Sony Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

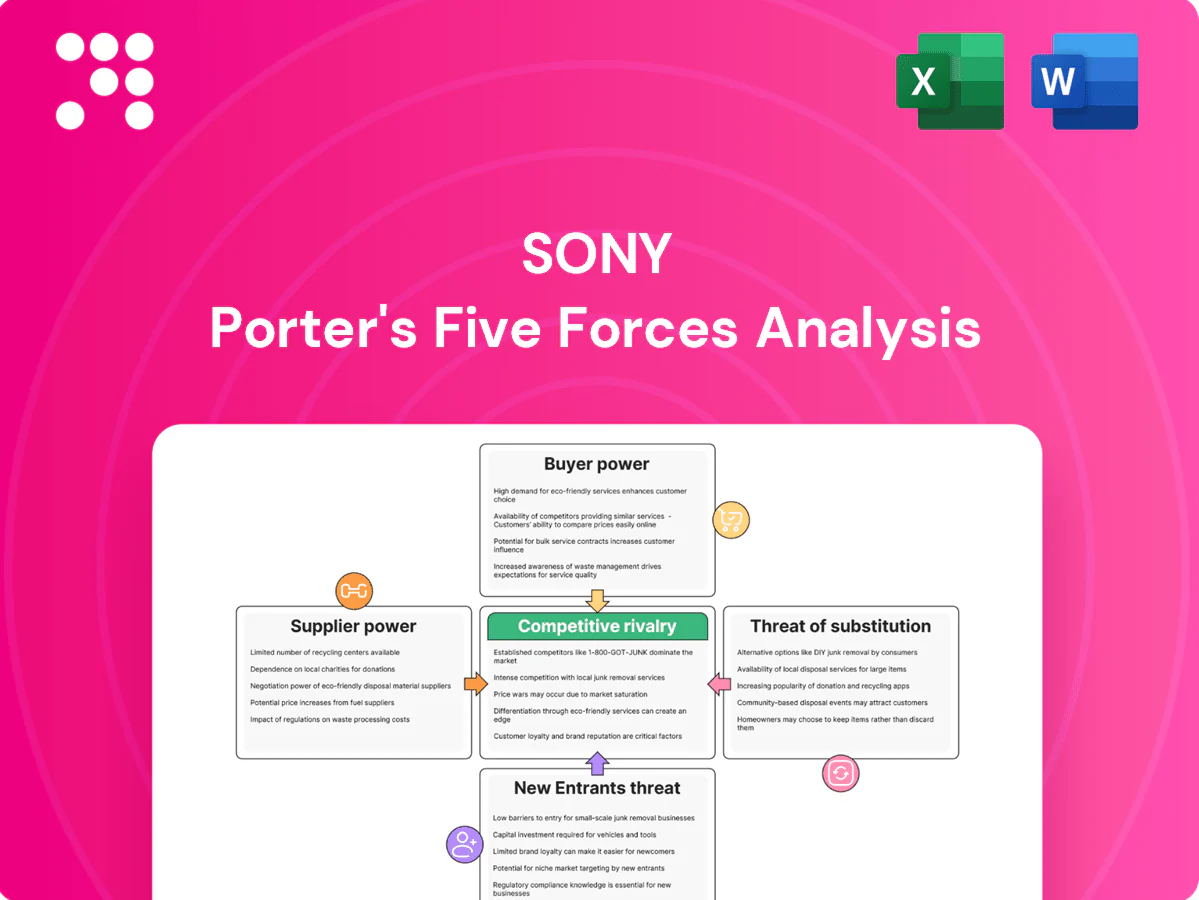

Sony's Porter's Five Forces highlights competitive rivalry across consoles, content, and electronics, supplier and buyer power, threat of substitutes, and barriers to entry. This snapshot shows strong brand and diversified revenue but rising digital distribution and platform competition increase pressure. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Key chip vendors

Sony depends on advanced CPUs/GPUs, memory and display drivers sourced from a concentrated supplier set where TSMC held roughly 53% of foundry share and Samsung about 18% in 2023–24, giving vendors leverage. Leading-edge node scarcity (3nm/5nm capacity tightness) raises pricing and priority risks despite Sony’s long-term contracts and scale. Dual-sourcing and selective in-house design reduce exposure.

Critical components & materials

High-spec lenses, image sensors, batteries, rare earths and OLED panels are concentrated supply pools, raising supplier power; Sony held roughly 50% of the global CMOS image‑sensor market in 2024, but panels and batteries remain vendor‑dependent. Tight quality thresholds reduce switchability without performance loss, while China controls >60% of rare‑earth processing. Sony offsets exposure via sensor leadership; strategic inventories and JVs (supplier partnerships) temper volatility.

