Sompo Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

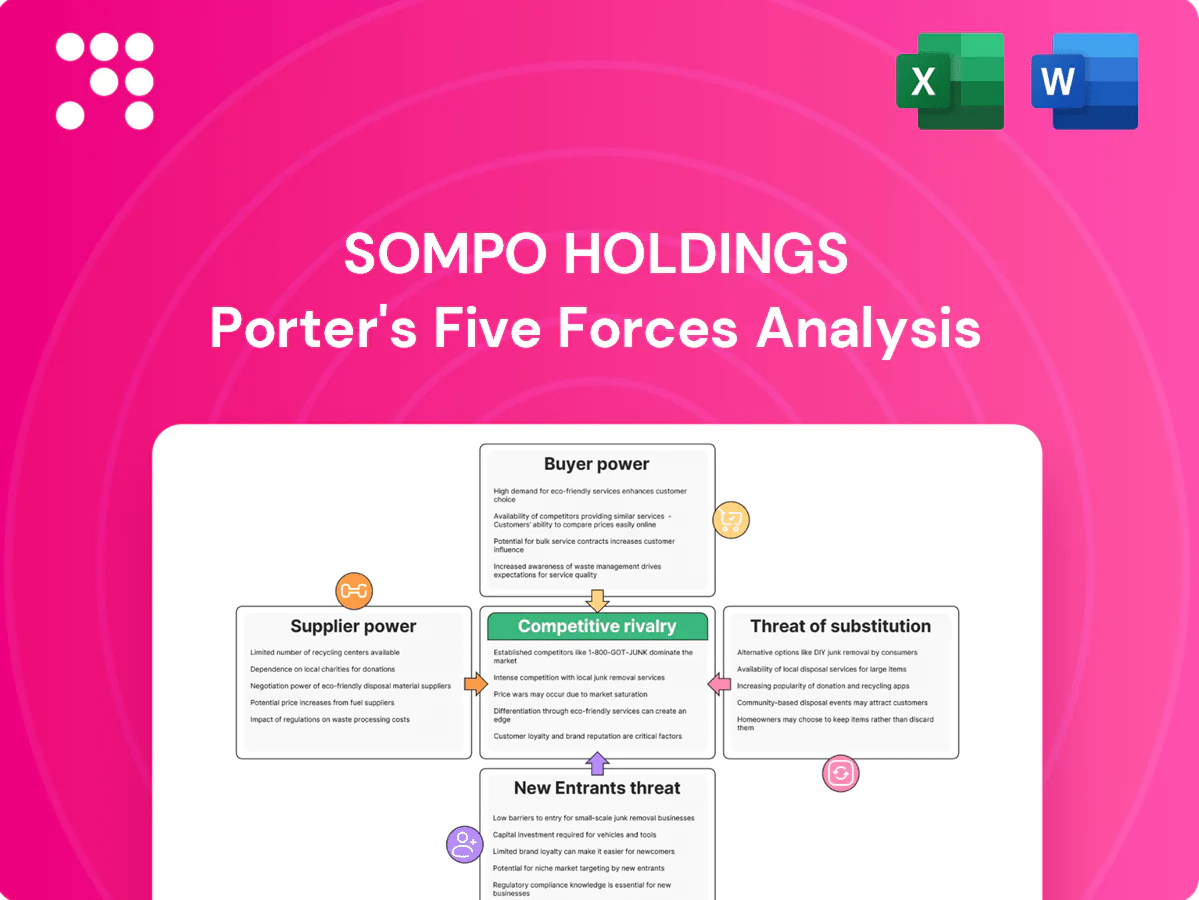

This snapshot highlights Sompo Holdings' competitive landscape, showing buyer and supplier power, rivalry intensity, and threats from new entrants and substitutes. Our full Porter's Five Forces Analysis breaks down each force with ratings, visuals, and strategic implications tailored to Sompo. Unlock the complete report to inform investments, strategy, or presentations.

Suppliers Bargaining Power

Concentrated reinsurance partners

Sompo relies on a relatively concentrated set of global reinsurers for catastrophe risk transfer, giving counterparties pricing and terms leverage particularly after large-loss years like 2023 when renewal tightenings were widely reported.

