SOLiD Porter's Five Forces Analysis

From Overview to Strategy Blueprint

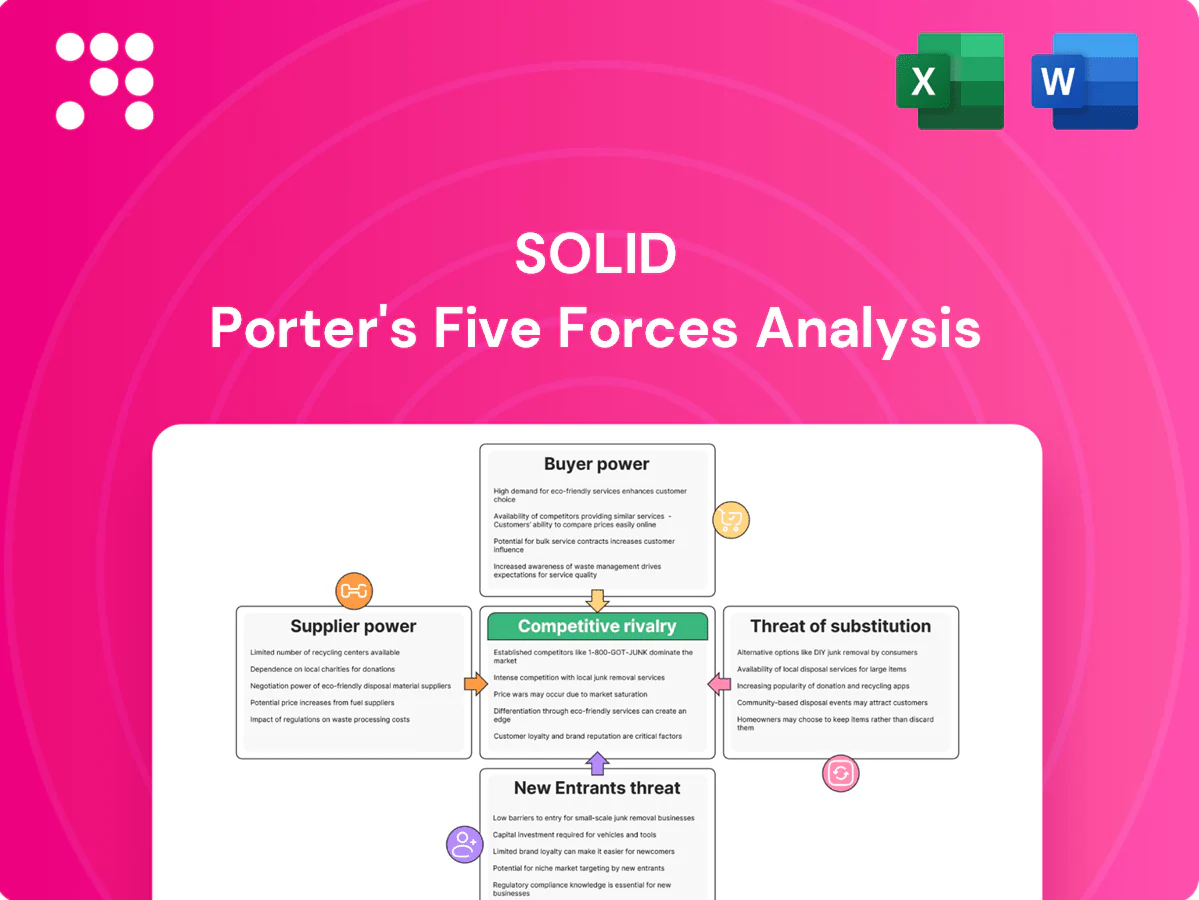

This snapshot outlines SOLiD’s bargaining power, competitive rivalry, supplier and buyer dynamics, and substitution risks, highlighting strategic pressure points and growth levers. The full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and actionable recommendations to quantify those threats and opportunities. Unlock the complete report to inform investment or strategic decisions with consultant-grade detail.

Suppliers Bargaining Power

Specialized RF and optical components

High-spec RF amps, filters and optical modules are sourced from a narrow vendor pool, with typical lead times of 12–20 weeks in 2024 and a handful of suppliers holding the majority of supply. Stringent qualification cycles (often 6–12 months) and tight performance specs limit switching, giving suppliers leverage on price and delivery. Dual-sourcing is feasible but usually adds 6–18 months and significant validation and tooling costs.

