Elite Body Sculpture Porter's Five Forces Analysis

From Overview to Strategy Blueprint

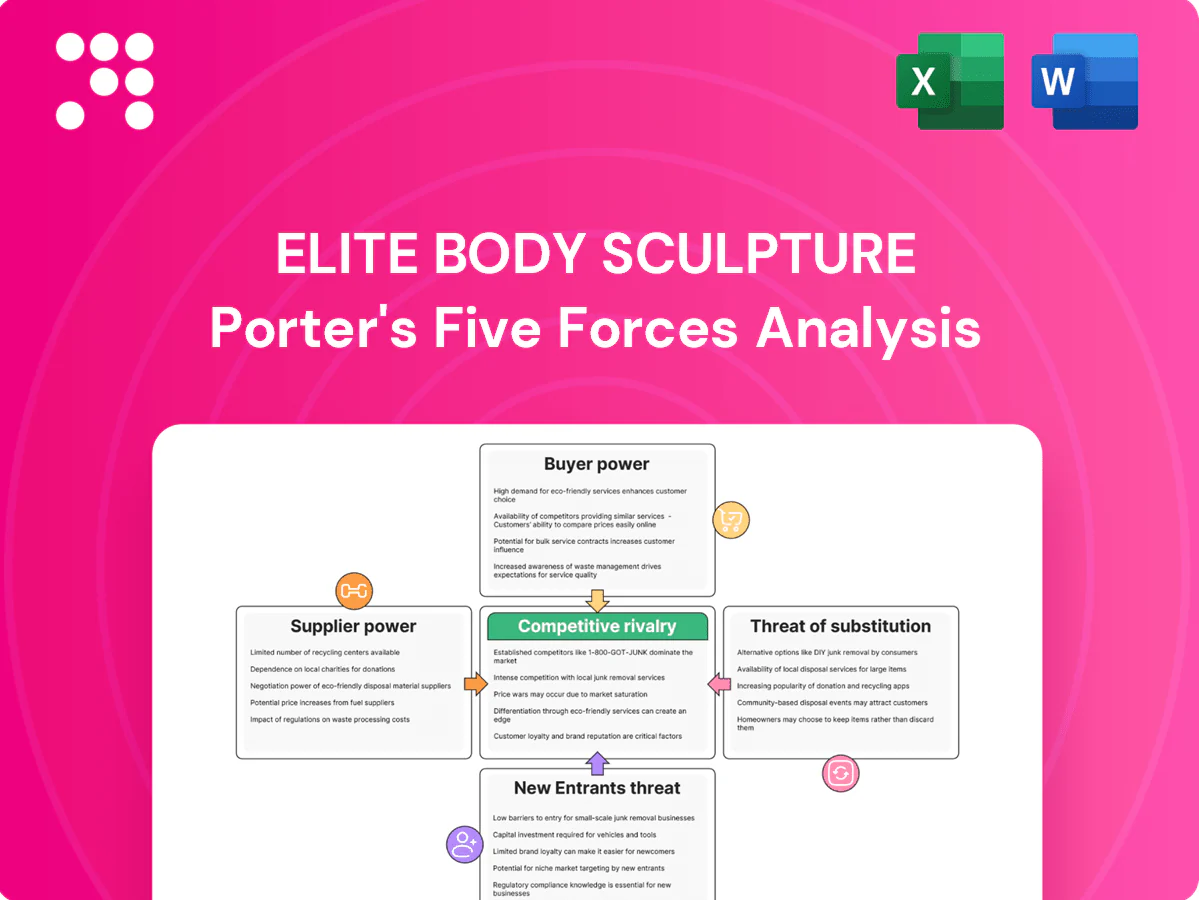

This brief Porter’s Five Forces snapshot highlights key pressures facing Elite Body Sculpture—competitive intensity, buyer leverage, supplier influence and substitute threats—without the full context. Unlock the complete analysis to see force-by-force ratings, visuals and strategic implications. Get the consultant-grade report for immediate use in investment or strategy decisions.

Suppliers Bargaining Power

Specialized device OEMs

AirSculpt relies on precision hardware and proprietary handpieces supplied by a small set of FDA‑compliant OEMs (fewer than five major suppliers), raising tangible switching costs and typical lead times of 12–24 weeks reported in 2024. Volume commitments can secure 10–20% price breaks but lock capacity and limit flexibility. Any supplier quality or regulatory lapse can halt procedures and cut monthly revenue by double digits.

