Spirax-Sarco Engineering PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Spirax-Sarco Engineering—spot regulatory, economic, and technological forces shaping growth and risk. Ideal for investors and strategists, it’s fully researched and actionable. Purchase the full report to get the complete, editable analysis instantly.

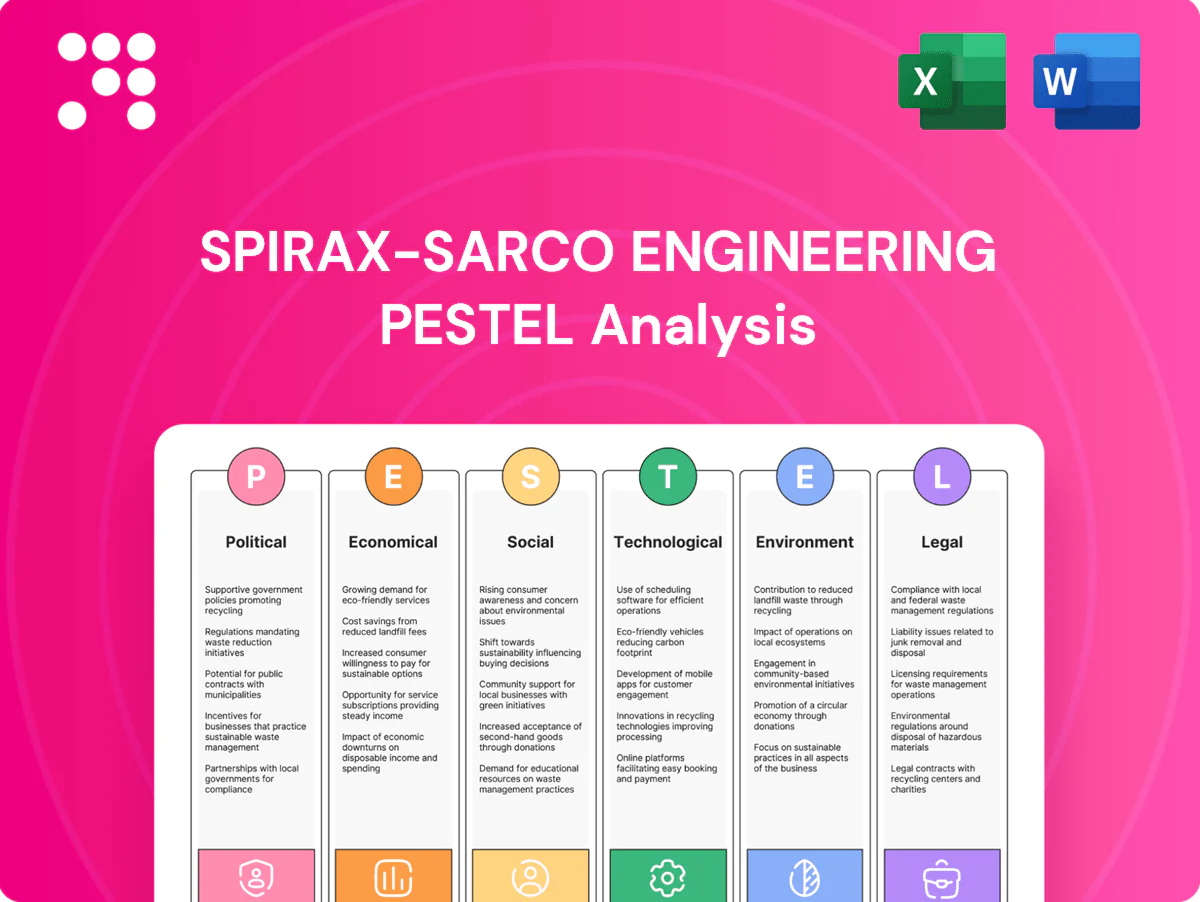

Political factors

Trade policy volatility

Trade policy volatility exposes Spirax-Sarco, including acquisitions Chromalox and Watson-Marlow (acquired 2021), to tariffs, sanctions and export controls that can interrupt component flows and customer deliveries; US Section 301 tariffs reached up to 25% on affected imports. US–China and EU trade tensions impact electronics and metals supply for heating and pump systems. Diversified sourcing and regionalization mitigate single-country risk. Active compliance and scenario planning are required to protect margins and lead times.

