South Plains Financial Porter's Five Forces Analysis

Don't Miss the Bigger Picture

South Plains Financial operates within a banking sector characterized by moderate rivalry and significant regulatory oversight. While customer switching costs are relatively low, the threat of new entrants is somewhat mitigated by capital requirements and established trust. Understanding the nuances of buyer power and the availability of substitutes is crucial for strategic planning.

The complete report reveals the real forces shaping South Plains Financial’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Power 1

Depositors are the primary suppliers for South Plains Financial, providing the crucial capital for its lending operations. Their bargaining power is directly tied to prevailing interest rates and the variety of alternative savings and investment opportunities available to them.

In 2024, as interest rates remained elevated compared to the preceding years, South Plains Financial, like many regional banks, faced pressure to offer more competitive deposit rates. For instance, average savings account rates across the industry saw significant increases, with some institutions offering yields exceeding 4.5% by late 2024, directly impacting the bank's cost of funds.

Supplier Power 2

Technology providers, offering essential banking systems and digital platforms, represent a key supplier group for financial institutions. As banks like South Plains Financial increasingly depend on advanced technology for operational efficiency and customer engagement, the influence of these specialized vendors grows. In 2024, the digital transformation in banking continues to accelerate, making robust and secure technology infrastructure a critical competitive factor.

Supplier Power 3

The labor market, especially for skilled financial and IT professionals, represents a significant supplier group for South Plains Financial. In 2024, the banking sector experienced continued upward pressure on compensation, with average salaries for financial analysts rising by an estimated 4-6% year-over-year, directly impacting operational costs.

The demand for specialized talent in crucial areas like digital banking, cybersecurity, and data analytics has amplified the bargaining power of these employees. For instance, the shortage of experienced cybersecurity professionals in 2024 led to an average salary increase of over 10% in that niche, giving these individuals considerable leverage when negotiating terms with financial institutions like South Plains Financial.

Supplier Power 4

The bargaining power of suppliers for South Plains Financial is significantly influenced by providers of capital, such as interbank lending markets and institutional investors. Their leverage hinges on South Plains Financial's financial robustness, adherence to regulatory capital mandates, and the prevailing liquidity conditions in the broader market. For instance, if regulatory bodies impose more stringent capital requirements, or if credit markets become less accessible, the cost of wholesale funding for South Plains Financial could escalate, or its availability might be curtailed.

In 2024, the cost of funds for many regional banks, including those similar to South Plains Financial, saw an upward trend due to sustained interest rate hikes by the Federal Reserve. This increased the expense of borrowing from interbank markets. Furthermore, heightened investor scrutiny on bank balance sheets, particularly after the regional banking stresses experienced earlier in 2023, means that institutional investors can demand more favorable terms when providing debt or equity capital.

- Increased Cost of Funds: Rising benchmark interest rates in 2024 directly translate to higher borrowing costs for banks in wholesale funding markets.

- Regulatory Capital Influence: Changes in capital adequacy ratios can force banks to seek more expensive or less readily available funding to meet requirements, thereby increasing supplier power.

- Market Liquidity Impact: Periods of reduced market liquidity empower capital providers, as demand for funds outstrips supply, allowing them to dictate terms.

- Investor Sentiment: Negative investor sentiment or perceived risk in the banking sector can lead to higher equity capital costs and stricter debt covenants.

Supplier Power 5

While not direct suppliers in the traditional sense, regulatory bodies wield significant influence over financial institutions like South Plains Financial. These entities impose operational frameworks and compliance costs that act as a powerful constraint. For instance, evolving regulations concerning capital adequacy, anti-money laundering protocols, and data privacy directly impact operational expenses and strategic planning, effectively raising the cost of doing business.

The burden of compliance can be substantial. In 2024, financial institutions globally continued to navigate a complex regulatory landscape. For example, the implementation of new data privacy laws or enhanced cybersecurity mandates requires significant investment in technology and personnel. This ongoing need to adapt and adhere to these evolving standards increases the 'cost' of operating for banks, demonstrating a form of supplier power where non-compliance carries severe penalties.

