Southern Glazer's Wine & Spirits SWOT Analysis

Make Insightful Decisions Backed by Expert Research

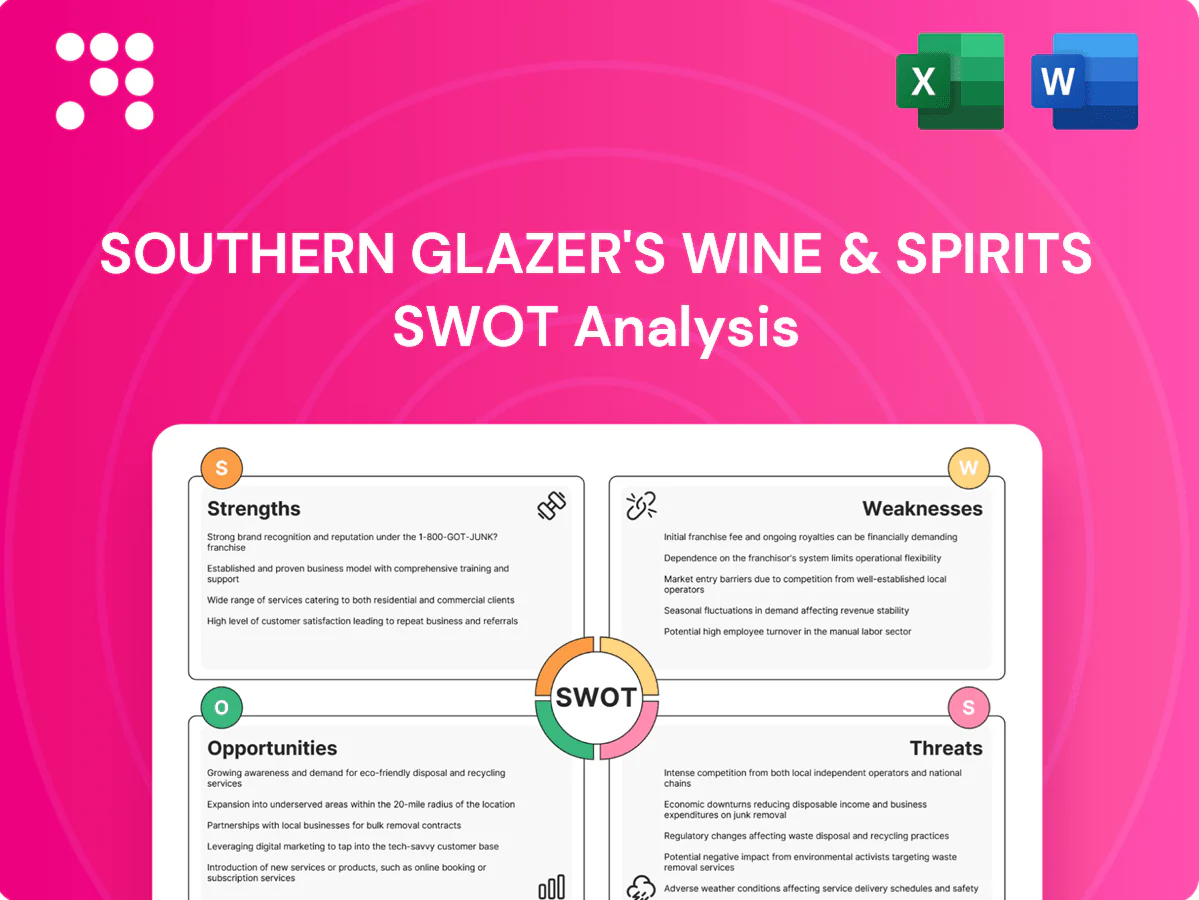

Southern Glazer’s SWOT highlights dominant distribution scale and supplier relationships, offset by margin pressure and regulatory exposure. Opportunities include premiumization and direct-to-consumer channels while competition and supply shocks pose real threats. Want the full story? Purchase the complete SWOT analysis for a professional Word report and editable Excel matrix with actionable insights.