Semiconductor dependency and cycles

SOLiD depends on chipsets for signal processing, power management and optics, and the semiconductor market—global sales >$500 billion annually—remains cyclical; peak lead times exceeded 30 weeks during upcycles, increasing supplier leverage and cost pass-through. Volatility in 2024 supply chains kept prices and delivery risk elevated, while strategic inventory and multi-sourcing/design flexibility can partially mitigate supplier power.

Compliance and certification constraints

Components must meet carrier-grade standards such as NEBS Level 3 and ETSI requirements; regional safety rules add further certification layers. Requalifying alternative suppliers typically adds months to deployment timelines and raises procurement costs. Certification lock-in strengthens supplier negotiating power. Approved-vendor lists further narrow the supplier pool.

Custom OEM/ODM relationships

Custom OEM/ODM relationships create mutual dependencies through bespoke subassemblies and firmware, securing capacity but raising switching costs; in 2024 the global electronics contract manufacturing market was roughly $500 billion, underscoring supplier leverage. Suppliers capture value via NRE and engineering changes unless IP ownership and modular design limit exposure.

- Mutual dependency

- Higher switching costs

- Supplier capture: NRE/EC

- Mitigation: clear IP + modular design

Logistics and rare materials exposure

Fiber optics, rare earth magnets, and precision passives expose SOLiD to logistics and materials risk; supply chokepoints and export controls can tighten availability and raise lead times. USGS 2024 reports China supplied about 60% of global rare-earth production, heightening geopolitical risk. Rising freight and tariff volatility lift landed cost; multi-region sourcing and buffer stocks are key mitigants.

- Supply concentration: rare-earths ~60% China (USGS 2024)

- Risk drivers: export controls, port disruption, tariffs

- Mitigants: multi-region sourcing, safety stock, dual suppliers

Supplier concentration: lead times 12-30+ weeks; dual-sourcing adds 6-18 months

High supplier concentration gives strong pricing and delivery leverage: RF/optical lead times 12–30+ weeks and semiconductor market >500 billion USD (2024). Requalification/dual-sourcing typically adds 6–18 months and tooling/NRE costs, increasing switching costs. Geopolitical/material risk high: China ~60% of rare-earth supply (USGS 2024); mitigants include multi-region sourcing, modular design and buffer stock.

| Metric | Value | Impact |

|---|---|---|

| Lead time | 12–30+ weeks | High delivery risk |

| Semiconductor market | >500B USD (2024) | Price cyclicality |

| Rare-earths | China ~60% (USGS 2024) | Geopolitical risk |

| Dual-sourcing delay | 6–18 months | Higher cost |

What is included in the product

Tailored Porter’s Five Forces analysis for SOLiD that uncovers key drivers of competition, buyer and supplier power, and entry and substitute threats impacting its pricing and profitability. Detailed, strategic insights identify disruptive forces and barriers protecting incumbents—delivered in an editable format for reports, investor decks, or internal strategy use.

SOLiD's Porter's Five Forces delivers a one-sheet, customizable view that converts complex competitive dynamics into actionable insights—use the radar chart to instantly spot intensity shifts and copy-clean visuals straight into pitch decks. No macros, easy data swap, and duplicate tabs let you model pre/post scenarios fast so teams can make confident strategic moves.

Customers Bargaining Power

Carrier and neutral host concentration

Mobile network operators and top neutral hosts are large, sophisticated buyers—China Mobile has >900 million mobile subscribers, Vodafone ~275 million and AT&T ~200 million—giving them scale to extract deep discounts. Framework agreements and RFPs commonly cover multi-year, multi-million-dollar deployments, intensifying vendor competition. Losing or winning a single anchor account can shift vendor revenues by double-digit percentages in targeted regions.

Technical validation and trials

Carriers require rigorous lab and field testing before deployment, with trials commonly extending months to over a year, which delays revenue recognition and shifts bargaining leverage to buyers. Compliance with multiband and multi-operator requirements increases custom engineering and integration work, raising time-to-market. Strong proven references and performance KPIs from prior deployments reduce perceived risk and can soften price pressure.