Sompo’s use of multi-year treaties and its scale partially offsets that leverage, while cyclical market swings mean negotiability can improve or deteriorate at successive renewals.

Critical data and modeling vendors

Catastrophe models, credit data and telematics/analytics platforms are concentrated—top three catastrophe model vendors (RMS, AIR, CoreLogic) cover roughly 70–80% of market while credit bureaus (Experian, Equifax, TransUnion) dominate pricing, creating supplier leverage. High switching costs and rigorous model validation make vendors sticky and directly affect pricing adequacy and capital allocation. Vendor choices can shift loss estimates and capital by tens of percent in stress scenarios. Investing in in‑house analytics (> $50m over several years) can gradually rebalance power.

IT infrastructure and cloud dependence

Core policy systems and cloud platforms for insurers are concentrated: in 2024 AWS held ~32% of public cloud IaaS/PaaS, Microsoft Azure ~22% and Google Cloud ~10%, increasing supplier leverage over Sompo. Long implementation cycles—commonly 18–24 months for core policy integrations—and high integration complexity create lock-in. Outages and cyber incidents (notable 2023–24 cloud outages) raise supplier criticality; multi-cloud and modular architectures can reduce bargaining power.

Claims repair and medical networks

Claims repair shops, medical providers and care facilities materially influence Sompo’s claims cost and cycle time through pricing, repair capacity and treatment availability, and in tight local markets providers can push rates or limit service levels. Network agreements, negotiated rate cards and insurer steerage lower supplier leverage and shorten cycles by directing volume to contracted providers. Sompo’s owned nursing care operations provide upstream supply control in aged-care services.

- Auto repair shops: local capacity drives rate negotiation

- Medical providers: affect severity and treatment duration

- Network agreements: reduce supplier bargaining power

- Sompo nursing care footprint: secures aged-care supply

Distribution intermediaries as quasi-suppliers

Distribution intermediaries—brokers, agents and bancassurance—function as quasi-suppliers by bringing customers; large brokers aggregate corporate demand and can push commission rates and contract terms.

Sompo’s shift to direct and digital channels is reducing dependence, though scaling takes time; a balanced channel mix weakens intermediary bargaining power and limits single-channel leverage.

- Brokers: aggregate demand, influence commissions

- Agents: customer reach, retention role

- Bancassurance: bank-led customer supply

- Direct/digital: lowers dependency but needs scale

Insurer faces reinsurer, cat-model and cloud concentration; analytics and treaties soften impact

Sompo faces supplier leverage from concentrated reinsurers and catastrophe-model vendors (RMS/AIR/CoreLogic ~70–80% share) and cloud providers (AWS ~32%, Azure ~22%, GCP ~10% in 2024), which can shift pricing and capital needs after large-loss years.

Sompo’s scale, multi-year treaties and in-house analytics investments (> $50m) partially offset power, while direct/digital channels and network agreements reduce broker and provider influence.

| Supplier | Concentration | 2024 impact |

|---|---|---|

| Cat models | RMS/AIR/CoreLogic ~70–80% | Alters loss estimates, capital |

| Cloud | AWS ~32%, Azure ~22%, GCP ~10% | Vendor lock‑in, outage risk |

| Reinsurers | Concentrated | Renewal pricing volatility |

What is included in the product

Concise Porter's Five Forces overview for Sompo Holdings, assessing competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and highlighting industry disruptors and entry barriers shaping its profitability.

A concise one-sheet Porter’s Five Forces for Sompo Holdings—visualize insurer-specific threats (regulation, reinsurers, tech entrants) with editable pressure levels and a ready-to-use radar chart for decks.

Customers Bargaining Power

Large corporate clients with scale

Large corporates buy sizable, complex programs that enable aggressive tendering; Sompo faces benchmarked bids and growing use of captives—Marsh reported captives managed roughly $97 billion of risk capital in 2024—forcing carriers to match terms not just price. Customization needs shift negotiations toward service excellence and tailored capacity, tempering pure price competition. Multi-year/global renewals can stabilize pricing but remain regularly contestable across markets.

Broker-driven price discovery

Global broker-driven placements increase transparency and price pressure, with the largest brokers handling roughly half of major commercial placements, intensifying buyer leverage through analytics that frame coverage comparability. Brokers’ playbooks push competitive bids and lower margins for carriers, yet broker preferences still reward insurers demonstrating underwriting expertise and superior claims service. In specialty lines, Sompo’s differentiated capabilities can soften buyer power by limiting true comparators.

