Sonic Healthcare Porter's Five Forces Analysis

Don't Miss the Bigger Picture

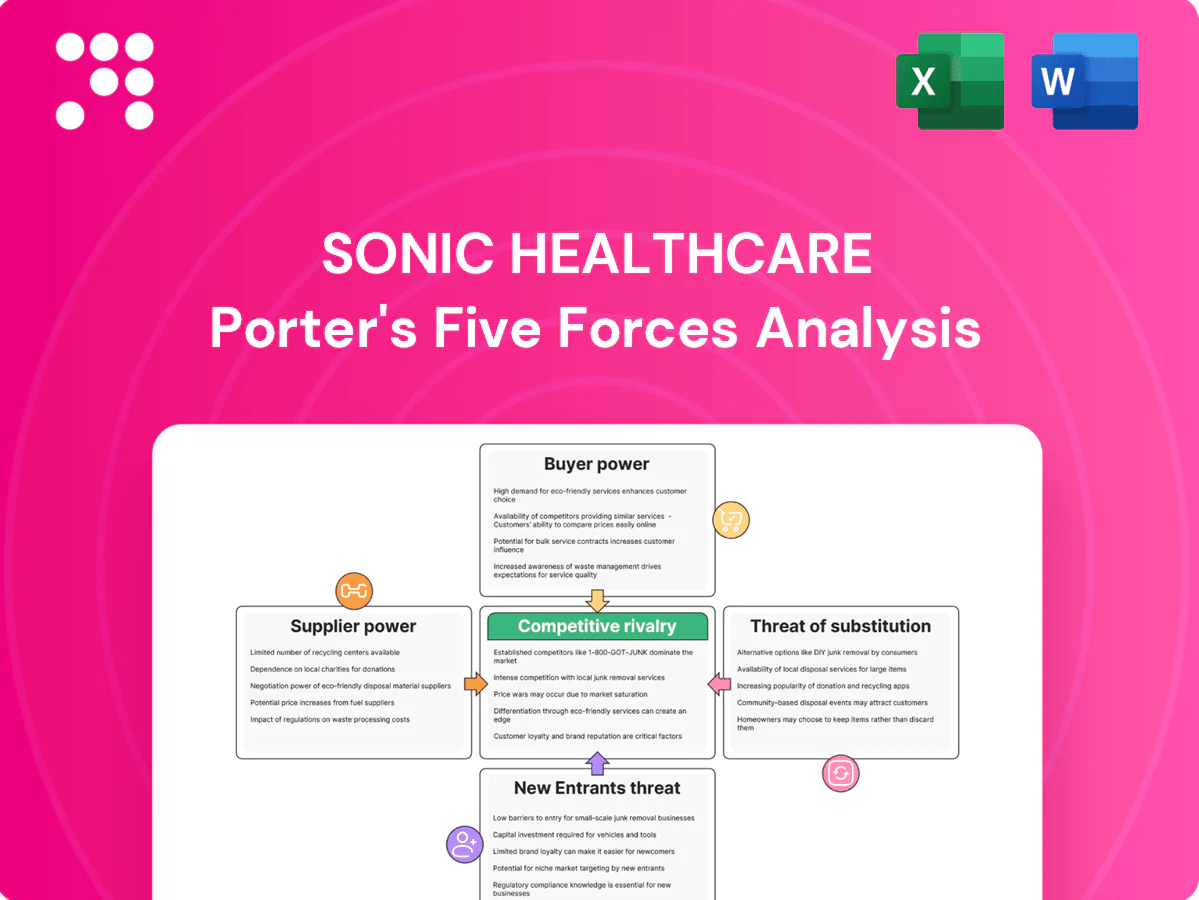

This snapshot highlights key pressures on Sonic Healthcare—from supplier and buyer power to substitutes, new entrants, and rivalry—and how they shape margins and strategic positioning. It surfaces high-level risks and advantages for investors and management. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Reagent and analyzer dependence

Core lab testing depends heavily on proprietary analyzers and reagents from major OEMs such as Roche, Abbott and Siemens, creating vendor lock‑in. Switching vendors requires validation, staff retraining and parallel runs, adding significant cost and operational complexity. Suppliers wield pricing power through bundled service and consumable contracts. Sonic’s international scale supports rebates and multi‑year pricing agreements that partially mitigate this supplier power.

