Spire Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

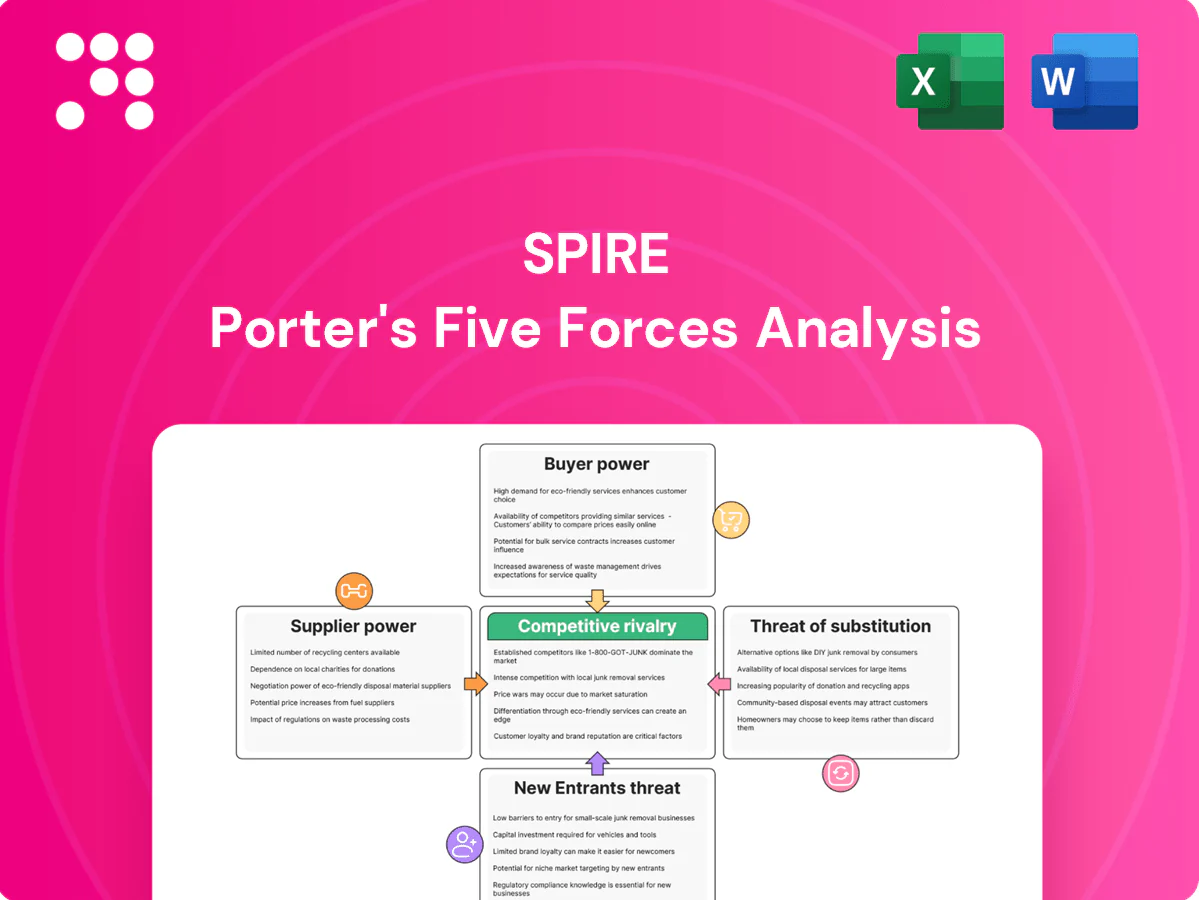

Spire's Porter's Five Forces snapshot highlights moderate buyer power, concentrated suppliers, significant entry barriers, intense competitive rivalry, and limited substitutes. This brief overview surfaces strategic risks and opportunities for growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated upstream gas producers

Spire procures gas from a mix of producers and marketers, but concentration in regional basins like the Marcellus/Utica increases supplier leverage when local output dominates pipeline capacity.

In tight markets producers can steer volumes to higher-priced outlets, while Spire’s long-term contracts and hedging programs mitigate but do not eliminate price exposure.

Ownership of storage assets provides short-term resilience against intra-seasonal price spikes and supply interruptions.