Retail customers’ low switching costs

Retail personal-lines customers can switch easily at renewal, with aggregators handling roughly 25% of online insurance quotes in Japan in 2024, boosting comparison-driven churn. High price sensitivity in auto and fire lines compresses margins, contributing to reported underwriting margin volatility of several hundred basis points in 2024. Sompo’s strong brand and claims reputation helps curb churn, while bundling and loyalty programs further reduce buyer power.

Demand for digital convenience

Customers demand seamless digital onboarding, endorsements, and claims; poor UX raises churn and bargaining power, while Sompo's scale (about JPY 2.8 trillion premiums in FY2023) lets it invest in digital journeys and straight-through processing to blunt price sensitivity. Data-driven personalization increases perceived value and retention, lowering buyer leverage.

- Seamless onboarding reduces churn

- STP lowers price sensitivity

- Personalization raises perceived value

Life and nursing care client expectations

Policyholders and families weigh service quality and long-term reliability heavily; Sompo Holdings leverages SOMPO Care and group nursing platforms to address this amid Japan’s 65+ population ~29.1% (OECD 2023). Transparency on fees and benefits materially affects perceived fairness, while agent advice quality directly shapes purchase and retention decisions. Integrated care-insurance offerings increase switching costs and customer loyalty.

- service-quality focus

- transparency impacts fairness

- agent advice drives bargaining

- integrated care locks loyalty

Insurer must match terms vs captives $97B, brokers ~50%

Large corporates use captives (~$97B risk capital in 2024) and brokers (~50% of major placements) to push benchmarked bids; Sompo must match terms and service, not just price. Retail churn rises via aggregators (~25% online quotes Japan 2024); Sompo’s JPY 2.8T premiums (FY2023) and digital/STP investments offset ~300bps 2024 underwriting volatility.

| Metric | Value |

|---|---|

| Captives (2024) | $97B |

| Brokers share | ~50% |

| Aggregators Japan (2024) | ~25% |

| Sompo premiums (FY2023) | JPY 2.8T |

| Underwriting vol (2024) | ~300bps |

What You See Is What You Get

Sompo Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sompo Holdings you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written and ready for download and use the moment you buy. You're viewing the final deliverable.

Don't Miss the Bigger Picture

This snapshot highlights Sompo Holdings' competitive landscape, showing buyer and supplier power, rivalry intensity, and threats from new entrants and substitutes. Our full Porter's Five Forces Analysis breaks down each force with ratings, visuals, and strategic implications tailored to Sompo. Unlock the complete report to inform investments, strategy, or presentations.

Suppliers Bargaining Power

Concentrated reinsurance partners

Sompo relies on a relatively concentrated set of global reinsurers for catastrophe risk transfer, giving counterparties pricing and terms leverage particularly after large-loss years like 2023 when renewal tightenings were widely reported.

Sompo’s use of multi-year treaties and its scale partially offsets that leverage, while cyclical market swings mean negotiability can improve or deteriorate at successive renewals.

Critical data and modeling vendors

Catastrophe models, credit data and telematics/analytics platforms are concentrated—top three catastrophe model vendors (RMS, AIR, CoreLogic) cover roughly 70–80% of market while credit bureaus (Experian, Equifax, TransUnion) dominate pricing, creating supplier leverage. High switching costs and rigorous model validation make vendors sticky and directly affect pricing adequacy and capital allocation. Vendor choices can shift loss estimates and capital by tens of percent in stress scenarios. Investing in in‑house analytics (> $50m over several years) can gradually rebalance power.

IT infrastructure and cloud dependence

Core policy systems and cloud platforms for insurers are concentrated: in 2024 AWS held ~32% of public cloud IaaS/PaaS, Microsoft Azure ~22% and Google Cloud ~10%, increasing supplier leverage over Sompo. Long implementation cycles—commonly 18–24 months for core policy integrations—and high integration complexity create lock-in. Outages and cyber incidents (notable 2023–24 cloud outages) raise supplier criticality; multi-cloud and modular architectures can reduce bargaining power.

