Soudronic GmbH Porter's Five Forces Analysis

Don't Miss the Bigger Picture

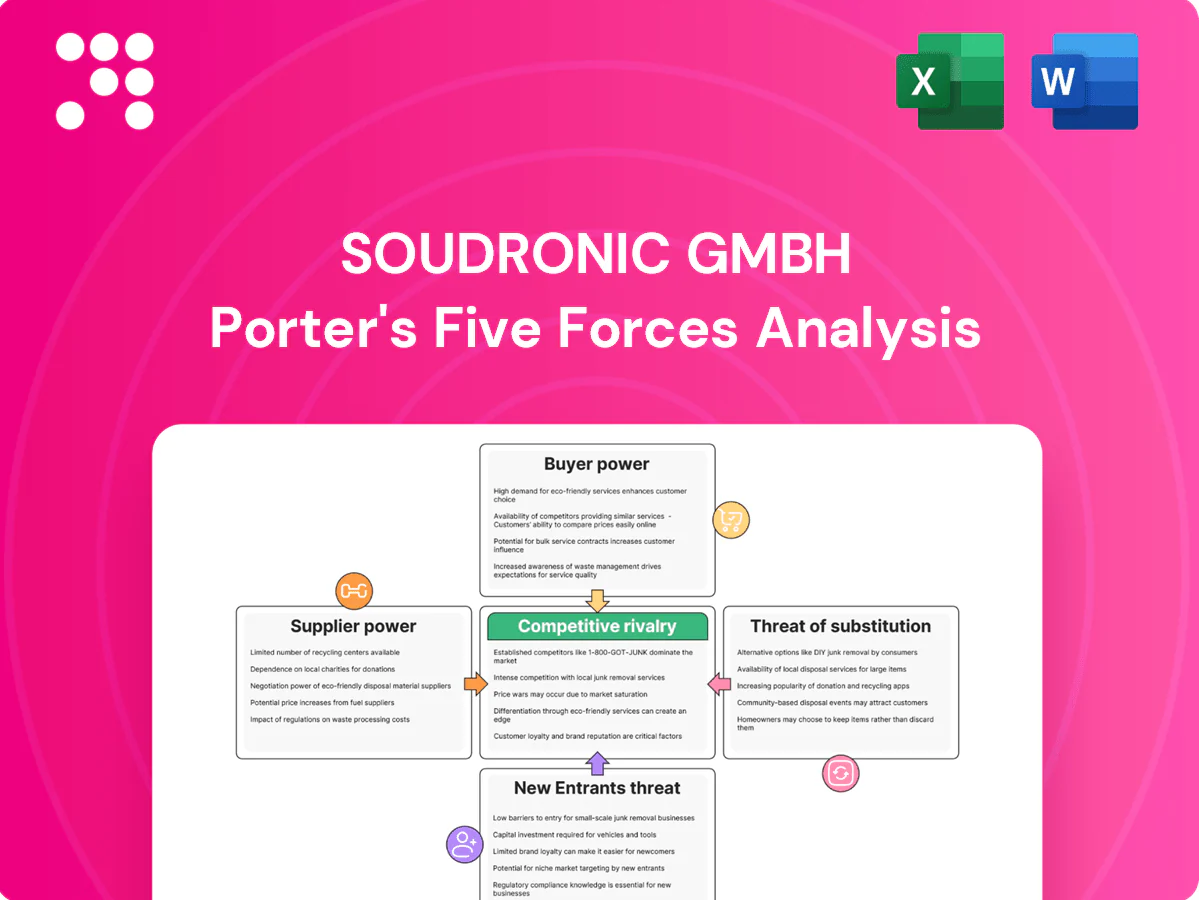

Soudronic GmbH's Porter's Five Forces analysis highlights strong supplier relationships, moderate buyer power, high competitive rivalry in metal forming, and manageable threat of substitutes but rising pressure from automation-focused entrants. This snapshot surfaces key strategic tensions and operational risks. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialty component dependence

Soudronic depends on precision parts—copper electrodes, power electronics, servos and control systems—sourced from a narrow pool of qualified vendors, creating high switching costs and supply-risk exposure. Qualification and validation for high-duty welding components commonly exceed 6 months, amplifying supplier leverage and lead-time vulnerability. Dual-sourcing and in-house engineering reduce but do not eliminate this specialized dependency.