Creative talent & IP

Actors, directors, game studios, music artists and rights holders act as quasi-suppliers whose marquee scarcity and hit-driven economics boost bargaining power; top exclusivity bids and talent fees materially raise content costs. Sony Music accounts for roughly a quarter of global recorded-music market (≈25% in 2023), and long-term label catalogs give Sony Music/Pictures negotiating weight, while Sony’s cross-media portfolio cushions cost spikes.

Platform & cloud partners

Contract manufacturers

- EMS exposure: reliance vs leverage

- Specialized-line bottlenecks

- Brand/demand predictability aids terms

- Process transfer dilutes supplier power

Foundry and cloud concentration heighten supplier risk; dual-sourcing, JVs, multi-cloud mitigate

Sony faces concentrated suppliers: TSMC ~53%/Samsung ~18% foundry (2023–24), CMOS sensors ~50% share gives Sony leverage but panels, batteries and rare‑earths (>60% processing in China) raise supplier power. Content talent and cloud (AWS 32%/Azure 22%/GCP 12% in 2024) add bargaining pressure; dual‑sourcing, inventories, JVs and multi‑cloud mitigate risks.

| Supplier | 2024 metric | Sony position |

|---|---|---|

| Foundry | TSMC 53%/Samsung 18% | Long‑term contracts |

| Image sensors | Sony ~50% market | Leadership mitigant |

| Cloud/content | AWS32%/AZ22%/GCP12% | Multi‑cloud/own infra |

What is included in the product

Tailored exclusively for Sony, analyzing its position within its competitive landscape. Identifies disruptive forces, substitutes, and the bargaining power of suppliers and buyers that shape Sony’s pricing, profitability, and market entry dynamics.

Clear one-sheet Porter's Five Forces for Sony—instantly shows competitive pressure and strategic levers to relieve decision-making pain. Customize force levels, swap in your data, and export clean visuals for decks or dashboards without macros.

Customers Bargaining Power

Price-aware consumers

Price-aware consumers compare features and prices instantly, boosting their bargaining power; by 2024 roughly 70% of electronics buyers used price-comparison tools, increasing switching. Reviews and social proof further amplify churn risk, especially in mid-tier segments where ASPs face intense price pressure and discounting. Premium Sony products retain higher ASPs, while bundles and ecosystem perks (PlayStation, Headphones, Imaging tie-ins) help preserve value and reduce churn.

Retail & e-commerce channels

Big-box retailers and online platforms extract placement, coop and returns concessions, with control over peak-season traffic amplifying leverage; Sony reported consolidated revenue of about 13.4 trillion yen for fiscal 2023 (year ended Mar 2024), highlighting the stakes. Direct-to-consumer channels and Sony Stores lower dependency on those partners, while DTC data improves pricing and product-mix decisions, boosting margin capture and inventory turns.

Gamers & subscribers

PlayStation users can churn to rival consoles, PC, or cloud services, but over 100 million PSN users and roughly a 50 million PS5 installed base by 2024 raise switching costs; network effects from multiplayer and communities strengthen lock-in. Large digital libraries and exclusive titles (first‑party releases and timed exclusives) further lower buyer power. Subscription tiers—around 60 million PlayStation Plus/paid subscribers—create price sensitivity yet increase stickiness. Regular content drops and backward compatibility sustain engagement and reduce churn.

Enterprise & pro clients

Enterprise and pro broadcast, imaging, and cinema customers demand high reliability and service SLAs (commonly 99.9% uptime) and use customization/integration needs to negotiate pricing and support terms, but Sony’s specialized performance and lower TCO for high-end workflows constrain switching; multi-year (typically 3–5 year) service contracts further lock in terms.