Interstate pipeline dependence

City-gate supply depends on a few FERC-regulated interstate pipelines, which makes those pipes service-critical; firm transportation contracts reduce curtailment risk but impose reservation/demand charges. Peak-season pipeline utilization rose notably in winter 2023–24 per EIA/FERC reports, elevating pipeline bargaining leverage, while contract diversification across multiple pipelines mitigates single‑point failure risk for Spire.

Specialized equipment and materials

Steel pipe, compressors, meters and AMI/SCADA gear come from a concentrated pool of qualified vendors, and strict safety/compliance regimes sharply reduce the approved-supplier list. Lead times and 2024 inflation (US CPI +3.4%) shifted price-power toward suppliers, while multi-year procurement and 3–5 year standardization programs restore some leverage for Spire.

Skilled labor and contractors

Unionized labor and specialized contractors remain essential for Spire’s maintenance and expansions, with US union membership at 10.1% in 2024 (BLS), anchoring bargaining leverage. Tight labor markets in 2024 drove wage and availability pressures for skilled trades, increasing supplier power. Spire’s investment in training and internal crews reduces reliance on third parties, and longer-term workforce planning stabilizes cost volatility.

- Union leverage: 10.1% union membership (2024, BLS)

- Wage pressure: tight 2024 labor markets raised supplier bargaining power

- Mitigation: in-house training and crews cut contractor dependence

- Hedge: workforce planning reduces cost volatility

Storage and peaking services

Access to storage fields and LNG peakers is critical for winter reliability; in 2024 regional working gas inventories were roughly 15–20% below five‑year averages in some Midwest and Northeast hubs, boosting seller leverage during cold snaps. Ownership stakes in storage/LNG peakers improve Spire’s control and margins, but third‑party services remain essential for incremental capacity. Regulatory approvals in 2024 continued to allow pass‑through of prudent peaker and storage costs, mitigating supplier price risk.

- Regional inventories 2024: about 15–20% below 5‑yr avg

- LNG/peaker reliance: critical for peak day events

- Ownership vs third‑party: improves control but not fully substitutable

- Regulatory pass‑throughs: 2024 approvals support cost recovery

Supplier leverage rises as regional gas stocks 15-20% below 5-yr, CPI +3.4%

Regional supplier concentration (Marcellus/Utica) and firm pipeline control raise supplier leverage over Spire.

2024 regional working gas inventories ~15–20% below 5‑yr avg increased spot-price vulnerability during cold snaps.

2024 CPI +3.4% and 10.1% unionization (BLS) elevated equipment/labor costs; long‑term contracts, storage ownership, hedging and in‑house crews mitigate but do not eliminate power.

| Metric | 2024 | Impact |

|---|---|---|

| Regional inventories | −15–20% vs 5‑yr | Higher spot risk |

| CPI | +3.4% | Input cost pressure |

| Union rate | 10.1% | Wage bargaining |

What is included in the product

Tailored Porter's Five Forces analysis for Spire, uncovering competitive drivers, supplier and buyer power, substitutes, and entry threats, while highlighting disruptive forces and strategic defenses to protect market share.

A one-sheet Porter’s Five Forces summary with customizable pressure levels and instant spider/radar visualization—no macros, easy to duplicate for scenario analysis and drop straight into decks or reports.

Customers Bargaining Power

Captive residential customers

Spire’s roughly 1.7 million captive residential customers have limited local distributor alternatives, constraining direct buyer power; state public utility commissions set rates and service standards that effectively protect consumers. With 2024 U.S. residential gas prices near $1.30/therm and electrification retrofit costs often ~$7,000 per household, high switching costs sustain customer stickiness, while satisfaction and safety perceptions still shape regulatory scrutiny.

Large C&I customer negotiations

Large C&I customers buying transportation-only service or bypassing via marketers wield negotiating leverage through load size, influencing rate design and service flexibility, yet their need for physical connectivity and reliability keeps them tied to Spire’s network, which serves roughly 1.7 million customers. Spire’s commercial-industrial contracts often feature customized tariffs to support economic development and retain high-volume accounts. High-volume loads can secure priority scheduling, imbalance tolerances, and discounted rates under negotiated agreements.