Strengths

Unmatched scale and reach

As the largest North American beverage alcohol distributor, Southern Glazer’s leverages national coverage and dense local footprints across the US and Canada to lower per-unit logistics costs and improve service reliability, driving stronger bargaining power with suppliers and retailers and enabling faster new-product rollouts and consistent execution.

Diverse portfolio and exclusive ties

Southern Glazer's holds broad, often exclusive relationships with leading wine, spirits and RTD brands, operating across 44 US states, Washington DC and Canada and employing about 18,000 staff. That portfolio breadth cushions revenue volatility from any single category and season. Exclusive distribution deals boost defensibility and supplier stickiness. These ties enable tailored assortments across on‑ and off‑premise, grocery and convenience formats.

Advanced logistics and warehousing

Integrated warehousing, route optimization and targeted cold-chain support high service levels across Southern Glazer's network, underpinning its position as North America’s largest wine and spirits distributor with roughly $22 billion in net sales (2023). Investments in WMS/TMS and demand-planning systems reduce out-of-stocks and waste while enhancing forecast accuracy. Reliable last-mile capabilities help retail partners manage inventory turns, creating an operational backbone that is costly and time-consuming for competitors to replicate.

Sales, marketing, and data capabilities

Southern Glazer's, the largest U.S. wine and spirits distributor, leverages deep on- and off-premise sales coverage to drive execution at the point of sale; category management, trade marketing, and analytics shape assortment and pricing; data sharing with suppliers enhances joint business planning; these capabilities boost shelf velocity and improve ROI.

- Point-of-sale execution

- Category-led assortment & pricing

- Supplier data sharing

- Higher velocity & ROI

Regulatory expertise and compliance

Operating across the three-tier system demands rigorous compliance; Southern Glazer’s experience navigating state-by-state rules across all 50 states and D.C. reduces legal risk for supplier and retail partners, and its established governance and regulator relationships—backed by an organization of over 22,000 employees—creates durable competitive advantage.

- operates in all 50 states + D.C.

- over 22,000 employees

- largest north american wine & spirits distributor

- compliance-driven durable advantage

Nationwide wine & spirits leader: $22B sales, 22,000 employees

Largest North American wine & spirits distributor with ~$22B net sales (2023), leveraging nationwide footprint and dense local routes to lower logistics costs and accelerate rollouts. Broad exclusive supplier roster and category services boost shelf velocity and supplier stickiness. Deep compliance experience across all 50 states + D.C. and ~22,000 employees underpins durable advantage.

| Metric | Value | Year |

|---|---|---|

| Net sales | $22B | 2023 |

| Employees | ~22,000 | 2024 |

| Footprint | All 50 states + D.C. | 2024 |

What is included in the product

Provides a clear SWOT framework examining Southern Glazer's Wine & Spirits’ strengths, weaknesses, opportunities, and threats, mapping its market leadership, distribution scale, supplier relationships and operational capabilities against regulatory, competitive, and macroeconomic risks to inform strategic decisions.

Provides a concise SWOT matrix tailored to Southern Glazer's Wine & Spirits for rapid identification of distribution, supplier, and regulatory pain points, helping executives align mitigation strategies and present clear action plans.

Weaknesses

Supplier concentration risk

Southern Glazer's position as the largest U.S. wine and spirits distributor—operating in 44 states plus DC with about 21,000 employees—creates supplier concentration risk: dependence on key suppliers and exclusive agreements can quickly shift volumes and portfolio mix if contracts change. Loss or renegotiation of major portfolios would materially affect sales mix and margins; ongoing relationship-management costs are significant, and diversification lowers but does not eliminate concentration exposure.

Low margins and high working capital

Distribution economics in beverage wholesaling are margin-thin and volume-driven, and Southern Glazer's—the largest U.S. wine & spirits distributor operating in 44 states plus DC—faces heavy working-capital needs as large inventories, receivables and a nationwide fleet tie up cash; cost inflation (notably COGS and transportation) is often hard to pass through immediately, squeezing returns and pressuring margins during demand slowdowns.