- SLAs: 99.9% uptime

- Contract length: 3–5 years

- Negotiation leverage: customization/integration

- Switching constraint: specialized performance/TCO

Advertisers & distributors

- Ad spend 2024: ~$885B

- Leverage: fragmentation + alternative channels

- Defense: IP, franchises, scale

- Yield: data targeting, cross-portfolio bundles

Price transparency spurs switching as 70% compare; console lock-in stays

Price-aware consumers compare features and prices instantly; by 2024 ~70% of electronics buyers used price-comparison tools, raising switching. Retailers and platforms extract placement/coop concessions; Sony reported ~13.4 trillion yen revenue (FY2023), increasing partner leverage. PlayStation lock-in (~50M PS5, ~100M PSN, ~60M subs) and exclusives reduce buyer power. Enterprise buyers use 3–5 year contracts and 99.9% SLAs to negotiate.

| Metric | Value (2024) |

|---|---|

| Price-comparison users | ~70% |

| Sony revenue (FY2023) | ~13.4T yen |

| PS5 installed base | ~50M |

| PSN users | ~100M |

| PlayStation subs | ~60M |

| Global ad spend | ~$885B |

| SLA | 99.9% |

| Contract length | 3–5 yrs |

Full Version Awaits

Sony Porter's Five Forces Analysis

This Sony Porter’s Five Forces Analysis preview is the exact, professionally formatted document you’ll receive immediately after purchase—no mockups or placeholders. It delivers a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, ready for immediate use.

Go Beyond the Preview—Access the Full Strategic Report

Sony's Porter's Five Forces highlights competitive rivalry across consoles, content, and electronics, supplier and buyer power, threat of substitutes, and barriers to entry. This snapshot shows strong brand and diversified revenue but rising digital distribution and platform competition increase pressure. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Key chip vendors

Sony depends on advanced CPUs/GPUs, memory and display drivers sourced from a concentrated supplier set where TSMC held roughly 53% of foundry share and Samsung about 18% in 2023–24, giving vendors leverage. Leading-edge node scarcity (3nm/5nm capacity tightness) raises pricing and priority risks despite Sony’s long-term contracts and scale. Dual-sourcing and selective in-house design reduce exposure.

Critical components & materials

High-spec lenses, image sensors, batteries, rare earths and OLED panels are concentrated supply pools, raising supplier power; Sony held roughly 50% of the global CMOS image‑sensor market in 2024, but panels and batteries remain vendor‑dependent. Tight quality thresholds reduce switchability without performance loss, while China controls >60% of rare‑earth processing. Sony offsets exposure via sensor leadership; strategic inventories and JVs (supplier partnerships) temper volatility.

Creative talent & IP

Actors, directors, game studios, music artists and rights holders act as quasi-suppliers whose marquee scarcity and hit-driven economics boost bargaining power; top exclusivity bids and talent fees materially raise content costs. Sony Music accounts for roughly a quarter of global recorded-music market (≈25% in 2023), and long-term label catalogs give Sony Music/Pictures negotiating weight, while Sony’s cross-media portfolio cushions cost spikes.

Platform & cloud partners

Contract manufacturers

- EMS exposure: reliance vs leverage

- Specialized-line bottlenecks

- Brand/demand predictability aids terms

- Process transfer dilutes supplier power

Foundry and cloud concentration heighten supplier risk; dual-sourcing, JVs, multi-cloud mitigate

Sony faces concentrated suppliers: TSMC ~53%/Samsung ~18% foundry (2023–24), CMOS sensors ~50% share gives Sony leverage but panels, batteries and rare‑earths (>60% processing in China) raise supplier power. Content talent and cloud (AWS 32%/Azure 22%/GCP 12% in 2024) add bargaining pressure; dual‑sourcing, inventories, JVs and multi‑cloud mitigate risks.

| Supplier | 2024 metric | Sony position |

|---|---|---|

| Foundry | TSMC 53%/Samsung 18% | Long‑term contracts |

| Image sensors | Sony ~50% market | Leadership mitigant |

| Cloud/content | AWS32%/AZ22%/GCP12% | Multi‑cloud/own infra |

What is included in the product

Tailored exclusively for Sony, analyzing its position within its competitive landscape. Identifies disruptive forces, substitutes, and the bargaining power of suppliers and buyers that shape Sony’s pricing, profitability, and market entry dynamics.

Clear one-sheet Porter's Five Forces for Sony—instantly shows competitive pressure and strategic levers to relieve decision-making pain. Customize force levels, swap in your data, and export clean visuals for decks or dashboards without macros.

Customers Bargaining Power

Price-aware consumers

Price-aware consumers compare features and prices instantly, boosting their bargaining power; by 2024 roughly 70% of electronics buyers used price-comparison tools, increasing switching. Reviews and social proof further amplify churn risk, especially in mid-tier segments where ASPs face intense price pressure and discounting. Premium Sony products retain higher ASPs, while bundles and ecosystem perks (PlayStation, Headphones, Imaging tie-ins) help preserve value and reduce churn.

