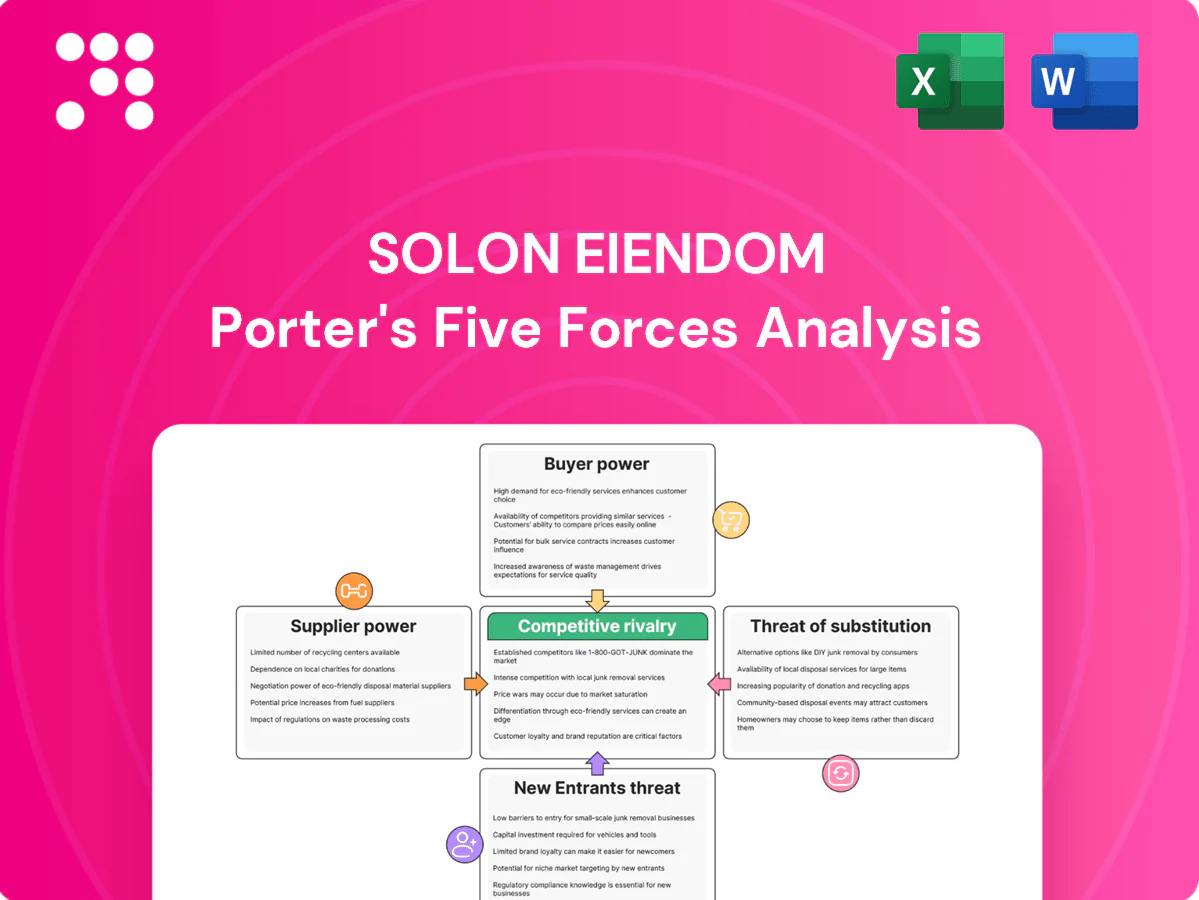

Solon Eiendom Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Solon Eiendom faces moderate supplier leverage, concentrated buyers in key segments, and rising competitive pressure from new mixed‑use developers, while substitutes and regulatory shifts create strategic uncertainty. This snapshot highlights core risks and advantages. Want full force-by-force ratings, visuals and actionable strategy? Unlock the complete Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown tailored to Solon Eiendom.

