Solus Advanced Materials Porter's Five Forces Analysis

Don't Miss the Bigger Picture

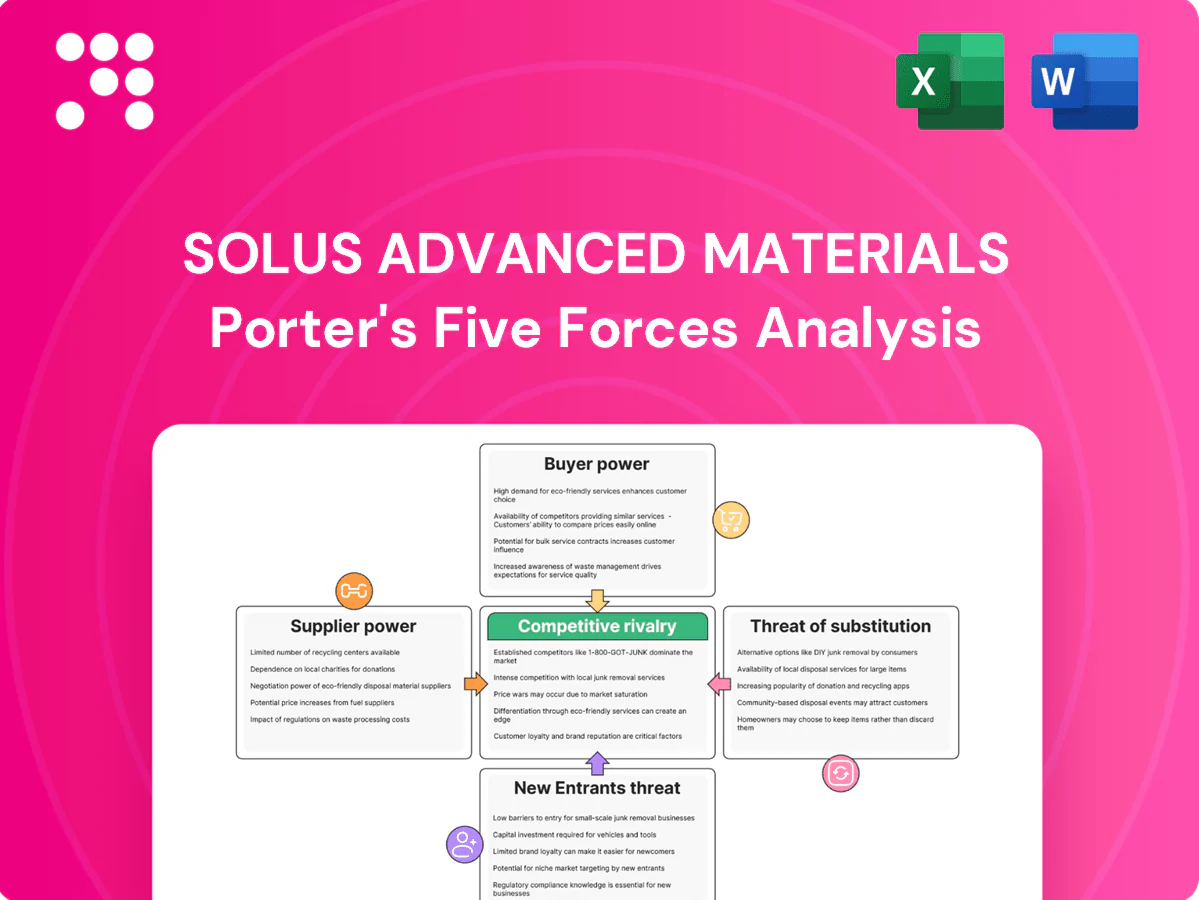

Solus Advanced Materials faces moderate supplier power due to specialized inputs, while buyer concentration and price sensitivity heighten competitive pressure; niche applications and IP offer some protection against substitutes and new entrants. Rivalry is intense as firms scale for battery-materials demand, making strategic positioning critical. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Solus Advanced Materials.

Suppliers Bargaining Power

Concentrated copper and chemical inputs

Core inputs—LME-priced copper cathodes (2024 avg ~US$9,500/t), high-purity chemicals, solvents and specialty additives—are often sourced from a small pool of qualified suppliers, giving suppliers leverage. Concentration and commodity volatility have compressed gross margins by an estimated 200–500 bps in tight cycles. Long-term contracts and hedging partially mitigate exposure, but shocks cascade into pricing. Dual-sourcing and recycling/scrap blending (offsetting ~10–20% of copper feed) materially reduce risk.