Total cost of ownership focus

Buyers prioritize capex efficiency and opex cuts—power, space and maintenance—using TCO analyses to justify procurement choices; a 2024 survey found 62% of enterprises rely on TCO models to compare vendors. They leverage those models to pressure for 20–35% discounts or service concessions, citing projected lifetime savings. Remote management and energy efficiency (up to 40% savings in modern deployments) become key negotiation levers. Bundled SLAs can differentiate offers but impose added operational and financial obligations.

Multi-vendor strategies

Most buyers maintain approved multi-vendor lists, driving competitive bidding and rapid price benchmarking; this lowers vendors margins and increases buyer leverage. Switching costs exist but become manageable after standardizing interfaces, and interoperability claims are routinely tested during procurement to keep vendors honest.

- Approved multi-vendor lists raise bargaining power

- Competitive bidding → faster price benchmarks

- Standardized interfaces reduce switching costs

- Interoperability testing enforces vendor accountability

Integration with 5G and future readiness

Customers increasingly demand 5G NR including C-band and mmWave and future-proof fronthaul; global 5G connections reached about 1.9 billion by end-2024, raising expectations for virtualization and ORAN alignment. Over 70% of operators pursued ORAN/virtualization strategies in 2024, so non-compliance risks exclusion from major bids. Clear roadmaps and software upgradability materially reduce buyer power and win rates.

- 5G scale: ~1.9B connections (end-2024)

- Operator push: >70% pursuing ORAN/virtualization (2024)

- Key tech: C-band, mmWave, virtualized fronthaul

- Mitigant: software upgradability and clear roadmaps reduce buyer leverage

MNOs extract 20–35% discounts as ORAN adoption tops >70%

Large MNOs and neutral hosts (eg China Mobile >900M, Vodafone ~275M, AT&T ~200M) extract deep discounts via multi-year RFPs; single anchor wins can shift vendor revenues by double digits. Buyers use lengthy trials and TCO (62% of enterprises use TCO in 2024) to push 20–35% concessions; ORAN/virtualization adoption (>70% operators in 2024) raises spec demands and exclusion risk.

| Metric | 2024 Data |

|---|---|

| Global 5G connections | ~1.9B |

| ORAN/virtualization adoption | >70% |

| Buyer discount pressure | 20–35% |

| TCO reliance (enterprises) | 62% |

Preview Before You Purchase

SOLiD Porter's Five Forces Analysis

This preview shows the exact SOLiD Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the professionally written, fully formatted file ready for download and use the moment you buy. You’re previewing the final version; once payment is complete you’ll get instant access to this exact deliverable.

From Overview to Strategy Blueprint

This snapshot outlines SOLiD’s bargaining power, competitive rivalry, supplier and buyer dynamics, and substitution risks, highlighting strategic pressure points and growth levers. The full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and actionable recommendations to quantify those threats and opportunities. Unlock the complete report to inform investment or strategic decisions with consultant-grade detail.

Suppliers Bargaining Power

Specialized RF and optical components

High-spec RF amps, filters and optical modules are sourced from a narrow vendor pool, with typical lead times of 12–20 weeks in 2024 and a handful of suppliers holding the majority of supply. Stringent qualification cycles (often 6–12 months) and tight performance specs limit switching, giving suppliers leverage on price and delivery. Dual-sourcing is feasible but usually adds 6–18 months and significant validation and tooling costs.

Semiconductor dependency and cycles

SOLiD depends on chipsets for signal processing, power management and optics, and the semiconductor market—global sales >$500 billion annually—remains cyclical; peak lead times exceeded 30 weeks during upcycles, increasing supplier leverage and cost pass-through. Volatility in 2024 supply chains kept prices and delivery risk elevated, while strategic inventory and multi-sourcing/design flexibility can partially mitigate supplier power.

Compliance and certification constraints

Components must meet carrier-grade standards such as NEBS Level 3 and ETSI requirements; regional safety rules add further certification layers. Requalifying alternative suppliers typically adds months to deployment timelines and raises procurement costs. Certification lock-in strengthens supplier negotiating power. Approved-vendor lists further narrow the supplier pool.

Custom OEM/ODM relationships

Custom OEM/ODM relationships create mutual dependencies through bespoke subassemblies and firmware, securing capacity but raising switching costs; in 2024 the global electronics contract manufacturing market was roughly $500 billion, underscoring supplier leverage. Suppliers capture value via NRE and engineering changes unless IP ownership and modular design limit exposure.

