Spirit Airlines Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

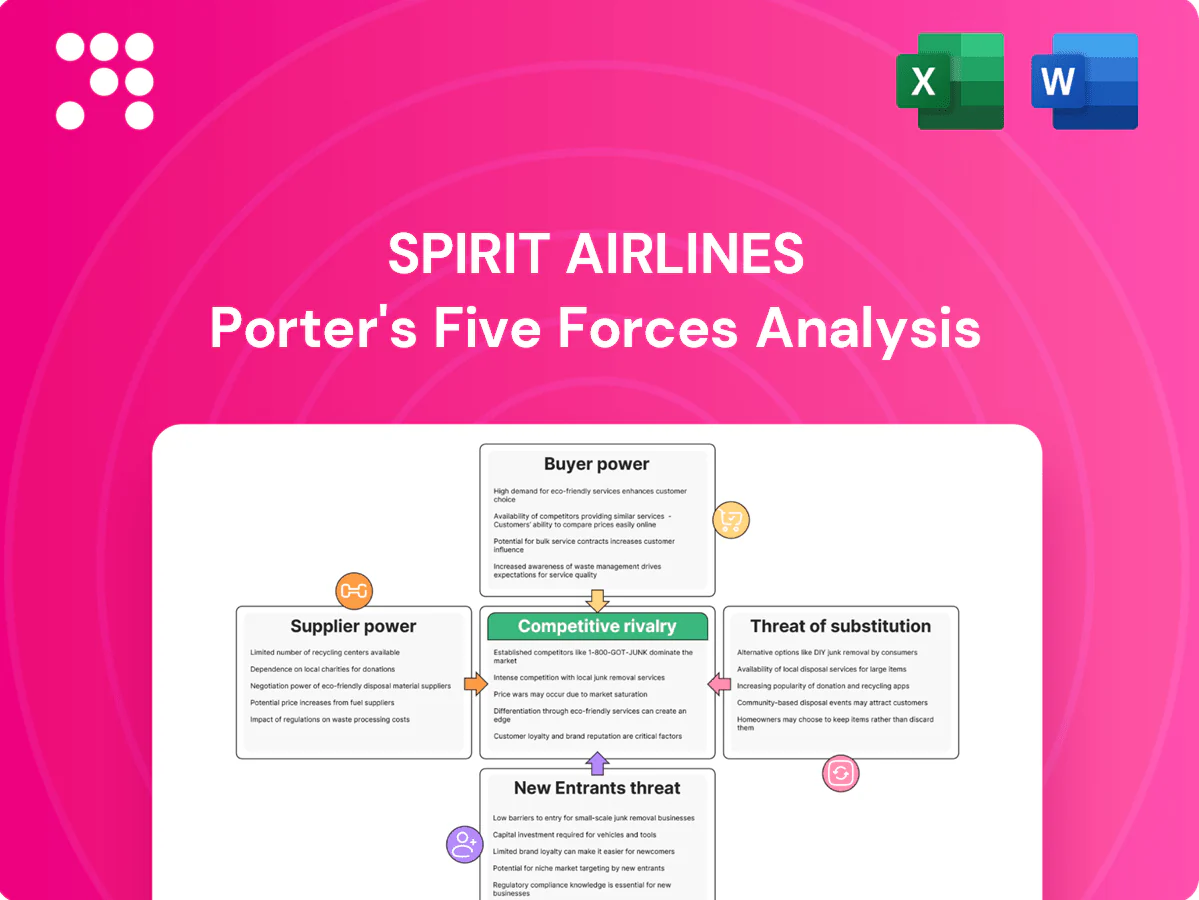

Spirit Airlines faces intense competitive rivalry, high buyer price sensitivity, moderate supplier leverage, growing substitute threats from other low-cost carriers and travel alternatives, and barriers that modestly deter new entrants; this snapshot outlines key pressures shaping margins and route strategy. The full Porter's Five Forces Analysis reveals force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy decisions—unlock it for the complete, consultant-grade breakdown.