High purity and qualification requirements

Solus requires ultra-high purity inputs (commonly 5N–7N, i.e., 99.999%–99.99999%) to meet battery-grade and semiconductor specs, which narrows the qualified supplier pool. Rigorous qualification and audit processes create switching friction and increase supplier leverage. Downstream revalidation often extends timelines by 6–12 months, and this technical gatekeeping raises supplier power in niche chemistries and consumables.

Energy intensity and utilities dependence

Electrodeposited copper foil and advanced-materials production is highly power-intensive, with industrial electricity prices in 2024 ranging roughly $0.06–$0.15 per kWh, directly tying margins to energy markets. Regional utility tariffs and policy (capacity charges, curtailment rules) shift cost competitiveness between sites. Short-term price spikes or forced curtailments can erode margins or limit output. Onsite efficiency measures and renewable PPAs materially reduce exposure to spot-price volatility.

Equipment and maintenance OEMs

Specialized plating, rolling and surface-treatment equipment is concentrated among a small group of OEMs; as of 2024 Solus faces limited vendor choice for critical lines, raising lead-time and price sensitivity. Spare parts, service agreements and upgrades often carry premiums and can extend project timelines during capacity expansions or node transitions. Robust in-house engineering and component standardization reduce OEM bargaining leverage and contingency risk.

- Concentration: small OEM pool

- Cost impact: premium spare/service pricing

- Risk peak: during expansions/node shifts

- Mitigation: in-house engineering and standards

Logistics and geopolitical frictions

Logistics and geopolitical frictions heighten supplier power for Solus Advanced Materials: Chile and Peru supplied about 38% of global copper mine output in 2023, concentrating copper concentrate flows and raising vulnerability to port congestion, sanctions, or export restrictions that can tighten supplies and lift costs. Regionalizing supply chains improves resilience but often increases input prices; diversification across regions lowers disruption exposure.

- Chile+Peru ~38% of copper mine output (2023)

- Port congestion, sanctions, export curbs → tighter supply/higher costs

- Regionalization = resilience at higher price

- Diversification reduces disruption risk

High copper supply power: US$9.5k/t, OEM concentration, Chile+Peru 38%

Suppliers hold moderate-to-high power: 2024 LME copper avg ~US$9,500/t, 5N–7N purity needs, 6–12 month requalification, and energy $0.06–$0.15/kWh raise switching costs. Dual-sourcing and recycling (offset ~10–20%) mitigate risk; OEM concentration and Chile+Peru ~38% of copper output sustain vulnerability.

| Metric | 2024/2023 |

|---|---|

| LME copper | ~US$9,500/t (2024) |

| Energy | $0.06–$0.15/kWh (2024) |

| Chile+Peru | ~38% (2023) |

| Recycling offset | 10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for Solus Advanced Materials that uncovers competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifies disruptive forces and industry-specific entry barriers to inform pricing, strategy, and investment decisions; fully editable for integration into reports, pitch decks, or academic work.

A compact one-sheet Porter's Five Forces for Solus Advanced Materials—visual radar and customizable pressure levels that quickly pinpoint competitive risks and opportunities, easing boardroom decision-making and investor briefings.

Customers Bargaining Power

Consolidated EV and electronics customers

Major battery makers and electronics OEMs are few and large: CATL held about 34% of global EV battery capacity in 2024 (SNE Research) and the top five battery suppliers account for roughly three-quarters of capacity, giving them strong bargaining leverage to demand volume discounts and favorable terms. Their multi‑year capacity plans directly set Solus utilization and pricing, increasing customer concentration and dependency risk for Solus Advanced Materials.

Stringent specs and long qualifications

Buyers demand tight tolerances (thickness, tensile, profile, impurities) and rigorous audits, with qualification cycles typically 12–24 months that raise switching costs but lock in standards; once qualified buyers can pressure price at renewals (commonly 5–10% downward leverage), while co-development partnerships embed Solus into product roadmaps and help rebalance bargaining power.

Price sensitivity amid battery cost targets

Pack-level cost targets — industry focus on a $100/kWh target by 2024 — cascade pressure down to copper foil and precursor materials, compressing supplier margins. Buyers benchmark aggressively against Chinese and regional suppliers to extract price concessions. Index-linked contracts transfer some raw-material moves but leave suppliers exposed to short-term volatility. Value-add features must show measurable TCO savings to defend premium pricing.