The impact of these regulatory demands can be quantified. Increased compliance spending means less capital available for growth initiatives or shareholder returns. Financial institutions must allocate resources to legal counsel, compliance officers, and technology upgrades to meet these requirements. This can lead to:

- Increased operational overhead

- Potential limitations on strategic flexibility

- Higher costs for technology and training

- Significant penalties for non-compliance

2024 Supplier Dynamics: Depositors, Tech, and Talent Drive Costs

South Plains Financial's suppliers include depositors, technology providers, and the labor market, each wielding varying degrees of bargaining power. Depositors' power is linked to interest rates, with 2024 seeing elevated rates pushing banks to offer more competitive yields, impacting funding costs. Technology vendors and skilled labor, particularly in areas like cybersecurity, also command higher prices due to increasing demand and specialization.

| Supplier Group | Key Influence Factors | 2024 Impact Example |

|---|---|---|

| Depositors | Interest Rates, Alternative Investments | Average savings account rates exceeded 4.5% |

| Technology Providers | Digitalization Needs, Security Requirements | Accelerated digital transformation drives demand for robust platforms |

| Skilled Labor (e.g., Cybersecurity) | Demand for Expertise, Talent Shortages | Average salary increases of over 10% for cybersecurity professionals |

What is included in the product

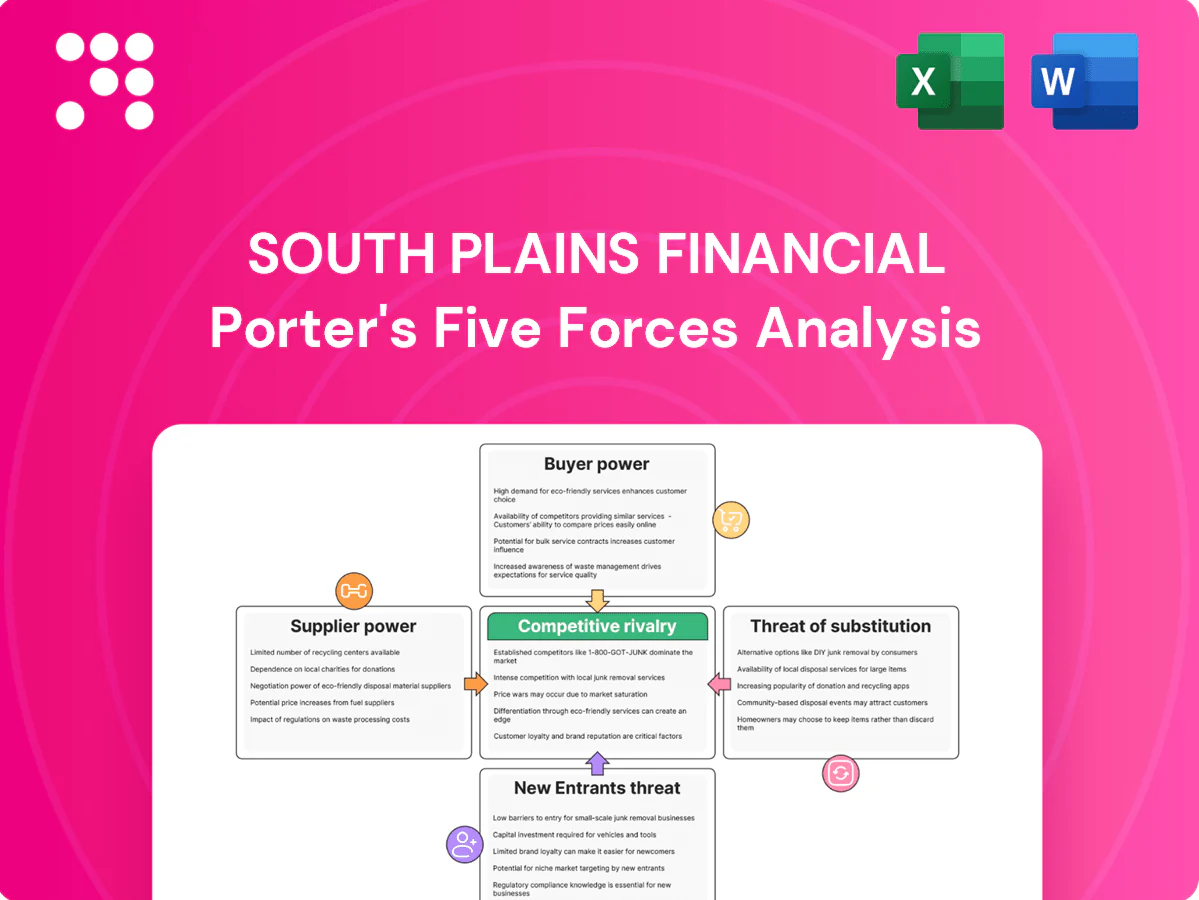

This Porter's Five Forces analysis for South Plains Financial dissects the competitive intensity, buyer and supplier power, threat of new entrants, and the impact of substitutes on the company's strategic positioning.

Instantly assess competitive pressures with a visual representation of each force, simplifying complex strategic analysis for South Plains Financial.

Customers Bargaining Power

Customer Power 1

Individual retail customers hold considerable sway, with a wide array of banking options readily available. This includes not only other regional and national banks but also credit unions operating within Texas and New Mexico, a key market for South Plains Financial. The ease with which customers can switch between basic banking products like checking accounts and savings accounts, often with minimal fees or hassle, amplifies their ability to shop for better deals.