Advanced materials pricing

Prices for conductive alloys, stainless steels and high-spec insulators drive Soudronic’s BOM — LME nickel averaged about $26,000/tonne in 2024 and copper near $9,500/tonne, lifting input bills. Commodity volatility and energy surcharges (often 3–7% on metal invoices) can squeeze margins. Long-term contracts hedge price swings but limit near-term sourcing flexibility. Passing surcharges to customers is feasible but risks losing competitive bids.

Automation and controls ecosystems

Reliance on major PLC, drive and vision suppliers (Siemens, Rockwell, Mitsubishi et al.) creates ecosystem lock-in, with the top vendors accounting for roughly 60% of PLC market revenue in 2024. Firmware compatibility and safety certifications lengthen validation cycles and typically add switching costs measured in months and hundreds of thousands of euros. Suppliers with broad service networks can dictate support terms across regions, while co-development roadmaps have reduced integration time in many projects by up to 30%, balancing power through joint value creation.

Aftermarket consumables

Electrode tips, welding wheels and wear parts are recurring, quality-critical inputs that often appear on approved-vendor lists, constraining alternatives and raising supplier bargaining power; the global welding consumables market reached about USD 18.6 billion in 2024, underscoring supplier scale. Predictable purchase volumes allow Soudronic to negotiate volume discounts (commonly 5–12%), while Soudronic’s proprietary designs can standardize interfaces to widen sourcing and reduce dependence.

- Approved-vendor concentration: raises supplier leverage

- Market size 2024: USD 18.6 billion

- Negotiated discounts: ~5–12% with volume visibility

- Design standardization: expands supplier pool, lowers risk

Logistics and lead-time constraints

Long lead times for custom assemblies and power modules (typically 18–24 weeks in 2024 versus 8–12 pre‑pandemic) increase supplier leverage over Soudronic, forcing higher reliance on expediting and premium freight as European/global disruptions raised expediting costs by an estimated 25% in 2023–24. Framework agreements and buffer stocks reduce exposure but lock up working capital (inventory carrying costs ~20–25% annually). Supplier development programs have shown OTD improvements of ~10–15% within 12–18 months in comparable metalworking supply chains.

- Long lead times: 18–24 weeks (2024)

- Expediting cost increase: ~25% (2023–24)

- Inventory carrying cost: ~20–25% p.a.

- Supplier development OTD gain: ~10–15% in 12–18 months

Supplier power tight: 18-24 weeks lead times, commodity cost pressure

Soudronic faces high supplier power from specialized vendors (qualification >6 months), concentrated PLC/welding consumables markets and long lead times (18–24 wks in 2024), raising switching costs and expediting spend. Volume discounts (5–12%) and in-house design reduce but do not neutralize leverage. Commodity inputs (LME Cu ~$9,500/t; Ni ~$26,000/t in 2024) add margin pressure.

| Metric | 2024 value |

|---|---|

| Lead time | 18–24 weeks |

| Copper (LME) | ~$9,500/tonne |

| Nickel (LME) | ~$26,000/tonne |

| Volume discounts | 5–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Soudronic GmbH uncovering key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and disruptive market risks affecting pricing and profitability; strategic commentary highlights barriers protecting incumbency and actionable insights for investors and management.

Concise one-sheet Porter's Five Forces for Soudronic GmbH—clean, simplified layout ready to copy into pitch decks or boardroom slides, instantly highlighting competitive pressures and strategic priorities.

Customers Bargaining Power

Concentrated can-makers

Large global and regional can-makers drive the majority of demand for Soudronic tooling and equipment, with global beverage can production approaching 350 billion cans per year in 2024, concentrating purchasing power with a handful of buyers.