Multi-sourcing and localization demands

OEMs increasingly pursue dual- and tri-sourcing to de-risk supply, reducing reliance on single suppliers and intensifying competition in RFPs. 2024 localization drivers such as the US Inflation Reduction Act tax credit (up to $7,500 per vehicle) and similar national incentives shift volumes regionally regardless of legacy ties. Solus must align its manufacturing footprint with customer factory geographies to retain share.

- Dual/tri-sourcing raises RFP competition

- IRA $7,500 credit shifts North American volumes

- Localization can override legacy supplier relationships

- Solus needs footprint alignment with OEM plants

Quality and delivery penalties

Just-in-time schedules and zero-defect expectations give buyers strong leverage through penalties and chargebacks, with 2024 industry surveys showing over 70% of OEM contracts including explicit chargeback clauses.

Minor defects can trigger large downstream scrap costs, forcing suppliers to absorb risk; vendor scorecards—weighted heavily on quality—directly affect future awards, so robust QA and traceability are critical to retain share and terms.

- JIT/zero-defect clauses: >70% adoption (2024)

- Chargebacks: primary supplier cost driver

- Scorecards determine award eligibility

- QA/traceability required to mitigate scrap risk

OEM leverage, JIT clauses & IRA localization hit batteries; top-5 ≈75%

Major OEMs and top-five battery suppliers (≈75% capacity; CATL ≈34% in 2024) wield strong leverage, forcing volume discounts and strict terms. Qualification cycles (12–24 months) raise switching costs but allow price pressure at renewals (~5–10%). JIT/zero-defect clauses (>70% of contracts in 2024) create chargebacks and high quality demands. IRA-driven localization (up to $7,500 EV credit) shifts volumes regionally, increasing RFP competition.

| Metric | Value (2024) |

|---|---|

| Top-5 battery share | ≈75% |

| CATL share | ≈34% |

| Qualification cycle | 12–24 months |

| Renewal price pressure | 5–10% |

| JIT/zero-defect adoption | >70% |

| IRA EV credit | up to $7,500 |

Preview Before You Purchase

Solus Advanced Materials Porter's Five Forces Analysis

This preview shows the exact Solus Advanced Materials Porter's Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is complete, professionally formatted, and ready for immediate download and use. What you see is precisely the deliverable provided upon payment.

Don't Miss the Bigger Picture

Solus Advanced Materials faces moderate supplier power due to specialized inputs, while buyer concentration and price sensitivity heighten competitive pressure; niche applications and IP offer some protection against substitutes and new entrants. Rivalry is intense as firms scale for battery-materials demand, making strategic positioning critical. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Solus Advanced Materials.

Suppliers Bargaining Power

Concentrated copper and chemical inputs

Core inputs—LME-priced copper cathodes (2024 avg ~US$9,500/t), high-purity chemicals, solvents and specialty additives—are often sourced from a small pool of qualified suppliers, giving suppliers leverage. Concentration and commodity volatility have compressed gross margins by an estimated 200–500 bps in tight cycles. Long-term contracts and hedging partially mitigate exposure, but shocks cascade into pricing. Dual-sourcing and recycling/scrap blending (offsetting ~10–20% of copper feed) materially reduce risk.

High purity and qualification requirements

Solus requires ultra-high purity inputs (commonly 5N–7N, i.e., 99.999%–99.99999%) to meet battery-grade and semiconductor specs, which narrows the qualified supplier pool. Rigorous qualification and audit processes create switching friction and increase supplier leverage. Downstream revalidation often extends timelines by 6–12 months, and this technical gatekeeping raises supplier power in niche chemistries and consumables.

Energy intensity and utilities dependence

Electrodeposited copper foil and advanced-materials production is highly power-intensive, with industrial electricity prices in 2024 ranging roughly $0.06–$0.15 per kWh, directly tying margins to energy markets. Regional utility tariffs and policy (capacity charges, curtailment rules) shift cost competitiveness between sites. Short-term price spikes or forced curtailments can erode margins or limit output. Onsite efficiency measures and renewable PPAs materially reduce exposure to spot-price volatility.

