Sonic Healthcare SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Sonic Healthcare’s SWOT highlights a robust global diagnostics network and strong cash flow, counterbalanced by regulatory exposure and technology-led disruption risks. Opportunities in digital pathology and emerging markets could accelerate growth, while competition pressures margins. Discover the full, editable SWOT (Word + Excel) to inform investment, strategy, and pitches—purchase now for the complete analysis.

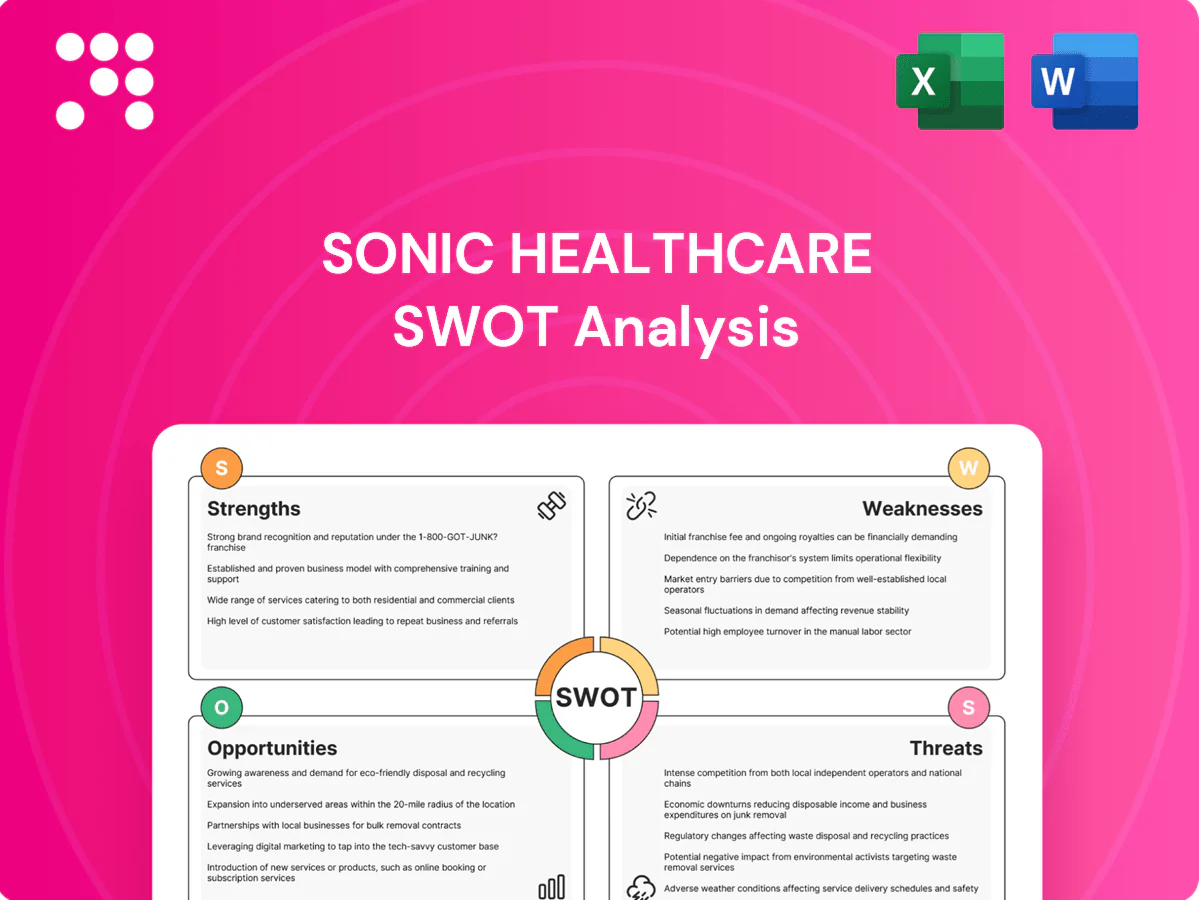

Strengths

Global scale and footprint

Operates extensive laboratory and imaging networks across 10+ countries on four continents, giving broad market access and diversified revenue streams; FY2024 group revenue was about AUD 7.0 billion. Scale drives purchasing power and logistics efficiency for reagents, equipment and IT, lowering unit costs and capital intensity. Cross-border best-practice sharing supports clinical quality and standardization across sites. Geographic spread mitigates localized regulatory or demand shocks.