Retail & e-commerce channels

Big-box retailers and online platforms extract placement, coop and returns concessions, with control over peak-season traffic amplifying leverage; Sony reported consolidated revenue of about 13.4 trillion yen for fiscal 2023 (year ended Mar 2024), highlighting the stakes. Direct-to-consumer channels and Sony Stores lower dependency on those partners, while DTC data improves pricing and product-mix decisions, boosting margin capture and inventory turns.

Gamers & subscribers

PlayStation users can churn to rival consoles, PC, or cloud services, but over 100 million PSN users and roughly a 50 million PS5 installed base by 2024 raise switching costs; network effects from multiplayer and communities strengthen lock-in. Large digital libraries and exclusive titles (first‑party releases and timed exclusives) further lower buyer power. Subscription tiers—around 60 million PlayStation Plus/paid subscribers—create price sensitivity yet increase stickiness. Regular content drops and backward compatibility sustain engagement and reduce churn.

Enterprise & pro clients

Enterprise and pro broadcast, imaging, and cinema customers demand high reliability and service SLAs (commonly 99.9% uptime) and use customization/integration needs to negotiate pricing and support terms, but Sony’s specialized performance and lower TCO for high-end workflows constrain switching; multi-year (typically 3–5 year) service contracts further lock in terms.

- SLAs: 99.9% uptime

- Contract length: 3–5 years

- Negotiation leverage: customization/integration

- Switching constraint: specialized performance/TCO

Advertisers & distributors

- Ad spend 2024: ~$885B

- Leverage: fragmentation + alternative channels

- Defense: IP, franchises, scale

- Yield: data targeting, cross-portfolio bundles

Price transparency spurs switching as 70% compare; console lock-in stays

Price-aware consumers compare features and prices instantly; by 2024 ~70% of electronics buyers used price-comparison tools, raising switching. Retailers and platforms extract placement/coop concessions; Sony reported ~13.4 trillion yen revenue (FY2023), increasing partner leverage. PlayStation lock-in (~50M PS5, ~100M PSN, ~60M subs) and exclusives reduce buyer power. Enterprise buyers use 3–5 year contracts and 99.9% SLAs to negotiate.

| Metric | Value (2024) |

|---|---|

| Price-comparison users | ~70% |

| Sony revenue (FY2023) | ~13.4T yen |

| PS5 installed base | ~50M |

| PSN users | ~100M |

| PlayStation subs | ~60M |

| Global ad spend | ~$885B |

| SLA | 99.9% |

| Contract length | 3–5 yrs |

Full Version Awaits

Sony Porter's Five Forces Analysis

This Sony Porter’s Five Forces Analysis preview is the exact, professionally formatted document you’ll receive immediately after purchase—no mockups or placeholders. It delivers a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, ready for immediate use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Sony's Porter's Five Forces highlights competitive rivalry across consoles, content, and electronics, supplier and buyer power, threat of substitutes, and barriers to entry. This snapshot shows strong brand and diversified revenue but rising digital distribution and platform competition increase pressure. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable implications for investment and strategy.

Suppliers Bargaining Power

Key chip vendors

Sony depends on advanced CPUs/GPUs, memory and display drivers sourced from a concentrated supplier set where TSMC held roughly 53% of foundry share and Samsung about 18% in 2023–24, giving vendors leverage. Leading-edge node scarcity (3nm/5nm capacity tightness) raises pricing and priority risks despite Sony’s long-term contracts and scale. Dual-sourcing and selective in-house design reduce exposure.

Critical components & materials

High-spec lenses, image sensors, batteries, rare earths and OLED panels are concentrated supply pools, raising supplier power; Sony held roughly 50% of the global CMOS image‑sensor market in 2024, but panels and batteries remain vendor‑dependent. Tight quality thresholds reduce switchability without performance loss, while China controls >60% of rare‑earth processing. Sony offsets exposure via sensor leadership; strategic inventories and JVs (supplier partnerships) temper volatility.

Creative talent & IP

Actors, directors, game studios, music artists and rights holders act as quasi-suppliers whose marquee scarcity and hit-driven economics boost bargaining power; top exclusivity bids and talent fees materially raise content costs. Sony Music accounts for roughly a quarter of global recorded-music market (≈25% in 2023), and long-term label catalogs give Sony Music/Pictures negotiating weight, while Sony’s cross-media portfolio cushions cost spikes.