Equipment and maintenance OEMs

Specialized plating, rolling and surface-treatment equipment is concentrated among a small group of OEMs; as of 2024 Solus faces limited vendor choice for critical lines, raising lead-time and price sensitivity. Spare parts, service agreements and upgrades often carry premiums and can extend project timelines during capacity expansions or node transitions. Robust in-house engineering and component standardization reduce OEM bargaining leverage and contingency risk.

- Concentration: small OEM pool

- Cost impact: premium spare/service pricing

- Risk peak: during expansions/node shifts

- Mitigation: in-house engineering and standards

Logistics and geopolitical frictions

Logistics and geopolitical frictions heighten supplier power for Solus Advanced Materials: Chile and Peru supplied about 38% of global copper mine output in 2023, concentrating copper concentrate flows and raising vulnerability to port congestion, sanctions, or export restrictions that can tighten supplies and lift costs. Regionalizing supply chains improves resilience but often increases input prices; diversification across regions lowers disruption exposure.

- Chile+Peru ~38% of copper mine output (2023)

- Port congestion, sanctions, export curbs → tighter supply/higher costs

- Regionalization = resilience at higher price

- Diversification reduces disruption risk

High copper supply power: US$9.5k/t, OEM concentration, Chile+Peru 38%

Suppliers hold moderate-to-high power: 2024 LME copper avg ~US$9,500/t, 5N–7N purity needs, 6–12 month requalification, and energy $0.06–$0.15/kWh raise switching costs. Dual-sourcing and recycling (offset ~10–20%) mitigate risk; OEM concentration and Chile+Peru ~38% of copper output sustain vulnerability.

| Metric | 2024/2023 |

|---|---|

| LME copper | ~US$9,500/t (2024) |

| Energy | $0.06–$0.15/kWh (2024) |

| Chile+Peru | ~38% (2023) |

| Recycling offset | 10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for Solus Advanced Materials that uncovers competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifies disruptive forces and industry-specific entry barriers to inform pricing, strategy, and investment decisions; fully editable for integration into reports, pitch decks, or academic work.

A compact one-sheet Porter's Five Forces for Solus Advanced Materials—visual radar and customizable pressure levels that quickly pinpoint competitive risks and opportunities, easing boardroom decision-making and investor briefings.

Customers Bargaining Power

Consolidated EV and electronics customers

Major battery makers and electronics OEMs are few and large: CATL held about 34% of global EV battery capacity in 2024 (SNE Research) and the top five battery suppliers account for roughly three-quarters of capacity, giving them strong bargaining leverage to demand volume discounts and favorable terms. Their multi‑year capacity plans directly set Solus utilization and pricing, increasing customer concentration and dependency risk for Solus Advanced Materials.

Stringent specs and long qualifications

Buyers demand tight tolerances (thickness, tensile, profile, impurities) and rigorous audits, with qualification cycles typically 12–24 months that raise switching costs but lock in standards; once qualified buyers can pressure price at renewals (commonly 5–10% downward leverage), while co-development partnerships embed Solus into product roadmaps and help rebalance bargaining power.

Price sensitivity amid battery cost targets

Pack-level cost targets — industry focus on a $100/kWh target by 2024 — cascade pressure down to copper foil and precursor materials, compressing supplier margins. Buyers benchmark aggressively against Chinese and regional suppliers to extract price concessions. Index-linked contracts transfer some raw-material moves but leave suppliers exposed to short-term volatility. Value-add features must show measurable TCO savings to defend premium pricing.

Multi-sourcing and localization demands

OEMs increasingly pursue dual- and tri-sourcing to de-risk supply, reducing reliance on single suppliers and intensifying competition in RFPs. 2024 localization drivers such as the US Inflation Reduction Act tax credit (up to $7,500 per vehicle) and similar national incentives shift volumes regionally regardless of legacy ties. Solus must align its manufacturing footprint with customer factory geographies to retain share.

- Dual/tri-sourcing raises RFP competition

- IRA $7,500 credit shifts North American volumes

- Localization can override legacy supplier relationships

- Solus needs footprint alignment with OEM plants

Quality and delivery penalties

Just-in-time schedules and zero-defect expectations give buyers strong leverage through penalties and chargebacks, with 2024 industry surveys showing over 70% of OEM contracts including explicit chargeback clauses.

Minor defects can trigger large downstream scrap costs, forcing suppliers to absorb risk; vendor scorecards—weighted heavily on quality—directly affect future awards, so robust QA and traceability are critical to retain share and terms.

