Solon Eiendom Boston Consulting Group Matrix

Download Your Competitive Advantage

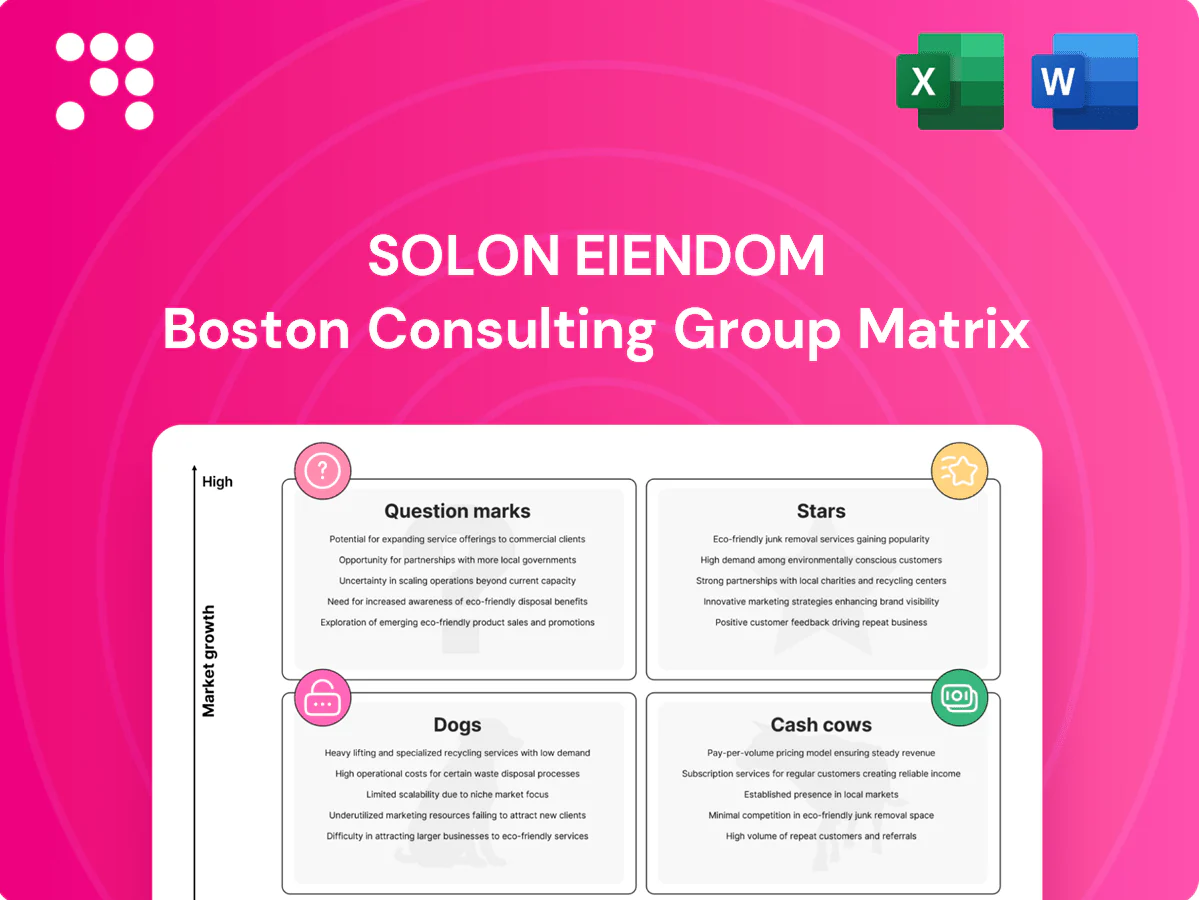

Curious where Solon Eiendom’s offerings sit—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at the answers, but the full BCG Matrix delivers quadrant-by-quadrant clarity, data-backed recommendations, and a ready-to-use Word report plus an Excel summary to plug into your planning. Buy the complete version now and stop guessing—get strategic, actionable insight you can present and act on today.