Their scale and multi-plant ordering creates strong price and term leverage, pushing suppliers toward thin margins and high-volume discounts.

Preferred-vendor lists and global frame agreements intensify margin pressure while winning reference accounts remains critical for pipeline visibility and securing long-term multi-million-euro contracts.

Capex scrutiny and ROI

Buyers assess capex by modeled payback under 24 months using throughput, OEE (baseline 50–70%), scrap rate reductions (target 10–30%) and energy cuts (often 5–15%) to justify spend.

Competitive tenders demand detailed TCO and 8–10 year lifecycle support proposals; 2024 procurement studies show >60% require full lifecycle cost models.

Deferred capex during downturns gives buyers timing leverage and makes performance guarantees and uptime SLAs (99%+ targets) central bargaining chips.

Technical specification power

Customers impose strict specs for seam integrity, line speed and multiple can formats, forcing Soudronic to meet tight tolerances and uptime targets.

Customization demands often shift significant engineering and testing costs onto the OEM, increasing CAPEX for bespoke tooling and controls.

Open interfaces and line-integration support such as OPC UA and PLC compatibility are commonly mandatory, adding integration overhead.

Compliance with food-grade and safety standards including ISO 22000, HACCP, BRCGS and CE increases validation, documentation and audit burdens.

Aftermarket negotiation

Aftermarket negotiation is critical as spare parts, tooling, and multi-year service contracts are recurring and contestable revenue streams; buyers press for multi-year discounts and response-time SLAs that compress OEM margins. Third-party service providers and in-house maintenance increasingly threaten Soudronic’s aftermarket share by offering lower-cost alternatives. Bundled parts-and-service offerings can lock customers in but typically require discounted pricing to retain share.

- Spare parts, tooling, service = recurring & contestable

- Buyers demand multi-year discounts + response-time SLAs

- Third-party/in-house maintenance pressure OEM margins

- Bundled offerings drive retention at discounted rates

Switching and multi-sourcing

Larger can-makers such as Ball, Crown and Ardagh commonly maintain dual sourcing across welding lines to hedge supply risk; in 2024 the global beverage can market exceeded 350 billion units, amplifying the need for redundancy. Dual sourcing reduces vendor lock-in and strengthens buyer leverage at contract renewals, but switching still requires retraining, spare-inventory duplication and downtime. Proven reliability and retrofit ease materially lower switching incentives.

- Dual sourcing: common among majors

- Market scale 2024: >350 billion cans

- Buyer leverage: stronger at renewal

- Switching costs: retraining, spares, downtime

- Mitigation: reliability and retrofit simplicity reduce churn

Buyers leverage dominates >350B-can market; aftermarket discounts squeeze OEM margins

Major global can-makers concentrate demand (global beverage can market >350 billion units in 2024), giving buyers strong price/term leverage, frequent dual sourcing and emphasis on 24-month payback models; >60% of tenders require full lifecycle TCO. Aftermarket is contestable—buyers push multi-year discounts and 99%+ uptime SLAs, pressuring OEM margins.

| Metric | 2024 | Impact |

|---|---|---|

| Global cans | >350B units | High buyer scale |

| Tenders w/ TCO | >60% | Lifecycle pricing required |

| Target OEE | 50–70% | Capex justification |

Same Document Delivered

Soudronic GmbH Porter's Five Forces Analysis

This Soudronic GmbH Porter's Five Forces analysis delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to the metal packaging sector. This preview is the exact document you'll receive instantly after purchase—fully formatted and ready to use. No placeholders, no samples—what you see is what you download.