- JIT/zero-defect clauses: >70% adoption (2024)

- Chargebacks: primary supplier cost driver

- Scorecards determine award eligibility

- QA/traceability required to mitigate scrap risk

OEM leverage, JIT clauses & IRA localization hit batteries; top-5 ≈75%

Major OEMs and top-five battery suppliers (≈75% capacity; CATL ≈34% in 2024) wield strong leverage, forcing volume discounts and strict terms. Qualification cycles (12–24 months) raise switching costs but allow price pressure at renewals (~5–10%). JIT/zero-defect clauses (>70% of contracts in 2024) create chargebacks and high quality demands. IRA-driven localization (up to $7,500 EV credit) shifts volumes regionally, increasing RFP competition.

| Metric | Value (2024) |

|---|---|

| Top-5 battery share | ≈75% |

| CATL share | ≈34% |

| Qualification cycle | 12–24 months |

| Renewal price pressure | 5–10% |

| JIT/zero-defect adoption | >70% |

| IRA EV credit | up to $7,500 |

Preview Before You Purchase

Solus Advanced Materials Porter's Five Forces Analysis

This preview shows the exact Solus Advanced Materials Porter's Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is complete, professionally formatted, and ready for immediate download and use. What you see is precisely the deliverable provided upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Solus Advanced Materials faces moderate supplier power due to specialized inputs, while buyer concentration and price sensitivity heighten competitive pressure; niche applications and IP offer some protection against substitutes and new entrants. Rivalry is intense as firms scale for battery-materials demand, making strategic positioning critical. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights tailored to Solus Advanced Materials.

Suppliers Bargaining Power

Concentrated copper and chemical inputs

Core inputs—LME-priced copper cathodes (2024 avg ~US$9,500/t), high-purity chemicals, solvents and specialty additives—are often sourced from a small pool of qualified suppliers, giving suppliers leverage. Concentration and commodity volatility have compressed gross margins by an estimated 200–500 bps in tight cycles. Long-term contracts and hedging partially mitigate exposure, but shocks cascade into pricing. Dual-sourcing and recycling/scrap blending (offsetting ~10–20% of copper feed) materially reduce risk.

High purity and qualification requirements

Solus requires ultra-high purity inputs (commonly 5N–7N, i.e., 99.999%–99.99999%) to meet battery-grade and semiconductor specs, which narrows the qualified supplier pool. Rigorous qualification and audit processes create switching friction and increase supplier leverage. Downstream revalidation often extends timelines by 6–12 months, and this technical gatekeeping raises supplier power in niche chemistries and consumables.

Energy intensity and utilities dependence

Electrodeposited copper foil and advanced-materials production is highly power-intensive, with industrial electricity prices in 2024 ranging roughly $0.06–$0.15 per kWh, directly tying margins to energy markets. Regional utility tariffs and policy (capacity charges, curtailment rules) shift cost competitiveness between sites. Short-term price spikes or forced curtailments can erode margins or limit output. Onsite efficiency measures and renewable PPAs materially reduce exposure to spot-price volatility.

Equipment and maintenance OEMs

Specialized plating, rolling and surface-treatment equipment is concentrated among a small group of OEMs; as of 2024 Solus faces limited vendor choice for critical lines, raising lead-time and price sensitivity. Spare parts, service agreements and upgrades often carry premiums and can extend project timelines during capacity expansions or node transitions. Robust in-house engineering and component standardization reduce OEM bargaining leverage and contingency risk.

- Concentration: small OEM pool

- Cost impact: premium spare/service pricing

- Risk peak: during expansions/node shifts

- Mitigation: in-house engineering and standards

Logistics and geopolitical frictions

Logistics and geopolitical frictions heighten supplier power for Solus Advanced Materials: Chile and Peru supplied about 38% of global copper mine output in 2023, concentrating copper concentrate flows and raising vulnerability to port congestion, sanctions, or export restrictions that can tighten supplies and lift costs. Regionalizing supply chains improves resilience but often increases input prices; diversification across regions lowers disruption exposure.