Industrial decarbonization push

Government net-zero roadmaps (EU target -55% by 2030) and industrial efficiency incentives increasingly favor steam optimization and electric thermal solutions, driving demand for retrofit technologies. Carbon pricing (EU ETS ~€90/t in 2024) and subsidies from programs like the US Inflation Reduction Act (~$369bn clean energy investment) shift customer CAPEX toward energy-saving retrofits. Spirax-Sarco and Chromalox can tap national grants and utility rebates to accelerate sales. Clear policy timelines speed order conversion; regulatory delays defer projects and capital deployment.

Infrastructure & reshoring agendas

Public investment—e.g., US CHIPS Act ~$280bn and IRA ~$369bn—plus EU net‑zero and pharma initiatives is reviving US/EU and selected EM plant builds, raising demand for process control, steam heating and hygienic pumps; global industrial pumps market was ~$68bn in 2023 with 4–5% CAGR, while local content rules and procurement standards (ASME, ISO, EHEDG) push regional manufacturing or partner deals.

Geopolitical instability

Geopolitical instability elevates logistics costs and insurance premiums and can halt projects in conflict zones, pressuring timelines for Spirax-Sarco’s steam and thermal management installations.

Energy-intensive end-markets commonly defer CAPEX during instability, but Spirax’s balanced end-market mix across industry and utilities helps mitigate regional demand shocks.

Maintaining safety stocks and dual-route logistics enhances delivery resilience and reduces single-route disruption risk.

- Logistics and insurance cost increases

- Deferred CAPEX in energy-intensive sectors

- Balanced end-market mix offsets regional shocks

- Safety stocks and dual-route logistics bolster resilience

Public health and food security

National emphasis on pharma readiness and safe food processing supports sustained investment in sterile systems; FAO estimated about 735 million people were undernourished in 2023, reinforcing food-safety priorities. Watson-Marlow, a Spirax-Sarco subsidiary, aligns with bioprocess capacity expansion trends. OECD data show public procurement ≈12% of GDP, so regulatory-backed procurement and biotech-cluster support can speed framework agreements and localized demand.

- Pharma readiness drives sterile-system spend

- Watson-Marlow aligns with bioprocess scale-up

- Public procurement ≈12% of GDP

- Biotech clusters increase local demand and framework deals

Tariffs, EU ETS €90/t & $369bn IRA reshape pumps

Trade tensions and tariffs (US Section 301 up to 25%) threaten supply chains; diversified sourcing and dual logistics reduce risk. EU ETS ≈€90/t (2024) and IRA ~$369bn shift CAPEX to efficiency/retrofits, boosting steam/electric solutions. Global pumps market ~$68bn (2023) with ~4–5% CAGR supports steady demand; public procurement ≈12% GDP aids framework deals.

| Metric | Value |

|---|---|

| EU ETS (2024) | ≈€90/t |

| IRA | ~$369bn |

| Global pumps (2023) | ~$68bn, 4–5% CAGR |

What is included in the product

Offers a focused PESTLE analysis of Spirax-Sarco Engineering, detailing Political, Economic, Social, Technological, Environmental, and Legal factors with data-driven trends and industry-specific examples to identify risks, opportunities, and strategic implications for executives, investors, and planners.

A concise, visually segmented Spirax‑Sarco PESTLE summary that removes complexity, lets teams add region- or line-specific notes, and serves as a shareable slide-ready brief to streamline risk discussions and strategic planning.

Economic factors

Industrial capex cycles

Orders for Spirax-Sarco track macro PMI and plant utilisation in chemicals, F&B and power, with S&P Global manufacturing PMI around 51 in late 2024 correlating with order flows. Slowdowns defer large capex projects but sustain maintenance and efficiency retrofits, which supported service demand in 2024. Installed-base services provided counter-cyclical revenue, underpinning group FY2024 revenue of about £1.9bn. Pipeline visibility and flexible pricing have protected throughput and margins.

Energy price dynamics

Surging wholesale gas prices (TTF peaked above 300 €/MWh in 2022, averaging ~35 €/MWh in 2024) raise payback periods for steam systems and make electrification and steam optimization more attractive. Customers increasingly prioritize thermal efficiency to cut OPEX. Suppliers like Chromalox gain when electrification lowers fossil dependence. Price volatility shifts demand between steam upgrades and electric solutions.