Suppliers Bargaining Power

Concentrated aircraft and engine makers

Spirit relies on the Airbus/Boeing duopoly and a small set of engine OEMs like CFM and Pratt & Whitney; Airbus and Boeing together account for over 95% of large commercial jet deliveries, concentrating upstream leverage.

Limited airframe and engine alternatives give manufacturers pricing, delivery-slot and support power, while supply disruptions quickly create capacity shortfalls and higher maintenance or lease costs.

Given ULCCs operate on very thin unit margins, these upstream pressures can materially compress yields and profitability.

Fuel suppliers and price volatility

Jet fuel is a major cost for Spirit, accounting for roughly 25% of operating expenses in 2024; US Gulf Coast jet fuel averaged about $2.90/gal in 2024 (EIA). Refinery and pipeline constraints create regional premiums and limited hedging capacity raises costs. Suppliers face low switching risk but high pricing power, and price spikes compress ULCC fare flexibility and margins.

Airport authorities and gate/slot access

Airports control gates, slots and fees that directly shape Spirit's schedules and unit costs. Congested hubs and the 17 US slot-controlled airports raise airport bargaining power through limited access. ULCCs favor secondary airports for lower fees, but availability tightens in growth markets. Lease terms and infrastructure charges materially alter route economics and margins.

Skilled labor and union dynamics

MRO, parts, and lessor dependence

Maintenance providers and OEMs control airworthiness parts with lead times that have in 2024 driven higher turnaround risk for Spirit, raising AOG costs and deferments. Lessors dictate fleet flexibility, lease rates and residual-value exposure after accelerated retirements, constraining Spirit’s ULCC utilization model. Supply shortages increase check-in-to-service times and maintenance costs, directly limiting block-hour availability.

- Lead-time risk: parts/OEM control

- Lessor power: fleet flexibility & lease rates

- Shortages: higher costs, longer turnarounds

- Impact: reduced utilization, ULCC margin pressure

Supplier squeeze hits ULCC: airframes >95%, fuel ~25%

Spirit faces concentrated airframe/engine suppliers (Airbus+Boeing >95% deliveries) and limited lessor/parts options; 2024 jet fuel ~25% of opex and US Gulf Coast ~$2.90/gal. Pilot shortage (Boeing 2024: ~248,000 needed) and airport slot constraints raise labor and access costs. These supplier pressures transmit directly to yields and ULCC margins.

| Supplier | 2024 metric |

|---|---|

| Airframe | Airbus+Boeing >95% |

| Fuel | ~25% opex; $2.90/gal GCC |

| Pilots | ~248,000 global need |

What is included in the product

Bespoke Porter’s Five Forces analysis for Spirit Airlines uncovering competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/operational barriers, identifying disruptive risks and strategic levers that influence pricing, margins, and market share.

One-sheet Porter's Five Forces for Spirit Airlines that visualizes competitive pressure in a clean spider chart and lets you customize force levels, swap in updated data, and drop straight into pitch decks or dashboards—no macros or finance expertise required.

Customers Bargaining Power

Extreme price sensitivity

Spirit’s customers are highly value-driven, prioritizing lowest total trip cost and often choosing fares advertised as low as $19 one-way in 2024, so small fare differences of $10–20 can trigger switching and reduce pricing power. This compresses margins and elevates elasticity, with promotions and fare sales producing double-digit spikes in short-term bookings and materially shifting demand.

Low switching costs and high transparency

Online travel agencies and metasearch show side-by-side fares and fees, enabling shoppers to compare Spirit with ULCC peers, LCCs, and legacy basic-economy options in seconds. Transparency amplifies buyer power across routes—customers can switch carriers with minimal friction and often lower out-of-pocket cost. In 2024 Spirit’s ancillary revenue remained a critical lever (roughly 30% of revenue and about $72 ancillary per passenger), so unbundling must stay competitive to avoid churn.

Limited loyalty lock-in

ULCC loyalty programs exert limited pull versus legacy carriers’ elite perks and global networks, and Free Spirit’s benefits remain low-friction; ancillaries accounted for roughly 40% of Spirit’s revenue in 2024, underscoring price-led demand. Irregular travelers dominate Spirit’s mix, reducing stickiness and repeat bookings. Co-branded credit card tie-ins boost retention but are less decisive for budget segments, so minimal lock-in raises buyer leverage.

