Phonak Holding AG Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

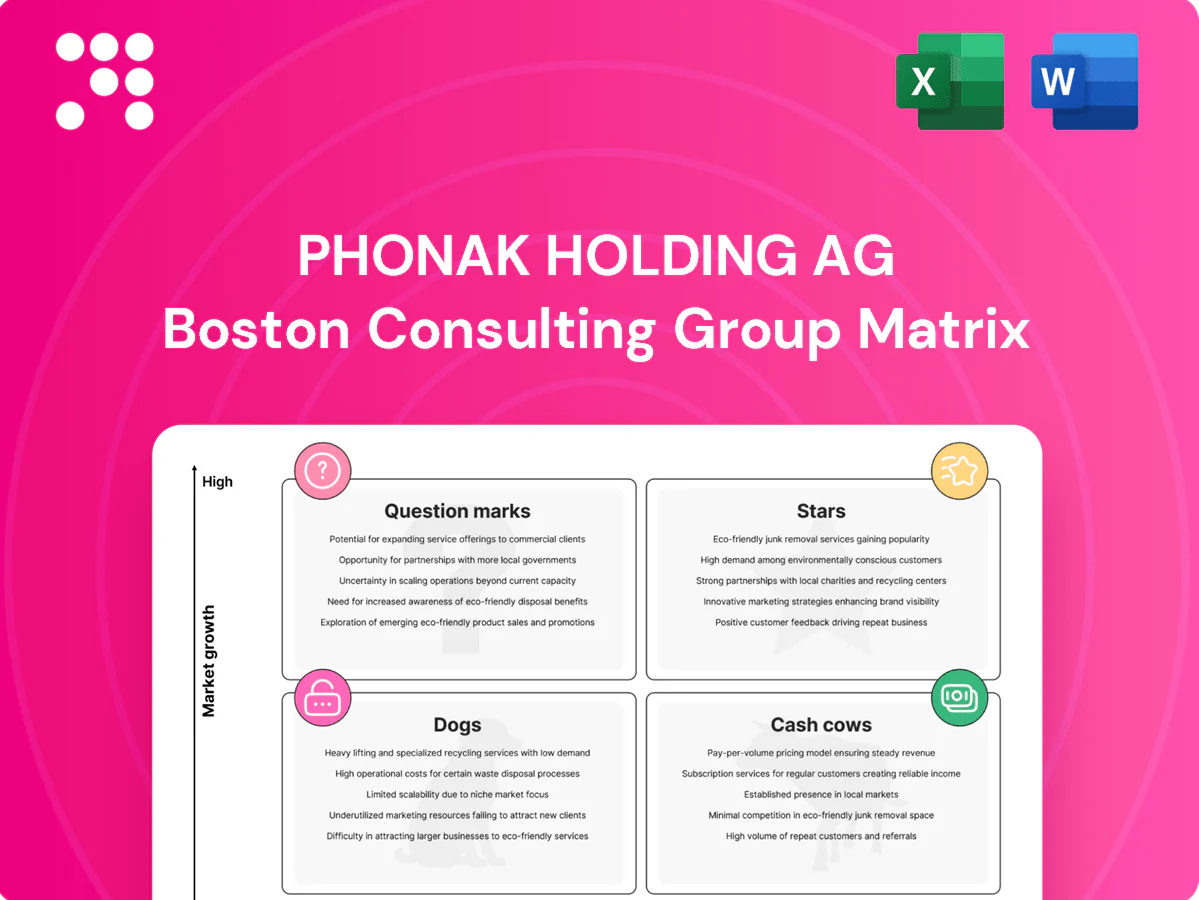

Phonak Holding AG’s BCG Matrix preview shows where its hearing-tech franchises sit as markets shift—some clear Stars, a couple steady Cash Cows, and a few Question Marks worth watching. You’ll get a quick sense of where revenue flows and where R&D might be overextended, but this is just the headline. Purchase the full BCG Matrix for quadrant-by-quadrant data, strategic recommendations, and editable Word + Excel files you can plug into your board deck. Get the full report and cut straight to confident, actionable decisions.