Surgical talent and training

Board-certified surgeons and specialized OR staff act as critical suppliers; ASPS reported roughly 7,000 board-certified plastic surgeons in the US in 2024, concentrating supply in top metros and giving clinicians leverage on pay and schedules. Proprietary technique training deepens dependence but raises consistency and outcomes. Retention programs and incentives (turnover replacement often costing ~20–30% of annual salary) are essential to manage supplier power.

Disposable kits and pharma inputs

Disposable cannulas, tubing, local anesthetics, antibiotics and PPE are recurring inputs with broad availability, so supplier pricing power is moderate. Access to GPO contracts—covering about 70% of hospital procurement in 2024—shifts leverage toward buyers. Supply shocks or recalls can still spike costs and force substitutions, as seen in past PPE disruptions. Standardization and dual-sourcing are practical mitigants to this volatility.

Clinical software and payments

Clinical software and payments (EMR, imaging, CRM, payment/financing platforms) create strong stickiness once integrated, enabling vendors to charge per-seat fees and restrict data portability, which elevates supplier pricing power; card processors commonly charge ~2.9% + $0.30 per transaction (2024). API openness and contract terms dictate lock-in, while negotiated enterprise agreements can lower per-clinic costs by roughly 20–40%.

- EMR/CRM: per-seat fees drive recurring costs

- Payments: ~2.9% + $0.30 average processing fee (2024)

- Data portability: limited APIs increase switching costs

- Enterprise deals: ~20–40% cost reduction

Facility landlords and accreditation

Facility landlords in premium retail-medical corridors command rents often 20–40% above suburban averages and negotiate tenant improvement (TI) allowances tightly; typical TI ranges for medical-retail buildouts are $50–150/sqft. AAAHC and Joint Commission accreditation add compliance costs and timelines—surveys and remediation commonly take 3–9 months. Multi-site scale can secure better TI and lease terms but does not erase landlord leverage.

- Premium rents +20–40%

- TI allowances $50–150/sqft

- Accreditation 3–9 months

- Scale improves but not eliminates leverage

High supplier power: proprietary OEM hardware, ≈7,000 surgeons, payments ≈2.9% + $0.30

Supplier power is high for proprietary AirSculpt hardware (fewer than five FDA‑compliant OEMs; 12–24 week lead times, 10–20% volume discounts), strong for board‑certified surgeons (≈7,000 US plastic surgeons in 2024) and clinical software/payments (≈2.9% + $0.30 transaction fees), moderate for disposables and GPO‑sourced items, and elevated by premium rents (+20–40%) and TI costs.

| Supplier | Metric (2024) |

|---|---|

| OEM hardware | <12–24 wk lead, <5 suppliers, 10–20% discounts |

| Surgeons | ≈7,000 board‑certified US surgeons |

| Payments | ≈2.9% + $0.30/tx |

| Rents/TI | Rents +20–40%, TI $50–150/sqft |

What is included in the product

Tailored exclusively for Elite Body Sculpture, this Porter's Five Forces overview uncovers competitive intensity, buyer and supplier leverage, substitute threats, and barriers to entry shaping profitability. It identifies disruptive forces and emerging rivals that could erode market share and highlights strategic implications for pricing and growth.

A single-sheet Porter's Five Forces for Elite Body Sculpture that highlights competitive pressures, supplier and patient bargaining power, and regulatory threats—quickly pinpointing strategic pain points and suggested mitigation moves for faster boardroom decisions.

Customers Bargaining Power

Elective-payer price sensitivity

Patients pay out-of-pocket for elective body contouring, increasing price sensitivity; ASPS reported roughly 15.6 million cosmetic procedures in 2023, underscoring a large self-pay market. Online transparent quotes and financing partners like CareCredit accelerate comparison shopping, while bundled pricing can blunt apples-to-apples checks. Outcome galleries and patient testimonials must justify premiums and drive conversions.

Information-rich shoppers

Information-rich shoppers use reviews, before/after photos, Reddit threads and influencers to benchmark Elite Body Sculpture; according to BrightLocal 2024, 93% consult online reviews, raising transparency-driven expectations and negotiation attempts. Consistent outcomes and swift, public responses to negative feedback are critical, while targeted education funnels can shift purchase drivers from price to perceived value.