Suppliers Bargaining Power

Constrained land sellers

Prime plots in Greater Oslo are scarce, controlled mainly by municipalities, institutions and a few private owners; the metro area surpassed 1.7 million residents in 2024, intensifying land demand. Limited rezoning options raise landholder leverage on price and terms. Solon mitigates this with early-stage option agreements and JV partnerships. Persistent bidding pressure keeps acquisition costs elevated.

Contractors and trades

Construction capacity in Norway is cyclical and persistent tightness in skilled trades—highlighted by SSB reporting high vacancy rates in construction in 2024—boosts contractor bargaining power.

Framework agreements and multi-sourcing temper headline rates, but complex urban projects narrow viable vendors and sustain premiums.

Cost inflation and index-linked contracts shift more risk onto developers, while strict quality and HSE standards limit substitutions.

Building materials volatility

Materials like timber, steel and HVAC components face global price swings and logistics risks; HRC steel spot prices swung roughly ±25% in 2023–24 and softwood lumber futures moved about 30% over the same period, amplifying supplier leverage during spikes and bottlenecks. Hedging, standardized specs and bulk purchasing mitigate shocks, but bespoke urban design limits full standardization. Green material requirements narrow approved suppliers and raise procurement premiums by double digits in many projects.

Design and engineering firms

Architects and planners with urban regeneration expertise are scarce in 2024, increasing their leverage over fees and delivery schedules; Solon’s place-making focus raises dependency on these firms. Long-term partnerships can align incentives but capacity constraints still delay permits and project starts. Premium, award-winning designs can lift selling prices while raising upfront development costs.

- Specialist scarcity → higher fees

- Dependency on place-making firms

- Long-term ties mitigate misalignment

- Capacity limits → permit/start delays

- Premium design → higher sales value and costs

Municipal permitting bodies

Municipal permitting bodies function as de facto suppliers by controlling zoning, density and compliance with TEK17, giving municipalities decisive leverage over project viability and timing. Proactive stakeholder engagement reduces friction but cannot override statutory powers under the Planning and Building Act; permit delays raise holding periods and financing costs.

- Regulatory control: zoning, TEK17

- Leverage: approvals determine density

- Mitigation: stakeholder engagement helps

- Risk: delays increase holding/financing costs

Oslo land scarcity, rezoning limits and HRC ±25%, lumber ~30% swings squeeze developers

Scarce Greater Oslo land (metro >1.7M in 2024) and limited rezoning give suppliers strong price leverage. Tight construction labor (SSB: high vacancy in 2024) and specialist architects raise contracting fees and schedule risk. Material swings (HRC ±25% 2023–24; lumber ~30%) and municipal permitting control further shift cost/timing risk to developers.

| Factor | 2024 metric |

|---|---|

| Population (Greater Oslo) | >1.7M |

| HRC steel swing | ±25% (2023–24) |

| Lumber futures | ~30% (2023–24) |

| Construction vacancies | High (SSB 2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Solon Eiendom that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging disruptive threats to its market position, with strategic commentary for investors and management.

One-sheet Porter's Five Forces for Solon Eiendom that pinpoints competitive pressures and opportunities, letting you quickly allocate defenses and growth actions and drop the chart directly into decks or stress-test scenarios.

Customers Bargaining Power

Price-sensitive homebuyers

End-buyers remain highly price-sensitive to mortgage costs, with Norwegian mortgage rates averaging around 4.5% in 2024, boosting bargaining power in downturns. Developers counter with incentives, flexible unit mix and staged pricing to stimulate uptake. In upcycles Oslo scarcity and low central inventory reduce buyer leverage, while strong brand trust and proven build quality allow Solon Eiendom to command premiums and face less price pushback.

High transparency market

Norway’s 98% internet penetration and Finn.no’s ~2.5 million monthly users in 2024 make comparisons across newbuilds and existing stock straightforward, boosting buyer leverage on features and pricing. Transparent comps and public transaction data shorten negotiation cycles and intensify price pressure at launch. Strong digital listings raise competition, while location, amenities and sustainability remain key differentiation levers.

Shift to sustainability

Buyers increasingly demand energy efficiency, low operating costs and green certifications; buildings account for about 40% of EU energy use (2024), raising expectations that can compress margins if ESG premiums are resisted. Market data in 2024 showed green-certified assets delivering roughly a 4% rent premium and ~6% value uplift, expanding the buyer pool and supporting pricing. Emphasizing long-term savings — operational cuts of 10–25% on energy bills in efficient buildings — helps justify higher upfront prices.