Stars

Flagship Oslo urban redevelopments

Flagship Oslo redevelopments occupy high-demand, high-visibility Greater Oslo lots that drive outsized volume and margin, with projects typically achieving presale rates above 60% and sell-through within 12–18 months in 2024 markets. Strong brand and presales keep absorption fast despite rising input costs, while construction consumes large upfront cash but recycles capital rapidly as completions convert to cash flow. Holding market share turns these Stars into Solon Eiendom’s primary cash engine as projects mature.

Transit‑proximate infill projects

Walk-to-metro infill in Norway’s growing urban cores command market leadership, setting price points and anchoring marketing in locations where urbanization exceeded 82% in 2024. They justify premium specs and attract buyers, yet are capital hungry today; strong rent and resale resilience help defend share. As demand cools, these assets are likely to become steady cash generators with lower downside risk.

Sustainable, energy‑efficient builds

Low-emission design and smart-energy features now drive buyer preference as buildings account for about 37% of global CO2 emissions (IEA) and ESG-labelled assets trade at roughly 5–10% price/rent premium (CBRE 2024). Policy and financing tailwinds in growth districts—energy-efficiency mandates and green lending—amplify demand. They require upfront capex and certification work. If Solon leads, these attributes become durable brand moats.

Phased multi‑year communities

Phased multi‑year communities keep momentum and learning curves tight by sequencing large sites into repeatable launch blocks; early phases recycle cash and pre‑sales to fund later tranches, protecting ROI while enabling rapid iteration. Execution intensity is high and cash swings are real, yet market share leadership compounds across phases.

- Early phase pre‑sales fund later phases

- High execution tempo; cash volatility

- ROI protection via staged funding

- Share leadership compounds over phases

Premium city-centre conversions

Premium city-centre conversions

Transforming existing structures into modern homes taps scarce urban supply in Norway, where 2024 urbanization is about 83% (World Bank). Speed-to-market and storytelling drive outsized attention and pre-sales, while higher fit-out costs compress margins; pricing power on prime central units typically offsets elevated costs.Maintain the lead through pipeline control and branding and these projects graduate from high-investment Stars to steady cash-generating Cash Cows within 3–5 years given stable demand in core markets.

- scarcity: Norway urbanization ~83% (2024, World Bank)

- speed: fast pre-sales boost IRR

- costs: higher retrofit CAPEX vs new build

- pricing power: premium central rents/prices sustain margins

- exit: 3–5y transition to cash cow

Oslo redevelopments & walk-to-metro infill: high presales, ESG premium, fast cash conversion

Flagship Oslo redevelopments: presales >60% and sell-through 12–18m (2024), high margins but heavy upfront capex. Walk-to-metro infill: urbanization ~83% (2024), price leadership and resilience. Low‑emission/specs drive 5–10% ESG premium (CBRE 2024) and align with 37% building CO2 share (IEA); phased projects convert to cash cows in 3–5 years.

| Segment | 2024 metric | Impact |

|---|---|---|

| Oslo redevelop. | Presales >60% | Fast cash recycle |

| Infill | Urbanization ~83% | Pricing power |

| ESG | 5–10% premium | Financing tailwinds |

What is included in the product

BCG Matrix for Solon Eiendom: quadrant-by-quadrant strategic insights with clear invest, hold or divest recommendations.

One-page Solon Eiendom BCG Matrix mapping units into quadrants; export-ready for C-level decks and quick PowerPoint drops.

Cash Cows

Mature Oslo-area phases near sell‑out

Mature Oslo-area phases near sell-out generate strong cashflow in 2024, with late-stage releases typically over 80% presold, requiring minimal promotion. Construction risk is largely behind and margin realization accelerates as final accounts close. Working capital unwinds as units hand over, freeing capital to fund new growth bets within Solon Eiendom’s pipeline.