Switching ease across clinics

Patients can easily consult multiple providers locally and virtually, with the American Society of Plastic Surgeons reporting over 15 million cosmetic procedures in 2023, reflecting high market activity and comparison shopping. Minimal switching costs increase buyer leverage pre-procedure, though deposits and scheduling windows create mild friction. Differentiated technique and faster recovery time reduce churn by raising perceived switching costs.

Demand seasonality and timing

Cosmetic demand at Elite Body Sculpture rises sharply pre-summer and around year-end, with industry seasonal peaks ~25% in May–July and ~20% in Nov–Dec in 2024; buyers exploit slow-season promos averaging ~15% off, pressuring margins; dynamic pricing and capacity management lift utilization while protecting margins by ~8–12%; waitlist strategies preserve price integrity, recovering roughly 10% of potential discounting.

- Seasonal peaks ~25% (May–Jul), ~20% (Nov–Dec) 2024

- Slow-season promotions ≈15% average discount

- Dynamic pricing boosts margin utilization ~8–12%

- Waitlists recover ~10% of lost pricing

Financing and payment plans

- third-party financing increases shopper leverage

- merchant fees 1.5–3.5% (2024)

- tiered plans preserve margins

- clear disclosures lower chargebacks (threshold ~0.9%)

Price-sensitive patients in ~15M elective market: financing + reviews boost buyer leverage

Patients are price-sensitive in a ~15M procedure elective market; financing increases comparison shopping. Low switching costs plus 93% review reliance (2024) raise buyer leverage. Slow-season promos (~15%) and merchant fees (1.5–3.5%) compress margins; dynamic pricing and waitlists recover ~8–12% margin and ~10% pricing integrity.

| Metric | Value |

|---|---|

| Annual procedures (ASPS) | ~15M |

| Review reliance (BrightLocal 2024) | 93% |

| Slow-season promo | ~15% |

| Merchant fees (2024) | 1.5–3.5% |

| Dyn pricing uplift | 8–12% |

| Waitlist recovery | ~10% |

Full Version Awaits

Elite Body Sculpture Porter's Five Forces Analysis

This preview shows the Elite Body Sculpture Porter's Five Forces Analysis exactly as delivered. The document is fully formatted, complete, and ready for immediate download after purchase. No samples or placeholders—what you see is the exact file you'll receive for use.

From Overview to Strategy Blueprint

This brief Porter’s Five Forces snapshot highlights key pressures facing Elite Body Sculpture—competitive intensity, buyer leverage, supplier influence and substitute threats—without the full context. Unlock the complete analysis to see force-by-force ratings, visuals and strategic implications. Get the consultant-grade report for immediate use in investment or strategy decisions.

Suppliers Bargaining Power

Specialized device OEMs

AirSculpt relies on precision hardware and proprietary handpieces supplied by a small set of FDA‑compliant OEMs (fewer than five major suppliers), raising tangible switching costs and typical lead times of 12–24 weeks reported in 2024. Volume commitments can secure 10–20% price breaks but lock capacity and limit flexibility. Any supplier quality or regulatory lapse can halt procedures and cut monthly revenue by double digits.

Surgical talent and training

Board-certified surgeons and specialized OR staff act as critical suppliers; ASPS reported roughly 7,000 board-certified plastic surgeons in the US in 2024, concentrating supply in top metros and giving clinicians leverage on pay and schedules. Proprietary technique training deepens dependence but raises consistency and outcomes. Retention programs and incentives (turnover replacement often costing ~20–30% of annual salary) are essential to manage supplier power.

Disposable kits and pharma inputs

Disposable cannulas, tubing, local anesthetics, antibiotics and PPE are recurring inputs with broad availability, so supplier pricing power is moderate. Access to GPO contracts—covering about 70% of hospital procurement in 2024—shifts leverage toward buyers. Supply shocks or recalls can still spike costs and force substitutions, as seen in past PPE disruptions. Standardization and dual-sourcing are practical mitigants to this volatility.

