Spire SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Spire’s strengths in data-driven services and global footprint face regulation and capital intensity risks, while satellite demand and ESG trends offer growth upside; our full SWOT unpacks strategic options, financial context, and execution risks—purchase the complete, editable Word+Excel report to plan, pitch, or invest with confidence.

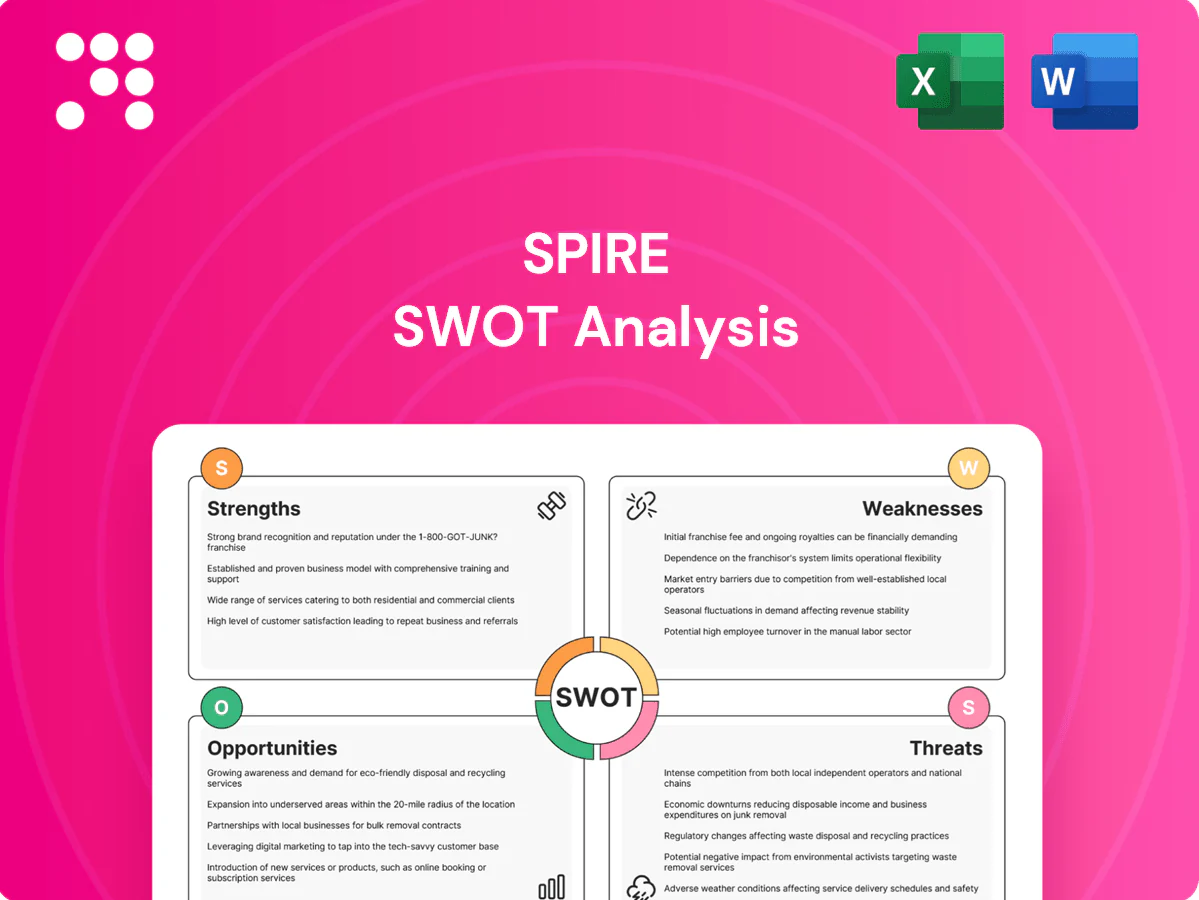

Strengths

Stable regulated revenue

As a regulated natural gas distributor serving about 1.7 million customers, Spire benefits from predictable cost-of-service returns. Regulatory frameworks allow recovery of prudently incurred capital through rates. This stability supports long-term planning and dividend reliability while cushioning cash flows against commodity price volatility.

Diverse customer base and footprint

Spire serves roughly 1.7 million residential, commercial and industrial customers across Alabama, Mississippi and Missouri. Geographic and end-market diversity helps smooth seasonal and sector demand variability. A multi-state footprint strengthens regulatory relationships and benchmarking across three jurisdictions. Cross-system operational learnings improve resiliency and drive efficiency gains.