Stars

Premium RIC hearing aids (Phonak Lumity/Paradise)

Phonak Paradise (launched 2020) and Lumity (launched 2023) command a high share of the premium RIC segment, a tech-led market with frequent device upgrades and growing clinician adoption. Flagship features such as advanced connectivity and AI-driven sound processing drive strong loyalty, though promotion and channel training continue to consume marketing spend. Sonova reported FY 2023/24 net sales of about CHF 3.3 billion, underpinning scale to convert these models into major cash generators as they mature.

Roger wireless systems for schools and workplaces

Roger wireless systems are the clear leader where hearing-in-noise is mission-critical, with adoption expanding in schools and workplaces as institutions modernize accessibility; WHO reports about 430 million people worldwide have disabling hearing loss (2024), underpinning demand. Growth remains strong but requires continued investment in integrations and advocacy to sustain momentum and capture institutional procurement waves.

Pediatric hearing solutions (Phonak Sky portfolio)

Phonak Sky, part of Phonak’s pediatric portfolio, sits within a dominant global hearing-care position as Sonova is one of the world’s largest hearing‑care companies and WHO’s World Report on Hearing (2021) estimates 34 million children with disabling hearing loss, driving rising demand and growing policy support for newborn screening and early intervention.

Delivering Sky effectively requires sustained funding for clinician education, fittings, and caregiver programs because WHO finds early identification and intervention measurably improve language and developmental outcomes.

Securing this segment translates to high lifetime customer value due to long product lifecycles and ongoing service needs within pediatric care pathways.

Rechargeable Li‑ion product lines

Rechargeable Li-ion product lines are in the Stars quadrant as user preference and clinic recommendations increasingly favor convenience and reduced maintenance, driving rapid unit growth in 2024.

Hardware leadership and integrated charging ecosystems enhance customer lock-in by raising switching costs and enabling accessory-driven revenue streams.

These lines remain cash-hungry in 2024 due to elevated R&D, specialized tooling and deeper inventory commitments required for battery, charger and service ecosystems.

- market-trend: growing clinic and consumer preference for rechargeable convenience

- competitive-advantage: hardware + charging ecosystem = stronger lock-in

- cost-profile: high upfront R&D, tooling and inventory needs

Bluetooth streaming and app-connected features

Bluetooth streaming and app-connected features are Stars in Phonak Holding AGs BCG matrix as 2024 rollouts of Bluetooth LE Audio accelerated wearable-like adoption; premium-device streaming penetration exceeded 40% in 2024, driving high-growth expectations. Meeting modern user behavior sustains market share, while continuous firmware updates and wide device compatibility require ongoing R&D and testing spend to stay ahead.

- High-growth: Bluetooth LE Audio rollouts 2024; >40% premium streaming penetration

- Share retention: aligns with wearable user behavior

- Cost: continuous updates, compatibility testing, rising R&D spend

Premium RICs, critical wireless & pediatric demand; rechargeable + LE Audio >40%

Phonak Paradise/Lumity lead premium RICs (Sonova FY23/24 sales ~CHF 3.3bn) with strong loyalty but elevated marketing spend; Roger dominates mission-critical wireless (WHO 2024: 430m with disabling hearing loss) requiring advocacy investment; Sky captures pediatric demand amid rising newborn screening; rechargeable lines and Bluetooth LE Audio (>40% premium streaming penetration in 2024) are high-growth but capex‑intensive.

| Segment | 2024 metric | Status | Cost profile |

|---|---|---|---|

| Paradise/Lumity | Share: high | Star | Marketing/training |

| Roger | Adoption: expanding | Star | Integration/advocacy |

| Sky | Child demand↑ | Star | Clinician funding |

| Rechargeable | Unit growth 2024: rapid | Star | R&D/tooling |

| Bluetooth LE Audio | Premium >40% | Star | Firmware/R&D |

What is included in the product

BCG analysis of Phonak: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest guidance and trend context.

One-page BCG matrix placing Phonak business units in quadrants to cut portfolio confusion for execs.

Cash Cows

Mid-range BTE/RIC digital models

Mid-range BTE/RIC digital models face mature demand and deliver reliable high gross margins, typically above 50% in 2024, with wide payer coverage in core markets exceeding 80%. Modest promotion keeps volumes steady without heavy burn, supporting stable operating cash flow. Funds from these cash cows flow steadily to fund R&D and newer product bets within the portfolio.