Diverse diagnostics portfolio

Sonic combines pathology, radiology and selected primary care to deliver end-to-end diagnostic pathways across its international network (ASX:SHL), leveraging integrated menus to increase hospital and clinician share-of-wallet. Cross-referrals between modalities lift volume density and utilization, while diversification smooths cyclical volatility across test categories.

Strong clinician relationships

Strong clinician relationships with hospitals, specialists and community providers create stable referral flows for Sonic Healthcare (ASX:SHL), reinforced by consistent service quality, fast turnaround times and broad accreditation that raise switching costs. Embedded courier logistics and phlebotomy networks increase patient and provider stickiness, while clinical consultative support positions Sonic as a specialist partner rather than a commodity tester.

Operational excellence and M&A track record

Sonic Healthcare’s long history of acquiring and integrating regional pathology and radiology businesses expands capacity while preserving strong local brands, enabling scale without disrupting referral patterns. Standardized IT systems and group procurement programs consistently unlock operational synergies and margin improvement. Centralized reference and specialty labs concentrate complex testing to boost throughput and turn-around, and proven integration expertise reduces execution risk for future consolidation.

- Acquisition-led capacity expansion

- Standardized systems & procurement synergies

- Centralized reference labs for complex testing

- Low execution risk from integration experience

Robust cash flow profile

Routine and chronic-disease testing provides steady, recurring demand for Sonic Healthcare, with high-throughput labs and automated workflows driving significant operating leverage and margin resilience across cycles. Strong cash conversion supports sustained capex, IT upgrades and bolt-on acquisitions, reinforcing defensive characteristics during economic downturns.

- Recurring demand: routine & chronic testing

- Operational leverage: high-throughput automation

- Resilience: defensive cash flows through cycles

- Uses of cash: capex, IT, bolt-on M&A

Integrated lab-imaging network, AUD 7.0bn FY2024 revenue, scale-driven resilience

Operates global lab/imaging network (FY2024 revenue ~AUD 7.0bn), driving procurement and IT scale and diversified cashflows. Integrated pathology, radiology and primary care lifts referrals, utilization and margin resilience. Strong clinician ties, accredited services and proven M&A integration sustain high recurring demand and cash conversion.

| Metric | Value |

|---|---|

| FY2024 revenue | AUD 7.0bn |

| Countries | 10+ |

| Recurring demand | High |

What is included in the product

Provides a clear SWOT framework analyzing Sonic Healthcare’s strengths, weaknesses, opportunities and threats, highlighting its diagnostic scale and clinical reputation, operational challenges, growth avenues in specialized testing and digital health, and regulatory, competitive and reimbursement risks.

Delivers a concise SWOT matrix tailored to Sonic Healthcare for rapid strategy alignment and stakeholder briefings; editable format enables quick updates to reflect operational or regulatory changes.

Weaknesses

Reimbursement dependence

Revenue for Sonic Healthcare is heavily tied to public and private payer fee schedules — the group reported FY2024 revenue of about AUD 11.7 billion, leaving topline exposure to tariff changes. Tariff cuts or coding changes flow directly to margins, while complex cross-jurisdictional billing raises administrative costs and denial risk. There is limited ability to offset payer cuts through price increases given regulated reimbursement frameworks.

Labor-intensive operations

Labor-intensive operations at SonicHealthcare are pressured by shortages of pathologists, radiologists and skilled lab staff, which drive up wage and contractor costs. Retention challenges and rigid scheduling increase risk of delayed turnaround times across diagnostic services. Extensive training and credentialing extend ramp-up for new sites, and dependence on specialist clinicians limits rapid operational flexibility.