Integrated assets: pipelines and storage

Ownership of pipelines and underground storage across Spire Missouri, Spire Mississippi and Spire Alabama bolsters supply reliability and flexibility for the ~1.7 million customers served. Vertical integration reduces bottlenecks and supports tighter cost control across the value chain. These assets enable effective peak-shaving and capacity management in cold seasons and generate incremental regulated and contracted earnings streams.

Safety and reliability focus

Utilities build stakeholder trust by delivering safe, reliable, affordable service; Spire serves about 1.7 million customers and emphasizes compliance, proactive maintenance, and rapid emergency responsiveness. A strong safety culture lowers incident rates and regulatory penalties, while high system reliability supports customer satisfaction and constructive rate-case outcomes.

- Stakeholder trust via safety and affordability

- Operating model: compliance, maintenance, emergency response

- Fewer incidents → lower penalties

- Reliability → customer satisfaction & favorable rates

Access to capital and scale efficiencies

As NYSE SR, Spire leverages public markets to fund growth and modernization while serving roughly 1.7 million customers, enabling procurement leverage and O&M efficiencies across its systems; its investment-grade positioning typically reduces borrowing costs over cycles, supporting steady infrastructure investment and grid upgrades.

- Public listing: NYSE SR

- Customer base: ~1.7 million

- Scale benefits: procurement & O&M

- Financial edge: investment-grade borrowing

Regulated natural gas utility serving ~1.7M customers with pipelines, storage, steady dividends

Spire is a regulated natural gas distributor serving ~1.7 million customers, delivering predictable cost-of-service returns and dividend visibility. Its multi-state footprint (Alabama, Mississippi, Missouri) smooths demand variability and enables regulatory benchmarking. Ownership of pipelines and underground storage supports peak-shaving, supply flexibility and operational resiliency. Publicly listed on NYSE (SR) drives capital access and scale efficiencies.

| Metric | Value |

|---|---|

| Customers | ~1.7 million |

| States served | 3 (AL, MS, MO) |

| Public listing | NYSE: SR |

| Key assets | Pipelines & underground storage |

What is included in the product

Delivers a strategic overview of Spire’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and inform strategic decision-making.

Provides a concise SWOT matrix to quickly identify Spire's strategic gaps and relieve decision-making bottlenecks, while an editable format enables fast updates and seamless integration into reports and presentations.

Weaknesses

Regulatory dependence

Earnings growth at Spire is closely tied to regulatory rate cases and approvals, with the company serving about 1.7 million customers across Missouri and Alabama (2024); adverse rulings or delayed filings can compress ROE and cash returns. Multi-jurisdiction oversight increases timing risk and regulatory complexity. Regulatory constraints limit pricing flexibility relative to competitive energy markets.

High capital intensity

Pipeline integrity, storage, and service expansions drive sustained capex—Spire guided roughly $1.1 billion in 2024 capital spending, pressuring cash flow. Heavy investment elevated leverage, with net debt/adjusted EBITDA near 4.2x in mid-2024 and rising interest expense. Cost overruns face prudency reviews and potential regulatory disallowances, limiting financial flexibility in downturns.

Aging infrastructure burden

Legacy pipes and assets across Spire’s 1.7 million-customer system require replacement to meet modern safety and efficiency standards, prompting accelerated replacement programs that raise near-term capital expenditures and rate pressure. Execution missteps during large-scale replacements can trigger reliability or safety incidents, while resulting customer bill impacts increase the risk of regulatory pushback and review on cost recovery mechanisms.

Limited organic growth vectors

Spire's core distribution demand is mature and weather-sensitive, leaving volumes exposed to seasonal swings and conservation that can flatten unit sales. Growth increasingly relies on rate base expansion and regulatory recovery rather than higher throughput. Unregulated ventures remain a smaller share of total earnings, limiting alternative growth drivers.

- Weather-sensitive volumes

- Efficiency/conservation flattening demand

- Growth via rate base, not unit sales

- Unregulated earnings remain small

Commodity perception risk

Commodity perception risk: even with pass-through mechanisms, spikes in wholesale natural gas (Henry Hub topped >9 USD/MMBtu in Aug 2022, EIA) amplify customer bills across Spire’s ~1.7 million customers, raising arrears and political scrutiny. Public perception often blames the utility despite market dynamics, complicating rate strategies and customer programs.