Don't Miss the Bigger Picture

Soudronic GmbH's Porter's Five Forces analysis highlights strong supplier relationships, moderate buyer power, high competitive rivalry in metal forming, and manageable threat of substitutes but rising pressure from automation-focused entrants. This snapshot surfaces key strategic tensions and operational risks. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialty component dependence

Soudronic depends on precision parts—copper electrodes, power electronics, servos and control systems—sourced from a narrow pool of qualified vendors, creating high switching costs and supply-risk exposure. Qualification and validation for high-duty welding components commonly exceed 6 months, amplifying supplier leverage and lead-time vulnerability. Dual-sourcing and in-house engineering reduce but do not eliminate this specialized dependency.

Advanced materials pricing

Prices for conductive alloys, stainless steels and high-spec insulators drive Soudronic’s BOM — LME nickel averaged about $26,000/tonne in 2024 and copper near $9,500/tonne, lifting input bills. Commodity volatility and energy surcharges (often 3–7% on metal invoices) can squeeze margins. Long-term contracts hedge price swings but limit near-term sourcing flexibility. Passing surcharges to customers is feasible but risks losing competitive bids.

Automation and controls ecosystems

Reliance on major PLC, drive and vision suppliers (Siemens, Rockwell, Mitsubishi et al.) creates ecosystem lock-in, with the top vendors accounting for roughly 60% of PLC market revenue in 2024. Firmware compatibility and safety certifications lengthen validation cycles and typically add switching costs measured in months and hundreds of thousands of euros. Suppliers with broad service networks can dictate support terms across regions, while co-development roadmaps have reduced integration time in many projects by up to 30%, balancing power through joint value creation.

Aftermarket consumables

Electrode tips, welding wheels and wear parts are recurring, quality-critical inputs that often appear on approved-vendor lists, constraining alternatives and raising supplier bargaining power; the global welding consumables market reached about USD 18.6 billion in 2024, underscoring supplier scale. Predictable purchase volumes allow Soudronic to negotiate volume discounts (commonly 5–12%), while Soudronic’s proprietary designs can standardize interfaces to widen sourcing and reduce dependence.

- Approved-vendor concentration: raises supplier leverage

- Market size 2024: USD 18.6 billion

- Negotiated discounts: ~5–12% with volume visibility

- Design standardization: expands supplier pool, lowers risk

Logistics and lead-time constraints

Long lead times for custom assemblies and power modules (typically 18–24 weeks in 2024 versus 8–12 pre‑pandemic) increase supplier leverage over Soudronic, forcing higher reliance on expediting and premium freight as European/global disruptions raised expediting costs by an estimated 25% in 2023–24. Framework agreements and buffer stocks reduce exposure but lock up working capital (inventory carrying costs ~20–25% annually). Supplier development programs have shown OTD improvements of ~10–15% within 12–18 months in comparable metalworking supply chains.

- Long lead times: 18–24 weeks (2024)

- Expediting cost increase: ~25% (2023–24)

- Inventory carrying cost: ~20–25% p.a.

- Supplier development OTD gain: ~10–15% in 12–18 months

Supplier power tight: 18-24 weeks lead times, commodity cost pressure

Soudronic faces high supplier power from specialized vendors (qualification >6 months), concentrated PLC/welding consumables markets and long lead times (18–24 wks in 2024), raising switching costs and expediting spend. Volume discounts (5–12%) and in-house design reduce but do not neutralize leverage. Commodity inputs (LME Cu ~$9,500/t; Ni ~$26,000/t in 2024) add margin pressure.

| Metric | 2024 value |

|---|---|

| Lead time | 18–24 weeks |

| Copper (LME) | ~$9,500/tonne |

| Nickel (LME) | ~$26,000/tonne |

| Volume discounts | 5–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Soudronic GmbH uncovering key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and disruptive market risks affecting pricing and profitability; strategic commentary highlights barriers protecting incumbency and actionable insights for investors and management.

Concise one-sheet Porter's Five Forces for Soudronic GmbH—clean, simplified layout ready to copy into pitch decks or boardroom slides, instantly highlighting competitive pressures and strategic priorities.