Investor and bulk buyers

Investor and bulk buyers (as of 2024) leverage scale to secure bulk discounts and bespoke terms, de-risking projects while compressing per-unit margins. Pre-sales to institutional investors often unlock financing and accelerate construction starts. Maintaining a mix of retail and bulk sales preserves Solon Eiendom's overall pricing power and margin flexibility.

- Bulk buyers: negotiated terms, lower unit margin

- Pre-sales: enable financing, earlier starts

- Mix strategy: balance pricing power

Alternatives in resale market

Norway's robust secondary market, accounting for roughly 85–90% of home transactions in 2024, offers immediate occupancy across diverse locations and raises buyer bargaining power. When newbuild premiums widen to about 5–12%, buyers often switch to existing homes, while renovation-ready units compete on total cost of ownership. Emphasizing 10-year warranty, energy efficiency and modern specs helps defend newbuild value.

- Secondary market share: ~85–90% (2024)

- Newbuild premium pressure: 5–12%

- Defensive levers: 10-year warranty; energy efficiency; modern specs

Buyers gain leverage as mortgages ~4.5%, newbuild premium squeezed; green assets uplift

Buyers hold strong price leverage when mortgage rates hit ~4.5% (2024) and can compare listings via Finn.no (~2.5M monthly users), pressuring newbuild premiums (5–12%). Secondary market share ~85–90% (2024) raises switching risk; green-certified assets show ~4% rent premium / ~6% value uplift. Bulk/investor pre-sales compress per-unit margins but enable financing.

| Metric | 2024 |

|---|---|

| Mortgage rate | ~4.5% |

| Finn.no users | ~2.5M/mo |

| Secondary market share | 85–90% |

| Green premium | Rent +4% / Value +6% |

| Newbuild premium | 5–12% |

Preview Before You Purchase

Solon Eiendom Porter's Five Forces Analysis

This preview shows the exact Solon Eiendom Porter's Five Forces Analysis you'll receive immediately after purchase—no mockups or placeholders. The file is the professionally formatted, final document ready for download and use the moment you buy. What you see here is precisely what will be available to you instantly after payment.

Don't Miss the Bigger Picture

Solon Eiendom faces moderate supplier leverage, concentrated buyers in key segments, and rising competitive pressure from new mixed‑use developers, while substitutes and regulatory shifts create strategic uncertainty. This snapshot highlights core risks and advantages. Want full force-by-force ratings, visuals and actionable strategy? Unlock the complete Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown tailored to Solon Eiendom.

Suppliers Bargaining Power

Constrained land sellers

Prime plots in Greater Oslo are scarce, controlled mainly by municipalities, institutions and a few private owners; the metro area surpassed 1.7 million residents in 2024, intensifying land demand. Limited rezoning options raise landholder leverage on price and terms. Solon mitigates this with early-stage option agreements and JV partnerships. Persistent bidding pressure keeps acquisition costs elevated.

Contractors and trades

Construction capacity in Norway is cyclical and persistent tightness in skilled trades—highlighted by SSB reporting high vacancy rates in construction in 2024—boosts contractor bargaining power.

Framework agreements and multi-sourcing temper headline rates, but complex urban projects narrow viable vendors and sustain premiums.

Cost inflation and index-linked contracts shift more risk onto developers, while strict quality and HSE standards limit substitutions.

Building materials volatility

Materials like timber, steel and HVAC components face global price swings and logistics risks; HRC steel spot prices swung roughly ±25% in 2023–24 and softwood lumber futures moved about 30% over the same period, amplifying supplier leverage during spikes and bottlenecks. Hedging, standardized specs and bulk purchasing mitigate shocks, but bespoke urban design limits full standardization. Green material requirements narrow approved suppliers and raise procurement premiums by double digits in many projects.