Customer Power 2

Small and medium-sized businesses, a key customer base for South Plains Financial, have numerous choices for commercial lending. These businesses can easily compare loan terms, fees, and digital offerings from various lenders, creating a competitive landscape.

While City Bank, a part of South Plains Financial, leverages strong relationships and local knowledge, its customers can still shop around. In 2024, South Plains Financial facilitated over $400 million in loans to small businesses, highlighting its active participation and the significant volume of business within this segment.

Customer Power 3

Customers today have more power than ever, largely due to the rise of digital banking and easy-to-use comparison tools. These platforms make it simple for consumers to see exactly what rates and fees other financial institutions are offering, creating a transparent market. This transparency directly pressures banks like South Plains Financial to offer more competitive terms to attract and retain business.

With readily available information, customers are empowered to shop around and negotiate for better deals on loans, accounts, and other financial products. In 2024, for instance, the average interest rate on a new car loan saw significant fluctuations, giving savvy consumers leverage to seek out the best rates. South Plains Financial’s own digital offerings, while designed for convenience, also serve to highlight this increased customer awareness and the need to consistently meet evolving expectations for value and transparency.

Customer Power 4

Customer bargaining power at South Plains Financial is significantly shaped by their sensitivity to interest rates, especially concerning deposit accounts and mortgage loans. When interest rates are volatile, customers are more inclined to shop around for better yields on their savings or more favorable rates on their borrowing. This can pressure financial institutions like South Plains Financial to be competitive with their pricing to retain and attract business, directly impacting their net interest margin.

For instance, during periods of rising interest rates, customers with substantial deposit balances can leverage their options to move funds to institutions offering higher APYs. Similarly, borrowers might refinance mortgages if they find lenders providing lower rates. In 2024, the Federal Reserve's monetary policy decisions, including potential rate adjustments, will continue to be a critical factor influencing this customer behavior and, consequently, the bank's pricing strategies.

- Customer Sensitivity to Interest Rates: Customers actively seek higher yields on deposits and lower rates on loans, especially during fluctuating rate environments.

- Impact on Net Interest Margin: This sensitivity forces banks to adjust their pricing, directly affecting profitability through the net interest margin.

- 2024 Market Dynamics: Anticipated shifts in interest rates in 2024 will likely amplify customer’s bargaining power as they seek optimal financial products.

- Competitive Landscape: The willingness of customers to switch providers based on rate differentials underscores the competitive nature of the banking sector.

Customer Power 5

The bargaining power of customers for South Plains Financial is influenced by the demand for specialized financial products. If customers require highly niche or innovative services not readily available through South Plains' broad offerings in commercial and retail banking, investment, trust, and mortgage services, they may seek out specialized providers.

This can shift power towards these customers, especially if the bank's current product suite doesn't fully cater to their unique needs. For example, in 2024, the fintech sector continued to offer highly specialized digital lending platforms, potentially drawing customers away from traditional banks for specific loan types.

South Plains Financial's ability to retain customers with unique demands hinges on its product development and the breadth of its service portfolio.

- Customer demand for specialized financial products can increase their bargaining power.

- Niche or innovative solutions might be sought from specialized providers if not offered by South Plains.

- The bank's diverse offerings in commercial, retail, investment, trust, and mortgage services aim to mitigate this.

- Competition from fintechs offering specialized digital services is a factor in 2024.

Customer Bargaining Power Influences Financial Institution Dynamics

Customers at South Plains Financial possess significant bargaining power due to the readily available alternatives and the ease of switching between financial institutions. This is particularly true for retail customers who can easily compare rates and services for basic accounts. For instance, in 2024, the average interest rate on savings accounts across the industry saw variations, giving customers leverage to seek higher yields.

Small and medium-sized businesses, a core demographic for South Plains Financial, also benefit from numerous lending options. They can actively compare loan terms and digital banking features from various providers, putting pressure on banks to offer competitive packages. South Plains Financial's commitment to this segment is evident, having facilitated over $400 million in small business loans in 2024.

The increasing transparency in financial services, driven by digital tools and comparison platforms, further empowers customers. They can easily access information on rates and fees, compelling institutions like South Plains Financial to maintain competitive pricing and service quality to retain their business.