Claims repair and medical networks

Claims repair shops, medical providers and care facilities materially influence Sompo’s claims cost and cycle time through pricing, repair capacity and treatment availability, and in tight local markets providers can push rates or limit service levels. Network agreements, negotiated rate cards and insurer steerage lower supplier leverage and shorten cycles by directing volume to contracted providers. Sompo’s owned nursing care operations provide upstream supply control in aged-care services.

- Auto repair shops: local capacity drives rate negotiation

- Medical providers: affect severity and treatment duration

- Network agreements: reduce supplier bargaining power

- Sompo nursing care footprint: secures aged-care supply

Distribution intermediaries as quasi-suppliers

Distribution intermediaries—brokers, agents and bancassurance—function as quasi-suppliers by bringing customers; large brokers aggregate corporate demand and can push commission rates and contract terms.

Sompo’s shift to direct and digital channels is reducing dependence, though scaling takes time; a balanced channel mix weakens intermediary bargaining power and limits single-channel leverage.

- Brokers: aggregate demand, influence commissions

- Agents: customer reach, retention role

- Bancassurance: bank-led customer supply

- Direct/digital: lowers dependency but needs scale

Insurer faces reinsurer, cat-model and cloud concentration; analytics and treaties soften impact

Sompo faces supplier leverage from concentrated reinsurers and catastrophe-model vendors (RMS/AIR/CoreLogic ~70–80% share) and cloud providers (AWS ~32%, Azure ~22%, GCP ~10% in 2024), which can shift pricing and capital needs after large-loss years.

Sompo’s scale, multi-year treaties and in-house analytics investments (> $50m) partially offset power, while direct/digital channels and network agreements reduce broker and provider influence.

| Supplier | Concentration | 2024 impact |

|---|---|---|

| Cat models | RMS/AIR/CoreLogic ~70–80% | Alters loss estimates, capital |

| Cloud | AWS ~32%, Azure ~22%, GCP ~10% | Vendor lock‑in, outage risk |

| Reinsurers | Concentrated | Renewal pricing volatility |

What is included in the product

Concise Porter's Five Forces overview for Sompo Holdings, assessing competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and highlighting industry disruptors and entry barriers shaping its profitability.

A concise one-sheet Porter’s Five Forces for Sompo Holdings—visualize insurer-specific threats (regulation, reinsurers, tech entrants) with editable pressure levels and a ready-to-use radar chart for decks.

Customers Bargaining Power

Large corporate clients with scale

Large corporates buy sizable, complex programs that enable aggressive tendering; Sompo faces benchmarked bids and growing use of captives—Marsh reported captives managed roughly $97 billion of risk capital in 2024—forcing carriers to match terms not just price. Customization needs shift negotiations toward service excellence and tailored capacity, tempering pure price competition. Multi-year/global renewals can stabilize pricing but remain regularly contestable across markets.

Broker-driven price discovery

Global broker-driven placements increase transparency and price pressure, with the largest brokers handling roughly half of major commercial placements, intensifying buyer leverage through analytics that frame coverage comparability. Brokers’ playbooks push competitive bids and lower margins for carriers, yet broker preferences still reward insurers demonstrating underwriting expertise and superior claims service. In specialty lines, Sompo’s differentiated capabilities can soften buyer power by limiting true comparators.

Retail customers’ low switching costs

Retail personal-lines customers can switch easily at renewal, with aggregators handling roughly 25% of online insurance quotes in Japan in 2024, boosting comparison-driven churn. High price sensitivity in auto and fire lines compresses margins, contributing to reported underwriting margin volatility of several hundred basis points in 2024. Sompo’s strong brand and claims reputation helps curb churn, while bundling and loyalty programs further reduce buyer power.

Demand for digital convenience

Customers demand seamless digital onboarding, endorsements, and claims; poor UX raises churn and bargaining power, while Sompo's scale (about JPY 2.8 trillion premiums in FY2023) lets it invest in digital journeys and straight-through processing to blunt price sensitivity. Data-driven personalization increases perceived value and retention, lowering buyer leverage.