Design and engineering firms

Architects and planners with urban regeneration expertise are scarce in 2024, increasing their leverage over fees and delivery schedules; Solon’s place-making focus raises dependency on these firms. Long-term partnerships can align incentives but capacity constraints still delay permits and project starts. Premium, award-winning designs can lift selling prices while raising upfront development costs.

- Specialist scarcity → higher fees

- Dependency on place-making firms

- Long-term ties mitigate misalignment

- Capacity limits → permit/start delays

- Premium design → higher sales value and costs

Municipal permitting bodies

Municipal permitting bodies function as de facto suppliers by controlling zoning, density and compliance with TEK17, giving municipalities decisive leverage over project viability and timing. Proactive stakeholder engagement reduces friction but cannot override statutory powers under the Planning and Building Act; permit delays raise holding periods and financing costs.

- Regulatory control: zoning, TEK17

- Leverage: approvals determine density

- Mitigation: stakeholder engagement helps

- Risk: delays increase holding/financing costs

Oslo land scarcity, rezoning limits and HRC ±25%, lumber ~30% swings squeeze developers

Scarce Greater Oslo land (metro >1.7M in 2024) and limited rezoning give suppliers strong price leverage. Tight construction labor (SSB: high vacancy in 2024) and specialist architects raise contracting fees and schedule risk. Material swings (HRC ±25% 2023–24; lumber ~30%) and municipal permitting control further shift cost/timing risk to developers.

| Factor | 2024 metric |

|---|---|

| Population (Greater Oslo) | >1.7M |

| HRC steel swing | ±25% (2023–24) |

| Lumber futures | ~30% (2023–24) |

| Construction vacancies | High (SSB 2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Solon Eiendom that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging disruptive threats to its market position, with strategic commentary for investors and management.

One-sheet Porter's Five Forces for Solon Eiendom that pinpoints competitive pressures and opportunities, letting you quickly allocate defenses and growth actions and drop the chart directly into decks or stress-test scenarios.

Customers Bargaining Power

Price-sensitive homebuyers

End-buyers remain highly price-sensitive to mortgage costs, with Norwegian mortgage rates averaging around 4.5% in 2024, boosting bargaining power in downturns. Developers counter with incentives, flexible unit mix and staged pricing to stimulate uptake. In upcycles Oslo scarcity and low central inventory reduce buyer leverage, while strong brand trust and proven build quality allow Solon Eiendom to command premiums and face less price pushback.

High transparency market

Norway’s 98% internet penetration and Finn.no’s ~2.5 million monthly users in 2024 make comparisons across newbuilds and existing stock straightforward, boosting buyer leverage on features and pricing. Transparent comps and public transaction data shorten negotiation cycles and intensify price pressure at launch. Strong digital listings raise competition, while location, amenities and sustainability remain key differentiation levers.

Shift to sustainability

Buyers increasingly demand energy efficiency, low operating costs and green certifications; buildings account for about 40% of EU energy use (2024), raising expectations that can compress margins if ESG premiums are resisted. Market data in 2024 showed green-certified assets delivering roughly a 4% rent premium and ~6% value uplift, expanding the buyer pool and supporting pricing. Emphasizing long-term savings — operational cuts of 10–25% on energy bills in efficient buildings — helps justify higher upfront prices.

Investor and bulk buyers

Investor and bulk buyers (as of 2024) leverage scale to secure bulk discounts and bespoke terms, de-risking projects while compressing per-unit margins. Pre-sales to institutional investors often unlock financing and accelerate construction starts. Maintaining a mix of retail and bulk sales preserves Solon Eiendom's overall pricing power and margin flexibility.

- Bulk buyers: negotiated terms, lower unit margin

- Pre-sales: enable financing, earlier starts

- Mix strategy: balance pricing power

Alternatives in resale market

Norway's robust secondary market, accounting for roughly 85–90% of home transactions in 2024, offers immediate occupancy across diverse locations and raises buyer bargaining power. When newbuild premiums widen to about 5–12%, buyers often switch to existing homes, while renovation-ready units compete on total cost of ownership. Emphasizing 10-year warranty, energy efficiency and modern specs helps defend newbuild value.