Regulatory oversight as proxy power

Public utility commissions act as powerful stand-ins for buyers, scrutinizing prudence, affordability and performance and effectively shaping contract terms. They set allowed returns — the US median authorized ROE was about 9.5% in 2024 per S&P Global Market Intelligence. Rate cases and riders (surcharges, amortizations) balance cost recovery with customer impact. Political pressure and consumer advocates frequently sway major case outcomes.

Demand elasticity and weather

Core residential demand for Spire is relatively inelastic but weather sensitive: extreme cold can lift throughput 15-30% during spikes while triggering customer scrutiny on bills; efficiency gains and tougher building codes have trimmed per-customer use ~1% annually; decoupling mechanisms typically blunt 70-90% of volume risk (2024 industry trend).

- inelastic vs weather

- cold spikes +15-30%

- efficiency ~-1%/yr

- decoupling 70-90%

Choice of competitive gas marketers

In Spires choice programs customers pick commodity suppliers while Spire (serving about 1.7 million gas customers in 2024) retains regulated distribution, increasing price sensitivity on the commodity portion of bills. Distribution charges remain tariffed and less negotiable, limiting customer leverage. Education and transparency on supplier offers materially influence switching rates.

- 2024 customers served: 1.7 million

- Commodity drives short-term price sensitivity

- Distribution charges regulated, limited negotiation

- Transparency/education affect switching

Gas resilience: +15–30% cold spikes, 9.5% ROE

Spire serves ~1.7M customers; residential demand is inelastic but weather-driven (cold spikes +15–30%); switching costs and regulated distribution limit buyer power; commodity price sensitivity (2024 gas ~$1.30/therm) raises short-term leverage for suppliers. Public utility commissions (median authorized ROE ~9.5% in 2024) and decoupling (70–90%) constrain customer bargaining.

| Metric | Value (2024) |

|---|---|

| Customers | 1.7M |

| Residential gas | $1.30/therm |

| Electrification retrofit | ~$7,000/household |

| Cold spike | +15–30% |

| Efficiency trend | −1%/yr |

| Decoupling | 70–90% |

| Authorized ROE | ~9.5% |

Preview the Actual Deliverable

Spire Porter's Five Forces Analysis

This preview displays the exact Spire Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The full document is professionally formatted, comprehensive, and ready for immediate download and use. Purchase grants instant access to this identical file with strategic insights and actionable conclusions.

A Must-Have Tool for Decision-Makers

Spire's Porter's Five Forces snapshot highlights moderate buyer power, concentrated suppliers, significant entry barriers, intense competitive rivalry, and limited substitutes. This brief overview surfaces strategic risks and opportunities for growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated upstream gas producers

Spire procures gas from a mix of producers and marketers, but concentration in regional basins like the Marcellus/Utica increases supplier leverage when local output dominates pipeline capacity.

In tight markets producers can steer volumes to higher-priced outlets, while Spire’s long-term contracts and hedging programs mitigate but do not eliminate price exposure.

Ownership of storage assets provides short-term resilience against intra-seasonal price spikes and supply interruptions.

Interstate pipeline dependence

City-gate supply depends on a few FERC-regulated interstate pipelines, which makes those pipes service-critical; firm transportation contracts reduce curtailment risk but impose reservation/demand charges. Peak-season pipeline utilization rose notably in winter 2023–24 per EIA/FERC reports, elevating pipeline bargaining leverage, while contract diversification across multiple pipelines mitigates single‑point failure risk for Spire.

Specialized equipment and materials

Steel pipe, compressors, meters and AMI/SCADA gear come from a concentrated pool of qualified vendors, and strict safety/compliance regimes sharply reduce the approved-supplier list. Lead times and 2024 inflation (US CPI +3.4%) shifted price-power toward suppliers, while multi-year procurement and 3–5 year standardization programs restore some leverage for Spire.

Skilled labor and contractors

Unionized labor and specialized contractors remain essential for Spire’s maintenance and expansions, with US union membership at 10.1% in 2024 (BLS), anchoring bargaining leverage. Tight labor markets in 2024 drove wage and availability pressures for skilled trades, increasing supplier power. Spire’s investment in training and internal crews reduces reliance on third parties, and longer-term workforce planning stabilizes cost volatility.