Customers Bargaining Power

Concentrated can-makers

Large global and regional can-makers drive the majority of demand for Soudronic tooling and equipment, with global beverage can production approaching 350 billion cans per year in 2024, concentrating purchasing power with a handful of buyers.

Their scale and multi-plant ordering creates strong price and term leverage, pushing suppliers toward thin margins and high-volume discounts.

Preferred-vendor lists and global frame agreements intensify margin pressure while winning reference accounts remains critical for pipeline visibility and securing long-term multi-million-euro contracts.

Capex scrutiny and ROI

Buyers assess capex by modeled payback under 24 months using throughput, OEE (baseline 50–70%), scrap rate reductions (target 10–30%) and energy cuts (often 5–15%) to justify spend.

Competitive tenders demand detailed TCO and 8–10 year lifecycle support proposals; 2024 procurement studies show >60% require full lifecycle cost models.

Deferred capex during downturns gives buyers timing leverage and makes performance guarantees and uptime SLAs (99%+ targets) central bargaining chips.

Technical specification power

Customers impose strict specs for seam integrity, line speed and multiple can formats, forcing Soudronic to meet tight tolerances and uptime targets.

Customization demands often shift significant engineering and testing costs onto the OEM, increasing CAPEX for bespoke tooling and controls.

Open interfaces and line-integration support such as OPC UA and PLC compatibility are commonly mandatory, adding integration overhead.

Compliance with food-grade and safety standards including ISO 22000, HACCP, BRCGS and CE increases validation, documentation and audit burdens.

Aftermarket negotiation

Aftermarket negotiation is critical as spare parts, tooling, and multi-year service contracts are recurring and contestable revenue streams; buyers press for multi-year discounts and response-time SLAs that compress OEM margins. Third-party service providers and in-house maintenance increasingly threaten Soudronic’s aftermarket share by offering lower-cost alternatives. Bundled parts-and-service offerings can lock customers in but typically require discounted pricing to retain share.

- Spare parts, tooling, service = recurring & contestable

- Buyers demand multi-year discounts + response-time SLAs

- Third-party/in-house maintenance pressure OEM margins

- Bundled offerings drive retention at discounted rates

Switching and multi-sourcing

Larger can-makers such as Ball, Crown and Ardagh commonly maintain dual sourcing across welding lines to hedge supply risk; in 2024 the global beverage can market exceeded 350 billion units, amplifying the need for redundancy. Dual sourcing reduces vendor lock-in and strengthens buyer leverage at contract renewals, but switching still requires retraining, spare-inventory duplication and downtime. Proven reliability and retrofit ease materially lower switching incentives.

- Dual sourcing: common among majors

- Market scale 2024: >350 billion cans

- Buyer leverage: stronger at renewal

- Switching costs: retraining, spares, downtime

- Mitigation: reliability and retrofit simplicity reduce churn

Buyers leverage dominates >350B-can market; aftermarket discounts squeeze OEM margins

Major global can-makers concentrate demand (global beverage can market >350 billion units in 2024), giving buyers strong price/term leverage, frequent dual sourcing and emphasis on 24-month payback models; >60% of tenders require full lifecycle TCO. Aftermarket is contestable—buyers push multi-year discounts and 99%+ uptime SLAs, pressuring OEM margins.

| Metric | 2024 | Impact |

|---|---|---|

| Global cans | >350B units | High buyer scale |

| Tenders w/ TCO | >60% | Lifecycle pricing required |

| Target OEE | 50–70% | Capex justification |

Same Document Delivered

Soudronic GmbH Porter's Five Forces Analysis

This Soudronic GmbH Porter's Five Forces analysis delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to the metal packaging sector. This preview is the exact document you'll receive instantly after purchase—fully formatted and ready to use. No placeholders, no samples—what you see is what you download.

Description

Don't Miss the Bigger Picture

Soudronic GmbH's Porter's Five Forces analysis highlights strong supplier relationships, moderate buyer power, high competitive rivalry in metal forming, and manageable threat of substitutes but rising pressure from automation-focused entrants. This snapshot surfaces key strategic tensions and operational risks. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable insights for smarter investment and strategy decisions.