- Higher bills -> increased arrears

- Political/regulatory pressure on rates

- Public misattribution of market-driven costs

Earnings at risk from regulatory delays; 1.7M customers, $1.1B capex, 4.2x leverage

Earnings tied to regulatory rate cases across 1.7M customers; adverse rulings or delays can compress ROE and cash returns.

2024 capex guided ~1.1B; leverage high with net debt/adjusted EBITDA ~4.2x (mid-2024), boosting interest expense.

Legacy pipe replacements raise near-term spend and rate pressure; volumes are weather-sensitive and unregulated earnings remain small.

| Metric | Value |

|---|---|

| Customers | 1.7M (2024) |

| 2024 Capex | ~$1.1B |

| Leverage | Net debt/Adj EBITDA ~4.2x (mid-2024) |

Preview Before You Purchase

Spire SWOT Analysis

This is the actual Spire SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you’ll download after checkout. Buy now to unlock the complete, in-depth version.

Dive Deeper Into the Company’s Strategic Blueprint

Spire’s strengths in data-driven services and global footprint face regulation and capital intensity risks, while satellite demand and ESG trends offer growth upside; our full SWOT unpacks strategic options, financial context, and execution risks—purchase the complete, editable Word+Excel report to plan, pitch, or invest with confidence.

Strengths

Stable regulated revenue

As a regulated natural gas distributor serving about 1.7 million customers, Spire benefits from predictable cost-of-service returns. Regulatory frameworks allow recovery of prudently incurred capital through rates. This stability supports long-term planning and dividend reliability while cushioning cash flows against commodity price volatility.

Diverse customer base and footprint

Spire serves roughly 1.7 million residential, commercial and industrial customers across Alabama, Mississippi and Missouri. Geographic and end-market diversity helps smooth seasonal and sector demand variability. A multi-state footprint strengthens regulatory relationships and benchmarking across three jurisdictions. Cross-system operational learnings improve resiliency and drive efficiency gains.

Integrated assets: pipelines and storage

Ownership of pipelines and underground storage across Spire Missouri, Spire Mississippi and Spire Alabama bolsters supply reliability and flexibility for the ~1.7 million customers served. Vertical integration reduces bottlenecks and supports tighter cost control across the value chain. These assets enable effective peak-shaving and capacity management in cold seasons and generate incremental regulated and contracted earnings streams.

Safety and reliability focus

Utilities build stakeholder trust by delivering safe, reliable, affordable service; Spire serves about 1.7 million customers and emphasizes compliance, proactive maintenance, and rapid emergency responsiveness. A strong safety culture lowers incident rates and regulatory penalties, while high system reliability supports customer satisfaction and constructive rate-case outcomes.

- Stakeholder trust via safety and affordability

- Operating model: compliance, maintenance, emergency response

- Fewer incidents → lower penalties

- Reliability → customer satisfaction & favorable rates

Access to capital and scale efficiencies

As NYSE SR, Spire leverages public markets to fund growth and modernization while serving roughly 1.7 million customers, enabling procurement leverage and O&M efficiencies across its systems; its investment-grade positioning typically reduces borrowing costs over cycles, supporting steady infrastructure investment and grid upgrades.

- Public listing: NYSE SR

- Customer base: ~1.7 million

- Scale benefits: procurement & O&M

- Financial edge: investment-grade borrowing

Regulated natural gas utility serving ~1.7M customers with pipelines, storage, steady dividends

Spire is a regulated natural gas distributor serving ~1.7 million customers, delivering predictable cost-of-service returns and dividend visibility. Its multi-state footprint (Alabama, Mississippi, Missouri) smooths demand variability and enables regulatory benchmarking. Ownership of pipelines and underground storage supports peak-shaving, supply flexibility and operational resiliency. Publicly listed on NYSE (SR) drives capital access and scale efficiencies.

| Metric | Value |

|---|---|

| Customers | ~1.7 million |

| States served | 3 (AL, MS, MO) |

| Public listing | NYSE: SR |

| Key assets | Pipelines & underground storage |

What is included in the product

Delivers a strategic overview of Spire’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and inform strategic decision-making.

Provides a concise SWOT matrix to quickly identify Spire's strategic gaps and relieve decision-making bottlenecks, while an editable format enables fast updates and seamless integration into reports and presentations.

Weaknesses

Regulatory dependence

Earnings growth at Spire is closely tied to regulatory rate cases and approvals, with the company serving about 1.7 million customers across Missouri and Alabama (2024); adverse rulings or delayed filings can compress ROE and cash returns. Multi-jurisdiction oversight increases timing risk and regulatory complexity. Regulatory constraints limit pricing flexibility relative to competitive energy markets.