FX and interest rates

Spirax-Sarco’s multi-currency revenues and costs create material translation and transaction exposures, with management noting FX effects on reported growth in recent FY updates. Strong USD and EUR swings versus sterling have intermittently altered price competitiveness across markets. Elevated policy rates—around 5% in major markets in mid-2025—increase likelihood of delayed customer capex approvals. Natural hedging and selective price adjustments are used to mitigate impacts.

Input costs and supply chain

Inflation in stainless steel, copper and electronics has compressed margins through 2024–mid‑2025, forcing Spirax‑Sarco to push customer surcharges and value‑based pricing while protecting margins. Supplier diversification and design‑to‑cost programs have re‑balanced BOM economics. Lean inventories improve cash conversion but must be weighed against uptime and reliability risks.

- Metals/electronics inflation pressures: ongoing through 2024–25

- Supplier diversification and DTC safeguard BOM

- Lean inventory vs reliability tradeoff

- Customer surcharges/value pricing recover costs

Life sciences growth

- Structural demand: bioprocessing USD 16–18bn (2024)

- GMP: premium margins, long lifecycles

- Defensive: cushions downturns

- KAM: deepens wallet share

Tariffs, EU ETS €90/t & $369bn IRA reshape pumps

Spirax-Sarco orders track PMI ~51 (late 2024) and FY2024 revenue ~£1.9bn, with installed-base services cushioning cycles. Wholesale gas avg ~35 €/MWh (2024) and metals inflation 2024–25 raise payback periods, boosting steam efficiency and electrification demand. FX volatility and ~5% policy rates (mid-2025) pressure capex timing and margins, mitigated by pricing, hedging and supplier diversification.

| Metric | Value |

|---|---|

| FY revenue | £1.9bn (2024) |

| S&P Global PMI | ~51 (late 2024) |

| TTF gas | ~35 €/MWh (avg 2024) |

| Policy rates | ~5% (mid-2025) |

| Bioprocessing market | USD 16–18bn (2024) |

Preview Before You Purchase

Spirax-Sarco Engineering PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Spirax‑Sarco Engineering PESTLE analysis examines political, economic, social, technological, legal and environmental factors affecting the company and market. It delivers concise, actionable insights for strategy and investment decisions.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Spirax-Sarco Engineering—spot regulatory, economic, and technological forces shaping growth and risk. Ideal for investors and strategists, it’s fully researched and actionable. Purchase the full report to get the complete, editable analysis instantly.

Political factors

Trade policy volatility

Trade policy volatility exposes Spirax-Sarco, including acquisitions Chromalox and Watson-Marlow (acquired 2021), to tariffs, sanctions and export controls that can interrupt component flows and customer deliveries; US Section 301 tariffs reached up to 25% on affected imports. US–China and EU trade tensions impact electronics and metals supply for heating and pump systems. Diversified sourcing and regionalization mitigate single-country risk. Active compliance and scenario planning are required to protect margins and lead times.

Industrial decarbonization push

Government net-zero roadmaps (EU target -55% by 2030) and industrial efficiency incentives increasingly favor steam optimization and electric thermal solutions, driving demand for retrofit technologies. Carbon pricing (EU ETS ~€90/t in 2024) and subsidies from programs like the US Inflation Reduction Act (~$369bn clean energy investment) shift customer CAPEX toward energy-saving retrofits. Spirax-Sarco and Chromalox can tap national grants and utility rebates to accelerate sales. Clear policy timelines speed order conversion; regulatory delays defer projects and capital deployment.

Infrastructure & reshoring agendas

Public investment—e.g., US CHIPS Act ~$280bn and IRA ~$369bn—plus EU net‑zero and pharma initiatives is reviving US/EU and selected EM plant builds, raising demand for process control, steam heating and hygienic pumps; global industrial pumps market was ~$68bn in 2023 with 4–5% CAGR, while local content rules and procurement standards (ASME, ISO, EHEDG) push regional manufacturing or partner deals.

Geopolitical instability

Geopolitical instability elevates logistics costs and insurance premiums and can halt projects in conflict zones, pressuring timelines for Spirax-Sarco’s steam and thermal management installations.