Sensitivity to total price including ancillaries

Customers judge Spirit by all-in cost—base fare plus baggage, seat selection and change fees—and in 2024 ancillaries account for roughly 40% of Spirit’s revenue, raising sensitivity to perceived nickel-and-diming. If competitors’ bundles appear cheaper, churn rises; transparent pricing and dynamic bundles reduce pushback while ancillary pricing must balance yield with perceived fairness.

- All-in cost focus

- 40% ancillaries (2024)

- Bundling lowers churn

- Transparency + dynamic offers

Social proof and service perception

- Reviews drive rapid booking changes

- Disruptions/fees deter purchases

- Reputation shifts boost rival bookings

$19 fares, $72 ancillaries, $10-20 churn

Customers are highly price-sensitive; advertised $19 one-way fares in 2024 mean $10–20 fare differences trigger switching, compressing margins and raising elasticity. Ancillaries (≈40% of revenue in 2024; about $72 per passenger) are critical yet increase churn risk if perceived as nickel-and-diming. OTA/metasearch transparency and low switching costs amplify buyer power and reputation-driven demand swings.

| Metric | 2024 Value |

|---|---|

| Ancillary share | ≈40% |

| Ancillary per passenger | $72 |

| Lowest advertised fare | $19 one-way |

| Switch trigger | $10–20 |

Preview the Actual Deliverable

Spirit Airlines Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Spirit Airlines you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written and ready for immediate download and use. You’re previewing the final deliverable.

Go Beyond the Preview—Access the Full Strategic Report

Spirit Airlines faces intense competitive rivalry, high buyer price sensitivity, moderate supplier leverage, growing substitute threats from other low-cost carriers and travel alternatives, and barriers that modestly deter new entrants; this snapshot outlines key pressures shaping margins and route strategy. The full Porter's Five Forces Analysis reveals force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy decisions—unlock it for the complete, consultant-grade breakdown.

Suppliers Bargaining Power

Concentrated aircraft and engine makers

Spirit relies on the Airbus/Boeing duopoly and a small set of engine OEMs like CFM and Pratt & Whitney; Airbus and Boeing together account for over 95% of large commercial jet deliveries, concentrating upstream leverage.

Limited airframe and engine alternatives give manufacturers pricing, delivery-slot and support power, while supply disruptions quickly create capacity shortfalls and higher maintenance or lease costs.

Given ULCCs operate on very thin unit margins, these upstream pressures can materially compress yields and profitability.

Fuel suppliers and price volatility

Jet fuel is a major cost for Spirit, accounting for roughly 25% of operating expenses in 2024; US Gulf Coast jet fuel averaged about $2.90/gal in 2024 (EIA). Refinery and pipeline constraints create regional premiums and limited hedging capacity raises costs. Suppliers face low switching risk but high pricing power, and price spikes compress ULCC fare flexibility and margins.

Airport authorities and gate/slot access

Airports control gates, slots and fees that directly shape Spirit's schedules and unit costs. Congested hubs and the 17 US slot-controlled airports raise airport bargaining power through limited access. ULCCs favor secondary airports for lower fees, but availability tightens in growth markets. Lease terms and infrastructure charges materially alter route economics and margins.

Skilled labor and union dynamics

MRO, parts, and lessor dependence

Maintenance providers and OEMs control airworthiness parts with lead times that have in 2024 driven higher turnaround risk for Spirit, raising AOG costs and deferments. Lessors dictate fleet flexibility, lease rates and residual-value exposure after accelerated retirements, constraining Spirit’s ULCC utilization model. Supply shortages increase check-in-to-service times and maintenance costs, directly limiting block-hour availability.