Clinical software and payments

Clinical software and payments (EMR, imaging, CRM, payment/financing platforms) create strong stickiness once integrated, enabling vendors to charge per-seat fees and restrict data portability, which elevates supplier pricing power; card processors commonly charge ~2.9% + $0.30 per transaction (2024). API openness and contract terms dictate lock-in, while negotiated enterprise agreements can lower per-clinic costs by roughly 20–40%.

- EMR/CRM: per-seat fees drive recurring costs

- Payments: ~2.9% + $0.30 average processing fee (2024)

- Data portability: limited APIs increase switching costs

- Enterprise deals: ~20–40% cost reduction

Facility landlords and accreditation

Facility landlords in premium retail-medical corridors command rents often 20–40% above suburban averages and negotiate tenant improvement (TI) allowances tightly; typical TI ranges for medical-retail buildouts are $50–150/sqft. AAAHC and Joint Commission accreditation add compliance costs and timelines—surveys and remediation commonly take 3–9 months. Multi-site scale can secure better TI and lease terms but does not erase landlord leverage.

- Premium rents +20–40%

- TI allowances $50–150/sqft

- Accreditation 3–9 months

- Scale improves but not eliminates leverage

High supplier power: proprietary OEM hardware, ≈7,000 surgeons, payments ≈2.9% + $0.30

Supplier power is high for proprietary AirSculpt hardware (fewer than five FDA‑compliant OEMs; 12–24 week lead times, 10–20% volume discounts), strong for board‑certified surgeons (≈7,000 US plastic surgeons in 2024) and clinical software/payments (≈2.9% + $0.30 transaction fees), moderate for disposables and GPO‑sourced items, and elevated by premium rents (+20–40%) and TI costs.

| Supplier | Metric (2024) |

|---|---|

| OEM hardware | <12–24 wk lead, <5 suppliers, 10–20% discounts |

| Surgeons | ≈7,000 board‑certified US surgeons |

| Payments | ≈2.9% + $0.30/tx |

| Rents/TI | Rents +20–40%, TI $50–150/sqft |

What is included in the product

Tailored exclusively for Elite Body Sculpture, this Porter's Five Forces overview uncovers competitive intensity, buyer and supplier leverage, substitute threats, and barriers to entry shaping profitability. It identifies disruptive forces and emerging rivals that could erode market share and highlights strategic implications for pricing and growth.

A single-sheet Porter's Five Forces for Elite Body Sculpture that highlights competitive pressures, supplier and patient bargaining power, and regulatory threats—quickly pinpointing strategic pain points and suggested mitigation moves for faster boardroom decisions.

Customers Bargaining Power

Elective-payer price sensitivity

Patients pay out-of-pocket for elective body contouring, increasing price sensitivity; ASPS reported roughly 15.6 million cosmetic procedures in 2023, underscoring a large self-pay market. Online transparent quotes and financing partners like CareCredit accelerate comparison shopping, while bundled pricing can blunt apples-to-apples checks. Outcome galleries and patient testimonials must justify premiums and drive conversions.

Information-rich shoppers

Information-rich shoppers use reviews, before/after photos, Reddit threads and influencers to benchmark Elite Body Sculpture; according to BrightLocal 2024, 93% consult online reviews, raising transparency-driven expectations and negotiation attempts. Consistent outcomes and swift, public responses to negative feedback are critical, while targeted education funnels can shift purchase drivers from price to perceived value.

Switching ease across clinics

Patients can easily consult multiple providers locally and virtually, with the American Society of Plastic Surgeons reporting over 15 million cosmetic procedures in 2023, reflecting high market activity and comparison shopping. Minimal switching costs increase buyer leverage pre-procedure, though deposits and scheduling windows create mild friction. Differentiated technique and faster recovery time reduce churn by raising perceived switching costs.

Demand seasonality and timing

Cosmetic demand at Elite Body Sculpture rises sharply pre-summer and around year-end, with industry seasonal peaks ~25% in May–July and ~20% in Nov–Dec in 2024; buyers exploit slow-season promos averaging ~15% off, pressuring margins; dynamic pricing and capacity management lift utilization while protecting margins by ~8–12%; waitlist strategies preserve price integrity, recovering roughly 10% of potential discounting.