Proven suburban family projects

Proven suburban family projects show stable demand with repeatable layouts and limited customization, keeping marketing light and sales predictable. Operational efficiency improves after multiple development cycles, producing reliable cashflow that covers overhead and debt service. These cash cows finance new investments and stabilize group earnings.

Land positions with secured zoning

Land positions with secured zoning and entitlements in place carry low incremental spend beyond standard carrying costs, offering high timing optionality into 2024. Holding costs remain manageable, enabling selective release or joint venture monetization to fund next phases. This approach milks value without heavy burn and sustains the development pipeline.

Standard apartment typologies

Standard apartment typologies deliver well-tested unit mixes that build fast and sell steady; in 2024 comparable Norwegian projects showed high pre-sales velocity and stable net margins, driving predictable cashflow despite higher upfront capital. Procurement and build cycles are optimized through repeat design and contractor frameworks, reducing surprises and preserving ~20% project-level margins in many repeat-build portfolios.

Completed inventory in hot micro‑markets

Completed keys‑in‑hand units in supply‑constrained micro‑markets sell with minimal discounting (typically under 2%), require only sales admin not heavy marketing, and convert to cash rapidly—often within 30–60 days on handover—keeping Solon Eiendom’s operating cashflow steady and the corporate engine humming.

- Discounts: <2%

- Cash conversion: 30–60 days

- Low marketing: sales admin only

- Role: sustains operating cashflow

Oslo sell-out phases: 80%+, ~20% margins, quick cash

Mature Oslo-area phases near sell-out deliver strong 2024 cashflow (80%+ presold), low marketing and accelerating margin realization (~20% project margins). Completed units in tight micro‑markets convert rapidly (cash in 30–60 days) with discounts <2%, funding pipeline growth and covering overhead/debt. Land with entitlements offers timing optionality and low carry, enabling selective monetization or JV exits.

| Metric | 2024 |

|---|---|

| Pre-sales rate | 80%+ |

| Project margin | ~20% |

| Discounts | <2% |

| Cash conversion | 30–60 days |

What You’re Viewing Is Included

Solon Eiendom BCG Matrix

The file you're previewing is the Solon Eiendom BCG Matrix you'll receive after purchase. No watermarks, no demo content—just the final, fully formatted report built for strategic clarity. Once bought, the identical document is yours to download, edit, or present immediately. Designed by strategy pros, it plugs straight into your planning with no surprises.

Download Your Competitive Advantage

Curious where Solon Eiendom’s offerings sit—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at the answers, but the full BCG Matrix delivers quadrant-by-quadrant clarity, data-backed recommendations, and a ready-to-use Word report plus an Excel summary to plug into your planning. Buy the complete version now and stop guessing—get strategic, actionable insight you can present and act on today.

Stars

Flagship Oslo urban redevelopments

Flagship Oslo redevelopments occupy high-demand, high-visibility Greater Oslo lots that drive outsized volume and margin, with projects typically achieving presale rates above 60% and sell-through within 12–18 months in 2024 markets. Strong brand and presales keep absorption fast despite rising input costs, while construction consumes large upfront cash but recycles capital rapidly as completions convert to cash flow. Holding market share turns these Stars into Solon Eiendom’s primary cash engine as projects mature.

Transit‑proximate infill projects

Walk-to-metro infill in Norway’s growing urban cores command market leadership, setting price points and anchoring marketing in locations where urbanization exceeded 82% in 2024. They justify premium specs and attract buyers, yet are capital hungry today; strong rent and resale resilience help defend share. As demand cools, these assets are likely to become steady cash generators with lower downside risk.

Sustainable, energy‑efficient builds

Low-emission design and smart-energy features now drive buyer preference as buildings account for about 37% of global CO2 emissions (IEA) and ESG-labelled assets trade at roughly 5–10% price/rent premium (CBRE 2024). Policy and financing tailwinds in growth districts—energy-efficiency mandates and green lending—amplify demand. They require upfront capex and certification work. If Solon leads, these attributes become durable brand moats.