- Union leverage: 10.1% union membership (2024, BLS)

- Wage pressure: tight 2024 labor markets raised supplier bargaining power

- Mitigation: in-house training and crews cut contractor dependence

- Hedge: workforce planning reduces cost volatility

Storage and peaking services

Access to storage fields and LNG peakers is critical for winter reliability; in 2024 regional working gas inventories were roughly 15–20% below five‑year averages in some Midwest and Northeast hubs, boosting seller leverage during cold snaps. Ownership stakes in storage/LNG peakers improve Spire’s control and margins, but third‑party services remain essential for incremental capacity. Regulatory approvals in 2024 continued to allow pass‑through of prudent peaker and storage costs, mitigating supplier price risk.

- Regional inventories 2024: about 15–20% below 5‑yr avg

- LNG/peaker reliance: critical for peak day events

- Ownership vs third‑party: improves control but not fully substitutable

- Regulatory pass‑throughs: 2024 approvals support cost recovery

Supplier leverage rises as regional gas stocks 15-20% below 5-yr, CPI +3.4%

Regional supplier concentration (Marcellus/Utica) and firm pipeline control raise supplier leverage over Spire.

2024 regional working gas inventories ~15–20% below 5‑yr avg increased spot-price vulnerability during cold snaps.

2024 CPI +3.4% and 10.1% unionization (BLS) elevated equipment/labor costs; long‑term contracts, storage ownership, hedging and in‑house crews mitigate but do not eliminate power.

| Metric | 2024 | Impact |

|---|---|---|

| Regional inventories | −15–20% vs 5‑yr | Higher spot risk |

| CPI | +3.4% | Input cost pressure |

| Union rate | 10.1% | Wage bargaining |

What is included in the product

Tailored Porter's Five Forces analysis for Spire, uncovering competitive drivers, supplier and buyer power, substitutes, and entry threats, while highlighting disruptive forces and strategic defenses to protect market share.

A one-sheet Porter’s Five Forces summary with customizable pressure levels and instant spider/radar visualization—no macros, easy to duplicate for scenario analysis and drop straight into decks or reports.

Customers Bargaining Power

Captive residential customers

Spire’s roughly 1.7 million captive residential customers have limited local distributor alternatives, constraining direct buyer power; state public utility commissions set rates and service standards that effectively protect consumers. With 2024 U.S. residential gas prices near $1.30/therm and electrification retrofit costs often ~$7,000 per household, high switching costs sustain customer stickiness, while satisfaction and safety perceptions still shape regulatory scrutiny.

Large C&I customer negotiations

Large C&I customers buying transportation-only service or bypassing via marketers wield negotiating leverage through load size, influencing rate design and service flexibility, yet their need for physical connectivity and reliability keeps them tied to Spire’s network, which serves roughly 1.7 million customers. Spire’s commercial-industrial contracts often feature customized tariffs to support economic development and retain high-volume accounts. High-volume loads can secure priority scheduling, imbalance tolerances, and discounted rates under negotiated agreements.

Regulatory oversight as proxy power

Public utility commissions act as powerful stand-ins for buyers, scrutinizing prudence, affordability and performance and effectively shaping contract terms. They set allowed returns — the US median authorized ROE was about 9.5% in 2024 per S&P Global Market Intelligence. Rate cases and riders (surcharges, amortizations) balance cost recovery with customer impact. Political pressure and consumer advocates frequently sway major case outcomes.

Demand elasticity and weather

Core residential demand for Spire is relatively inelastic but weather sensitive: extreme cold can lift throughput 15-30% during spikes while triggering customer scrutiny on bills; efficiency gains and tougher building codes have trimmed per-customer use ~1% annually; decoupling mechanisms typically blunt 70-90% of volume risk (2024 industry trend).

- inelastic vs weather

- cold spikes +15-30%

- efficiency ~-1%/yr

- decoupling 70-90%

Choice of competitive gas marketers

In Spires choice programs customers pick commodity suppliers while Spire (serving about 1.7 million gas customers in 2024) retains regulated distribution, increasing price sensitivity on the commodity portion of bills. Distribution charges remain tariffed and less negotiable, limiting customer leverage. Education and transparency on supplier offers materially influence switching rates.