Imaging equipment concentration

Radiology depends on high‑end MRI/CT/US from a few OEMs—GE, Siemens Healthineers and Philips account for roughly 70–80% of global installed base. Capital outlays (MRI $1–3m, CT $0.3–2m) plus service contracts (commonly 10–15% pa) give OEMs pricing and uptime leverage. Software licenses and 7–10 year replacement cycles create ongoing dependency. Sonic can mitigate by multi‑vendor procurement and centralized fleet management to rebalance supplier power.

Specialist labor scarcity

Pathologists, radiologists and subspecialists are scarce in many markets, driving supplier power as Sonic faces rising wage inflation and recruitment/retention packages that compressed margins in 2024. Unions, credentialing and mandatory on‑call coverage reduce staffing flexibility and increase operational cost and risk. Training pipeline growth, telepathology/teleradiology and greater global mobility provide mitigation but do not eliminate the constraint.

IT, LIMS, and PACS vendors

Specimen logistics and consumables

Cold-chain couriers, collection kits and disposables are critical inputs for Sonic Healthcare; in 2024 fuel surcharges and biohazard disposal fees commonly added 5–10% to logistics invoices, and regulatory compliance costs rose with tighter waste rules. Regional courier concentration in key markets increases rate and service risk, while multi-sourcing and route optimization have been used to improve negotiating leverage and cut unit costs.

- Cold‑chain essential

- Fuel/disposal +5–10% (2024)

- Regional concentration = higher risk

- Multi‑sourcing & route optimization = leverage

OEM supplier power: 70–80% imaging share; scale A$13.5bn

Suppliers exert strong power via proprietary analyzers/reagents (OEMs Roche/Abbott/Siemens), high-capex imaging (MRI $1–3m; CT $0.3–2m) and long service contracts (10–15% pa). OEMs hold ~70–80% installed base; Sonic’s A$13.5bn FY2024 scale secures rebates but vendor lock‑in and specialist labor inflation remain material risks.

| Item | 2024 Fact |

|---|---|

| FY Revenue | A$13.5bn |

| OEM share (imaging) | 70–80% |

| Fuel/disposal | +5–10% |

| Service contracts | 10–15% pa |

What is included in the product

Tailored Porter’s Five Forces analysis for Sonic Healthcare that uncovers competitive drivers, buyer and supplier power, threat of substitutes, and barriers to entry, highlighting disruptive threats and strategic levers shaping its pricing and profitability.

A clear, one-sheet summary of Sonic Healthcare's five competitive pressures—ideal for quick C-suite decisions; customize pressure levels to reflect regulation shifts, consolidation or new entrants for instant strategic clarity.

Customers Bargaining Power

Consolidated payers and health systems

Public payers, insurers and large hospital groups buy at scale and run competitive tenders, pressuring prices and service levels especially for commoditized tests; Sonic reported FY2024 revenue AU$6.9bn, underscoring exposure to large buyers.

Contract renewals are often winner-takes-most, with single-provider framework awards capturing the majority of volumes in a region.

Sonic’s national breadth, accreditations and published quality metrics help secure multi-year frameworks and mitigate price erosion.

Reimbursement and fee schedules

Government fee cuts and payer utilization controls in 2024 continue to cap Sonic Healthcare’s pricing power, as mandated fee schedules limit rate increases. Rising test volumes can still compress margins if the case mix shifts toward lower-reimbursement assays. Prior authorization and intensified coding scrutiny elevate denial risk and revenue leakage. Robust RCM and test stewardship programs are essential to protect yield and recover claim denials.