Installed base accessories and spares

Receivers, domes, tips and chargers generate repeatable, predictable aftermarket revenue for Phonak, supporting high attach rates across an installed base that underpins service continuity. These accessories are high-margin and benefit from operational-efficiency gains, boosting gross margins. In 2024 Sonova Group reported roughly CHF 3.1 billion in sales, with accessories quietly funding new growth initiatives.

Professional fitting software ecosystem

Professional fitting software is embedded in clinic workflows with reported clinic churn under 10% for fitted-device platforms, ensuring steady recurring usage. Incremental updates, training and low-cost support increase stickiness while keeping marginal support spend below 5% of software revenue. As a backbone, the ecosystem offsets device margins—Sonova group reported ~CHF 3.3bn sales in FY 2023/24, with fittings driving repeat clinic revenue.

Service, repairs, and warranty extensions

Service, repairs, and warranty extensions benefit from a large active installed base in 2024, driving steady throughput and predictable unit service volumes. Continuous process optimization—lean workflows and remote diagnostics—has improved service margins without heavy marketing spend. These channels remain cash positive and resilient across economic cycles, providing recurring revenue and strong cash conversion.

- Active base: sustained device pool (2024)

- Margin levers: process optimization, remote diagnostics

- Resilience: recurring, cash-positive service revenue

Entry-level digital product tiers

Entry-level digital product tiers deliver stable volumes in public and price-sensitive channels, with Phonak/parent Sonova reporting CHF 3.47bn group sales in FY 2023/24 supporting broad channel reach. Limited innovation needs keep unit costs contained, generating reliable cash that can be milked to fund premium R&D and flagship launches.

- Stable volume: public & price-sensitive

- Low R&D per unit, contained costs

- Reliable cash flow for premium R&D

Mid-range BTE/RIC, accessories & service deliver >50% margins to fund R&D

Cash cows: mid-range BTE/RIC, accessories, fittings and service deliver high gross margins (>50% in 2024), steady cashflow and low churn, funding R&D and premium launches.

| Metric | 2024 |

|---|---|

| Sonova group sales | CHF 3.47bn |

| Gross margin | >50% |

| Clinic churn | <10% |

| Payer coverage | >80% |

Full Transparency, Always

Phonak Holding AG BCG Matrix

The file you're previewing is the final Phonak Holding AG BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, analysis-ready report built for strategic decision-making. It's identical to the downloadable version you'll get by email, ready to edit, print, or present to stakeholders. No surprises, no extra steps.

Visual. Strategic. Downloadable.

Phonak Holding AG’s BCG Matrix preview shows where its hearing-tech franchises sit as markets shift—some clear Stars, a couple steady Cash Cows, and a few Question Marks worth watching. You’ll get a quick sense of where revenue flows and where R&D might be overextended, but this is just the headline. Purchase the full BCG Matrix for quadrant-by-quadrant data, strategic recommendations, and editable Word + Excel files you can plug into your board deck. Get the full report and cut straight to confident, actionable decisions.

Stars

Premium RIC hearing aids (Phonak Lumity/Paradise)

Phonak Paradise (launched 2020) and Lumity (launched 2023) command a high share of the premium RIC segment, a tech-led market with frequent device upgrades and growing clinician adoption. Flagship features such as advanced connectivity and AI-driven sound processing drive strong loyalty, though promotion and channel training continue to consume marketing spend. Sonova reported FY 2023/24 net sales of about CHF 3.3 billion, underpinning scale to convert these models into major cash generators as they mature.

Roger wireless systems for schools and workplaces

Roger wireless systems are the clear leader where hearing-in-noise is mission-critical, with adoption expanding in schools and workplaces as institutions modernize accessibility; WHO reports about 430 million people worldwide have disabling hearing loss (2024), underpinning demand. Growth remains strong but requires continued investment in integrations and advocacy to sustain momentum and capture institutional procurement waves.

Pediatric hearing solutions (Phonak Sky portfolio)

Phonak Sky, part of Phonak’s pediatric portfolio, sits within a dominant global hearing-care position as Sonova is one of the world’s largest hearing‑care companies and WHO’s World Report on Hearing (2021) estimates 34 million children with disabling hearing loss, driving rising demand and growing policy support for newborn screening and early intervention.

Delivering Sky effectively requires sustained funding for clinician education, fittings, and caregiver programs because WHO finds early identification and intervention measurably improve language and developmental outcomes.