Customer sensitivity to interest rates is a primary driver of their bargaining power. In 2024, with potential shifts in monetary policy, customers with substantial deposits or seeking mortgages are more likely to move their funds or refinance to secure better rates. This dynamic directly impacts South Plains Financial's net interest margin, necessitating agile pricing strategies.

| Factor | Impact on South Plains Financial | 2024 Relevance |

| Availability of Alternatives | Increases customer ability to switch | High, with numerous regional and national banks, plus credit unions |

| Ease of Switching | Lowers customer switching costs | Significant for basic deposit and checking accounts |

| Interest Rate Sensitivity | Pressures pricing for deposits and loans | Amplified by potential Fed rate adjustments in 2024 |

| Digital Transparency | Enhances customer comparison shopping | Facilitated by online tools and comparison websites |

Same Document Delivered

South Plains Financial Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis for South Plains Financial, detailing the competitive landscape and strategic implications for the company. The document you see here is the exact, professionally formatted report you will receive immediately after purchase, offering a comprehensive understanding of industry rivalry, buyer and supplier power, threats of new entrants, and substitute products. You're looking at the actual document; once you complete your purchase, you’ll get instant access to this exact file, ready for your strategic planning needs.

Don't Miss the Bigger Picture

South Plains Financial operates within a banking sector characterized by moderate rivalry and significant regulatory oversight. While customer switching costs are relatively low, the threat of new entrants is somewhat mitigated by capital requirements and established trust. Understanding the nuances of buyer power and the availability of substitutes is crucial for strategic planning.

The complete report reveals the real forces shaping South Plains Financial’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Power 1

Depositors are the primary suppliers for South Plains Financial, providing the crucial capital for its lending operations. Their bargaining power is directly tied to prevailing interest rates and the variety of alternative savings and investment opportunities available to them.

In 2024, as interest rates remained elevated compared to the preceding years, South Plains Financial, like many regional banks, faced pressure to offer more competitive deposit rates. For instance, average savings account rates across the industry saw significant increases, with some institutions offering yields exceeding 4.5% by late 2024, directly impacting the bank's cost of funds.

Supplier Power 2

Technology providers, offering essential banking systems and digital platforms, represent a key supplier group for financial institutions. As banks like South Plains Financial increasingly depend on advanced technology for operational efficiency and customer engagement, the influence of these specialized vendors grows. In 2024, the digital transformation in banking continues to accelerate, making robust and secure technology infrastructure a critical competitive factor.

Supplier Power 3

The labor market, especially for skilled financial and IT professionals, represents a significant supplier group for South Plains Financial. In 2024, the banking sector experienced continued upward pressure on compensation, with average salaries for financial analysts rising by an estimated 4-6% year-over-year, directly impacting operational costs.

The demand for specialized talent in crucial areas like digital banking, cybersecurity, and data analytics has amplified the bargaining power of these employees. For instance, the shortage of experienced cybersecurity professionals in 2024 led to an average salary increase of over 10% in that niche, giving these individuals considerable leverage when negotiating terms with financial institutions like South Plains Financial.

Supplier Power 4

The bargaining power of suppliers for South Plains Financial is significantly influenced by providers of capital, such as interbank lending markets and institutional investors. Their leverage hinges on South Plains Financial's financial robustness, adherence to regulatory capital mandates, and the prevailing liquidity conditions in the broader market. For instance, if regulatory bodies impose more stringent capital requirements, or if credit markets become less accessible, the cost of wholesale funding for South Plains Financial could escalate, or its availability might be curtailed.

In 2024, the cost of funds for many regional banks, including those similar to South Plains Financial, saw an upward trend due to sustained interest rate hikes by the Federal Reserve. This increased the expense of borrowing from interbank markets. Furthermore, heightened investor scrutiny on bank balance sheets, particularly after the regional banking stresses experienced earlier in 2023, means that institutional investors can demand more favorable terms when providing debt or equity capital.

- Increased Cost of Funds: Rising benchmark interest rates in 2024 directly translate to higher borrowing costs for banks in wholesale funding markets.

- Regulatory Capital Influence: Changes in capital adequacy ratios can force banks to seek more expensive or less readily available funding to meet requirements, thereby increasing supplier power.

- Market Liquidity Impact: Periods of reduced market liquidity empower capital providers, as demand for funds outstrips supply, allowing them to dictate terms.

- Investor Sentiment: Negative investor sentiment or perceived risk in the banking sector can lead to higher equity capital costs and stricter debt covenants.

Supplier Power 5

While not direct suppliers in the traditional sense, regulatory bodies wield significant influence over financial institutions like South Plains Financial. These entities impose operational frameworks and compliance costs that act as a powerful constraint. For instance, evolving regulations concerning capital adequacy, anti-money laundering protocols, and data privacy directly impact operational expenses and strategic planning, effectively raising the cost of doing business.

The burden of compliance can be substantial. In 2024, financial institutions globally continued to navigate a complex regulatory landscape. For example, the implementation of new data privacy laws or enhanced cybersecurity mandates requires significant investment in technology and personnel. This ongoing need to adapt and adhere to these evolving standards increases the 'cost' of operating for banks, demonstrating a form of supplier power where non-compliance carries severe penalties.