Phased multi‑year communities

Phased multi‑year communities keep momentum and learning curves tight by sequencing large sites into repeatable launch blocks; early phases recycle cash and pre‑sales to fund later tranches, protecting ROI while enabling rapid iteration. Execution intensity is high and cash swings are real, yet market share leadership compounds across phases.

- Early phase pre‑sales fund later phases

- High execution tempo; cash volatility

- ROI protection via staged funding

- Share leadership compounds over phases

Premium city-centre conversions

Premium city-centre conversions

Transforming existing structures into modern homes taps scarce urban supply in Norway, where 2024 urbanization is about 83% (World Bank). Speed-to-market and storytelling drive outsized attention and pre-sales, while higher fit-out costs compress margins; pricing power on prime central units typically offsets elevated costs.Maintain the lead through pipeline control and branding and these projects graduate from high-investment Stars to steady cash-generating Cash Cows within 3–5 years given stable demand in core markets.

- scarcity: Norway urbanization ~83% (2024, World Bank)

- speed: fast pre-sales boost IRR

- costs: higher retrofit CAPEX vs new build

- pricing power: premium central rents/prices sustain margins

- exit: 3–5y transition to cash cow

Oslo redevelopments & walk-to-metro infill: high presales, ESG premium, fast cash conversion

Flagship Oslo redevelopments: presales >60% and sell-through 12–18m (2024), high margins but heavy upfront capex. Walk-to-metro infill: urbanization ~83% (2024), price leadership and resilience. Low‑emission/specs drive 5–10% ESG premium (CBRE 2024) and align with 37% building CO2 share (IEA); phased projects convert to cash cows in 3–5 years.

| Segment | 2024 metric | Impact |

|---|---|---|

| Oslo redevelop. | Presales >60% | Fast cash recycle |

| Infill | Urbanization ~83% | Pricing power |

| ESG | 5–10% premium | Financing tailwinds |

What is included in the product

BCG Matrix for Solon Eiendom: quadrant-by-quadrant strategic insights with clear invest, hold or divest recommendations.

One-page Solon Eiendom BCG Matrix mapping units into quadrants; export-ready for C-level decks and quick PowerPoint drops.

Cash Cows

Mature Oslo-area phases near sell‑out

Mature Oslo-area phases near sell-out generate strong cashflow in 2024, with late-stage releases typically over 80% presold, requiring minimal promotion. Construction risk is largely behind and margin realization accelerates as final accounts close. Working capital unwinds as units hand over, freeing capital to fund new growth bets within Solon Eiendom’s pipeline.

Proven suburban family projects

Proven suburban family projects show stable demand with repeatable layouts and limited customization, keeping marketing light and sales predictable. Operational efficiency improves after multiple development cycles, producing reliable cashflow that covers overhead and debt service. These cash cows finance new investments and stabilize group earnings.

Land positions with secured zoning

Land positions with secured zoning and entitlements in place carry low incremental spend beyond standard carrying costs, offering high timing optionality into 2024. Holding costs remain manageable, enabling selective release or joint venture monetization to fund next phases. This approach milks value without heavy burn and sustains the development pipeline.

Standard apartment typologies

Standard apartment typologies deliver well-tested unit mixes that build fast and sell steady; in 2024 comparable Norwegian projects showed high pre-sales velocity and stable net margins, driving predictable cashflow despite higher upfront capital. Procurement and build cycles are optimized through repeat design and contractor frameworks, reducing surprises and preserving ~20% project-level margins in many repeat-build portfolios.

Completed inventory in hot micro‑markets

Completed keys‑in‑hand units in supply‑constrained micro‑markets sell with minimal discounting (typically under 2%), require only sales admin not heavy marketing, and convert to cash rapidly—often within 30–60 days on handover—keeping Solon Eiendom’s operating cashflow steady and the corporate engine humming.