- Mutual dependency

- Higher switching costs

- Supplier capture: NRE/EC

- Mitigation: clear IP + modular design

Logistics and rare materials exposure

Fiber optics, rare earth magnets, and precision passives expose SOLiD to logistics and materials risk; supply chokepoints and export controls can tighten availability and raise lead times. USGS 2024 reports China supplied about 60% of global rare-earth production, heightening geopolitical risk. Rising freight and tariff volatility lift landed cost; multi-region sourcing and buffer stocks are key mitigants.

- Supply concentration: rare-earths ~60% China (USGS 2024)

- Risk drivers: export controls, port disruption, tariffs

- Mitigants: multi-region sourcing, safety stock, dual suppliers

Supplier concentration: lead times 12-30+ weeks; dual-sourcing adds 6-18 months

High supplier concentration gives strong pricing and delivery leverage: RF/optical lead times 12–30+ weeks and semiconductor market >500 billion USD (2024). Requalification/dual-sourcing typically adds 6–18 months and tooling/NRE costs, increasing switching costs. Geopolitical/material risk high: China ~60% of rare-earth supply (USGS 2024); mitigants include multi-region sourcing, modular design and buffer stock.

| Metric | Value | Impact |

|---|---|---|

| Lead time | 12–30+ weeks | High delivery risk |

| Semiconductor market | >500B USD (2024) | Price cyclicality |

| Rare-earths | China ~60% (USGS 2024) | Geopolitical risk |

| Dual-sourcing delay | 6–18 months | Higher cost |

What is included in the product

Tailored Porter’s Five Forces analysis for SOLiD that uncovers key drivers of competition, buyer and supplier power, and entry and substitute threats impacting its pricing and profitability. Detailed, strategic insights identify disruptive forces and barriers protecting incumbents—delivered in an editable format for reports, investor decks, or internal strategy use.

SOLiD's Porter's Five Forces delivers a one-sheet, customizable view that converts complex competitive dynamics into actionable insights—use the radar chart to instantly spot intensity shifts and copy-clean visuals straight into pitch decks. No macros, easy data swap, and duplicate tabs let you model pre/post scenarios fast so teams can make confident strategic moves.

Customers Bargaining Power

Carrier and neutral host concentration

Mobile network operators and top neutral hosts are large, sophisticated buyers—China Mobile has >900 million mobile subscribers, Vodafone ~275 million and AT&T ~200 million—giving them scale to extract deep discounts. Framework agreements and RFPs commonly cover multi-year, multi-million-dollar deployments, intensifying vendor competition. Losing or winning a single anchor account can shift vendor revenues by double-digit percentages in targeted regions.

Technical validation and trials

Carriers require rigorous lab and field testing before deployment, with trials commonly extending months to over a year, which delays revenue recognition and shifts bargaining leverage to buyers. Compliance with multiband and multi-operator requirements increases custom engineering and integration work, raising time-to-market. Strong proven references and performance KPIs from prior deployments reduce perceived risk and can soften price pressure.

Total cost of ownership focus

Buyers prioritize capex efficiency and opex cuts—power, space and maintenance—using TCO analyses to justify procurement choices; a 2024 survey found 62% of enterprises rely on TCO models to compare vendors. They leverage those models to pressure for 20–35% discounts or service concessions, citing projected lifetime savings. Remote management and energy efficiency (up to 40% savings in modern deployments) become key negotiation levers. Bundled SLAs can differentiate offers but impose added operational and financial obligations.

Multi-vendor strategies

Most buyers maintain approved multi-vendor lists, driving competitive bidding and rapid price benchmarking; this lowers vendors margins and increases buyer leverage. Switching costs exist but become manageable after standardizing interfaces, and interoperability claims are routinely tested during procurement to keep vendors honest.

- Approved multi-vendor lists raise bargaining power

- Competitive bidding → faster price benchmarks

- Standardized interfaces reduce switching costs

- Interoperability testing enforces vendor accountability

Integration with 5G and future readiness

Customers increasingly demand 5G NR including C-band and mmWave and future-proof fronthaul; global 5G connections reached about 1.9 billion by end-2024, raising expectations for virtualization and ORAN alignment. Over 70% of operators pursued ORAN/virtualization strategies in 2024, so non-compliance risks exclusion from major bids. Clear roadmaps and software upgradability materially reduce buyer power and win rates.