Energy-intensive end-markets commonly defer CAPEX during instability, but Spirax’s balanced end-market mix across industry and utilities helps mitigate regional demand shocks.

Maintaining safety stocks and dual-route logistics enhances delivery resilience and reduces single-route disruption risk.

- Logistics and insurance cost increases

- Deferred CAPEX in energy-intensive sectors

- Balanced end-market mix offsets regional shocks

- Safety stocks and dual-route logistics bolster resilience

Public health and food security

National emphasis on pharma readiness and safe food processing supports sustained investment in sterile systems; FAO estimated about 735 million people were undernourished in 2023, reinforcing food-safety priorities. Watson-Marlow, a Spirax-Sarco subsidiary, aligns with bioprocess capacity expansion trends. OECD data show public procurement ≈12% of GDP, so regulatory-backed procurement and biotech-cluster support can speed framework agreements and localized demand.

- Pharma readiness drives sterile-system spend

- Watson-Marlow aligns with bioprocess scale-up

- Public procurement ≈12% of GDP

- Biotech clusters increase local demand and framework deals

Tariffs, EU ETS €90/t & $369bn IRA reshape pumps

Trade tensions and tariffs (US Section 301 up to 25%) threaten supply chains; diversified sourcing and dual logistics reduce risk. EU ETS ≈€90/t (2024) and IRA ~$369bn shift CAPEX to efficiency/retrofits, boosting steam/electric solutions. Global pumps market ~$68bn (2023) with ~4–5% CAGR supports steady demand; public procurement ≈12% GDP aids framework deals.

| Metric | Value |

|---|---|

| EU ETS (2024) | ≈€90/t |

| IRA | ~$369bn |

| Global pumps (2023) | ~$68bn, 4–5% CAGR |

What is included in the product

Offers a focused PESTLE analysis of Spirax-Sarco Engineering, detailing Political, Economic, Social, Technological, Environmental, and Legal factors with data-driven trends and industry-specific examples to identify risks, opportunities, and strategic implications for executives, investors, and planners.

A concise, visually segmented Spirax‑Sarco PESTLE summary that removes complexity, lets teams add region- or line-specific notes, and serves as a shareable slide-ready brief to streamline risk discussions and strategic planning.

Economic factors

Industrial capex cycles

Orders for Spirax-Sarco track macro PMI and plant utilisation in chemicals, F&B and power, with S&P Global manufacturing PMI around 51 in late 2024 correlating with order flows. Slowdowns defer large capex projects but sustain maintenance and efficiency retrofits, which supported service demand in 2024. Installed-base services provided counter-cyclical revenue, underpinning group FY2024 revenue of about £1.9bn. Pipeline visibility and flexible pricing have protected throughput and margins.

Energy price dynamics

Surging wholesale gas prices (TTF peaked above 300 €/MWh in 2022, averaging ~35 €/MWh in 2024) raise payback periods for steam systems and make electrification and steam optimization more attractive. Customers increasingly prioritize thermal efficiency to cut OPEX. Suppliers like Chromalox gain when electrification lowers fossil dependence. Price volatility shifts demand between steam upgrades and electric solutions.

FX and interest rates

Spirax-Sarco’s multi-currency revenues and costs create material translation and transaction exposures, with management noting FX effects on reported growth in recent FY updates. Strong USD and EUR swings versus sterling have intermittently altered price competitiveness across markets. Elevated policy rates—around 5% in major markets in mid-2025—increase likelihood of delayed customer capex approvals. Natural hedging and selective price adjustments are used to mitigate impacts.

Input costs and supply chain

Inflation in stainless steel, copper and electronics has compressed margins through 2024–mid‑2025, forcing Spirax‑Sarco to push customer surcharges and value‑based pricing while protecting margins. Supplier diversification and design‑to‑cost programs have re‑balanced BOM economics. Lean inventories improve cash conversion but must be weighed against uptime and reliability risks.

