth priorities, and risk mitigation.

Provides a concise SNAAM Group SWOT matrix for fast, visual strategy alignment across business units, enabling leaders to spot strategic gaps quickly. Ideal for executives and teams needing a compact, decision-ready overview to prioritize initiatives and communicate priorities efficiently.

Weaknesses

Customization-heavy delivery model

Engineering-heavy, customization-first delivery compresses margins (custom project gross margins often 10–18% vs 20–35% for standardized SKUs), extends lead times by 30–60%, and raises working-capital needs by 20–40% due to bespoke components; scope creep without strict project controls is common, and scalability lags behind standardized manufacturing.

Exposure to capex cycles

Industrial customers commonly defer ventilation upgrades in downturns, causing project revenue to become lumpy and quarterly bookings to swing, with cashflow timing tied to milestone billing that typically creates 30–90 day receivable lags. Budget freezes in pharma and food plants often pause awards, compressing forecast accuracy and increasing working capital strain. Such capex sensitivity can drive pronounced volatility in order intake and margin visibility.

Potential geographic concentration

Limited geographic footprint heightens dependency on local demand and networks, concentrating revenue risk in core regions.

Expanding beyond these areas raises logistics and on-site commissioning costs, eroding margins on distant projects.

Service response times often lag in remote markets, while market entry faces certification and vendor-approval delays that slow scaling.

Aftermarket dependency on consumables

Aftermarket dependence on consumables exposes SNAAM to price erosion as generics and private-label entrants — which captured about 25% of filter sales in 2024 — push prices down; survey data in 2024 shows 62% of buyers dual-source consumables to reduce cost. Managing inventory across dozens of sizes and media increases working capital and SKU complexity, and client use of subpar consumables can degrade perceived system performance.

Brand visibility versus global incumbents

SNAAM Group's brand visibility lags versus global incumbents that dominate engineered air solutions, where 2024 procurement surveys report over 60% of complex tenders shortlist legacy vendors with global references. Bid lists and client RFPs often favor suppliers with multiregional case studies, and winning such contracts demands extensive credentials and certifications. Marketing spend and channel reach are constrained versus multinational peers, limiting lead generation.

- Low brand awareness vs global incumbents

- >60% of tenders shortlist legacy vendors (2024 surveys)

- High credential threshold for complex wins

- Limited marketing spend and channel reach

Engineering-first customization cuts margins to 10-18%, extends lead times

Engineering-first, customization-led delivery compresses project gross margins (10–18% vs 20–35% for standardized SKUs), lengthens lead times 30–60% and raises working capital; demand is lumpy with 30–90 day receivable lags and capex sensitivity. Aftermarket faces 25% generics (2024) and 62% dual-sourcing; brand shortlisting remains >60% for legacy global vendors (2024).

| Metric | Value |

|---|---|

| Custom project GM | 10–18% |

| Standard SKU GM | 20–35% |

| Receivable lag | 30–90 days |

| Generics share (2024) | 25% |

| Dual-source buyers (2024) | 62% |

| Tenders shortlist legacy (2024) | >60% |

Same Document Delivered

SNAAM Group SWOT Analysis

This is the actual SNAAM Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy now to unlock the complete, editable version with in-depth insights.

Description

Go Beyond the Preview—Access the Full Strategic Report

SNAAM Group’s strategic foothold, operational strengths, and sector-specific risks are only partially revealed here—our full SWOT unpacks competitive advantages, emergent threats, and growth levers with data-driven analysis. Purchase the complete SWOT to receive a professionally written, editable report plus an Excel matrix for planning, pitching, or investing with confidence. Unlock the full picture and act faster.

Strengths

Integrated design-to-install capability

End-to-end ownership from engineering to commissioning reduces handoffs and errors, cutting rework that industry studies estimate at 5–10% of project value. It enables faster project cycles and tighter quality control within a global HVAC/filtration market ~USD 240 billion (2023), while clients prefer a single accountable partner for complex deployments and faster, consistent warranty service.

Sector expertise in regulated industries

SNAAM Group's deep experience in food, pharma and manufacturing matches strict GMP/HACCP needs, supporting tailored cleanroom and contamination-control solutions; the global cleanroom market, valued at about USD 4.2 billion in 2023 with ~6% CAGR, underlines demand. Proven familiarity with validation, documentation and audits reduces compliance risk and sales friction, enabling premium pricing and higher contract margins.

Diverse product portfolio

Diverse portfolio—dust collectors, filtration units, and custom systems—expands addressable use cases across manufacturing, mining, and power, supporting resilience as the industrial dust collector market targets about 6% CAGR to 2030. Cross-selling and modular upgrades boost customer lifetime value and aftermarket revenue. Standardized cores with configurable options balance cost and customization, cushioning demand swings across segments.

Focus on air quality and safety outcomes

SNAAM Group ties a clear value proposition to worker health, productivity and regulatory compliance, framing air quality as an operational KPI rather than just equipment. Measured KPIs such as HEPA filter capture efficiency (99.97% at 0.3 μm) and PM2.5 reduction targets aligned with WHO 2021 guideline (5 μg/m3) support robust ROI and EHS case-making. Safety-first messaging directly resonates with EHS and operations leaders and differentiates outcome-focused solutions from commodity hardware vendors.