The impact of these regulatory demands can be quantified. Increased compliance spending means less capital available for growth initiatives or shareholder returns. Financial institutions must allocate resources to legal counsel, compliance officers, and technology upgrades to meet these requirements. This can lead to:

- Increased operational overhead

- Potential limitations on strategic flexibility

- Higher costs for technology and training

- Significant penalties for non-compliance

2024 Supplier Dynamics: Depositors, Tech, and Talent Drive Costs

South Plains Financial's suppliers include depositors, technology providers, and the labor market, each wielding varying degrees of bargaining power. Depositors' power is linked to interest rates, with 2024 seeing elevated rates pushing banks to offer more competitive yields, impacting funding costs. Technology vendors and skilled labor, particularly in areas like cybersecurity, also command higher prices due to increasing demand and specialization.

| Supplier Group | Key Influence Factors | 2024 Impact Example |

|---|---|---|

| Depositors | Interest Rates, Alternative Investments | Average savings account rates exceeded 4.5% |

| Technology Providers | Digitalization Needs, Security Requirements | Accelerated digital transformation drives demand for robust platforms |

| Skilled Labor (e.g., Cybersecurity) | Demand for Expertise, Talent Shortages | Average salary increases of over 10% for cybersecurity professionals |

What is included in the product

This Porter's Five Forces analysis for South Plains Financial dissects the competitive intensity, buyer and supplier power, threat of new entrants, and the impact of substitutes on the company's strategic positioning.

Instantly assess competitive pressures with a visual representation of each force, simplifying complex strategic analysis for South Plains Financial.

Customers Bargaining Power

Customer Power 1

Individual retail customers hold considerable sway, with a wide array of banking options readily available. This includes not only other regional and national banks but also credit unions operating within Texas and New Mexico, a key market for South Plains Financial. The ease with which customers can switch between basic banking products like checking accounts and savings accounts, often with minimal fees or hassle, amplifies their ability to shop for better deals.

Customer Power 2

Small and medium-sized businesses, a key customer base for South Plains Financial, have numerous choices for commercial lending. These businesses can easily compare loan terms, fees, and digital offerings from various lenders, creating a competitive landscape.

While City Bank, a part of South Plains Financial, leverages strong relationships and local knowledge, its customers can still shop around. In 2024, South Plains Financial facilitated over $400 million in loans to small businesses, highlighting its active participation and the significant volume of business within this segment.

Customer Power 3

Customers today have more power than ever, largely due to the rise of digital banking and easy-to-use comparison tools. These platforms make it simple for consumers to see exactly what rates and fees other financial institutions are offering, creating a transparent market. This transparency directly pressures banks like South Plains Financial to offer more competitive terms to attract and retain business.

With readily available information, customers are empowered to shop around and negotiate for better deals on loans, accounts, and other financial products. In 2024, for instance, the average interest rate on a new car loan saw significant fluctuations, giving savvy consumers leverage to seek out the best rates. South Plains Financial’s own digital offerings, while designed for convenience, also serve to highlight this increased customer awareness and the need to consistently meet evolving expectations for value and transparency.

Customer Power 4

Customer bargaining power at South Plains Financial is significantly shaped by their sensitivity to interest rates, especially concerning deposit accounts and mortgage loans. When interest rates are volatile, customers are more inclined to shop around for better yields on their savings or more favorable rates on their borrowing. This can pressure financial institutions like South Plains Financial to be competitive with their pricing to retain and attract business, directly impacting their net interest margin.

For instance, during periods of rising interest rates, customers with substantial deposit balances can leverage their options to move funds to institutions offering higher APYs. Similarly, borrowers might refinance mortgages if they find lenders providing lower rates. In 2024, the Federal Reserve's monetary policy decisions, including potential rate adjustments, will continue to be a critical factor influencing this customer behavior and, consequently, the bank's pricing strategies.

- Customer Sensitivity to Interest Rates: Customers actively seek higher yields on deposits and lower rates on loans, especially during fluctuating rate environments.

- Impact on Net Interest Margin: This sensitivity forces banks to adjust their pricing, directly affecting profitability through the net interest margin.

- 2024 Market Dynamics: Anticipated shifts in interest rates in 2024 will likely amplify customer’s bargaining power as they seek optimal financial products.

- Competitive Landscape: The willingness of customers to switch providers based on rate differentials underscores the competitive nature of the banking sector.

Customer Power 5

The bargaining power of customers for South Plains Financial is influenced by the demand for specialized financial products. If customers require highly niche or innovative services not readily available through South Plains' broad offerings in commercial and retail banking, investment, trust, and mortgage services, they may seek out specialized providers.