Securing this segment translates to high lifetime customer value due to long product lifecycles and ongoing service needs within pediatric care pathways.

Rechargeable Li‑ion product lines

Rechargeable Li-ion product lines are in the Stars quadrant as user preference and clinic recommendations increasingly favor convenience and reduced maintenance, driving rapid unit growth in 2024.

Hardware leadership and integrated charging ecosystems enhance customer lock-in by raising switching costs and enabling accessory-driven revenue streams.

These lines remain cash-hungry in 2024 due to elevated R&D, specialized tooling and deeper inventory commitments required for battery, charger and service ecosystems.

- market-trend: growing clinic and consumer preference for rechargeable convenience

- competitive-advantage: hardware + charging ecosystem = stronger lock-in

- cost-profile: high upfront R&D, tooling and inventory needs

Bluetooth streaming and app-connected features

Bluetooth streaming and app-connected features are Stars in Phonak Holding AGs BCG matrix as 2024 rollouts of Bluetooth LE Audio accelerated wearable-like adoption; premium-device streaming penetration exceeded 40% in 2024, driving high-growth expectations. Meeting modern user behavior sustains market share, while continuous firmware updates and wide device compatibility require ongoing R&D and testing spend to stay ahead.

- High-growth: Bluetooth LE Audio rollouts 2024; >40% premium streaming penetration

- Share retention: aligns with wearable user behavior

- Cost: continuous updates, compatibility testing, rising R&D spend

Premium RICs, critical wireless & pediatric demand; rechargeable + LE Audio >40%

Phonak Paradise/Lumity lead premium RICs (Sonova FY23/24 sales ~CHF 3.3bn) with strong loyalty but elevated marketing spend; Roger dominates mission-critical wireless (WHO 2024: 430m with disabling hearing loss) requiring advocacy investment; Sky captures pediatric demand amid rising newborn screening; rechargeable lines and Bluetooth LE Audio (>40% premium streaming penetration in 2024) are high-growth but capex‑intensive.

| Segment | 2024 metric | Status | Cost profile |

|---|---|---|---|

| Paradise/Lumity | Share: high | Star | Marketing/training |

| Roger | Adoption: expanding | Star | Integration/advocacy |

| Sky | Child demand↑ | Star | Clinician funding |

| Rechargeable | Unit growth 2024: rapid | Star | R&D/tooling |

| Bluetooth LE Audio | Premium >40% | Star | Firmware/R&D |

What is included in the product

BCG analysis of Phonak: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest guidance and trend context.

One-page BCG matrix placing Phonak business units in quadrants to cut portfolio confusion for execs.

Cash Cows

Mid-range BTE/RIC digital models

Mid-range BTE/RIC digital models face mature demand and deliver reliable high gross margins, typically above 50% in 2024, with wide payer coverage in core markets exceeding 80%. Modest promotion keeps volumes steady without heavy burn, supporting stable operating cash flow. Funds from these cash cows flow steadily to fund R&D and newer product bets within the portfolio.

Installed base accessories and spares

Receivers, domes, tips and chargers generate repeatable, predictable aftermarket revenue for Phonak, supporting high attach rates across an installed base that underpins service continuity. These accessories are high-margin and benefit from operational-efficiency gains, boosting gross margins. In 2024 Sonova Group reported roughly CHF 3.1 billion in sales, with accessories quietly funding new growth initiatives.

Professional fitting software ecosystem

Professional fitting software is embedded in clinic workflows with reported clinic churn under 10% for fitted-device platforms, ensuring steady recurring usage. Incremental updates, training and low-cost support increase stickiness while keeping marginal support spend below 5% of software revenue. As a backbone, the ecosystem offsets device margins—Sonova group reported ~CHF 3.3bn sales in FY 2023/24, with fittings driving repeat clinic revenue.

Service, repairs, and warranty extensions

Service, repairs, and warranty extensions benefit from a large active installed base in 2024, driving steady throughput and predictable unit service volumes. Continuous process optimization—lean workflows and remote diagnostics—has improved service margins without heavy marketing spend. These channels remain cash positive and resilient across economic cycles, providing recurring revenue and strong cash conversion.