- Secondary market share: ~85–90% (2024)

- Newbuild premium pressure: 5–12%

- Defensive levers: 10-year warranty; energy efficiency; modern specs

Buyers gain leverage as mortgages ~4.5%, newbuild premium squeezed; green assets uplift

Buyers hold strong price leverage when mortgage rates hit ~4.5% (2024) and can compare listings via Finn.no (~2.5M monthly users), pressuring newbuild premiums (5–12%). Secondary market share ~85–90% (2024) raises switching risk; green-certified assets show ~4% rent premium / ~6% value uplift. Bulk/investor pre-sales compress per-unit margins but enable financing.

| Metric | 2024 |

|---|---|

| Mortgage rate | ~4.5% |

| Finn.no users | ~2.5M/mo |

| Secondary market share | 85–90% |

| Green premium | Rent +4% / Value +6% |

| Newbuild premium | 5–12% |

Preview Before You Purchase

Solon Eiendom Porter's Five Forces Analysis

This preview shows the exact Solon Eiendom Porter's Five Forces Analysis you'll receive immediately after purchase—no mockups or placeholders. The file is the professionally formatted, final document ready for download and use the moment you buy. What you see here is precisely what will be available to you instantly after payment.

Description

Don't Miss the Bigger Picture

Solon Eiendom faces moderate supplier leverage, concentrated buyers in key segments, and rising competitive pressure from new mixed‑use developers, while substitutes and regulatory shifts create strategic uncertainty. This snapshot highlights core risks and advantages. Want full force-by-force ratings, visuals and actionable strategy? Unlock the complete Porter's Five Forces Analysis for a consultant-grade, data-driven breakdown tailored to Solon Eiendom.

Suppliers Bargaining Power

Constrained land sellers

Prime plots in Greater Oslo are scarce, controlled mainly by municipalities, institutions and a few private owners; the metro area surpassed 1.7 million residents in 2024, intensifying land demand. Limited rezoning options raise landholder leverage on price and terms. Solon mitigates this with early-stage option agreements and JV partnerships. Persistent bidding pressure keeps acquisition costs elevated.

Contractors and trades

Construction capacity in Norway is cyclical and persistent tightness in skilled trades—highlighted by SSB reporting high vacancy rates in construction in 2024—boosts contractor bargaining power.

Framework agreements and multi-sourcing temper headline rates, but complex urban projects narrow viable vendors and sustain premiums.

Cost inflation and index-linked contracts shift more risk onto developers, while strict quality and HSE standards limit substitutions.

Building materials volatility

Materials like timber, steel and HVAC components face global price swings and logistics risks; HRC steel spot prices swung roughly ±25% in 2023–24 and softwood lumber futures moved about 30% over the same period, amplifying supplier leverage during spikes and bottlenecks. Hedging, standardized specs and bulk purchasing mitigate shocks, but bespoke urban design limits full standardization. Green material requirements narrow approved suppliers and raise procurement premiums by double digits in many projects.

Design and engineering firms

Architects and planners with urban regeneration expertise are scarce in 2024, increasing their leverage over fees and delivery schedules; Solon’s place-making focus raises dependency on these firms. Long-term partnerships can align incentives but capacity constraints still delay permits and project starts. Premium, award-winning designs can lift selling prices while raising upfront development costs.

- Specialist scarcity → higher fees

- Dependency on place-making firms

- Long-term ties mitigate misalignment

- Capacity limits → permit/start delays

- Premium design → higher sales value and costs

Municipal permitting bodies

Municipal permitting bodies function as de facto suppliers by controlling zoning, density and compliance with TEK17, giving municipalities decisive leverage over project viability and timing. Proactive stakeholder engagement reduces friction but cannot override statutory powers under the Planning and Building Act; permit delays raise holding periods and financing costs.