This can shift power towards these customers, especially if the bank's current product suite doesn't fully cater to their unique needs. For example, in 2024, the fintech sector continued to offer highly specialized digital lending platforms, potentially drawing customers away from traditional banks for specific loan types.

South Plains Financial's ability to retain customers with unique demands hinges on its product development and the breadth of its service portfolio.

- Customer demand for specialized financial products can increase their bargaining power.

- Niche or innovative solutions might be sought from specialized providers if not offered by South Plains.

- The bank's diverse offerings in commercial, retail, investment, trust, and mortgage services aim to mitigate this.

- Competition from fintechs offering specialized digital services is a factor in 2024.

Customer Bargaining Power Influences Financial Institution Dynamics

Customers at South Plains Financial possess significant bargaining power due to the readily available alternatives and the ease of switching between financial institutions. This is particularly true for retail customers who can easily compare rates and services for basic accounts. For instance, in 2024, the average interest rate on savings accounts across the industry saw variations, giving customers leverage to seek higher yields.

Small and medium-sized businesses, a core demographic for South Plains Financial, also benefit from numerous lending options. They can actively compare loan terms and digital banking features from various providers, putting pressure on banks to offer competitive packages. South Plains Financial's commitment to this segment is evident, having facilitated over $400 million in small business loans in 2024.

The increasing transparency in financial services, driven by digital tools and comparison platforms, further empowers customers. They can easily access information on rates and fees, compelling institutions like South Plains Financial to maintain competitive pricing and service quality to retain their business.

Customer sensitivity to interest rates is a primary driver of their bargaining power. In 2024, with potential shifts in monetary policy, customers with substantial deposits or seeking mortgages are more likely to move their funds or refinance to secure better rates. This dynamic directly impacts South Plains Financial's net interest margin, necessitating agile pricing strategies.

| Factor | Impact on South Plains Financial | 2024 Relevance |

| Availability of Alternatives | Increases customer ability to switch | High, with numerous regional and national banks, plus credit unions |

| Ease of Switching | Lowers customer switching costs | Significant for basic deposit and checking accounts |

| Interest Rate Sensitivity | Pressures pricing for deposits and loans | Amplified by potential Fed rate adjustments in 2024 |

| Digital Transparency | Enhances customer comparison shopping | Facilitated by online tools and comparison websites |

Same Document Delivered

South Plains Financial Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis for South Plains Financial, detailing the competitive landscape and strategic implications for the company. The document you see here is the exact, professionally formatted report you will receive immediately after purchase, offering a comprehensive understanding of industry rivalry, buyer and supplier power, threats of new entrants, and substitute products. You're looking at the actual document; once you complete your purchase, you’ll get instant access to this exact file, ready for your strategic planning needs.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

South Plains Financial operates within a banking sector characterized by moderate rivalry and significant regulatory oversight. While customer switching costs are relatively low, the threat of new entrants is somewhat mitigated by capital requirements and established trust. Understanding the nuances of buyer power and the availability of substitutes is crucial for strategic planning.

The complete report reveals the real forces shaping South Plains Financial’s industry—from supplier influence to threat of new entrants. Gain actionable insights to drive smarter decision-making.

Suppliers Bargaining Power

Supplier Power 1

Depositors are the primary suppliers for South Plains Financial, providing the crucial capital for its lending operations. Their bargaining power is directly tied to prevailing interest rates and the variety of alternative savings and investment opportunities available to them.

In 2024, as interest rates remained elevated compared to the preceding years, South Plains Financial, like many regional banks, faced pressure to offer more competitive deposit rates. For instance, average savings account rates across the industry saw significant increases, with some institutions offering yields exceeding 4.5% by late 2024, directly impacting the bank's cost of funds.

Supplier Power 2

Technology providers, offering essential banking systems and digital platforms, represent a key supplier group for financial institutions. As banks like South Plains Financial increasingly depend on advanced technology for operational efficiency and customer engagement, the influence of these specialized vendors grows. In 2024, the digital transformation in banking continues to accelerate, making robust and secure technology infrastructure a critical competitive factor.

Supplier Power 3

The labor market, especially for skilled financial and IT professionals, represents a significant supplier group for South Plains Financial. In 2024, the banking sector experienced continued upward pressure on compensation, with average salaries for financial analysts rising by an estimated 4-6% year-over-year, directly impacting operational costs.

The demand for specialized talent in crucial areas like digital banking, cybersecurity, and data analytics has amplified the bargaining power of these employees. For instance, the shortage of experienced cybersecurity professionals in 2024 led to an average salary increase of over 10% in that niche, giving these individuals considerable leverage when negotiating terms with financial institutions like South Plains Financial.