Switching costs and integration

Buyers can switch labs but interface rebuilds, courier re‑routing and clinician habits create measurable friction; high‑acuity sites prioritize continuity and validated reference ranges for patient safety. Strong TAT and service levels reduce willingness to switch, with many hospitals demanding sub‑24‑hour results for core panels. EMR integration penetration now exceeds 96% in US hospitals (ONC), increasing stickiness to incumbent providers.

Demand inelastic yet price sensitive

Clinical necessity makes many Sonic tests non‑discretionary, stabilizing volume even amid pricing pressure; FY2024 commentary highlights resilient core demand. Buyers still press for lower unit prices on high‑volume assays, but Sonic’s esoteric testing and consultative pathology services reduce pure price competition. Increasing value‑based proposals in 2024 shifted some negotiations toward outcomes and cost‑per‑patient metrics.

- Stable demand: clinical necessity (FY2024)

- Price pressure on high‑volume assays

- Differentiation: esoteric tests & consultative services

- Shift to value/outcomes in 2024 negotiations

Direct‑to‑consumer and employers

Direct-to-consumer and employer wellness channels broaden Sonic Healthcare buyers, with Sonic processing over 100 million diagnostic tests annually and trading as ASX:SHL in 2024; customers now compare convenience, turnaround and price transparently online. Volume can be episodic and promotion-driven, while packaging, digital results and brand trust improve retention.

- Buyers: DTC & employers

- Comparison: convenience, turnaround, price

- Volume: episodic/promotional

- Retention: packaging, digital results, brand trust

National lab scale AU$6.9bn cushions but does not end payer pricing pressure

Large payers and hospital groups exert strong price leverage through tenders; Sonic’s FY2024 revenue AU$6.9bn and national scale mitigate but do not eliminate pressure. Government fee cuts and utilization controls in 2024 capped pricing; stickiness arises from accreditations, TAT and EMR integration (>96% US). DTC/employer channels (100m+ tests/year) increase price and convenience comparison.

| Metric | 2024 |

|---|---|

| Revenue | AU$6.9bn |

| Tests processed | 100m+ |

| EMR integration (US) | >96% |

What You See Is What You Get

Sonic Healthcare Porter's Five Forces Analysis

This preview shows the exact Sonic Healthcare Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is professionally formatted, complete, and ready for download; once you buy, you get instant access to this same document for use without further setup.

Don't Miss the Bigger Picture

This snapshot highlights key pressures on Sonic Healthcare—from supplier and buyer power to substitutes, new entrants, and rivalry—and how they shape margins and strategic positioning. It surfaces high-level risks and advantages for investors and management. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Reagent and analyzer dependence

Core lab testing depends heavily on proprietary analyzers and reagents from major OEMs such as Roche, Abbott and Siemens, creating vendor lock‑in. Switching vendors requires validation, staff retraining and parallel runs, adding significant cost and operational complexity. Suppliers wield pricing power through bundled service and consumable contracts. Sonic’s international scale supports rebates and multi‑year pricing agreements that partially mitigate this supplier power.

Imaging equipment concentration

Radiology depends on high‑end MRI/CT/US from a few OEMs—GE, Siemens Healthineers and Philips account for roughly 70–80% of global installed base. Capital outlays (MRI $1–3m, CT $0.3–2m) plus service contracts (commonly 10–15% pa) give OEMs pricing and uptime leverage. Software licenses and 7–10 year replacement cycles create ongoing dependency. Sonic can mitigate by multi‑vendor procurement and centralized fleet management to rebalance supplier power.

Specialist labor scarcity

Pathologists, radiologists and subspecialists are scarce in many markets, driving supplier power as Sonic faces rising wage inflation and recruitment/retention packages that compressed margins in 2024. Unions, credentialing and mandatory on‑call coverage reduce staffing flexibility and increase operational cost and risk. Training pipeline growth, telepathology/teleradiology and greater global mobility provide mitigation but do not eliminate the constraint.