- Regulatory control: zoning, TEK17

- Leverage: approvals determine density

- Mitigation: stakeholder engagement helps

- Risk: delays increase holding/financing costs

Oslo land scarcity, rezoning limits and HRC ±25%, lumber ~30% swings squeeze developers

Scarce Greater Oslo land (metro >1.7M in 2024) and limited rezoning give suppliers strong price leverage. Tight construction labor (SSB: high vacancy in 2024) and specialist architects raise contracting fees and schedule risk. Material swings (HRC ±25% 2023–24; lumber ~30%) and municipal permitting control further shift cost/timing risk to developers.

| Factor | 2024 metric |

|---|---|

| Population (Greater Oslo) | >1.7M |

| HRC steel swing | ±25% (2023–24) |

| Lumber futures | ~30% (2023–24) |

| Construction vacancies | High (SSB 2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Solon Eiendom that uncovers key competitive drivers, buyer and supplier power, entry barriers, substitutes, and emerging disruptive threats to its market position, with strategic commentary for investors and management.

One-sheet Porter's Five Forces for Solon Eiendom that pinpoints competitive pressures and opportunities, letting you quickly allocate defenses and growth actions and drop the chart directly into decks or stress-test scenarios.

Customers Bargaining Power

Price-sensitive homebuyers

End-buyers remain highly price-sensitive to mortgage costs, with Norwegian mortgage rates averaging around 4.5% in 2024, boosting bargaining power in downturns. Developers counter with incentives, flexible unit mix and staged pricing to stimulate uptake. In upcycles Oslo scarcity and low central inventory reduce buyer leverage, while strong brand trust and proven build quality allow Solon Eiendom to command premiums and face less price pushback.

High transparency market

Norway’s 98% internet penetration and Finn.no’s ~2.5 million monthly users in 2024 make comparisons across newbuilds and existing stock straightforward, boosting buyer leverage on features and pricing. Transparent comps and public transaction data shorten negotiation cycles and intensify price pressure at launch. Strong digital listings raise competition, while location, amenities and sustainability remain key differentiation levers.

Shift to sustainability

Buyers increasingly demand energy efficiency, low operating costs and green certifications; buildings account for about 40% of EU energy use (2024), raising expectations that can compress margins if ESG premiums are resisted. Market data in 2024 showed green-certified assets delivering roughly a 4% rent premium and ~6% value uplift, expanding the buyer pool and supporting pricing. Emphasizing long-term savings — operational cuts of 10–25% on energy bills in efficient buildings — helps justify higher upfront prices.

Investor and bulk buyers

Investor and bulk buyers (as of 2024) leverage scale to secure bulk discounts and bespoke terms, de-risking projects while compressing per-unit margins. Pre-sales to institutional investors often unlock financing and accelerate construction starts. Maintaining a mix of retail and bulk sales preserves Solon Eiendom's overall pricing power and margin flexibility.

- Bulk buyers: negotiated terms, lower unit margin

- Pre-sales: enable financing, earlier starts

- Mix strategy: balance pricing power

Alternatives in resale market

Norway's robust secondary market, accounting for roughly 85–90% of home transactions in 2024, offers immediate occupancy across diverse locations and raises buyer bargaining power. When newbuild premiums widen to about 5–12%, buyers often switch to existing homes, while renovation-ready units compete on total cost of ownership. Emphasizing 10-year warranty, energy efficiency and modern specs helps defend newbuild value.

- Secondary market share: ~85–90% (2024)

- Newbuild premium pressure: 5–12%

- Defensive levers: 10-year warranty; energy efficiency; modern specs

Buyers gain leverage as mortgages ~4.5%, newbuild premium squeezed; green assets uplift

Buyers hold strong price leverage when mortgage rates hit ~4.5% (2024) and can compare listings via Finn.no (~2.5M monthly users), pressuring newbuild premiums (5–12%). Secondary market share ~85–90% (2024) raises switching risk; green-certified assets show ~4% rent premium / ~6% value uplift. Bulk/investor pre-sales compress per-unit margins but enable financing.

| Metric | 2024 |

|---|---|

| Mortgage rate | ~4.5% |

| Finn.no users | ~2.5M/mo |

| Secondary market share | 85–90% |

| Green premium | Rent +4% / Value +6% |

| Newbuild premium | 5–12% |

Preview Before You Purchase

Solon Eiendom Porter's Five Forces Analysis

This preview shows the exact Solon Eiendom Porter's Five Forces Analysis you'll receive immediately after purchase—no mockups or placeholders. The file is the professionally formatted, final document ready for download and use the moment you buy. What you see here is precisely what will be available to you instantly after payment.