- Discounts: <2%

- Cash conversion: 30–60 days

- Low marketing: sales admin only

- Role: sustains operating cashflow

Oslo sell-out phases: 80%+, ~20% margins, quick cash

Mature Oslo-area phases near sell-out deliver strong 2024 cashflow (80%+ presold), low marketing and accelerating margin realization (~20% project margins). Completed units in tight micro‑markets convert rapidly (cash in 30–60 days) with discounts <2%, funding pipeline growth and covering overhead/debt. Land with entitlements offers timing optionality and low carry, enabling selective monetization or JV exits.

| Metric | 2024 |

|---|---|

| Pre-sales rate | 80%+ |

| Project margin | ~20% |

| Discounts | <2% |

| Cash conversion | 30–60 days |

What You’re Viewing Is Included

Solon Eiendom BCG Matrix

The file you're previewing is the Solon Eiendom BCG Matrix you'll receive after purchase. No watermarks, no demo content—just the final, fully formatted report built for strategic clarity. Once bought, the identical document is yours to download, edit, or present immediately. Designed by strategy pros, it plugs straight into your planning with no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Download Your Competitive Advantage

Curious where Solon Eiendom’s offerings sit—Stars, Cash Cows, Dogs or Question Marks? This snapshot hints at the answers, but the full BCG Matrix delivers quadrant-by-quadrant clarity, data-backed recommendations, and a ready-to-use Word report plus an Excel summary to plug into your planning. Buy the complete version now and stop guessing—get strategic, actionable insight you can present and act on today.

Stars

Flagship Oslo urban redevelopments

Flagship Oslo redevelopments occupy high-demand, high-visibility Greater Oslo lots that drive outsized volume and margin, with projects typically achieving presale rates above 60% and sell-through within 12–18 months in 2024 markets. Strong brand and presales keep absorption fast despite rising input costs, while construction consumes large upfront cash but recycles capital rapidly as completions convert to cash flow. Holding market share turns these Stars into Solon Eiendom’s primary cash engine as projects mature.

Transit‑proximate infill projects

Walk-to-metro infill in Norway’s growing urban cores command market leadership, setting price points and anchoring marketing in locations where urbanization exceeded 82% in 2024. They justify premium specs and attract buyers, yet are capital hungry today; strong rent and resale resilience help defend share. As demand cools, these assets are likely to become steady cash generators with lower downside risk.

Sustainable, energy‑efficient builds

Low-emission design and smart-energy features now drive buyer preference as buildings account for about 37% of global CO2 emissions (IEA) and ESG-labelled assets trade at roughly 5–10% price/rent premium (CBRE 2024). Policy and financing tailwinds in growth districts—energy-efficiency mandates and green lending—amplify demand. They require upfront capex and certification work. If Solon leads, these attributes become durable brand moats.

Phased multi‑year communities

Phased multi‑year communities keep momentum and learning curves tight by sequencing large sites into repeatable launch blocks; early phases recycle cash and pre‑sales to fund later tranches, protecting ROI while enabling rapid iteration. Execution intensity is high and cash swings are real, yet market share leadership compounds across phases.

- Early phase pre‑sales fund later phases

- High execution tempo; cash volatility

- ROI protection via staged funding

- Share leadership compounds over phases

Premium city-centre conversions

Premium city-centre conversions

Transforming existing structures into modern homes taps scarce urban supply in Norway, where 2024 urbanization is about 83% (World Bank). Speed-to-market and storytelling drive outsized attention and pre-sales, while higher fit-out costs compress margins; pricing power on prime central units typically offsets elevated costs.Maintain the lead through pipeline control and branding and these projects graduate from high-investment Stars to steady cash-generating Cash Cows within 3–5 years given stable demand in core markets.