- Metals/electronics inflation pressures: ongoing through 2024–25

- Supplier diversification and DTC safeguard BOM

- Lean inventory vs reliability tradeoff

- Customer surcharges/value pricing recover costs

Life sciences growth

- Structural demand: bioprocessing USD 16–18bn (2024)

- GMP: premium margins, long lifecycles

- Defensive: cushions downturns

- KAM: deepens wallet share

Tariffs, EU ETS €90/t & $369bn IRA reshape pumps

Spirax-Sarco orders track PMI ~51 (late 2024) and FY2024 revenue ~£1.9bn, with installed-base services cushioning cycles. Wholesale gas avg ~35 €/MWh (2024) and metals inflation 2024–25 raise payback periods, boosting steam efficiency and electrification demand. FX volatility and ~5% policy rates (mid-2025) pressure capex timing and margins, mitigated by pricing, hedging and supplier diversification.

| Metric | Value |

|---|---|

| FY revenue | £1.9bn (2024) |

| S&P Global PMI | ~51 (late 2024) |

| TTF gas | ~35 €/MWh (avg 2024) |

| Policy rates | ~5% (mid-2025) |

| Bioprocessing market | USD 16–18bn (2024) |

Preview Before You Purchase

Spirax-Sarco Engineering PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Spirax‑Sarco Engineering PESTLE analysis examines political, economic, social, technological, legal and environmental factors affecting the company and market. It delivers concise, actionable insights for strategy and investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our PESTLE Analysis of Spirax-Sarco Engineering—spot regulatory, economic, and technological forces shaping growth and risk. Ideal for investors and strategists, it’s fully researched and actionable. Purchase the full report to get the complete, editable analysis instantly.

Political factors

Trade policy volatility

Trade policy volatility exposes Spirax-Sarco, including acquisitions Chromalox and Watson-Marlow (acquired 2021), to tariffs, sanctions and export controls that can interrupt component flows and customer deliveries; US Section 301 tariffs reached up to 25% on affected imports. US–China and EU trade tensions impact electronics and metals supply for heating and pump systems. Diversified sourcing and regionalization mitigate single-country risk. Active compliance and scenario planning are required to protect margins and lead times.

Industrial decarbonization push

Government net-zero roadmaps (EU target -55% by 2030) and industrial efficiency incentives increasingly favor steam optimization and electric thermal solutions, driving demand for retrofit technologies. Carbon pricing (EU ETS ~€90/t in 2024) and subsidies from programs like the US Inflation Reduction Act (~$369bn clean energy investment) shift customer CAPEX toward energy-saving retrofits. Spirax-Sarco and Chromalox can tap national grants and utility rebates to accelerate sales. Clear policy timelines speed order conversion; regulatory delays defer projects and capital deployment.

Infrastructure & reshoring agendas

Public investment—e.g., US CHIPS Act ~$280bn and IRA ~$369bn—plus EU net‑zero and pharma initiatives is reviving US/EU and selected EM plant builds, raising demand for process control, steam heating and hygienic pumps; global industrial pumps market was ~$68bn in 2023 with 4–5% CAGR, while local content rules and procurement standards (ASME, ISO, EHEDG) push regional manufacturing or partner deals.

Geopolitical instability

Geopolitical instability elevates logistics costs and insurance premiums and can halt projects in conflict zones, pressuring timelines for Spirax-Sarco’s steam and thermal management installations.

Energy-intensive end-markets commonly defer CAPEX during instability, but Spirax’s balanced end-market mix across industry and utilities helps mitigate regional demand shocks.

Maintaining safety stocks and dual-route logistics enhances delivery resilience and reduces single-route disruption risk.

- Logistics and insurance cost increases

- Deferred CAPEX in energy-intensive sectors

- Balanced end-market mix offsets regional shocks

- Safety stocks and dual-route logistics bolster resilience

Public health and food security

National emphasis on pharma readiness and safe food processing supports sustained investment in sterile systems; FAO estimated about 735 million people were undernourished in 2023, reinforcing food-safety priorities. Watson-Marlow, a Spirax-Sarco subsidiary, aligns with bioprocess capacity expansion trends. OECD data show public procurement ≈12% of GDP, so regulatory-backed procurement and biotech-cluster support can speed framework agreements and localized demand.