IT, LIMS, and PACS vendors

Specimen logistics and consumables

Cold-chain couriers, collection kits and disposables are critical inputs for Sonic Healthcare; in 2024 fuel surcharges and biohazard disposal fees commonly added 5–10% to logistics invoices, and regulatory compliance costs rose with tighter waste rules. Regional courier concentration in key markets increases rate and service risk, while multi-sourcing and route optimization have been used to improve negotiating leverage and cut unit costs.

- Cold‑chain essential

- Fuel/disposal +5–10% (2024)

- Regional concentration = higher risk

- Multi‑sourcing & route optimization = leverage

OEM supplier power: 70–80% imaging share; scale A$13.5bn

Suppliers exert strong power via proprietary analyzers/reagents (OEMs Roche/Abbott/Siemens), high-capex imaging (MRI $1–3m; CT $0.3–2m) and long service contracts (10–15% pa). OEMs hold ~70–80% installed base; Sonic’s A$13.5bn FY2024 scale secures rebates but vendor lock‑in and specialist labor inflation remain material risks.

| Item | 2024 Fact |

|---|---|

| FY Revenue | A$13.5bn |

| OEM share (imaging) | 70–80% |

| Fuel/disposal | +5–10% |

| Service contracts | 10–15% pa |

What is included in the product

Tailored Porter’s Five Forces analysis for Sonic Healthcare that uncovers competitive drivers, buyer and supplier power, threat of substitutes, and barriers to entry, highlighting disruptive threats and strategic levers shaping its pricing and profitability.

A clear, one-sheet summary of Sonic Healthcare's five competitive pressures—ideal for quick C-suite decisions; customize pressure levels to reflect regulation shifts, consolidation or new entrants for instant strategic clarity.

Customers Bargaining Power

Consolidated payers and health systems

Public payers, insurers and large hospital groups buy at scale and run competitive tenders, pressuring prices and service levels especially for commoditized tests; Sonic reported FY2024 revenue AU$6.9bn, underscoring exposure to large buyers.

Contract renewals are often winner-takes-most, with single-provider framework awards capturing the majority of volumes in a region.

Sonic’s national breadth, accreditations and published quality metrics help secure multi-year frameworks and mitigate price erosion.

Reimbursement and fee schedules

Government fee cuts and payer utilization controls in 2024 continue to cap Sonic Healthcare’s pricing power, as mandated fee schedules limit rate increases. Rising test volumes can still compress margins if the case mix shifts toward lower-reimbursement assays. Prior authorization and intensified coding scrutiny elevate denial risk and revenue leakage. Robust RCM and test stewardship programs are essential to protect yield and recover claim denials.

Switching costs and integration

Buyers can switch labs but interface rebuilds, courier re‑routing and clinician habits create measurable friction; high‑acuity sites prioritize continuity and validated reference ranges for patient safety. Strong TAT and service levels reduce willingness to switch, with many hospitals demanding sub‑24‑hour results for core panels. EMR integration penetration now exceeds 96% in US hospitals (ONC), increasing stickiness to incumbent providers.

Demand inelastic yet price sensitive

Clinical necessity makes many Sonic tests non‑discretionary, stabilizing volume even amid pricing pressure; FY2024 commentary highlights resilient core demand. Buyers still press for lower unit prices on high‑volume assays, but Sonic’s esoteric testing and consultative pathology services reduce pure price competition. Increasing value‑based proposals in 2024 shifted some negotiations toward outcomes and cost‑per‑patient metrics.

- Stable demand: clinical necessity (FY2024)

- Price pressure on high‑volume assays

- Differentiation: esoteric tests & consultative services

- Shift to value/outcomes in 2024 negotiations

Direct‑to‑consumer and employers

Direct-to-consumer and employer wellness channels broaden Sonic Healthcare buyers, with Sonic processing over 100 million diagnostic tests annually and trading as ASX:SHL in 2024; customers now compare convenience, turnaround and price transparently online. Volume can be episodic and promotion-driven, while packaging, digital results and brand trust improve retention.