Suppliers Bargaining Power

Specialty component dependence

Soudronic depends on precision parts—copper electrodes, power electronics, servos and control systems—sourced from a narrow pool of qualified vendors, creating high switching costs and supply-risk exposure. Qualification and validation for high-duty welding components commonly exceed 6 months, amplifying supplier leverage and lead-time vulnerability. Dual-sourcing and in-house engineering reduce but do not eliminate this specialized dependency.

Advanced materials pricing

Prices for conductive alloys, stainless steels and high-spec insulators drive Soudronic’s BOM — LME nickel averaged about $26,000/tonne in 2024 and copper near $9,500/tonne, lifting input bills. Commodity volatility and energy surcharges (often 3–7% on metal invoices) can squeeze margins. Long-term contracts hedge price swings but limit near-term sourcing flexibility. Passing surcharges to customers is feasible but risks losing competitive bids.

Automation and controls ecosystems

Reliance on major PLC, drive and vision suppliers (Siemens, Rockwell, Mitsubishi et al.) creates ecosystem lock-in, with the top vendors accounting for roughly 60% of PLC market revenue in 2024. Firmware compatibility and safety certifications lengthen validation cycles and typically add switching costs measured in months and hundreds of thousands of euros. Suppliers with broad service networks can dictate support terms across regions, while co-development roadmaps have reduced integration time in many projects by up to 30%, balancing power through joint value creation.

Aftermarket consumables

Electrode tips, welding wheels and wear parts are recurring, quality-critical inputs that often appear on approved-vendor lists, constraining alternatives and raising supplier bargaining power; the global welding consumables market reached about USD 18.6 billion in 2024, underscoring supplier scale. Predictable purchase volumes allow Soudronic to negotiate volume discounts (commonly 5–12%), while Soudronic’s proprietary designs can standardize interfaces to widen sourcing and reduce dependence.

- Approved-vendor concentration: raises supplier leverage

- Market size 2024: USD 18.6 billion

- Negotiated discounts: ~5–12% with volume visibility

- Design standardization: expands supplier pool, lowers risk

Logistics and lead-time constraints

Long lead times for custom assemblies and power modules (typically 18–24 weeks in 2024 versus 8–12 pre‑pandemic) increase supplier leverage over Soudronic, forcing higher reliance on expediting and premium freight as European/global disruptions raised expediting costs by an estimated 25% in 2023–24. Framework agreements and buffer stocks reduce exposure but lock up working capital (inventory carrying costs ~20–25% annually). Supplier development programs have shown OTD improvements of ~10–15% within 12–18 months in comparable metalworking supply chains.

- Long lead times: 18–24 weeks (2024)

- Expediting cost increase: ~25% (2023–24)

- Inventory carrying cost: ~20–25% p.a.

- Supplier development OTD gain: ~10–15% in 12–18 months

Supplier power tight: 18-24 weeks lead times, commodity cost pressure

Soudronic faces high supplier power from specialized vendors (qualification >6 months), concentrated PLC/welding consumables markets and long lead times (18–24 wks in 2024), raising switching costs and expediting spend. Volume discounts (5–12%) and in-house design reduce but do not neutralize leverage. Commodity inputs (LME Cu ~$9,500/t; Ni ~$26,000/t in 2024) add margin pressure.

| Metric | 2024 value |

|---|---|

| Lead time | 18–24 weeks |

| Copper (LME) | ~$9,500/tonne |

| Nickel (LME) | ~$26,000/tonne |

| Volume discounts | 5–12% |

What is included in the product

Tailored Porter's Five Forces analysis for Soudronic GmbH uncovering key drivers of competition, buyer and supplier power, threat of substitutes and new entrants, and disruptive market risks affecting pricing and profitability; strategic commentary highlights barriers protecting incumbency and actionable insights for investors and management.