- Chile+Peru ~38% of copper mine output (2023)

- Port congestion, sanctions, export curbs → tighter supply/higher costs

- Regionalization = resilience at higher price

- Diversification reduces disruption risk

High copper supply power: US$9.5k/t, OEM concentration, Chile+Peru 38%

Suppliers hold moderate-to-high power: 2024 LME copper avg ~US$9,500/t, 5N–7N purity needs, 6–12 month requalification, and energy $0.06–$0.15/kWh raise switching costs. Dual-sourcing and recycling (offset ~10–20%) mitigate risk; OEM concentration and Chile+Peru ~38% of copper output sustain vulnerability.

| Metric | 2024/2023 |

|---|---|

| LME copper | ~US$9,500/t (2024) |

| Energy | $0.06–$0.15/kWh (2024) |

| Chile+Peru | ~38% (2023) |

| Recycling offset | 10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for Solus Advanced Materials that uncovers competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and identifies disruptive forces and industry-specific entry barriers to inform pricing, strategy, and investment decisions; fully editable for integration into reports, pitch decks, or academic work.

A compact one-sheet Porter's Five Forces for Solus Advanced Materials—visual radar and customizable pressure levels that quickly pinpoint competitive risks and opportunities, easing boardroom decision-making and investor briefings.

Customers Bargaining Power

Consolidated EV and electronics customers

Major battery makers and electronics OEMs are few and large: CATL held about 34% of global EV battery capacity in 2024 (SNE Research) and the top five battery suppliers account for roughly three-quarters of capacity, giving them strong bargaining leverage to demand volume discounts and favorable terms. Their multi‑year capacity plans directly set Solus utilization and pricing, increasing customer concentration and dependency risk for Solus Advanced Materials.

Stringent specs and long qualifications

Buyers demand tight tolerances (thickness, tensile, profile, impurities) and rigorous audits, with qualification cycles typically 12–24 months that raise switching costs but lock in standards; once qualified buyers can pressure price at renewals (commonly 5–10% downward leverage), while co-development partnerships embed Solus into product roadmaps and help rebalance bargaining power.

Price sensitivity amid battery cost targets

Pack-level cost targets — industry focus on a $100/kWh target by 2024 — cascade pressure down to copper foil and precursor materials, compressing supplier margins. Buyers benchmark aggressively against Chinese and regional suppliers to extract price concessions. Index-linked contracts transfer some raw-material moves but leave suppliers exposed to short-term volatility. Value-add features must show measurable TCO savings to defend premium pricing.

Multi-sourcing and localization demands

OEMs increasingly pursue dual- and tri-sourcing to de-risk supply, reducing reliance on single suppliers and intensifying competition in RFPs. 2024 localization drivers such as the US Inflation Reduction Act tax credit (up to $7,500 per vehicle) and similar national incentives shift volumes regionally regardless of legacy ties. Solus must align its manufacturing footprint with customer factory geographies to retain share.

- Dual/tri-sourcing raises RFP competition

- IRA $7,500 credit shifts North American volumes

- Localization can override legacy supplier relationships

- Solus needs footprint alignment with OEM plants

Quality and delivery penalties

Just-in-time schedules and zero-defect expectations give buyers strong leverage through penalties and chargebacks, with 2024 industry surveys showing over 70% of OEM contracts including explicit chargeback clauses.

Minor defects can trigger large downstream scrap costs, forcing suppliers to absorb risk; vendor scorecards—weighted heavily on quality—directly affect future awards, so robust QA and traceability are critical to retain share and terms.

- JIT/zero-defect clauses: >70% adoption (2024)

- Chargebacks: primary supplier cost driver

- Scorecards determine award eligibility

- QA/traceability required to mitigate scrap risk

OEM leverage, JIT clauses & IRA localization hit batteries; top-5 ≈75%

Major OEMs and top-five battery suppliers (≈75% capacity; CATL ≈34% in 2024) wield strong leverage, forcing volume discounts and strict terms. Qualification cycles (12–24 months) raise switching costs but allow price pressure at renewals (~5–10%). JIT/zero-defect clauses (>70% of contracts in 2024) create chargebacks and high quality demands. IRA-driven localization (up to $7,500 EV credit) shifts volumes regionally, increasing RFP competition.

| Metric | Value (2024) |

|---|---|

| Top-5 battery share | ≈75% |

| CATL share | ≈34% |

| Qualification cycle | 12–24 months |

| Renewal price pressure | 5–10% |

| JIT/zero-defect adoption | >70% |

| IRA EV credit | up to $7,500 |

Preview Before You Purchase

Solus Advanced Materials Porter's Five Forces Analysis

This preview shows the exact Solus Advanced Materials Porter's Five Forces analysis you’ll receive after purchase—no placeholders or mockups. The file is complete, professionally formatted, and ready for immediate download and use. What you see is precisely the deliverable provided upon payment.