Complex, fragmented regulation

Southern Glazer's faces regulatory fragmentation across 50 state regimes, plus control markets and franchise laws that add cost and rigidity; as the US largest distributor (reported revenue $34.6 billion in 2023), this variability limits rapid process standardization. Frequent legal changes force costly IT and compliance upgrades, slowing innovation and raising overhead.

Operational exposure to labor and fuel

Warehousing and last-mile delivery hinge on stable labor and energy costs; tight labor markets pushed transportation and warehousing average hourly earnings up about 4.6% YoY in 2024, raising wages and turnover. Diesel volatility (around $4/gal average in 2024) squeezed margins and lifted distribution costs. Disruptions ripple into service levels and fill rates, risking fulfillment for a distributor with ~21.4B revenue (2023).

- Labor pressure: tag - wages +4.6% (2024)

- Fuel squeeze: tag - diesel ~4/gal (2024)

- Margin impact: tag - higher operating costs

- Service risk: tag - fill rates, turnover

Limited brand ownership

As an intermediary, Southern Glazer's does not own the consumer brands it sells, limiting value capture compared with suppliers that hold brand equity; SGWS reported approximately $24.4 billion in net sales in 2023, but margins remain constrained by its role in the value chain. Differentiation depends on service, logistics scale and data analytics rather than proprietary IP, which caps pricing power and exposes SGWS to supplier-led promotional pressure.

- Role: distributor, not brand owner

- 2023 net sales: $24.4 billion

- Value capture: lower margins vs brand owners

- Dependence: service, scale, data over IP

Supplier concentration and thin margins risk rapid volume loss at largest US distributor

Supplier concentration and exclusive portfolios risk rapid volume/mix loss for the US largest distributor (revenue $34.6B 2023). Margin-thin, volume-driven model ties up working capital; cost inflation and receivables pressure margins. Regulatory fragmentation, plus labor (+4.6% avg wages 2024) and diesel volatility (~$4/gal 2024), raise operating costs and service risk.

| Metric | Value |

|---|---|

| Revenue (2023) | $34.6B |

| Wage change (2024) | +4.6% |

| Diesel avg (2024) | ~$4/gal |

Preview the Actual Deliverable

Southern Glazer's Wine & Spirits SWOT Analysis

This is the actual Southern Glazer's Wine & Spirits SWOT analysis document you’ll receive upon purchase—no surprises, just professional, structured content. The preview below is pulled directly from the full report; buying unlocks the complete, editable version. Get immediate access to the entire in-depth analysis after checkout.

Make Insightful Decisions Backed by Expert Research

Southern Glazer’s SWOT highlights dominant distribution scale and supplier relationships, offset by margin pressure and regulatory exposure. Opportunities include premiumization and direct-to-consumer channels while competition and supply shocks pose real threats. Want the full story? Purchase the complete SWOT analysis for a professional Word report and editable Excel matrix with actionable insights.

Strengths

Unmatched scale and reach

As the largest North American beverage alcohol distributor, Southern Glazer’s leverages national coverage and dense local footprints across the US and Canada to lower per-unit logistics costs and improve service reliability, driving stronger bargaining power with suppliers and retailers and enabling faster new-product rollouts and consistent execution.

Diverse portfolio and exclusive ties

Southern Glazer's holds broad, often exclusive relationships with leading wine, spirits and RTD brands, operating across 44 US states, Washington DC and Canada and employing about 18,000 staff. That portfolio breadth cushions revenue volatility from any single category and season. Exclusive distribution deals boost defensibility and supplier stickiness. These ties enable tailored assortments across on‑ and off‑premise, grocery and convenience formats.

Advanced logistics and warehousing

Integrated warehousing, route optimization and targeted cold-chain support high service levels across Southern Glazer's network, underpinning its position as North America’s largest wine and spirits distributor with roughly $22 billion in net sales (2023). Investments in WMS/TMS and demand-planning systems reduce out-of-stocks and waste while enhancing forecast accuracy. Reliable last-mile capabilities help retail partners manage inventory turns, creating an operational backbone that is costly and time-consuming for competitors to replicate.