High capex and consumables cost

Continuous investment in analysers, imaging kit and IT creates sustained capital intensity for Sonic, squeezing free cash flow. Reagent and consumable inflation has pressured gross margins across the diagnostics sector. Rapid obsolescence cycles force disciplined multi-year capex planning and upgrade timing. Concentration among major equipment vendors limits Sonic’s price and supply negotiating flexibility.

Regulatory complexity

Regulatory complexity forces Sonic to manage multi-jurisdiction accreditation, data-privacy regimes such as GDPR and HIPAA, and varying quality standards; triennial accreditation cycles and frequent audits create fixed overhead. Documentation and audit demands increase operating cost, non-compliance risks fines (GDPR up to 4% of global turnover) or licence limits, and changes in test-utilisation rules (eg MBS adjustments) can abruptly reduce volumes.

- Multi-jurisdiction compliance

- Audit/documentation overhead

- Fines/licence risk; utilisation volatility

Limited pricing power

Diagnostics is often treated as a cost center, limiting Sonic Healthcare (ASX:SHL) pricing power as payers and hospital systems use procurement leverage to push rates lower.

Volume-based discounting can erode unit economics, so sustainable margins depend on differentiation through faster turnaround, specialist services and quality rather than competing on price.

- Payer/hospital leverage

- Commodity pricing pressure

- Volume discounts hurt margins

- Must compete on service & quality

Diagnostics sector exposed to tariff, labor, capex and GDPR risks after AUD 11.7bn FY2024

Revenue exposure: FY2024 revenue AUD 11.7bn ties topline to payer fee schedules and tariff risk. Labor shortages of pathologists and technicians increase wages, contractor use and turnaround risk. High capex for analysers, consumables inflation and vendor concentration compress free cash flow. Multi-jurisdiction regulation (eg GDPR fines up to 4% of global turnover) raises compliance costs and licence risk.

| Metric | Value |

|---|---|

| FY2024 revenue | AUD 11.7bn |

| GDPR fine cap | Up to 4% turnover |

Full Version Awaits

Sonic Healthcare SWOT Analysis

This preview is the actual Sonic Healthcare SWOT analysis document you’ll receive upon purchase—no placeholders, just professional quality. The excerpt below is taken directly from the full report and reflects the same structure, findings, and editable format included in the download. Buy now to unlock the complete, detailed version immediately after checkout.

Elevate Your Analysis with the Complete SWOT Report

Sonic Healthcare’s SWOT highlights a robust global diagnostics network and strong cash flow, counterbalanced by regulatory exposure and technology-led disruption risks. Opportunities in digital pathology and emerging markets could accelerate growth, while competition pressures margins. Discover the full, editable SWOT (Word + Excel) to inform investment, strategy, and pitches—purchase now for the complete analysis.

Strengths

Global scale and footprint

Operates extensive laboratory and imaging networks across 10+ countries on four continents, giving broad market access and diversified revenue streams; FY2024 group revenue was about AUD 7.0 billion. Scale drives purchasing power and logistics efficiency for reagents, equipment and IT, lowering unit costs and capital intensity. Cross-border best-practice sharing supports clinical quality and standardization across sites. Geographic spread mitigates localized regulatory or demand shocks.

Diverse diagnostics portfolio

Sonic combines pathology, radiology and selected primary care to deliver end-to-end diagnostic pathways across its international network (ASX:SHL), leveraging integrated menus to increase hospital and clinician share-of-wallet. Cross-referrals between modalities lift volume density and utilization, while diversification smooths cyclical volatility across test categories.

Strong clinician relationships

Strong clinician relationships with hospitals, specialists and community providers create stable referral flows for Sonic Healthcare (ASX:SHL), reinforced by consistent service quality, fast turnaround times and broad accreditation that raise switching costs. Embedded courier logistics and phlebotomy networks increase patient and provider stickiness, while clinical consultative support positions Sonic as a specialist partner rather than a commodity tester.