- 5G scale: ~1.9B connections (end-2024)

- Operator push: >70% pursuing ORAN/virtualization (2024)

- Key tech: C-band, mmWave, virtualized fronthaul

- Mitigant: software upgradability and clear roadmaps reduce buyer leverage

MNOs extract 20–35% discounts as ORAN adoption tops >70%

Large MNOs and neutral hosts (eg China Mobile >900M, Vodafone ~275M, AT&T ~200M) extract deep discounts via multi-year RFPs; single anchor wins can shift vendor revenues by double digits. Buyers use lengthy trials and TCO (62% of enterprises use TCO in 2024) to push 20–35% concessions; ORAN/virtualization adoption (>70% operators in 2024) raises spec demands and exclusion risk.

| Metric | 2024 Data |

|---|---|

| Global 5G connections | ~1.9B |

| ORAN/virtualization adoption | >70% |

| Buyer discount pressure | 20–35% |

| TCO reliance (enterprises) | 62% |

Preview Before You Purchase

SOLiD Porter's Five Forces Analysis

This preview shows the exact SOLiD Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the professionally written, fully formatted file ready for download and use the moment you buy. You’re previewing the final version; once payment is complete you’ll get instant access to this exact deliverable.

Description

From Overview to Strategy Blueprint

This snapshot outlines SOLiD’s bargaining power, competitive rivalry, supplier and buyer dynamics, and substitution risks, highlighting strategic pressure points and growth levers. The full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and actionable recommendations to quantify those threats and opportunities. Unlock the complete report to inform investment or strategic decisions with consultant-grade detail.

Suppliers Bargaining Power

Specialized RF and optical components

High-spec RF amps, filters and optical modules are sourced from a narrow vendor pool, with typical lead times of 12–20 weeks in 2024 and a handful of suppliers holding the majority of supply. Stringent qualification cycles (often 6–12 months) and tight performance specs limit switching, giving suppliers leverage on price and delivery. Dual-sourcing is feasible but usually adds 6–18 months and significant validation and tooling costs.

Semiconductor dependency and cycles

SOLiD depends on chipsets for signal processing, power management and optics, and the semiconductor market—global sales >$500 billion annually—remains cyclical; peak lead times exceeded 30 weeks during upcycles, increasing supplier leverage and cost pass-through. Volatility in 2024 supply chains kept prices and delivery risk elevated, while strategic inventory and multi-sourcing/design flexibility can partially mitigate supplier power.

Compliance and certification constraints

Components must meet carrier-grade standards such as NEBS Level 3 and ETSI requirements; regional safety rules add further certification layers. Requalifying alternative suppliers typically adds months to deployment timelines and raises procurement costs. Certification lock-in strengthens supplier negotiating power. Approved-vendor lists further narrow the supplier pool.

Custom OEM/ODM relationships

Custom OEM/ODM relationships create mutual dependencies through bespoke subassemblies and firmware, securing capacity but raising switching costs; in 2024 the global electronics contract manufacturing market was roughly $500 billion, underscoring supplier leverage. Suppliers capture value via NRE and engineering changes unless IP ownership and modular design limit exposure.

- Mutual dependency

- Higher switching costs

- Supplier capture: NRE/EC

- Mitigation: clear IP + modular design

Logistics and rare materials exposure

Fiber optics, rare earth magnets, and precision passives expose SOLiD to logistics and materials risk; supply chokepoints and export controls can tighten availability and raise lead times. USGS 2024 reports China supplied about 60% of global rare-earth production, heightening geopolitical risk. Rising freight and tariff volatility lift landed cost; multi-region sourcing and buffer stocks are key mitigants.

- Supply concentration: rare-earths ~60% China (USGS 2024)

- Risk drivers: export controls, port disruption, tariffs

- Mitigants: multi-region sourcing, safety stock, dual suppliers

Supplier concentration: lead times 12-30+ weeks; dual-sourcing adds 6-18 months

High supplier concentration gives strong pricing and delivery leverage: RF/optical lead times 12–30+ weeks and semiconductor market >500 billion USD (2024). Requalification/dual-sourcing typically adds 6–18 months and tooling/NRE costs, increasing switching costs. Geopolitical/material risk high: China ~60% of rare-earth supply (USGS 2024); mitigants include multi-region sourcing, modular design and buffer stock.

| Metric | Value | Impact |

|---|---|---|

| Lead time | 12–30+ weeks | High delivery risk |

| Semiconductor market | >500B USD (2024) | Price cyclicality |

| Rare-earths | China ~60% (USGS 2024) | Geopolitical risk |

| Dual-sourcing delay | 6–18 months | Higher cost |

What is included in the product

Tailored Porter’s Five Forces analysis for SOLiD that uncovers key drivers of competition, buyer and supplier power, and entry and substitute threats impacting its pricing and profitability. Detailed, strategic insights identify disruptive forces and barriers protecting incumbents—delivered in an editable format for reports, investor decks, or internal strategy use.