Supplier Power 4

The bargaining power of suppliers for South Plains Financial is significantly influenced by providers of capital, such as interbank lending markets and institutional investors. Their leverage hinges on South Plains Financial's financial robustness, adherence to regulatory capital mandates, and the prevailing liquidity conditions in the broader market. For instance, if regulatory bodies impose more stringent capital requirements, or if credit markets become less accessible, the cost of wholesale funding for South Plains Financial could escalate, or its availability might be curtailed.

In 2024, the cost of funds for many regional banks, including those similar to South Plains Financial, saw an upward trend due to sustained interest rate hikes by the Federal Reserve. This increased the expense of borrowing from interbank markets. Furthermore, heightened investor scrutiny on bank balance sheets, particularly after the regional banking stresses experienced earlier in 2023, means that institutional investors can demand more favorable terms when providing debt or equity capital.

- Increased Cost of Funds: Rising benchmark interest rates in 2024 directly translate to higher borrowing costs for banks in wholesale funding markets.

- Regulatory Capital Influence: Changes in capital adequacy ratios can force banks to seek more expensive or less readily available funding to meet requirements, thereby increasing supplier power.

- Market Liquidity Impact: Periods of reduced market liquidity empower capital providers, as demand for funds outstrips supply, allowing them to dictate terms.

- Investor Sentiment: Negative investor sentiment or perceived risk in the banking sector can lead to higher equity capital costs and stricter debt covenants.

Supplier Power 5

While not direct suppliers in the traditional sense, regulatory bodies wield significant influence over financial institutions like South Plains Financial. These entities impose operational frameworks and compliance costs that act as a powerful constraint. For instance, evolving regulations concerning capital adequacy, anti-money laundering protocols, and data privacy directly impact operational expenses and strategic planning, effectively raising the cost of doing business.

The burden of compliance can be substantial. In 2024, financial institutions globally continued to navigate a complex regulatory landscape. For example, the implementation of new data privacy laws or enhanced cybersecurity mandates requires significant investment in technology and personnel. This ongoing need to adapt and adhere to these evolving standards increases the 'cost' of operating for banks, demonstrating a form of supplier power where non-compliance carries severe penalties.

The impact of these regulatory demands can be quantified. Increased compliance spending means less capital available for growth initiatives or shareholder returns. Financial institutions must allocate resources to legal counsel, compliance officers, and technology upgrades to meet these requirements. This can lead to:

- Increased operational overhead

- Potential limitations on strategic flexibility

- Higher costs for technology and training

- Significant penalties for non-compliance

2024 Supplier Dynamics: Depositors, Tech, and Talent Drive Costs

South Plains Financial's suppliers include depositors, technology providers, and the labor market, each wielding varying degrees of bargaining power. Depositors' power is linked to interest rates, with 2024 seeing elevated rates pushing banks to offer more competitive yields, impacting funding costs. Technology vendors and skilled labor, particularly in areas like cybersecurity, also command higher prices due to increasing demand and specialization.

| Supplier Group | Key Influence Factors | 2024 Impact Example |

|---|---|---|

| Depositors | Interest Rates, Alternative Investments | Average savings account rates exceeded 4.5% |

| Technology Providers | Digitalization Needs, Security Requirements | Accelerated digital transformation drives demand for robust platforms |

| Skilled Labor (e.g., Cybersecurity) | Demand for Expertise, Talent Shortages | Average salary increases of over 10% for cybersecurity professionals |

What is included in the product

This Porter's Five Forces analysis for South Plains Financial dissects the competitive intensity, buyer and supplier power, threat of new entrants, and the impact of substitutes on the company's strategic positioning.

Instantly assess competitive pressures with a visual representation of each force, simplifying complex strategic analysis for South Plains Financial.

Customers Bargaining Power

Customer Power 1

Individual retail customers hold considerable sway, with a wide array of banking options readily available. This includes not only other regional and national banks but also credit unions operating within Texas and New Mexico, a key market for South Plains Financial. The ease with which customers can switch between basic banking products like checking accounts and savings accounts, often with minimal fees or hassle, amplifies their ability to shop for better deals.

Customer Power 2

Small and medium-sized businesses, a key customer base for South Plains Financial, have numerous choices for commercial lending. These businesses can easily compare loan terms, fees, and digital offerings from various lenders, creating a competitive landscape.

While City Bank, a part of South Plains Financial, leverages strong relationships and local knowledge, its customers can still shop around. In 2024, South Plains Financial facilitated over $400 million in loans to small businesses, highlighting its active participation and the significant volume of business within this segment.

Customer Power 3

Customers today have more power than ever, largely due to the rise of digital banking and easy-to-use comparison tools. These platforms make it simple for consumers to see exactly what rates and fees other financial institutions are offering, creating a transparent market. This transparency directly pressures banks like South Plains Financial to offer more competitive terms to attract and retain business.