Operational excellence and M&A track record

Sonic Healthcare’s long history of acquiring and integrating regional pathology and radiology businesses expands capacity while preserving strong local brands, enabling scale without disrupting referral patterns. Standardized IT systems and group procurement programs consistently unlock operational synergies and margin improvement. Centralized reference and specialty labs concentrate complex testing to boost throughput and turn-around, and proven integration expertise reduces execution risk for future consolidation.

- Acquisition-led capacity expansion

- Standardized systems & procurement synergies

- Centralized reference labs for complex testing

- Low execution risk from integration experience

Robust cash flow profile

Routine and chronic-disease testing provides steady, recurring demand for Sonic Healthcare, with high-throughput labs and automated workflows driving significant operating leverage and margin resilience across cycles. Strong cash conversion supports sustained capex, IT upgrades and bolt-on acquisitions, reinforcing defensive characteristics during economic downturns.

- Recurring demand: routine & chronic testing

- Operational leverage: high-throughput automation

- Resilience: defensive cash flows through cycles

- Uses of cash: capex, IT, bolt-on M&A

Integrated lab-imaging network, AUD 7.0bn FY2024 revenue, scale-driven resilience

Operates global lab/imaging network (FY2024 revenue ~AUD 7.0bn), driving procurement and IT scale and diversified cashflows. Integrated pathology, radiology and primary care lifts referrals, utilization and margin resilience. Strong clinician ties, accredited services and proven M&A integration sustain high recurring demand and cash conversion.

| Metric | Value |

|---|---|

| FY2024 revenue | AUD 7.0bn |

| Countries | 10+ |

| Recurring demand | High |

What is included in the product

Provides a clear SWOT framework analyzing Sonic Healthcare’s strengths, weaknesses, opportunities and threats, highlighting its diagnostic scale and clinical reputation, operational challenges, growth avenues in specialized testing and digital health, and regulatory, competitive and reimbursement risks.

Delivers a concise SWOT matrix tailored to Sonic Healthcare for rapid strategy alignment and stakeholder briefings; editable format enables quick updates to reflect operational or regulatory changes.

Weaknesses

Reimbursement dependence

Revenue for Sonic Healthcare is heavily tied to public and private payer fee schedules — the group reported FY2024 revenue of about AUD 11.7 billion, leaving topline exposure to tariff changes. Tariff cuts or coding changes flow directly to margins, while complex cross-jurisdictional billing raises administrative costs and denial risk. There is limited ability to offset payer cuts through price increases given regulated reimbursement frameworks.

Labor-intensive operations

Labor-intensive operations at SonicHealthcare are pressured by shortages of pathologists, radiologists and skilled lab staff, which drive up wage and contractor costs. Retention challenges and rigid scheduling increase risk of delayed turnaround times across diagnostic services. Extensive training and credentialing extend ramp-up for new sites, and dependence on specialist clinicians limits rapid operational flexibility.

High capex and consumables cost

Continuous investment in analysers, imaging kit and IT creates sustained capital intensity for Sonic, squeezing free cash flow. Reagent and consumable inflation has pressured gross margins across the diagnostics sector. Rapid obsolescence cycles force disciplined multi-year capex planning and upgrade timing. Concentration among major equipment vendors limits Sonic’s price and supply negotiating flexibility.

Regulatory complexity

Regulatory complexity forces Sonic to manage multi-jurisdiction accreditation, data-privacy regimes such as GDPR and HIPAA, and varying quality standards; triennial accreditation cycles and frequent audits create fixed overhead. Documentation and audit demands increase operating cost, non-compliance risks fines (GDPR up to 4% of global turnover) or licence limits, and changes in test-utilisation rules (eg MBS adjustments) can abruptly reduce volumes.

- Multi-jurisdiction compliance

- Audit/documentation overhead

- Fines/licence risk; utilisation volatility

Limited pricing power

Diagnostics is often treated as a cost center, limiting Sonic Healthcare (ASX:SHL) pricing power as payers and hospital systems use procurement leverage to push rates lower.