SOLiD's Porter's Five Forces delivers a one-sheet, customizable view that converts complex competitive dynamics into actionable insights—use the radar chart to instantly spot intensity shifts and copy-clean visuals straight into pitch decks. No macros, easy data swap, and duplicate tabs let you model pre/post scenarios fast so teams can make confident strategic moves.

Customers Bargaining Power

Carrier and neutral host concentration

Mobile network operators and top neutral hosts are large, sophisticated buyers—China Mobile has >900 million mobile subscribers, Vodafone ~275 million and AT&T ~200 million—giving them scale to extract deep discounts. Framework agreements and RFPs commonly cover multi-year, multi-million-dollar deployments, intensifying vendor competition. Losing or winning a single anchor account can shift vendor revenues by double-digit percentages in targeted regions.

Technical validation and trials

Carriers require rigorous lab and field testing before deployment, with trials commonly extending months to over a year, which delays revenue recognition and shifts bargaining leverage to buyers. Compliance with multiband and multi-operator requirements increases custom engineering and integration work, raising time-to-market. Strong proven references and performance KPIs from prior deployments reduce perceived risk and can soften price pressure.

Total cost of ownership focus

Buyers prioritize capex efficiency and opex cuts—power, space and maintenance—using TCO analyses to justify procurement choices; a 2024 survey found 62% of enterprises rely on TCO models to compare vendors. They leverage those models to pressure for 20–35% discounts or service concessions, citing projected lifetime savings. Remote management and energy efficiency (up to 40% savings in modern deployments) become key negotiation levers. Bundled SLAs can differentiate offers but impose added operational and financial obligations.

Multi-vendor strategies

Most buyers maintain approved multi-vendor lists, driving competitive bidding and rapid price benchmarking; this lowers vendors margins and increases buyer leverage. Switching costs exist but become manageable after standardizing interfaces, and interoperability claims are routinely tested during procurement to keep vendors honest.

- Approved multi-vendor lists raise bargaining power

- Competitive bidding → faster price benchmarks

- Standardized interfaces reduce switching costs

- Interoperability testing enforces vendor accountability

Integration with 5G and future readiness

Customers increasingly demand 5G NR including C-band and mmWave and future-proof fronthaul; global 5G connections reached about 1.9 billion by end-2024, raising expectations for virtualization and ORAN alignment. Over 70% of operators pursued ORAN/virtualization strategies in 2024, so non-compliance risks exclusion from major bids. Clear roadmaps and software upgradability materially reduce buyer power and win rates.

- 5G scale: ~1.9B connections (end-2024)

- Operator push: >70% pursuing ORAN/virtualization (2024)

- Key tech: C-band, mmWave, virtualized fronthaul

- Mitigant: software upgradability and clear roadmaps reduce buyer leverage

MNOs extract 20–35% discounts as ORAN adoption tops >70%

Large MNOs and neutral hosts (eg China Mobile >900M, Vodafone ~275M, AT&T ~200M) extract deep discounts via multi-year RFPs; single anchor wins can shift vendor revenues by double digits. Buyers use lengthy trials and TCO (62% of enterprises use TCO in 2024) to push 20–35% concessions; ORAN/virtualization adoption (>70% operators in 2024) raises spec demands and exclusion risk.

| Metric | 2024 Data |

|---|---|

| Global 5G connections | ~1.9B |

| ORAN/virtualization adoption | >70% |

| Buyer discount pressure | 20–35% |

| TCO reliance (enterprises) | 62% |

Preview Before You Purchase

SOLiD Porter's Five Forces Analysis

This preview shows the exact SOLiD Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document displayed is the professionally written, fully formatted file ready for download and use the moment you buy. You’re previewing the final version; once payment is complete you’ll get instant access to this exact deliverable.