- Buyers: DTC & employers

- Comparison: convenience, turnaround, price

- Volume: episodic/promotional

- Retention: packaging, digital results, brand trust

National lab scale AU$6.9bn cushions but does not end payer pricing pressure

Large payers and hospital groups exert strong price leverage through tenders; Sonic’s FY2024 revenue AU$6.9bn and national scale mitigate but do not eliminate pressure. Government fee cuts and utilization controls in 2024 capped pricing; stickiness arises from accreditations, TAT and EMR integration (>96% US). DTC/employer channels (100m+ tests/year) increase price and convenience comparison.

| Metric | 2024 |

|---|---|

| Revenue | AU$6.9bn |

| Tests processed | 100m+ |

| EMR integration (US) | >96% |

What You See Is What You Get

Sonic Healthcare Porter's Five Forces Analysis

This preview shows the exact Sonic Healthcare Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is professionally formatted, complete, and ready for download; once you buy, you get instant access to this same document for use without further setup.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

This snapshot highlights key pressures on Sonic Healthcare—from supplier and buyer power to substitutes, new entrants, and rivalry—and how they shape margins and strategic positioning. It surfaces high-level risks and advantages for investors and management. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy guidance.

Suppliers Bargaining Power

Reagent and analyzer dependence

Core lab testing depends heavily on proprietary analyzers and reagents from major OEMs such as Roche, Abbott and Siemens, creating vendor lock‑in. Switching vendors requires validation, staff retraining and parallel runs, adding significant cost and operational complexity. Suppliers wield pricing power through bundled service and consumable contracts. Sonic’s international scale supports rebates and multi‑year pricing agreements that partially mitigate this supplier power.

Imaging equipment concentration

Radiology depends on high‑end MRI/CT/US from a few OEMs—GE, Siemens Healthineers and Philips account for roughly 70–80% of global installed base. Capital outlays (MRI $1–3m, CT $0.3–2m) plus service contracts (commonly 10–15% pa) give OEMs pricing and uptime leverage. Software licenses and 7–10 year replacement cycles create ongoing dependency. Sonic can mitigate by multi‑vendor procurement and centralized fleet management to rebalance supplier power.

Specialist labor scarcity

Pathologists, radiologists and subspecialists are scarce in many markets, driving supplier power as Sonic faces rising wage inflation and recruitment/retention packages that compressed margins in 2024. Unions, credentialing and mandatory on‑call coverage reduce staffing flexibility and increase operational cost and risk. Training pipeline growth, telepathology/teleradiology and greater global mobility provide mitigation but do not eliminate the constraint.

IT, LIMS, and PACS vendors

Specimen logistics and consumables

Cold-chain couriers, collection kits and disposables are critical inputs for Sonic Healthcare; in 2024 fuel surcharges and biohazard disposal fees commonly added 5–10% to logistics invoices, and regulatory compliance costs rose with tighter waste rules. Regional courier concentration in key markets increases rate and service risk, while multi-sourcing and route optimization have been used to improve negotiating leverage and cut unit costs.

- Cold‑chain essential

- Fuel/disposal +5–10% (2024)

- Regional concentration = higher risk

- Multi‑sourcing & route optimization = leverage

OEM supplier power: 70–80% imaging share; scale A$13.5bn

Suppliers exert strong power via proprietary analyzers/reagents (OEMs Roche/Abbott/Siemens), high-capex imaging (MRI $1–3m; CT $0.3–2m) and long service contracts (10–15% pa). OEMs hold ~70–80% installed base; Sonic’s A$13.5bn FY2024 scale secures rebates but vendor lock‑in and specialist labor inflation remain material risks.

| Item | 2024 Fact |

|---|---|

| FY Revenue | A$13.5bn |

| OEM share (imaging) | 70–80% |

| Fuel/disposal | +5–10% |

| Service contracts | 10–15% pa |

What is included in the product

Tailored Porter’s Five Forces analysis for Sonic Healthcare that uncovers competitive drivers, buyer and supplier power, threat of substitutes, and barriers to entry, highlighting disruptive threats and strategic levers shaping its pricing and profitability.