With readily available information, customers are empowered to shop around and negotiate for better deals on loans, accounts, and other financial products. In 2024, for instance, the average interest rate on a new car loan saw significant fluctuations, giving savvy consumers leverage to seek out the best rates. South Plains Financial’s own digital offerings, while designed for convenience, also serve to highlight this increased customer awareness and the need to consistently meet evolving expectations for value and transparency.

Customer Power 4

Customer bargaining power at South Plains Financial is significantly shaped by their sensitivity to interest rates, especially concerning deposit accounts and mortgage loans. When interest rates are volatile, customers are more inclined to shop around for better yields on their savings or more favorable rates on their borrowing. This can pressure financial institutions like South Plains Financial to be competitive with their pricing to retain and attract business, directly impacting their net interest margin.

For instance, during periods of rising interest rates, customers with substantial deposit balances can leverage their options to move funds to institutions offering higher APYs. Similarly, borrowers might refinance mortgages if they find lenders providing lower rates. In 2024, the Federal Reserve's monetary policy decisions, including potential rate adjustments, will continue to be a critical factor influencing this customer behavior and, consequently, the bank's pricing strategies.

- Customer Sensitivity to Interest Rates: Customers actively seek higher yields on deposits and lower rates on loans, especially during fluctuating rate environments.

- Impact on Net Interest Margin: This sensitivity forces banks to adjust their pricing, directly affecting profitability through the net interest margin.

- 2024 Market Dynamics: Anticipated shifts in interest rates in 2024 will likely amplify customer’s bargaining power as they seek optimal financial products.

- Competitive Landscape: The willingness of customers to switch providers based on rate differentials underscores the competitive nature of the banking sector.

Customer Power 5

The bargaining power of customers for South Plains Financial is influenced by the demand for specialized financial products. If customers require highly niche or innovative services not readily available through South Plains' broad offerings in commercial and retail banking, investment, trust, and mortgage services, they may seek out specialized providers.

This can shift power towards these customers, especially if the bank's current product suite doesn't fully cater to their unique needs. For example, in 2024, the fintech sector continued to offer highly specialized digital lending platforms, potentially drawing customers away from traditional banks for specific loan types.

South Plains Financial's ability to retain customers with unique demands hinges on its product development and the breadth of its service portfolio.

- Customer demand for specialized financial products can increase their bargaining power.

- Niche or innovative solutions might be sought from specialized providers if not offered by South Plains.

- The bank's diverse offerings in commercial, retail, investment, trust, and mortgage services aim to mitigate this.

- Competition from fintechs offering specialized digital services is a factor in 2024.

Customer Bargaining Power Influences Financial Institution Dynamics

Customers at South Plains Financial possess significant bargaining power due to the readily available alternatives and the ease of switching between financial institutions. This is particularly true for retail customers who can easily compare rates and services for basic accounts. For instance, in 2024, the average interest rate on savings accounts across the industry saw variations, giving customers leverage to seek higher yields.

Small and medium-sized businesses, a core demographic for South Plains Financial, also benefit from numerous lending options. They can actively compare loan terms and digital banking features from various providers, putting pressure on banks to offer competitive packages. South Plains Financial's commitment to this segment is evident, having facilitated over $400 million in small business loans in 2024.

The increasing transparency in financial services, driven by digital tools and comparison platforms, further empowers customers. They can easily access information on rates and fees, compelling institutions like South Plains Financial to maintain competitive pricing and service quality to retain their business.

Customer sensitivity to interest rates is a primary driver of their bargaining power. In 2024, with potential shifts in monetary policy, customers with substantial deposits or seeking mortgages are more likely to move their funds or refinance to secure better rates. This dynamic directly impacts South Plains Financial's net interest margin, necessitating agile pricing strategies.

| Factor | Impact on South Plains Financial | 2024 Relevance |

| Availability of Alternatives | Increases customer ability to switch | High, with numerous regional and national banks, plus credit unions |

| Ease of Switching | Lowers customer switching costs | Significant for basic deposit and checking accounts |

| Interest Rate Sensitivity | Pressures pricing for deposits and loans | Amplified by potential Fed rate adjustments in 2024 |

| Digital Transparency | Enhances customer comparison shopping | Facilitated by online tools and comparison websites |

Same Document Delivered

South Plains Financial Porter's Five Forces Analysis

This preview showcases the complete Porter's Five Forces Analysis for South Plains Financial, detailing the competitive landscape and strategic implications for the company. The document you see here is the exact, professionally formatted report you will receive immediately after purchase, offering a comprehensive understanding of industry rivalry, buyer and supplier power, threats of new entrants, and substitute products. You're looking at the actual document; once you complete your purchase, you’ll get instant access to this exact file, ready for your strategic planning needs.