High capital intensity

Pipeline integrity, storage, and service expansions drive sustained capex—Spire guided roughly $1.1 billion in 2024 capital spending, pressuring cash flow. Heavy investment elevated leverage, with net debt/adjusted EBITDA near 4.2x in mid-2024 and rising interest expense. Cost overruns face prudency reviews and potential regulatory disallowances, limiting financial flexibility in downturns.

Aging infrastructure burden

Legacy pipes and assets across Spire’s 1.7 million-customer system require replacement to meet modern safety and efficiency standards, prompting accelerated replacement programs that raise near-term capital expenditures and rate pressure. Execution missteps during large-scale replacements can trigger reliability or safety incidents, while resulting customer bill impacts increase the risk of regulatory pushback and review on cost recovery mechanisms.

Limited organic growth vectors

Spire's core distribution demand is mature and weather-sensitive, leaving volumes exposed to seasonal swings and conservation that can flatten unit sales. Growth increasingly relies on rate base expansion and regulatory recovery rather than higher throughput. Unregulated ventures remain a smaller share of total earnings, limiting alternative growth drivers.

- Weather-sensitive volumes

- Efficiency/conservation flattening demand

- Growth via rate base, not unit sales

- Unregulated earnings remain small

Commodity perception risk

Commodity perception risk: even with pass-through mechanisms, spikes in wholesale natural gas (Henry Hub topped >9 USD/MMBtu in Aug 2022, EIA) amplify customer bills across Spire’s ~1.7 million customers, raising arrears and political scrutiny. Public perception often blames the utility despite market dynamics, complicating rate strategies and customer programs.

- Higher bills -> increased arrears

- Political/regulatory pressure on rates

- Public misattribution of market-driven costs

Earnings at risk from regulatory delays; 1.7M customers, $1.1B capex, 4.2x leverage

Earnings tied to regulatory rate cases across 1.7M customers; adverse rulings or delays can compress ROE and cash returns.

2024 capex guided ~1.1B; leverage high with net debt/adjusted EBITDA ~4.2x (mid-2024), boosting interest expense.

Legacy pipe replacements raise near-term spend and rate pressure; volumes are weather-sensitive and unregulated earnings remain small.

| Metric | Value |

|---|---|

| Customers | 1.7M (2024) |

| 2024 Capex | ~$1.1B |

| Leverage | Net debt/Adj EBITDA ~4.2x (mid-2024) |

Preview Before You Purchase

Spire SWOT Analysis

This is the actual Spire SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you’ll download after checkout. Buy now to unlock the complete, in-depth version.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Spire’s strengths in data-driven services and global footprint face regulation and capital intensity risks, while satellite demand and ESG trends offer growth upside; our full SWOT unpacks strategic options, financial context, and execution risks—purchase the complete, editable Word+Excel report to plan, pitch, or invest with confidence.

Strengths

Stable regulated revenue

As a regulated natural gas distributor serving about 1.7 million customers, Spire benefits from predictable cost-of-service returns. Regulatory frameworks allow recovery of prudently incurred capital through rates. This stability supports long-term planning and dividend reliability while cushioning cash flows against commodity price volatility.

Diverse customer base and footprint

Spire serves roughly 1.7 million residential, commercial and industrial customers across Alabama, Mississippi and Missouri. Geographic and end-market diversity helps smooth seasonal and sector demand variability. A multi-state footprint strengthens regulatory relationships and benchmarking across three jurisdictions. Cross-system operational learnings improve resiliency and drive efficiency gains.

Integrated assets: pipelines and storage

Ownership of pipelines and underground storage across Spire Missouri, Spire Mississippi and Spire Alabama bolsters supply reliability and flexibility for the ~1.7 million customers served. Vertical integration reduces bottlenecks and supports tighter cost control across the value chain. These assets enable effective peak-shaving and capacity management in cold seasons and generate incremental regulated and contracted earnings streams.

Safety and reliability focus

Utilities build stakeholder trust by delivering safe, reliable, affordable service; Spire serves about 1.7 million customers and emphasizes compliance, proactive maintenance, and rapid emergency responsiveness. A strong safety culture lowers incident rates and regulatory penalties, while high system reliability supports customer satisfaction and constructive rate-case outcomes.