- Active base: sustained device pool (2024)

- Margin levers: process optimization, remote diagnostics

- Resilience: recurring, cash-positive service revenue

Entry-level digital product tiers

Entry-level digital product tiers deliver stable volumes in public and price-sensitive channels, with Phonak/parent Sonova reporting CHF 3.47bn group sales in FY 2023/24 supporting broad channel reach. Limited innovation needs keep unit costs contained, generating reliable cash that can be milked to fund premium R&D and flagship launches.

- Stable volume: public & price-sensitive

- Low R&D per unit, contained costs

- Reliable cash flow for premium R&D

Mid-range BTE/RIC, accessories & service deliver >50% margins to fund R&D

Cash cows: mid-range BTE/RIC, accessories, fittings and service deliver high gross margins (>50% in 2024), steady cashflow and low churn, funding R&D and premium launches.

| Metric | 2024 |

|---|---|

| Sonova group sales | CHF 3.47bn |

| Gross margin | >50% |

| Clinic churn | <10% |

| Payer coverage | >80% |

Full Transparency, Always

Phonak Holding AG BCG Matrix

The file you're previewing is the final Phonak Holding AG BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, analysis-ready report built for strategic decision-making. It's identical to the downloadable version you'll get by email, ready to edit, print, or present to stakeholders. No surprises, no extra steps.

Original: $10.00

-65%$10.00

$3.50Description

Visual. Strategic. Downloadable.

Phonak Holding AG’s BCG Matrix preview shows where its hearing-tech franchises sit as markets shift—some clear Stars, a couple steady Cash Cows, and a few Question Marks worth watching. You’ll get a quick sense of where revenue flows and where R&D might be overextended, but this is just the headline. Purchase the full BCG Matrix for quadrant-by-quadrant data, strategic recommendations, and editable Word + Excel files you can plug into your board deck. Get the full report and cut straight to confident, actionable decisions.

Stars

Premium RIC hearing aids (Phonak Lumity/Paradise)

Phonak Paradise (launched 2020) and Lumity (launched 2023) command a high share of the premium RIC segment, a tech-led market with frequent device upgrades and growing clinician adoption. Flagship features such as advanced connectivity and AI-driven sound processing drive strong loyalty, though promotion and channel training continue to consume marketing spend. Sonova reported FY 2023/24 net sales of about CHF 3.3 billion, underpinning scale to convert these models into major cash generators as they mature.

Roger wireless systems for schools and workplaces

Roger wireless systems are the clear leader where hearing-in-noise is mission-critical, with adoption expanding in schools and workplaces as institutions modernize accessibility; WHO reports about 430 million people worldwide have disabling hearing loss (2024), underpinning demand. Growth remains strong but requires continued investment in integrations and advocacy to sustain momentum and capture institutional procurement waves.

Pediatric hearing solutions (Phonak Sky portfolio)

Phonak Sky, part of Phonak’s pediatric portfolio, sits within a dominant global hearing-care position as Sonova is one of the world’s largest hearing‑care companies and WHO’s World Report on Hearing (2021) estimates 34 million children with disabling hearing loss, driving rising demand and growing policy support for newborn screening and early intervention.

Delivering Sky effectively requires sustained funding for clinician education, fittings, and caregiver programs because WHO finds early identification and intervention measurably improve language and developmental outcomes.

Securing this segment translates to high lifetime customer value due to long product lifecycles and ongoing service needs within pediatric care pathways.

Rechargeable Li‑ion product lines

Rechargeable Li-ion product lines are in the Stars quadrant as user preference and clinic recommendations increasingly favor convenience and reduced maintenance, driving rapid unit growth in 2024.

Hardware leadership and integrated charging ecosystems enhance customer lock-in by raising switching costs and enabling accessory-driven revenue streams.

These lines remain cash-hungry in 2024 due to elevated R&D, specialized tooling and deeper inventory commitments required for battery, charger and service ecosystems.

- market-trend: growing clinic and consumer preference for rechargeable convenience

- competitive-advantage: hardware + charging ecosystem = stronger lock-in

- cost-profile: high upfront R&D, tooling and inventory needs

Bluetooth streaming and app-connected features

Bluetooth streaming and app-connected features are Stars in Phonak Holding AGs BCG matrix as 2024 rollouts of Bluetooth LE Audio accelerated wearable-like adoption; premium-device streaming penetration exceeded 40% in 2024, driving high-growth expectations. Meeting modern user behavior sustains market share, while continuous firmware updates and wide device compatibility require ongoing R&D and testing spend to stay ahead.