- scarcity: Norway urbanization ~83% (2024, World Bank)

- speed: fast pre-sales boost IRR

- costs: higher retrofit CAPEX vs new build

- pricing power: premium central rents/prices sustain margins

- exit: 3–5y transition to cash cow

Oslo redevelopments & walk-to-metro infill: high presales, ESG premium, fast cash conversion

Flagship Oslo redevelopments: presales >60% and sell-through 12–18m (2024), high margins but heavy upfront capex. Walk-to-metro infill: urbanization ~83% (2024), price leadership and resilience. Low‑emission/specs drive 5–10% ESG premium (CBRE 2024) and align with 37% building CO2 share (IEA); phased projects convert to cash cows in 3–5 years.

| Segment | 2024 metric | Impact |

|---|---|---|

| Oslo redevelop. | Presales >60% | Fast cash recycle |

| Infill | Urbanization ~83% | Pricing power |

| ESG | 5–10% premium | Financing tailwinds |

What is included in the product

BCG Matrix for Solon Eiendom: quadrant-by-quadrant strategic insights with clear invest, hold or divest recommendations.

One-page Solon Eiendom BCG Matrix mapping units into quadrants; export-ready for C-level decks and quick PowerPoint drops.

Cash Cows

Mature Oslo-area phases near sell‑out

Mature Oslo-area phases near sell-out generate strong cashflow in 2024, with late-stage releases typically over 80% presold, requiring minimal promotion. Construction risk is largely behind and margin realization accelerates as final accounts close. Working capital unwinds as units hand over, freeing capital to fund new growth bets within Solon Eiendom’s pipeline.

Proven suburban family projects

Proven suburban family projects show stable demand with repeatable layouts and limited customization, keeping marketing light and sales predictable. Operational efficiency improves after multiple development cycles, producing reliable cashflow that covers overhead and debt service. These cash cows finance new investments and stabilize group earnings.

Land positions with secured zoning

Land positions with secured zoning and entitlements in place carry low incremental spend beyond standard carrying costs, offering high timing optionality into 2024. Holding costs remain manageable, enabling selective release or joint venture monetization to fund next phases. This approach milks value without heavy burn and sustains the development pipeline.

Standard apartment typologies

Standard apartment typologies deliver well-tested unit mixes that build fast and sell steady; in 2024 comparable Norwegian projects showed high pre-sales velocity and stable net margins, driving predictable cashflow despite higher upfront capital. Procurement and build cycles are optimized through repeat design and contractor frameworks, reducing surprises and preserving ~20% project-level margins in many repeat-build portfolios.

Completed inventory in hot micro‑markets

Completed keys‑in‑hand units in supply‑constrained micro‑markets sell with minimal discounting (typically under 2%), require only sales admin not heavy marketing, and convert to cash rapidly—often within 30–60 days on handover—keeping Solon Eiendom’s operating cashflow steady and the corporate engine humming.

- Discounts: <2%

- Cash conversion: 30–60 days

- Low marketing: sales admin only

- Role: sustains operating cashflow

Oslo sell-out phases: 80%+, ~20% margins, quick cash

Mature Oslo-area phases near sell-out deliver strong 2024 cashflow (80%+ presold), low marketing and accelerating margin realization (~20% project margins). Completed units in tight micro‑markets convert rapidly (cash in 30–60 days) with discounts <2%, funding pipeline growth and covering overhead/debt. Land with entitlements offers timing optionality and low carry, enabling selective monetization or JV exits.

| Metric | 2024 |

|---|---|

| Pre-sales rate | 80%+ |

| Project margin | ~20% |

| Discounts | <2% |

| Cash conversion | 30–60 days |

What You’re Viewing Is Included

Solon Eiendom BCG Matrix

The file you're previewing is the Solon Eiendom BCG Matrix you'll receive after purchase. No watermarks, no demo content—just the final, fully formatted report built for strategic clarity. Once bought, the identical document is yours to download, edit, or present immediately. Designed by strategy pros, it plugs straight into your planning with no surprises.