- 2024 customers served: 1.7 million

- Commodity drives short-term price sensitivity

- Distribution charges regulated, limited negotiation

- Transparency/education affect switching

Gas resilience: +15–30% cold spikes, 9.5% ROE

Spire serves ~1.7M customers; residential demand is inelastic but weather-driven (cold spikes +15–30%); switching costs and regulated distribution limit buyer power; commodity price sensitivity (2024 gas ~$1.30/therm) raises short-term leverage for suppliers. Public utility commissions (median authorized ROE ~9.5% in 2024) and decoupling (70–90%) constrain customer bargaining.

| Metric | Value (2024) |

|---|---|

| Customers | 1.7M |

| Residential gas | $1.30/therm |

| Electrification retrofit | ~$7,000/household |

| Cold spike | +15–30% |

| Efficiency trend | −1%/yr |

| Decoupling | 70–90% |

| Authorized ROE | ~9.5% |

Preview the Actual Deliverable

Spire Porter's Five Forces Analysis

This preview displays the exact Spire Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The full document is professionally formatted, comprehensive, and ready for immediate download and use. Purchase grants instant access to this identical file with strategic insights and actionable conclusions.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Spire's Porter's Five Forces snapshot highlights moderate buyer power, concentrated suppliers, significant entry barriers, intense competitive rivalry, and limited substitutes. This brief overview surfaces strategic risks and opportunities for growth. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy.

Suppliers Bargaining Power

Concentrated upstream gas producers

Spire procures gas from a mix of producers and marketers, but concentration in regional basins like the Marcellus/Utica increases supplier leverage when local output dominates pipeline capacity.

In tight markets producers can steer volumes to higher-priced outlets, while Spire’s long-term contracts and hedging programs mitigate but do not eliminate price exposure.

Ownership of storage assets provides short-term resilience against intra-seasonal price spikes and supply interruptions.

Interstate pipeline dependence

City-gate supply depends on a few FERC-regulated interstate pipelines, which makes those pipes service-critical; firm transportation contracts reduce curtailment risk but impose reservation/demand charges. Peak-season pipeline utilization rose notably in winter 2023–24 per EIA/FERC reports, elevating pipeline bargaining leverage, while contract diversification across multiple pipelines mitigates single‑point failure risk for Spire.

Specialized equipment and materials

Steel pipe, compressors, meters and AMI/SCADA gear come from a concentrated pool of qualified vendors, and strict safety/compliance regimes sharply reduce the approved-supplier list. Lead times and 2024 inflation (US CPI +3.4%) shifted price-power toward suppliers, while multi-year procurement and 3–5 year standardization programs restore some leverage for Spire.

Skilled labor and contractors

Unionized labor and specialized contractors remain essential for Spire’s maintenance and expansions, with US union membership at 10.1% in 2024 (BLS), anchoring bargaining leverage. Tight labor markets in 2024 drove wage and availability pressures for skilled trades, increasing supplier power. Spire’s investment in training and internal crews reduces reliance on third parties, and longer-term workforce planning stabilizes cost volatility.

- Union leverage: 10.1% union membership (2024, BLS)

- Wage pressure: tight 2024 labor markets raised supplier bargaining power

- Mitigation: in-house training and crews cut contractor dependence

- Hedge: workforce planning reduces cost volatility

Storage and peaking services

Access to storage fields and LNG peakers is critical for winter reliability; in 2024 regional working gas inventories were roughly 15–20% below five‑year averages in some Midwest and Northeast hubs, boosting seller leverage during cold snaps. Ownership stakes in storage/LNG peakers improve Spire’s control and margins, but third‑party services remain essential for incremental capacity. Regulatory approvals in 2024 continued to allow pass‑through of prudent peaker and storage costs, mitigating supplier price risk.

- Regional inventories 2024: about 15–20% below 5‑yr avg

- LNG/peaker reliance: critical for peak day events

- Ownership vs third‑party: improves control but not fully substitutable

- Regulatory pass‑throughs: 2024 approvals support cost recovery

Supplier leverage rises as regional gas stocks 15-20% below 5-yr, CPI +3.4%

Regional supplier concentration (Marcellus/Utica) and firm pipeline control raise supplier leverage over Spire.

2024 regional working gas inventories ~15–20% below 5‑yr avg increased spot-price vulnerability during cold snaps.