Sales, marketing, and data capabilities

Southern Glazer's, the largest U.S. wine and spirits distributor, leverages deep on- and off-premise sales coverage to drive execution at the point of sale; category management, trade marketing, and analytics shape assortment and pricing; data sharing with suppliers enhances joint business planning; these capabilities boost shelf velocity and improve ROI.

- Point-of-sale execution

- Category-led assortment & pricing

- Supplier data sharing

- Higher velocity & ROI

Regulatory expertise and compliance

Operating across the three-tier system demands rigorous compliance; Southern Glazer’s experience navigating state-by-state rules across all 50 states and D.C. reduces legal risk for supplier and retail partners, and its established governance and regulator relationships—backed by an organization of over 22,000 employees—creates durable competitive advantage.

- operates in all 50 states + D.C.

- over 22,000 employees

- largest north american wine & spirits distributor

- compliance-driven durable advantage

Nationwide wine & spirits leader: $22B sales, 22,000 employees

Largest North American wine & spirits distributor with ~$22B net sales (2023), leveraging nationwide footprint and dense local routes to lower logistics costs and accelerate rollouts. Broad exclusive supplier roster and category services boost shelf velocity and supplier stickiness. Deep compliance experience across all 50 states + D.C. and ~22,000 employees underpins durable advantage.

| Metric | Value | Year |

|---|---|---|

| Net sales | $22B | 2023 |

| Employees | ~22,000 | 2024 |

| Footprint | All 50 states + D.C. | 2024 |

What is included in the product

Provides a clear SWOT framework examining Southern Glazer's Wine & Spirits’ strengths, weaknesses, opportunities, and threats, mapping its market leadership, distribution scale, supplier relationships and operational capabilities against regulatory, competitive, and macroeconomic risks to inform strategic decisions.

Provides a concise SWOT matrix tailored to Southern Glazer's Wine & Spirits for rapid identification of distribution, supplier, and regulatory pain points, helping executives align mitigation strategies and present clear action plans.

Weaknesses

Supplier concentration risk

Southern Glazer's position as the largest U.S. wine and spirits distributor—operating in 44 states plus DC with about 21,000 employees—creates supplier concentration risk: dependence on key suppliers and exclusive agreements can quickly shift volumes and portfolio mix if contracts change. Loss or renegotiation of major portfolios would materially affect sales mix and margins; ongoing relationship-management costs are significant, and diversification lowers but does not eliminate concentration exposure.

Low margins and high working capital

Distribution economics in beverage wholesaling are margin-thin and volume-driven, and Southern Glazer's—the largest U.S. wine & spirits distributor operating in 44 states plus DC—faces heavy working-capital needs as large inventories, receivables and a nationwide fleet tie up cash; cost inflation (notably COGS and transportation) is often hard to pass through immediately, squeezing returns and pressuring margins during demand slowdowns.

Complex, fragmented regulation

Southern Glazer's faces regulatory fragmentation across 50 state regimes, plus control markets and franchise laws that add cost and rigidity; as the US largest distributor (reported revenue $34.6 billion in 2023), this variability limits rapid process standardization. Frequent legal changes force costly IT and compliance upgrades, slowing innovation and raising overhead.

Operational exposure to labor and fuel

Warehousing and last-mile delivery hinge on stable labor and energy costs; tight labor markets pushed transportation and warehousing average hourly earnings up about 4.6% YoY in 2024, raising wages and turnover. Diesel volatility (around $4/gal average in 2024) squeezed margins and lifted distribution costs. Disruptions ripple into service levels and fill rates, risking fulfillment for a distributor with ~21.4B revenue (2023).

- Labor pressure: tag - wages +4.6% (2024)

- Fuel squeeze: tag - diesel ~4/gal (2024)

- Margin impact: tag - higher operating costs

- Service risk: tag - fill rates, turnover

Limited brand ownership

As an intermediary, Southern Glazer's does not own the consumer brands it sells, limiting value capture compared with suppliers that hold brand equity; SGWS reported approximately $24.4 billion in net sales in 2023, but margins remain constrained by its role in the value chain. Differentiation depends on service, logistics scale and data analytics rather than proprietary IP, which caps pricing power and exposes SGWS to supplier-led promotional pressure.