A clear, one-sheet summary of Sonic Healthcare's five competitive pressures—ideal for quick C-suite decisions; customize pressure levels to reflect regulation shifts, consolidation or new entrants for instant strategic clarity.

Customers Bargaining Power

Consolidated payers and health systems

Public payers, insurers and large hospital groups buy at scale and run competitive tenders, pressuring prices and service levels especially for commoditized tests; Sonic reported FY2024 revenue AU$6.9bn, underscoring exposure to large buyers.

Contract renewals are often winner-takes-most, with single-provider framework awards capturing the majority of volumes in a region.

Sonic’s national breadth, accreditations and published quality metrics help secure multi-year frameworks and mitigate price erosion.

Reimbursement and fee schedules

Government fee cuts and payer utilization controls in 2024 continue to cap Sonic Healthcare’s pricing power, as mandated fee schedules limit rate increases. Rising test volumes can still compress margins if the case mix shifts toward lower-reimbursement assays. Prior authorization and intensified coding scrutiny elevate denial risk and revenue leakage. Robust RCM and test stewardship programs are essential to protect yield and recover claim denials.

Switching costs and integration

Buyers can switch labs but interface rebuilds, courier re‑routing and clinician habits create measurable friction; high‑acuity sites prioritize continuity and validated reference ranges for patient safety. Strong TAT and service levels reduce willingness to switch, with many hospitals demanding sub‑24‑hour results for core panels. EMR integration penetration now exceeds 96% in US hospitals (ONC), increasing stickiness to incumbent providers.

Demand inelastic yet price sensitive

Clinical necessity makes many Sonic tests non‑discretionary, stabilizing volume even amid pricing pressure; FY2024 commentary highlights resilient core demand. Buyers still press for lower unit prices on high‑volume assays, but Sonic’s esoteric testing and consultative pathology services reduce pure price competition. Increasing value‑based proposals in 2024 shifted some negotiations toward outcomes and cost‑per‑patient metrics.

- Stable demand: clinical necessity (FY2024)

- Price pressure on high‑volume assays

- Differentiation: esoteric tests & consultative services

- Shift to value/outcomes in 2024 negotiations

Direct‑to‑consumer and employers

Direct-to-consumer and employer wellness channels broaden Sonic Healthcare buyers, with Sonic processing over 100 million diagnostic tests annually and trading as ASX:SHL in 2024; customers now compare convenience, turnaround and price transparently online. Volume can be episodic and promotion-driven, while packaging, digital results and brand trust improve retention.

- Buyers: DTC & employers

- Comparison: convenience, turnaround, price

- Volume: episodic/promotional

- Retention: packaging, digital results, brand trust

National lab scale AU$6.9bn cushions but does not end payer pricing pressure

Large payers and hospital groups exert strong price leverage through tenders; Sonic’s FY2024 revenue AU$6.9bn and national scale mitigate but do not eliminate pressure. Government fee cuts and utilization controls in 2024 capped pricing; stickiness arises from accreditations, TAT and EMR integration (>96% US). DTC/employer channels (100m+ tests/year) increase price and convenience comparison.

| Metric | 2024 |

|---|---|

| Revenue | AU$6.9bn |

| Tests processed | 100m+ |

| EMR integration (US) | >96% |

What You See Is What You Get

Sonic Healthcare Porter's Five Forces Analysis

This preview shows the exact Sonic Healthcare Porter’s Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The file is professionally formatted, complete, and ready for download; once you buy, you get instant access to this same document for use without further setup.