2024 CPI +3.4% and 10.1% unionization (BLS) elevated equipment/labor costs; long‑term contracts, storage ownership, hedging and in‑house crews mitigate but do not eliminate power.

| Metric | 2024 | Impact |

|---|---|---|

| Regional inventories | −15–20% vs 5‑yr | Higher spot risk |

| CPI | +3.4% | Input cost pressure |

| Union rate | 10.1% | Wage bargaining |

What is included in the product

Tailored Porter's Five Forces analysis for Spire, uncovering competitive drivers, supplier and buyer power, substitutes, and entry threats, while highlighting disruptive forces and strategic defenses to protect market share.

A one-sheet Porter’s Five Forces summary with customizable pressure levels and instant spider/radar visualization—no macros, easy to duplicate for scenario analysis and drop straight into decks or reports.

Customers Bargaining Power

Captive residential customers

Spire’s roughly 1.7 million captive residential customers have limited local distributor alternatives, constraining direct buyer power; state public utility commissions set rates and service standards that effectively protect consumers. With 2024 U.S. residential gas prices near $1.30/therm and electrification retrofit costs often ~$7,000 per household, high switching costs sustain customer stickiness, while satisfaction and safety perceptions still shape regulatory scrutiny.

Large C&I customer negotiations

Large C&I customers buying transportation-only service or bypassing via marketers wield negotiating leverage through load size, influencing rate design and service flexibility, yet their need for physical connectivity and reliability keeps them tied to Spire’s network, which serves roughly 1.7 million customers. Spire’s commercial-industrial contracts often feature customized tariffs to support economic development and retain high-volume accounts. High-volume loads can secure priority scheduling, imbalance tolerances, and discounted rates under negotiated agreements.

Regulatory oversight as proxy power

Public utility commissions act as powerful stand-ins for buyers, scrutinizing prudence, affordability and performance and effectively shaping contract terms. They set allowed returns — the US median authorized ROE was about 9.5% in 2024 per S&P Global Market Intelligence. Rate cases and riders (surcharges, amortizations) balance cost recovery with customer impact. Political pressure and consumer advocates frequently sway major case outcomes.

Demand elasticity and weather

Core residential demand for Spire is relatively inelastic but weather sensitive: extreme cold can lift throughput 15-30% during spikes while triggering customer scrutiny on bills; efficiency gains and tougher building codes have trimmed per-customer use ~1% annually; decoupling mechanisms typically blunt 70-90% of volume risk (2024 industry trend).

- inelastic vs weather

- cold spikes +15-30%

- efficiency ~-1%/yr

- decoupling 70-90%

Choice of competitive gas marketers

In Spires choice programs customers pick commodity suppliers while Spire (serving about 1.7 million gas customers in 2024) retains regulated distribution, increasing price sensitivity on the commodity portion of bills. Distribution charges remain tariffed and less negotiable, limiting customer leverage. Education and transparency on supplier offers materially influence switching rates.

- 2024 customers served: 1.7 million

- Commodity drives short-term price sensitivity

- Distribution charges regulated, limited negotiation

- Transparency/education affect switching

Gas resilience: +15–30% cold spikes, 9.5% ROE

Spire serves ~1.7M customers; residential demand is inelastic but weather-driven (cold spikes +15–30%); switching costs and regulated distribution limit buyer power; commodity price sensitivity (2024 gas ~$1.30/therm) raises short-term leverage for suppliers. Public utility commissions (median authorized ROE ~9.5% in 2024) and decoupling (70–90%) constrain customer bargaining.

| Metric | Value (2024) |

|---|---|

| Customers | 1.7M |

| Residential gas | $1.30/therm |

| Electrification retrofit | ~$7,000/household |

| Cold spike | +15–30% |

| Efficiency trend | −1%/yr |

| Decoupling | 70–90% |

| Authorized ROE | ~9.5% |

Preview the Actual Deliverable

Spire Porter's Five Forces Analysis

This preview displays the exact Spire Porter's Five Forces Analysis you'll receive upon purchase—no placeholders or samples. The full document is professionally formatted, comprehensive, and ready for immediate download and use. Purchase grants instant access to this identical file with strategic insights and actionable conclusions.