- Role: distributor, not brand owner

- 2023 net sales: $24.4 billion

- Value capture: lower margins vs brand owners

- Dependence: service, scale, data over IP

Supplier concentration and thin margins risk rapid volume loss at largest US distributor

Supplier concentration and exclusive portfolios risk rapid volume/mix loss for the US largest distributor (revenue $34.6B 2023). Margin-thin, volume-driven model ties up working capital; cost inflation and receivables pressure margins. Regulatory fragmentation, plus labor (+4.6% avg wages 2024) and diesel volatility (~$4/gal 2024), raise operating costs and service risk.

| Metric | Value |

|---|---|

| Revenue (2023) | $34.6B |

| Wage change (2024) | +4.6% |

| Diesel avg (2024) | ~$4/gal |

Preview the Actual Deliverable

Southern Glazer's Wine & Spirits SWOT Analysis

This is the actual Southern Glazer's Wine & Spirits SWOT analysis document you’ll receive upon purchase—no surprises, just professional, structured content. The preview below is pulled directly from the full report; buying unlocks the complete, editable version. Get immediate access to the entire in-depth analysis after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Make Insightful Decisions Backed by Expert Research

Southern Glazer’s SWOT highlights dominant distribution scale and supplier relationships, offset by margin pressure and regulatory exposure. Opportunities include premiumization and direct-to-consumer channels while competition and supply shocks pose real threats. Want the full story? Purchase the complete SWOT analysis for a professional Word report and editable Excel matrix with actionable insights.

Strengths

Unmatched scale and reach

As the largest North American beverage alcohol distributor, Southern Glazer’s leverages national coverage and dense local footprints across the US and Canada to lower per-unit logistics costs and improve service reliability, driving stronger bargaining power with suppliers and retailers and enabling faster new-product rollouts and consistent execution.

Diverse portfolio and exclusive ties

Southern Glazer's holds broad, often exclusive relationships with leading wine, spirits and RTD brands, operating across 44 US states, Washington DC and Canada and employing about 18,000 staff. That portfolio breadth cushions revenue volatility from any single category and season. Exclusive distribution deals boost defensibility and supplier stickiness. These ties enable tailored assortments across on‑ and off‑premise, grocery and convenience formats.

Advanced logistics and warehousing

Integrated warehousing, route optimization and targeted cold-chain support high service levels across Southern Glazer's network, underpinning its position as North America’s largest wine and spirits distributor with roughly $22 billion in net sales (2023). Investments in WMS/TMS and demand-planning systems reduce out-of-stocks and waste while enhancing forecast accuracy. Reliable last-mile capabilities help retail partners manage inventory turns, creating an operational backbone that is costly and time-consuming for competitors to replicate.

Sales, marketing, and data capabilities

Southern Glazer's, the largest U.S. wine and spirits distributor, leverages deep on- and off-premise sales coverage to drive execution at the point of sale; category management, trade marketing, and analytics shape assortment and pricing; data sharing with suppliers enhances joint business planning; these capabilities boost shelf velocity and improve ROI.

- Point-of-sale execution

- Category-led assortment & pricing

- Supplier data sharing

- Higher velocity & ROI

Regulatory expertise and compliance

Operating across the three-tier system demands rigorous compliance; Southern Glazer’s experience navigating state-by-state rules across all 50 states and D.C. reduces legal risk for supplier and retail partners, and its established governance and regulator relationships—backed by an organization of over 22,000 employees—creates durable competitive advantage.

- operates in all 50 states + D.C.