Volume-based discounting can erode unit economics, so sustainable margins depend on differentiation through faster turnaround, specialist services and quality rather than competing on price.

- Payer/hospital leverage

- Commodity pricing pressure

- Volume discounts hurt margins

- Must compete on service & quality

Diagnostics sector exposed to tariff, labor, capex and GDPR risks after AUD 11.7bn FY2024

Revenue exposure: FY2024 revenue AUD 11.7bn ties topline to payer fee schedules and tariff risk. Labor shortages of pathologists and technicians increase wages, contractor use and turnaround risk. High capex for analysers, consumables inflation and vendor concentration compress free cash flow. Multi-jurisdiction regulation (eg GDPR fines up to 4% of global turnover) raises compliance costs and licence risk.

| Metric | Value |

|---|---|

| FY2024 revenue | AUD 11.7bn |

| GDPR fine cap | Up to 4% turnover |

Full Version Awaits

Sonic Healthcare SWOT Analysis

This preview is the actual Sonic Healthcare SWOT analysis document you’ll receive upon purchase—no placeholders, just professional quality. The excerpt below is taken directly from the full report and reflects the same structure, findings, and editable format included in the download. Buy now to unlock the complete, detailed version immediately after checkout.

Description

Elevate Your Analysis with the Complete SWOT Report

Sonic Healthcare’s SWOT highlights a robust global diagnostics network and strong cash flow, counterbalanced by regulatory exposure and technology-led disruption risks. Opportunities in digital pathology and emerging markets could accelerate growth, while competition pressures margins. Discover the full, editable SWOT (Word + Excel) to inform investment, strategy, and pitches—purchase now for the complete analysis.

Strengths

Global scale and footprint

Operates extensive laboratory and imaging networks across 10+ countries on four continents, giving broad market access and diversified revenue streams; FY2024 group revenue was about AUD 7.0 billion. Scale drives purchasing power and logistics efficiency for reagents, equipment and IT, lowering unit costs and capital intensity. Cross-border best-practice sharing supports clinical quality and standardization across sites. Geographic spread mitigates localized regulatory or demand shocks.

Diverse diagnostics portfolio

Sonic combines pathology, radiology and selected primary care to deliver end-to-end diagnostic pathways across its international network (ASX:SHL), leveraging integrated menus to increase hospital and clinician share-of-wallet. Cross-referrals between modalities lift volume density and utilization, while diversification smooths cyclical volatility across test categories.

Strong clinician relationships

Strong clinician relationships with hospitals, specialists and community providers create stable referral flows for Sonic Healthcare (ASX:SHL), reinforced by consistent service quality, fast turnaround times and broad accreditation that raise switching costs. Embedded courier logistics and phlebotomy networks increase patient and provider stickiness, while clinical consultative support positions Sonic as a specialist partner rather than a commodity tester.

Operational excellence and M&A track record

Sonic Healthcare’s long history of acquiring and integrating regional pathology and radiology businesses expands capacity while preserving strong local brands, enabling scale without disrupting referral patterns. Standardized IT systems and group procurement programs consistently unlock operational synergies and margin improvement. Centralized reference and specialty labs concentrate complex testing to boost throughput and turn-around, and proven integration expertise reduces execution risk for future consolidation.

- Acquisition-led capacity expansion

- Standardized systems & procurement synergies

- Centralized reference labs for complex testing

- Low execution risk from integration experience

Robust cash flow profile

Routine and chronic-disease testing provides steady, recurring demand for Sonic Healthcare, with high-throughput labs and automated workflows driving significant operating leverage and margin resilience across cycles. Strong cash conversion supports sustained capex, IT upgrades and bolt-on acquisitions, reinforcing defensive characteristics during economic downturns.