- Seamless onboarding reduces churn

- STP lowers price sensitivity

- Personalization raises perceived value

Life and nursing care client expectations

Policyholders and families weigh service quality and long-term reliability heavily; Sompo Holdings leverages SOMPO Care and group nursing platforms to address this amid Japan’s 65+ population ~29.1% (OECD 2023). Transparency on fees and benefits materially affects perceived fairness, while agent advice quality directly shapes purchase and retention decisions. Integrated care-insurance offerings increase switching costs and customer loyalty.

- service-quality focus

- transparency impacts fairness

- agent advice drives bargaining

- integrated care locks loyalty

Insurer must match terms vs captives $97B, brokers ~50%

Large corporates use captives (~$97B risk capital in 2024) and brokers (~50% of major placements) to push benchmarked bids; Sompo must match terms and service, not just price. Retail churn rises via aggregators (~25% online quotes Japan 2024); Sompo’s JPY 2.8T premiums (FY2023) and digital/STP investments offset ~300bps 2024 underwriting volatility.

| Metric | Value |

|---|---|

| Captives (2024) | $97B |

| Brokers share | ~50% |

| Aggregators Japan (2024) | ~25% |

| Sompo premiums (FY2023) | JPY 2.8T |

| Underwriting vol (2024) | ~300bps |

What You See Is What You Get

Sompo Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sompo Holdings you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written and ready for download and use the moment you buy. You're viewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

This snapshot highlights Sompo Holdings' competitive landscape, showing buyer and supplier power, rivalry intensity, and threats from new entrants and substitutes. Our full Porter's Five Forces Analysis breaks down each force with ratings, visuals, and strategic implications tailored to Sompo. Unlock the complete report to inform investments, strategy, or presentations.

Suppliers Bargaining Power

Concentrated reinsurance partners

Sompo relies on a relatively concentrated set of global reinsurers for catastrophe risk transfer, giving counterparties pricing and terms leverage particularly after large-loss years like 2023 when renewal tightenings were widely reported.

Sompo’s use of multi-year treaties and its scale partially offsets that leverage, while cyclical market swings mean negotiability can improve or deteriorate at successive renewals.

Critical data and modeling vendors

Catastrophe models, credit data and telematics/analytics platforms are concentrated—top three catastrophe model vendors (RMS, AIR, CoreLogic) cover roughly 70–80% of market while credit bureaus (Experian, Equifax, TransUnion) dominate pricing, creating supplier leverage. High switching costs and rigorous model validation make vendors sticky and directly affect pricing adequacy and capital allocation. Vendor choices can shift loss estimates and capital by tens of percent in stress scenarios. Investing in in‑house analytics (> $50m over several years) can gradually rebalance power.

IT infrastructure and cloud dependence

Core policy systems and cloud platforms for insurers are concentrated: in 2024 AWS held ~32% of public cloud IaaS/PaaS, Microsoft Azure ~22% and Google Cloud ~10%, increasing supplier leverage over Sompo. Long implementation cycles—commonly 18–24 months for core policy integrations—and high integration complexity create lock-in. Outages and cyber incidents (notable 2023–24 cloud outages) raise supplier criticality; multi-cloud and modular architectures can reduce bargaining power.

Claims repair and medical networks

Claims repair shops, medical providers and care facilities materially influence Sompo’s claims cost and cycle time through pricing, repair capacity and treatment availability, and in tight local markets providers can push rates or limit service levels. Network agreements, negotiated rate cards and insurer steerage lower supplier leverage and shorten cycles by directing volume to contracted providers. Sompo’s owned nursing care operations provide upstream supply control in aged-care services.

- Auto repair shops: local capacity drives rate negotiation

- Medical providers: affect severity and treatment duration

- Network agreements: reduce supplier bargaining power

- Sompo nursing care footprint: secures aged-care supply

Distribution intermediaries as quasi-suppliers

Distribution intermediaries—brokers, agents and bancassurance—function as quasi-suppliers by bringing customers; large brokers aggregate corporate demand and can push commission rates and contract terms.

Sompo’s shift to direct and digital channels is reducing dependence, though scaling takes time; a balanced channel mix weakens intermediary bargaining power and limits single-channel leverage.

- Brokers: aggregate demand, influence commissions

- Agents: customer reach, retention role

- Bancassurance: bank-led customer supply

- Direct/digital: lowers dependency but needs scale

Insurer faces reinsurer, cat-model and cloud concentration; analytics and treaties soften impact

Sompo faces supplier leverage from concentrated reinsurers and catastrophe-model vendors (RMS/AIR/CoreLogic ~70–80% share) and cloud providers (AWS ~32%, Azure ~22%, GCP ~10% in 2024), which can shift pricing and capital needs after large-loss years.