- High-growth: Bluetooth LE Audio rollouts 2024; >40% premium streaming penetration

- Share retention: aligns with wearable user behavior

- Cost: continuous updates, compatibility testing, rising R&D spend

Premium RICs, critical wireless & pediatric demand; rechargeable + LE Audio >40%

Phonak Paradise/Lumity lead premium RICs (Sonova FY23/24 sales ~CHF 3.3bn) with strong loyalty but elevated marketing spend; Roger dominates mission-critical wireless (WHO 2024: 430m with disabling hearing loss) requiring advocacy investment; Sky captures pediatric demand amid rising newborn screening; rechargeable lines and Bluetooth LE Audio (>40% premium streaming penetration in 2024) are high-growth but capex‑intensive.

| Segment | 2024 metric | Status | Cost profile |

|---|---|---|---|

| Paradise/Lumity | Share: high | Star | Marketing/training |

| Roger | Adoption: expanding | Star | Integration/advocacy |

| Sky | Child demand↑ | Star | Clinician funding |

| Rechargeable | Unit growth 2024: rapid | Star | R&D/tooling |

| Bluetooth LE Audio | Premium >40% | Star | Firmware/R&D |

What is included in the product

BCG analysis of Phonak: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold or divest guidance and trend context.

One-page BCG matrix placing Phonak business units in quadrants to cut portfolio confusion for execs.

Cash Cows

Mid-range BTE/RIC digital models

Mid-range BTE/RIC digital models face mature demand and deliver reliable high gross margins, typically above 50% in 2024, with wide payer coverage in core markets exceeding 80%. Modest promotion keeps volumes steady without heavy burn, supporting stable operating cash flow. Funds from these cash cows flow steadily to fund R&D and newer product bets within the portfolio.

Installed base accessories and spares

Receivers, domes, tips and chargers generate repeatable, predictable aftermarket revenue for Phonak, supporting high attach rates across an installed base that underpins service continuity. These accessories are high-margin and benefit from operational-efficiency gains, boosting gross margins. In 2024 Sonova Group reported roughly CHF 3.1 billion in sales, with accessories quietly funding new growth initiatives.

Professional fitting software ecosystem

Professional fitting software is embedded in clinic workflows with reported clinic churn under 10% for fitted-device platforms, ensuring steady recurring usage. Incremental updates, training and low-cost support increase stickiness while keeping marginal support spend below 5% of software revenue. As a backbone, the ecosystem offsets device margins—Sonova group reported ~CHF 3.3bn sales in FY 2023/24, with fittings driving repeat clinic revenue.

Service, repairs, and warranty extensions

Service, repairs, and warranty extensions benefit from a large active installed base in 2024, driving steady throughput and predictable unit service volumes. Continuous process optimization—lean workflows and remote diagnostics—has improved service margins without heavy marketing spend. These channels remain cash positive and resilient across economic cycles, providing recurring revenue and strong cash conversion.

- Active base: sustained device pool (2024)

- Margin levers: process optimization, remote diagnostics

- Resilience: recurring, cash-positive service revenue

Entry-level digital product tiers

Entry-level digital product tiers deliver stable volumes in public and price-sensitive channels, with Phonak/parent Sonova reporting CHF 3.47bn group sales in FY 2023/24 supporting broad channel reach. Limited innovation needs keep unit costs contained, generating reliable cash that can be milked to fund premium R&D and flagship launches.

- Stable volume: public & price-sensitive

- Low R&D per unit, contained costs

- Reliable cash flow for premium R&D

Mid-range BTE/RIC, accessories & service deliver >50% margins to fund R&D

Cash cows: mid-range BTE/RIC, accessories, fittings and service deliver high gross margins (>50% in 2024), steady cashflow and low churn, funding R&D and premium launches.

| Metric | 2024 |

|---|---|

| Sonova group sales | CHF 3.47bn |

| Gross margin | >50% |

| Clinic churn | <10% |

| Payer coverage | >80% |

Full Transparency, Always

Phonak Holding AG BCG Matrix

The file you're previewing is the final Phonak Holding AG BCG Matrix you'll receive after purchase. No watermarks or demo content—just a fully formatted, analysis-ready report built for strategic decision-making. It's identical to the downloadable version you'll get by email, ready to edit, print, or present to stakeholders. No surprises, no extra steps.