- Value: worker health → productivity, compliance

- KPIs: HEPA 99.97% capture; PM2.5 target 5 μg/m3

- Audience: EHS & operations alignment

- Edge: outcome-driven vs commodity hardware

Field service and lifecycle support

Installation, maintenance and scheduled filter replacement create steady, recurring revenue streams; the field service management market is growing at roughly a 10% CAGR through 2030, underpinning long-term service monetization. Ongoing performance monitoring and tune-ups sustain system efficiency and reduce churn, while close service relationships boost retention and referrals. Service feedback loops directly inform product improvements and lower R&D cycles.

- Recurring revenue from installs/filters

- 10% CAGR FSM market to 2030

- Monitoring sustains efficiency

- Service drives retention/referrals

- Feedback accelerates product improvement

End-to-end HVAC filtration cuts rework 5-10% and targets USD 240bn market

End-to-end ownership reduces rework (industry 5–10% of project value) and accelerates cycles in a ~USD 240bn HVAC/filtration market (2023). Cleanroom expertise targets USD 4.2bn market (2023, ~6% CAGR), enabling premium margins via compliance. Recurring service (filters/installation) taps FSM market ~10% CAGR to 2030, supporting steady aftermarket revenue.

| Metric | Value |

|---|---|

| HVAC/filtration market | ~USD 240bn (2023) |

| Cleanroom market | USD 4.2bn (2023), ~6% CAGR |

| HEPA efficiency | 99.97% @ 0.3 μm |

| FSM CAGR | ~10% to 2030 |

| Typical rework | 5–10% project value |

What is included in the product

Provides a concise SWOT overview of SNAAM Group, highlighting internal strengths and weaknesses alongside external opportunities and threats to inform strategic positioning, growth priorities, and risk mitigation.

Provides a concise SNAAM Group SWOT matrix for fast, visual strategy alignment across business units, enabling leaders to spot strategic gaps quickly. Ideal for executives and teams needing a compact, decision-ready overview to prioritize initiatives and communicate priorities efficiently.

Weaknesses

Customization-heavy delivery model

Engineering-heavy, customization-first delivery compresses margins (custom project gross margins often 10–18% vs 20–35% for standardized SKUs), extends lead times by 30–60%, and raises working-capital needs by 20–40% due to bespoke components; scope creep without strict project controls is common, and scalability lags behind standardized manufacturing.

Exposure to capex cycles

Industrial customers commonly defer ventilation upgrades in downturns, causing project revenue to become lumpy and quarterly bookings to swing, with cashflow timing tied to milestone billing that typically creates 30–90 day receivable lags. Budget freezes in pharma and food plants often pause awards, compressing forecast accuracy and increasing working capital strain. Such capex sensitivity can drive pronounced volatility in order intake and margin visibility.

Potential geographic concentration

Limited geographic footprint heightens dependency on local demand and networks, concentrating revenue risk in core regions.

Expanding beyond these areas raises logistics and on-site commissioning costs, eroding margins on distant projects.

Service response times often lag in remote markets, while market entry faces certification and vendor-approval delays that slow scaling.

Aftermarket dependency on consumables

Aftermarket dependence on consumables exposes SNAAM to price erosion as generics and private-label entrants — which captured about 25% of filter sales in 2024 — push prices down; survey data in 2024 shows 62% of buyers dual-source consumables to reduce cost. Managing inventory across dozens of sizes and media increases working capital and SKU complexity, and client use of subpar consumables can degrade perceived system performance.

Brand visibility versus global incumbents

SNAAM Group's brand visibility lags versus global incumbents that dominate engineered air solutions, where 2024 procurement surveys report over 60% of complex tenders shortlist legacy vendors with global references. Bid lists and client RFPs often favor suppliers with multiregional case studies, and winning such contracts demands extensive credentials and certifications. Marketing spend and channel reach are constrained versus multinational peers, limiting lead generation.

- Low brand awareness vs global incumbents

- >60% of tenders shortlist legacy vendors (2024 surveys)

- High credential threshold for complex wins

- Limited marketing spend and channel reach

Engineering-first customization cuts margins to 10-18%, extends lead times

Engineering-first, customization-led delivery compresses project gross margins (10–18% vs 20–35% for standardized SKUs), lengthens lead times 30–60% and raises working capital; demand is lumpy with 30–90 day receivable lags and capex sensitivity. Aftermarket faces 25% generics (2024) and 62% dual-sourcing; brand shortlisting remains >60% for legacy global vendors (2024).

| Metric | Value |

|---|---|

| Custom project GM | 10–18% |

| Standard SKU GM | 20–35% |

| Receivable lag | 30–90 days |

| Generics share (2024) | 25% |

| Dual-source buyers (2024) | 62% |

| Tenders shortlist legacy (2024) | >60% |

Same Document Delivered

SNAAM Group SWOT Analysis

This is the actual SNAAM Group SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report; buy now to unlock the complete, editable version with in-depth insights.