Sompo’s scale, multi-year treaties and in-house analytics investments (> $50m) partially offset power, while direct/digital channels and network agreements reduce broker and provider influence.

| Supplier | Concentration | 2024 impact |

|---|---|---|

| Cat models | RMS/AIR/CoreLogic ~70–80% | Alters loss estimates, capital |

| Cloud | AWS ~32%, Azure ~22%, GCP ~10% | Vendor lock‑in, outage risk |

| Reinsurers | Concentrated | Renewal pricing volatility |

What is included in the product

Concise Porter's Five Forces overview for Sompo Holdings, assessing competitive rivalry, buyer/supplier power, threat of new entrants and substitutes, and highlighting industry disruptors and entry barriers shaping its profitability.

A concise one-sheet Porter’s Five Forces for Sompo Holdings—visualize insurer-specific threats (regulation, reinsurers, tech entrants) with editable pressure levels and a ready-to-use radar chart for decks.

Customers Bargaining Power

Large corporate clients with scale

Large corporates buy sizable, complex programs that enable aggressive tendering; Sompo faces benchmarked bids and growing use of captives—Marsh reported captives managed roughly $97 billion of risk capital in 2024—forcing carriers to match terms not just price. Customization needs shift negotiations toward service excellence and tailored capacity, tempering pure price competition. Multi-year/global renewals can stabilize pricing but remain regularly contestable across markets.

Broker-driven price discovery

Global broker-driven placements increase transparency and price pressure, with the largest brokers handling roughly half of major commercial placements, intensifying buyer leverage through analytics that frame coverage comparability. Brokers’ playbooks push competitive bids and lower margins for carriers, yet broker preferences still reward insurers demonstrating underwriting expertise and superior claims service. In specialty lines, Sompo’s differentiated capabilities can soften buyer power by limiting true comparators.

Retail customers’ low switching costs

Retail personal-lines customers can switch easily at renewal, with aggregators handling roughly 25% of online insurance quotes in Japan in 2024, boosting comparison-driven churn. High price sensitivity in auto and fire lines compresses margins, contributing to reported underwriting margin volatility of several hundred basis points in 2024. Sompo’s strong brand and claims reputation helps curb churn, while bundling and loyalty programs further reduce buyer power.

Demand for digital convenience

Customers demand seamless digital onboarding, endorsements, and claims; poor UX raises churn and bargaining power, while Sompo's scale (about JPY 2.8 trillion premiums in FY2023) lets it invest in digital journeys and straight-through processing to blunt price sensitivity. Data-driven personalization increases perceived value and retention, lowering buyer leverage.

- Seamless onboarding reduces churn

- STP lowers price sensitivity

- Personalization raises perceived value

Life and nursing care client expectations

Policyholders and families weigh service quality and long-term reliability heavily; Sompo Holdings leverages SOMPO Care and group nursing platforms to address this amid Japan’s 65+ population ~29.1% (OECD 2023). Transparency on fees and benefits materially affects perceived fairness, while agent advice quality directly shapes purchase and retention decisions. Integrated care-insurance offerings increase switching costs and customer loyalty.

- service-quality focus

- transparency impacts fairness

- agent advice drives bargaining

- integrated care locks loyalty

Insurer must match terms vs captives $97B, brokers ~50%

Large corporates use captives (~$97B risk capital in 2024) and brokers (~50% of major placements) to push benchmarked bids; Sompo must match terms and service, not just price. Retail churn rises via aggregators (~25% online quotes Japan 2024); Sompo’s JPY 2.8T premiums (FY2023) and digital/STP investments offset ~300bps 2024 underwriting volatility.

| Metric | Value |

|---|---|

| Captives (2024) | $97B |

| Brokers share | ~50% |

| Aggregators Japan (2024) | ~25% |

| Sompo premiums (FY2023) | JPY 2.8T |

| Underwriting vol (2024) | ~300bps |

What You See Is What You Get

Sompo Holdings Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Sompo Holdings you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written and ready for download and use the moment you buy. You're viewing the final deliverable.