- Pharma readiness drives sterile-system spend

- Watson-Marlow aligns with bioprocess scale-up

- Public procurement ≈12% of GDP

- Biotech clusters increase local demand and framework deals

Tariffs, EU ETS €90/t & $369bn IRA reshape pumps

Trade tensions and tariffs (US Section 301 up to 25%) threaten supply chains; diversified sourcing and dual logistics reduce risk. EU ETS ≈€90/t (2024) and IRA ~$369bn shift CAPEX to efficiency/retrofits, boosting steam/electric solutions. Global pumps market ~$68bn (2023) with ~4–5% CAGR supports steady demand; public procurement ≈12% GDP aids framework deals.

| Metric | Value |

|---|---|

| EU ETS (2024) | ≈€90/t |

| IRA | ~$369bn |

| Global pumps (2023) | ~$68bn, 4–5% CAGR |

What is included in the product

Offers a focused PESTLE analysis of Spirax-Sarco Engineering, detailing Political, Economic, Social, Technological, Environmental, and Legal factors with data-driven trends and industry-specific examples to identify risks, opportunities, and strategic implications for executives, investors, and planners.

A concise, visually segmented Spirax‑Sarco PESTLE summary that removes complexity, lets teams add region- or line-specific notes, and serves as a shareable slide-ready brief to streamline risk discussions and strategic planning.

Economic factors

Industrial capex cycles

Orders for Spirax-Sarco track macro PMI and plant utilisation in chemicals, F&B and power, with S&P Global manufacturing PMI around 51 in late 2024 correlating with order flows. Slowdowns defer large capex projects but sustain maintenance and efficiency retrofits, which supported service demand in 2024. Installed-base services provided counter-cyclical revenue, underpinning group FY2024 revenue of about £1.9bn. Pipeline visibility and flexible pricing have protected throughput and margins.

Energy price dynamics

Surging wholesale gas prices (TTF peaked above 300 €/MWh in 2022, averaging ~35 €/MWh in 2024) raise payback periods for steam systems and make electrification and steam optimization more attractive. Customers increasingly prioritize thermal efficiency to cut OPEX. Suppliers like Chromalox gain when electrification lowers fossil dependence. Price volatility shifts demand between steam upgrades and electric solutions.

FX and interest rates

Spirax-Sarco’s multi-currency revenues and costs create material translation and transaction exposures, with management noting FX effects on reported growth in recent FY updates. Strong USD and EUR swings versus sterling have intermittently altered price competitiveness across markets. Elevated policy rates—around 5% in major markets in mid-2025—increase likelihood of delayed customer capex approvals. Natural hedging and selective price adjustments are used to mitigate impacts.

Input costs and supply chain

Inflation in stainless steel, copper and electronics has compressed margins through 2024–mid‑2025, forcing Spirax‑Sarco to push customer surcharges and value‑based pricing while protecting margins. Supplier diversification and design‑to‑cost programs have re‑balanced BOM economics. Lean inventories improve cash conversion but must be weighed against uptime and reliability risks.

- Metals/electronics inflation pressures: ongoing through 2024–25

- Supplier diversification and DTC safeguard BOM

- Lean inventory vs reliability tradeoff

- Customer surcharges/value pricing recover costs

Life sciences growth

- Structural demand: bioprocessing USD 16–18bn (2024)

- GMP: premium margins, long lifecycles

- Defensive: cushions downturns

- KAM: deepens wallet share

Tariffs, EU ETS €90/t & $369bn IRA reshape pumps

Spirax-Sarco orders track PMI ~51 (late 2024) and FY2024 revenue ~£1.9bn, with installed-base services cushioning cycles. Wholesale gas avg ~35 €/MWh (2024) and metals inflation 2024–25 raise payback periods, boosting steam efficiency and electrification demand. FX volatility and ~5% policy rates (mid-2025) pressure capex timing and margins, mitigated by pricing, hedging and supplier diversification.

| Metric | Value |

|---|---|

| FY revenue | £1.9bn (2024) |

| S&P Global PMI | ~51 (late 2024) |

| TTF gas | ~35 €/MWh (avg 2024) |

| Policy rates | ~5% (mid-2025) |

| Bioprocessing market | USD 16–18bn (2024) |

Preview Before You Purchase

Spirax-Sarco Engineering PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. This Spirax‑Sarco Engineering PESTLE analysis examines political, economic, social, technological, legal and environmental factors affecting the company and market. It delivers concise, actionable insights for strategy and investment decisions.