- Seasonal peaks ~25% (May–Jul), ~20% (Nov–Dec) 2024

- Slow-season promotions ≈15% average discount

- Dynamic pricing boosts margin utilization ~8–12%

- Waitlists recover ~10% of lost pricing

Financing and payment plans

- third-party financing increases shopper leverage

- merchant fees 1.5–3.5% (2024)

- tiered plans preserve margins

- clear disclosures lower chargebacks (threshold ~0.9%)

Price-sensitive patients in ~15M elective market: financing + reviews boost buyer leverage

Patients are price-sensitive in a ~15M procedure elective market; financing increases comparison shopping. Low switching costs plus 93% review reliance (2024) raise buyer leverage. Slow-season promos (~15%) and merchant fees (1.5–3.5%) compress margins; dynamic pricing and waitlists recover ~8–12% margin and ~10% pricing integrity.

| Metric | Value |

|---|---|

| Annual procedures (ASPS) | ~15M |

| Review reliance (BrightLocal 2024) | 93% |

| Slow-season promo | ~15% |

| Merchant fees (2024) | 1.5–3.5% |

| Dyn pricing uplift | 8–12% |

| Waitlist recovery | ~10% |

Full Version Awaits

Elite Body Sculpture Porter's Five Forces Analysis

This preview shows the Elite Body Sculpture Porter's Five Forces Analysis exactly as delivered. The document is fully formatted, complete, and ready for immediate download after purchase. No samples or placeholders—what you see is the exact file you'll receive for use.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

This brief Porter’s Five Forces snapshot highlights key pressures facing Elite Body Sculpture—competitive intensity, buyer leverage, supplier influence and substitute threats—without the full context. Unlock the complete analysis to see force-by-force ratings, visuals and strategic implications. Get the consultant-grade report for immediate use in investment or strategy decisions.

Suppliers Bargaining Power

Specialized device OEMs

AirSculpt relies on precision hardware and proprietary handpieces supplied by a small set of FDA‑compliant OEMs (fewer than five major suppliers), raising tangible switching costs and typical lead times of 12–24 weeks reported in 2024. Volume commitments can secure 10–20% price breaks but lock capacity and limit flexibility. Any supplier quality or regulatory lapse can halt procedures and cut monthly revenue by double digits.

Surgical talent and training

Board-certified surgeons and specialized OR staff act as critical suppliers; ASPS reported roughly 7,000 board-certified plastic surgeons in the US in 2024, concentrating supply in top metros and giving clinicians leverage on pay and schedules. Proprietary technique training deepens dependence but raises consistency and outcomes. Retention programs and incentives (turnover replacement often costing ~20–30% of annual salary) are essential to manage supplier power.

Disposable kits and pharma inputs

Disposable cannulas, tubing, local anesthetics, antibiotics and PPE are recurring inputs with broad availability, so supplier pricing power is moderate. Access to GPO contracts—covering about 70% of hospital procurement in 2024—shifts leverage toward buyers. Supply shocks or recalls can still spike costs and force substitutions, as seen in past PPE disruptions. Standardization and dual-sourcing are practical mitigants to this volatility.

Clinical software and payments

Clinical software and payments (EMR, imaging, CRM, payment/financing platforms) create strong stickiness once integrated, enabling vendors to charge per-seat fees and restrict data portability, which elevates supplier pricing power; card processors commonly charge ~2.9% + $0.30 per transaction (2024). API openness and contract terms dictate lock-in, while negotiated enterprise agreements can lower per-clinic costs by roughly 20–40%.

- EMR/CRM: per-seat fees drive recurring costs

- Payments: ~2.9% + $0.30 average processing fee (2024)

- Data portability: limited APIs increase switching costs

- Enterprise deals: ~20–40% cost reduction

Facility landlords and accreditation

Facility landlords in premium retail-medical corridors command rents often 20–40% above suburban averages and negotiate tenant improvement (TI) allowances tightly; typical TI ranges for medical-retail buildouts are $50–150/sqft. AAAHC and Joint Commission accreditation add compliance costs and timelines—surveys and remediation commonly take 3–9 months. Multi-site scale can secure better TI and lease terms but does not erase landlord leverage.