Platform & cloud partners

Contract manufacturers

- EMS exposure: reliance vs leverage

- Specialized-line bottlenecks

- Brand/demand predictability aids terms

- Process transfer dilutes supplier power

Foundry and cloud concentration heighten supplier risk; dual-sourcing, JVs, multi-cloud mitigate

Sony faces concentrated suppliers: TSMC ~53%/Samsung ~18% foundry (2023–24), CMOS sensors ~50% share gives Sony leverage but panels, batteries and rare‑earths (>60% processing in China) raise supplier power. Content talent and cloud (AWS 32%/Azure 22%/GCP 12% in 2024) add bargaining pressure; dual‑sourcing, inventories, JVs and multi‑cloud mitigate risks.

| Supplier | 2024 metric | Sony position |

|---|---|---|

| Foundry | TSMC 53%/Samsung 18% | Long‑term contracts |

| Image sensors | Sony ~50% market | Leadership mitigant |

| Cloud/content | AWS32%/AZ22%/GCP12% | Multi‑cloud/own infra |

What is included in the product

Tailored exclusively for Sony, analyzing its position within its competitive landscape. Identifies disruptive forces, substitutes, and the bargaining power of suppliers and buyers that shape Sony’s pricing, profitability, and market entry dynamics.

Clear one-sheet Porter's Five Forces for Sony—instantly shows competitive pressure and strategic levers to relieve decision-making pain. Customize force levels, swap in your data, and export clean visuals for decks or dashboards without macros.

Customers Bargaining Power

Price-aware consumers

Price-aware consumers compare features and prices instantly, boosting their bargaining power; by 2024 roughly 70% of electronics buyers used price-comparison tools, increasing switching. Reviews and social proof further amplify churn risk, especially in mid-tier segments where ASPs face intense price pressure and discounting. Premium Sony products retain higher ASPs, while bundles and ecosystem perks (PlayStation, Headphones, Imaging tie-ins) help preserve value and reduce churn.

Retail & e-commerce channels

Big-box retailers and online platforms extract placement, coop and returns concessions, with control over peak-season traffic amplifying leverage; Sony reported consolidated revenue of about 13.4 trillion yen for fiscal 2023 (year ended Mar 2024), highlighting the stakes. Direct-to-consumer channels and Sony Stores lower dependency on those partners, while DTC data improves pricing and product-mix decisions, boosting margin capture and inventory turns.

Gamers & subscribers

PlayStation users can churn to rival consoles, PC, or cloud services, but over 100 million PSN users and roughly a 50 million PS5 installed base by 2024 raise switching costs; network effects from multiplayer and communities strengthen lock-in. Large digital libraries and exclusive titles (first‑party releases and timed exclusives) further lower buyer power. Subscription tiers—around 60 million PlayStation Plus/paid subscribers—create price sensitivity yet increase stickiness. Regular content drops and backward compatibility sustain engagement and reduce churn.

Enterprise & pro clients

Enterprise and pro broadcast, imaging, and cinema customers demand high reliability and service SLAs (commonly 99.9% uptime) and use customization/integration needs to negotiate pricing and support terms, but Sony’s specialized performance and lower TCO for high-end workflows constrain switching; multi-year (typically 3–5 year) service contracts further lock in terms.

- SLAs: 99.9% uptime

- Contract length: 3–5 years

- Negotiation leverage: customization/integration

- Switching constraint: specialized performance/TCO

Advertisers & distributors

- Ad spend 2024: ~$885B

- Leverage: fragmentation + alternative channels

- Defense: IP, franchises, scale

- Yield: data targeting, cross-portfolio bundles

Price transparency spurs switching as 70% compare; console lock-in stays

Price-aware consumers compare features and prices instantly; by 2024 ~70% of electronics buyers used price-comparison tools, raising switching. Retailers and platforms extract placement/coop concessions; Sony reported ~13.4 trillion yen revenue (FY2023), increasing partner leverage. PlayStation lock-in (~50M PS5, ~100M PSN, ~60M subs) and exclusives reduce buyer power. Enterprise buyers use 3–5 year contracts and 99.9% SLAs to negotiate.

| Metric | Value (2024) |

|---|---|

| Price-comparison users | ~70% |

| Sony revenue (FY2023) | ~13.4T yen |

| PS5 installed base | ~50M |

| PSN users | ~100M |

| PlayStation subs | ~60M |

| Global ad spend | ~$885B |

| SLA | 99.9% |

| Contract length | 3–5 yrs |

Full Version Awaits

Sony Porter's Five Forces Analysis

This Sony Porter’s Five Forces Analysis preview is the exact, professionally formatted document you’ll receive immediately after purchase—no mockups or placeholders. It delivers a complete assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution, ready for immediate use.