- over 22,000 employees

- largest north american wine & spirits distributor

- compliance-driven durable advantage

Nationwide wine & spirits leader: $22B sales, 22,000 employees

Largest North American wine & spirits distributor with ~$22B net sales (2023), leveraging nationwide footprint and dense local routes to lower logistics costs and accelerate rollouts. Broad exclusive supplier roster and category services boost shelf velocity and supplier stickiness. Deep compliance experience across all 50 states + D.C. and ~22,000 employees underpins durable advantage.

| Metric | Value | Year |

|---|---|---|

| Net sales | $22B | 2023 |

| Employees | ~22,000 | 2024 |

| Footprint | All 50 states + D.C. | 2024 |

What is included in the product

Provides a clear SWOT framework examining Southern Glazer's Wine & Spirits’ strengths, weaknesses, opportunities, and threats, mapping its market leadership, distribution scale, supplier relationships and operational capabilities against regulatory, competitive, and macroeconomic risks to inform strategic decisions.

Provides a concise SWOT matrix tailored to Southern Glazer's Wine & Spirits for rapid identification of distribution, supplier, and regulatory pain points, helping executives align mitigation strategies and present clear action plans.

Weaknesses

Supplier concentration risk

Southern Glazer's position as the largest U.S. wine and spirits distributor—operating in 44 states plus DC with about 21,000 employees—creates supplier concentration risk: dependence on key suppliers and exclusive agreements can quickly shift volumes and portfolio mix if contracts change. Loss or renegotiation of major portfolios would materially affect sales mix and margins; ongoing relationship-management costs are significant, and diversification lowers but does not eliminate concentration exposure.

Low margins and high working capital

Distribution economics in beverage wholesaling are margin-thin and volume-driven, and Southern Glazer's—the largest U.S. wine & spirits distributor operating in 44 states plus DC—faces heavy working-capital needs as large inventories, receivables and a nationwide fleet tie up cash; cost inflation (notably COGS and transportation) is often hard to pass through immediately, squeezing returns and pressuring margins during demand slowdowns.

Complex, fragmented regulation

Southern Glazer's faces regulatory fragmentation across 50 state regimes, plus control markets and franchise laws that add cost and rigidity; as the US largest distributor (reported revenue $34.6 billion in 2023), this variability limits rapid process standardization. Frequent legal changes force costly IT and compliance upgrades, slowing innovation and raising overhead.

Operational exposure to labor and fuel

Warehousing and last-mile delivery hinge on stable labor and energy costs; tight labor markets pushed transportation and warehousing average hourly earnings up about 4.6% YoY in 2024, raising wages and turnover. Diesel volatility (around $4/gal average in 2024) squeezed margins and lifted distribution costs. Disruptions ripple into service levels and fill rates, risking fulfillment for a distributor with ~21.4B revenue (2023).

- Labor pressure: tag - wages +4.6% (2024)

- Fuel squeeze: tag - diesel ~4/gal (2024)

- Margin impact: tag - higher operating costs

- Service risk: tag - fill rates, turnover

Limited brand ownership

As an intermediary, Southern Glazer's does not own the consumer brands it sells, limiting value capture compared with suppliers that hold brand equity; SGWS reported approximately $24.4 billion in net sales in 2023, but margins remain constrained by its role in the value chain. Differentiation depends on service, logistics scale and data analytics rather than proprietary IP, which caps pricing power and exposes SGWS to supplier-led promotional pressure.

- Role: distributor, not brand owner

- 2023 net sales: $24.4 billion

- Value capture: lower margins vs brand owners

- Dependence: service, scale, data over IP

Supplier concentration and thin margins risk rapid volume loss at largest US distributor

Supplier concentration and exclusive portfolios risk rapid volume/mix loss for the US largest distributor (revenue $34.6B 2023). Margin-thin, volume-driven model ties up working capital; cost inflation and receivables pressure margins. Regulatory fragmentation, plus labor (+4.6% avg wages 2024) and diesel volatility (~$4/gal 2024), raise operating costs and service risk.

| Metric | Value |

|---|---|

| Revenue (2023) | $34.6B |

| Wage change (2024) | +4.6% |

| Diesel avg (2024) | ~$4/gal |

Preview the Actual Deliverable

Southern Glazer's Wine & Spirits SWOT Analysis

This is the actual Southern Glazer's Wine & Spirits SWOT analysis document you’ll receive upon purchase—no surprises, just professional, structured content. The preview below is pulled directly from the full report; buying unlocks the complete, editable version. Get immediate access to the entire in-depth analysis after checkout.