- Recurring demand: routine & chronic testing

- Operational leverage: high-throughput automation

- Resilience: defensive cash flows through cycles

- Uses of cash: capex, IT, bolt-on M&A

Integrated lab-imaging network, AUD 7.0bn FY2024 revenue, scale-driven resilience

Operates global lab/imaging network (FY2024 revenue ~AUD 7.0bn), driving procurement and IT scale and diversified cashflows. Integrated pathology, radiology and primary care lifts referrals, utilization and margin resilience. Strong clinician ties, accredited services and proven M&A integration sustain high recurring demand and cash conversion.

| Metric | Value |

|---|---|

| FY2024 revenue | AUD 7.0bn |

| Countries | 10+ |

| Recurring demand | High |

What is included in the product

Provides a clear SWOT framework analyzing Sonic Healthcare’s strengths, weaknesses, opportunities and threats, highlighting its diagnostic scale and clinical reputation, operational challenges, growth avenues in specialized testing and digital health, and regulatory, competitive and reimbursement risks.

Delivers a concise SWOT matrix tailored to Sonic Healthcare for rapid strategy alignment and stakeholder briefings; editable format enables quick updates to reflect operational or regulatory changes.

Weaknesses

Reimbursement dependence

Revenue for Sonic Healthcare is heavily tied to public and private payer fee schedules — the group reported FY2024 revenue of about AUD 11.7 billion, leaving topline exposure to tariff changes. Tariff cuts or coding changes flow directly to margins, while complex cross-jurisdictional billing raises administrative costs and denial risk. There is limited ability to offset payer cuts through price increases given regulated reimbursement frameworks.

Labor-intensive operations

Labor-intensive operations at SonicHealthcare are pressured by shortages of pathologists, radiologists and skilled lab staff, which drive up wage and contractor costs. Retention challenges and rigid scheduling increase risk of delayed turnaround times across diagnostic services. Extensive training and credentialing extend ramp-up for new sites, and dependence on specialist clinicians limits rapid operational flexibility.

High capex and consumables cost

Continuous investment in analysers, imaging kit and IT creates sustained capital intensity for Sonic, squeezing free cash flow. Reagent and consumable inflation has pressured gross margins across the diagnostics sector. Rapid obsolescence cycles force disciplined multi-year capex planning and upgrade timing. Concentration among major equipment vendors limits Sonic’s price and supply negotiating flexibility.

Regulatory complexity

Regulatory complexity forces Sonic to manage multi-jurisdiction accreditation, data-privacy regimes such as GDPR and HIPAA, and varying quality standards; triennial accreditation cycles and frequent audits create fixed overhead. Documentation and audit demands increase operating cost, non-compliance risks fines (GDPR up to 4% of global turnover) or licence limits, and changes in test-utilisation rules (eg MBS adjustments) can abruptly reduce volumes.

- Multi-jurisdiction compliance

- Audit/documentation overhead

- Fines/licence risk; utilisation volatility

Limited pricing power

Diagnostics is often treated as a cost center, limiting Sonic Healthcare (ASX:SHL) pricing power as payers and hospital systems use procurement leverage to push rates lower.

Volume-based discounting can erode unit economics, so sustainable margins depend on differentiation through faster turnaround, specialist services and quality rather than competing on price.

- Payer/hospital leverage

- Commodity pricing pressure

- Volume discounts hurt margins

- Must compete on service & quality

Diagnostics sector exposed to tariff, labor, capex and GDPR risks after AUD 11.7bn FY2024

Revenue exposure: FY2024 revenue AUD 11.7bn ties topline to payer fee schedules and tariff risk. Labor shortages of pathologists and technicians increase wages, contractor use and turnaround risk. High capex for analysers, consumables inflation and vendor concentration compress free cash flow. Multi-jurisdiction regulation (eg GDPR fines up to 4% of global turnover) raises compliance costs and licence risk.

| Metric | Value |

|---|---|

| FY2024 revenue | AUD 11.7bn |

| GDPR fine cap | Up to 4% turnover |

Full Version Awaits

Sonic Healthcare SWOT Analysis

This preview is the actual Sonic Healthcare SWOT analysis document you’ll receive upon purchase—no placeholders, just professional quality. The excerpt below is taken directly from the full report and reflects the same structure, findings, and editable format included in the download. Buy now to unlock the complete, detailed version immediately after checkout.