- Premium rents +20–40%

- TI allowances $50–150/sqft

- Accreditation 3–9 months

- Scale improves but not eliminates leverage

High supplier power: proprietary OEM hardware, ≈7,000 surgeons, payments ≈2.9% + $0.30

Supplier power is high for proprietary AirSculpt hardware (fewer than five FDA‑compliant OEMs; 12–24 week lead times, 10–20% volume discounts), strong for board‑certified surgeons (≈7,000 US plastic surgeons in 2024) and clinical software/payments (≈2.9% + $0.30 transaction fees), moderate for disposables and GPO‑sourced items, and elevated by premium rents (+20–40%) and TI costs.

| Supplier | Metric (2024) |

|---|---|

| OEM hardware | <12–24 wk lead, <5 suppliers, 10–20% discounts |

| Surgeons | ≈7,000 board‑certified US surgeons |

| Payments | ≈2.9% + $0.30/tx |

| Rents/TI | Rents +20–40%, TI $50–150/sqft |

What is included in the product

Tailored exclusively for Elite Body Sculpture, this Porter's Five Forces overview uncovers competitive intensity, buyer and supplier leverage, substitute threats, and barriers to entry shaping profitability. It identifies disruptive forces and emerging rivals that could erode market share and highlights strategic implications for pricing and growth.

A single-sheet Porter's Five Forces for Elite Body Sculpture that highlights competitive pressures, supplier and patient bargaining power, and regulatory threats—quickly pinpointing strategic pain points and suggested mitigation moves for faster boardroom decisions.

Customers Bargaining Power

Elective-payer price sensitivity

Patients pay out-of-pocket for elective body contouring, increasing price sensitivity; ASPS reported roughly 15.6 million cosmetic procedures in 2023, underscoring a large self-pay market. Online transparent quotes and financing partners like CareCredit accelerate comparison shopping, while bundled pricing can blunt apples-to-apples checks. Outcome galleries and patient testimonials must justify premiums and drive conversions.

Information-rich shoppers

Information-rich shoppers use reviews, before/after photos, Reddit threads and influencers to benchmark Elite Body Sculpture; according to BrightLocal 2024, 93% consult online reviews, raising transparency-driven expectations and negotiation attempts. Consistent outcomes and swift, public responses to negative feedback are critical, while targeted education funnels can shift purchase drivers from price to perceived value.

Switching ease across clinics

Patients can easily consult multiple providers locally and virtually, with the American Society of Plastic Surgeons reporting over 15 million cosmetic procedures in 2023, reflecting high market activity and comparison shopping. Minimal switching costs increase buyer leverage pre-procedure, though deposits and scheduling windows create mild friction. Differentiated technique and faster recovery time reduce churn by raising perceived switching costs.

Demand seasonality and timing

Cosmetic demand at Elite Body Sculpture rises sharply pre-summer and around year-end, with industry seasonal peaks ~25% in May–July and ~20% in Nov–Dec in 2024; buyers exploit slow-season promos averaging ~15% off, pressuring margins; dynamic pricing and capacity management lift utilization while protecting margins by ~8–12%; waitlist strategies preserve price integrity, recovering roughly 10% of potential discounting.

- Seasonal peaks ~25% (May–Jul), ~20% (Nov–Dec) 2024

- Slow-season promotions ≈15% average discount

- Dynamic pricing boosts margin utilization ~8–12%

- Waitlists recover ~10% of lost pricing

Financing and payment plans

- third-party financing increases shopper leverage

- merchant fees 1.5–3.5% (2024)

- tiered plans preserve margins

- clear disclosures lower chargebacks (threshold ~0.9%)

Price-sensitive patients in ~15M elective market: financing + reviews boost buyer leverage

Patients are price-sensitive in a ~15M procedure elective market; financing increases comparison shopping. Low switching costs plus 93% review reliance (2024) raise buyer leverage. Slow-season promos (~15%) and merchant fees (1.5–3.5%) compress margins; dynamic pricing and waitlists recover ~8–12% margin and ~10% pricing integrity.

| Metric | Value |

|---|---|

| Annual procedures (ASPS) | ~15M |

| Review reliance (BrightLocal 2024) | 93% |

| Slow-season promo | ~15% |

| Merchant fees (2024) | 1.5–3.5% |

| Dyn pricing uplift | 8–12% |

| Waitlist recovery | ~10% |

Full Version Awaits

Elite Body Sculpture Porter's Five Forces Analysis

This preview shows the Elite Body Sculpture Porter's Five Forces Analysis exactly as delivered. The document is fully formatted, complete, and ready for immediate download after purchase. No samples or placeholders—what you see is the exact file you'll receive for use.