- Stakeholder trust via safety and affordability

- Operating model: compliance, maintenance, emergency response

- Fewer incidents → lower penalties

- Reliability → customer satisfaction & favorable rates

Access to capital and scale efficiencies

As NYSE SR, Spire leverages public markets to fund growth and modernization while serving roughly 1.7 million customers, enabling procurement leverage and O&M efficiencies across its systems; its investment-grade positioning typically reduces borrowing costs over cycles, supporting steady infrastructure investment and grid upgrades.

- Public listing: NYSE SR

- Customer base: ~1.7 million

- Scale benefits: procurement & O&M

- Financial edge: investment-grade borrowing

Regulated natural gas utility serving ~1.7M customers with pipelines, storage, steady dividends

Spire is a regulated natural gas distributor serving ~1.7 million customers, delivering predictable cost-of-service returns and dividend visibility. Its multi-state footprint (Alabama, Mississippi, Missouri) smooths demand variability and enables regulatory benchmarking. Ownership of pipelines and underground storage supports peak-shaving, supply flexibility and operational resiliency. Publicly listed on NYSE (SR) drives capital access and scale efficiencies.

| Metric | Value |

|---|---|

| Customers | ~1.7 million |

| States served | 3 (AL, MS, MO) |

| Public listing | NYSE: SR |

| Key assets | Pipelines & underground storage |

What is included in the product

Delivers a strategic overview of Spire’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and inform strategic decision-making.

Provides a concise SWOT matrix to quickly identify Spire's strategic gaps and relieve decision-making bottlenecks, while an editable format enables fast updates and seamless integration into reports and presentations.

Weaknesses

Regulatory dependence

Earnings growth at Spire is closely tied to regulatory rate cases and approvals, with the company serving about 1.7 million customers across Missouri and Alabama (2024); adverse rulings or delayed filings can compress ROE and cash returns. Multi-jurisdiction oversight increases timing risk and regulatory complexity. Regulatory constraints limit pricing flexibility relative to competitive energy markets.

High capital intensity

Pipeline integrity, storage, and service expansions drive sustained capex—Spire guided roughly $1.1 billion in 2024 capital spending, pressuring cash flow. Heavy investment elevated leverage, with net debt/adjusted EBITDA near 4.2x in mid-2024 and rising interest expense. Cost overruns face prudency reviews and potential regulatory disallowances, limiting financial flexibility in downturns.

Aging infrastructure burden

Legacy pipes and assets across Spire’s 1.7 million-customer system require replacement to meet modern safety and efficiency standards, prompting accelerated replacement programs that raise near-term capital expenditures and rate pressure. Execution missteps during large-scale replacements can trigger reliability or safety incidents, while resulting customer bill impacts increase the risk of regulatory pushback and review on cost recovery mechanisms.

Limited organic growth vectors

Spire's core distribution demand is mature and weather-sensitive, leaving volumes exposed to seasonal swings and conservation that can flatten unit sales. Growth increasingly relies on rate base expansion and regulatory recovery rather than higher throughput. Unregulated ventures remain a smaller share of total earnings, limiting alternative growth drivers.

- Weather-sensitive volumes

- Efficiency/conservation flattening demand

- Growth via rate base, not unit sales

- Unregulated earnings remain small

Commodity perception risk

Commodity perception risk: even with pass-through mechanisms, spikes in wholesale natural gas (Henry Hub topped >9 USD/MMBtu in Aug 2022, EIA) amplify customer bills across Spire’s ~1.7 million customers, raising arrears and political scrutiny. Public perception often blames the utility despite market dynamics, complicating rate strategies and customer programs.

- Higher bills -> increased arrears

- Political/regulatory pressure on rates

- Public misattribution of market-driven costs

Earnings at risk from regulatory delays; 1.7M customers, $1.1B capex, 4.2x leverage

Earnings tied to regulatory rate cases across 1.7M customers; adverse rulings or delays can compress ROE and cash returns.

2024 capex guided ~1.1B; leverage high with net debt/adjusted EBITDA ~4.2x (mid-2024), boosting interest expense.

Legacy pipe replacements raise near-term spend and rate pressure; volumes are weather-sensitive and unregulated earnings remain small.

| Metric | Value |

|---|---|

| Customers | 1.7M (2024) |

| 2024 Capex | ~$1.1B |

| Leverage | Net debt/Adj EBITDA ~4.2x (mid-2024) |

Preview Before You Purchase

Spire SWOT Analysis

This is the actual Spire SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you’ll download after checkout. Buy now to unlock the complete, in-depth version.