Concise one-sheet Porter's Five Forces for Soudronic GmbH—clean, simplified layout ready to copy into pitch decks or boardroom slides, instantly highlighting competitive pressures and strategic priorities.

Customers Bargaining Power

Concentrated can-makers

Large global and regional can-makers drive the majority of demand for Soudronic tooling and equipment, with global beverage can production approaching 350 billion cans per year in 2024, concentrating purchasing power with a handful of buyers.

Their scale and multi-plant ordering creates strong price and term leverage, pushing suppliers toward thin margins and high-volume discounts.

Preferred-vendor lists and global frame agreements intensify margin pressure while winning reference accounts remains critical for pipeline visibility and securing long-term multi-million-euro contracts.

Capex scrutiny and ROI

Buyers assess capex by modeled payback under 24 months using throughput, OEE (baseline 50–70%), scrap rate reductions (target 10–30%) and energy cuts (often 5–15%) to justify spend.

Competitive tenders demand detailed TCO and 8–10 year lifecycle support proposals; 2024 procurement studies show >60% require full lifecycle cost models.

Deferred capex during downturns gives buyers timing leverage and makes performance guarantees and uptime SLAs (99%+ targets) central bargaining chips.

Technical specification power

Customers impose strict specs for seam integrity, line speed and multiple can formats, forcing Soudronic to meet tight tolerances and uptime targets.

Customization demands often shift significant engineering and testing costs onto the OEM, increasing CAPEX for bespoke tooling and controls.

Open interfaces and line-integration support such as OPC UA and PLC compatibility are commonly mandatory, adding integration overhead.

Compliance with food-grade and safety standards including ISO 22000, HACCP, BRCGS and CE increases validation, documentation and audit burdens.

Aftermarket negotiation

Aftermarket negotiation is critical as spare parts, tooling, and multi-year service contracts are recurring and contestable revenue streams; buyers press for multi-year discounts and response-time SLAs that compress OEM margins. Third-party service providers and in-house maintenance increasingly threaten Soudronic’s aftermarket share by offering lower-cost alternatives. Bundled parts-and-service offerings can lock customers in but typically require discounted pricing to retain share.

- Spare parts, tooling, service = recurring & contestable

- Buyers demand multi-year discounts + response-time SLAs

- Third-party/in-house maintenance pressure OEM margins

- Bundled offerings drive retention at discounted rates

Switching and multi-sourcing

Larger can-makers such as Ball, Crown and Ardagh commonly maintain dual sourcing across welding lines to hedge supply risk; in 2024 the global beverage can market exceeded 350 billion units, amplifying the need for redundancy. Dual sourcing reduces vendor lock-in and strengthens buyer leverage at contract renewals, but switching still requires retraining, spare-inventory duplication and downtime. Proven reliability and retrofit ease materially lower switching incentives.

- Dual sourcing: common among majors

- Market scale 2024: >350 billion cans

- Buyer leverage: stronger at renewal

- Switching costs: retraining, spares, downtime

- Mitigation: reliability and retrofit simplicity reduce churn

Buyers leverage dominates >350B-can market; aftermarket discounts squeeze OEM margins

Major global can-makers concentrate demand (global beverage can market >350 billion units in 2024), giving buyers strong price/term leverage, frequent dual sourcing and emphasis on 24-month payback models; >60% of tenders require full lifecycle TCO. Aftermarket is contestable—buyers push multi-year discounts and 99%+ uptime SLAs, pressuring OEM margins.

| Metric | 2024 | Impact |

|---|---|---|

| Global cans | >350B units | High buyer scale |

| Tenders w/ TCO | >60% | Lifecycle pricing required |

| Target OEE | 50–70% | Capex justification |

Same Document Delivered

Soudronic GmbH Porter's Five Forces Analysis

This Soudronic GmbH Porter's Five Forces analysis delivers a concise assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry tailored to the metal packaging sector. This preview is the exact document you'll receive instantly after purchase—fully formatted and ready to use. No placeholders, no samples—what you see is what you download.