- Lead-time risk: parts/OEM control

- Lessor power: fleet flexibility & lease rates

- Shortages: higher costs, longer turnarounds

- Impact: reduced utilization, ULCC margin pressure

Supplier squeeze hits ULCC: airframes >95%, fuel ~25%

Spirit faces concentrated airframe/engine suppliers (Airbus+Boeing >95% deliveries) and limited lessor/parts options; 2024 jet fuel ~25% of opex and US Gulf Coast ~$2.90/gal. Pilot shortage (Boeing 2024: ~248,000 needed) and airport slot constraints raise labor and access costs. These supplier pressures transmit directly to yields and ULCC margins.

| Supplier | 2024 metric |

|---|---|

| Airframe | Airbus+Boeing >95% |

| Fuel | ~25% opex; $2.90/gal GCC |

| Pilots | ~248,000 global need |

What is included in the product

Bespoke Porter’s Five Forces analysis for Spirit Airlines uncovering competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/operational barriers, identifying disruptive risks and strategic levers that influence pricing, margins, and market share.

One-sheet Porter's Five Forces for Spirit Airlines that visualizes competitive pressure in a clean spider chart and lets you customize force levels, swap in updated data, and drop straight into pitch decks or dashboards—no macros or finance expertise required.

Customers Bargaining Power

Extreme price sensitivity

Spirit’s customers are highly value-driven, prioritizing lowest total trip cost and often choosing fares advertised as low as $19 one-way in 2024, so small fare differences of $10–20 can trigger switching and reduce pricing power. This compresses margins and elevates elasticity, with promotions and fare sales producing double-digit spikes in short-term bookings and materially shifting demand.

Low switching costs and high transparency

Online travel agencies and metasearch show side-by-side fares and fees, enabling shoppers to compare Spirit with ULCC peers, LCCs, and legacy basic-economy options in seconds. Transparency amplifies buyer power across routes—customers can switch carriers with minimal friction and often lower out-of-pocket cost. In 2024 Spirit’s ancillary revenue remained a critical lever (roughly 30% of revenue and about $72 ancillary per passenger), so unbundling must stay competitive to avoid churn.

Limited loyalty lock-in

ULCC loyalty programs exert limited pull versus legacy carriers’ elite perks and global networks, and Free Spirit’s benefits remain low-friction; ancillaries accounted for roughly 40% of Spirit’s revenue in 2024, underscoring price-led demand. Irregular travelers dominate Spirit’s mix, reducing stickiness and repeat bookings. Co-branded credit card tie-ins boost retention but are less decisive for budget segments, so minimal lock-in raises buyer leverage.

Sensitivity to total price including ancillaries

Customers judge Spirit by all-in cost—base fare plus baggage, seat selection and change fees—and in 2024 ancillaries account for roughly 40% of Spirit’s revenue, raising sensitivity to perceived nickel-and-diming. If competitors’ bundles appear cheaper, churn rises; transparent pricing and dynamic bundles reduce pushback while ancillary pricing must balance yield with perceived fairness.

- All-in cost focus

- 40% ancillaries (2024)

- Bundling lowers churn

- Transparency + dynamic offers

Social proof and service perception

- Reviews drive rapid booking changes

- Disruptions/fees deter purchases

- Reputation shifts boost rival bookings

$19 fares, $72 ancillaries, $10-20 churn

Customers are highly price-sensitive; advertised $19 one-way fares in 2024 mean $10–20 fare differences trigger switching, compressing margins and raising elasticity. Ancillaries (≈40% of revenue in 2024; about $72 per passenger) are critical yet increase churn risk if perceived as nickel-and-diming. OTA/metasearch transparency and low switching costs amplify buyer power and reputation-driven demand swings.

| Metric | 2024 Value |

|---|---|

| Ancillary share | ≈40% |

| Ancillary per passenger | $72 |

| Lowest advertised fare | $19 one-way |

| Switch trigger | $10–20 |

Preview the Actual Deliverable

Spirit Airlines Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Spirit Airlines you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written and ready for immediate download and use. You’re previewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Spirit Airlines faces intense competitive rivalry, high buyer price sensitivity, moderate supplier leverage, growing substitute threats from other low-cost carriers and travel alternatives, and barriers that modestly deter new entrants; this snapshot outlines key pressures shaping margins and route strategy. The full Porter's Five Forces Analysis reveals force-by-force ratings, visuals, and actionable recommendations to inform investment or strategy decisions—unlock it for the complete, consultant-grade breakdown.

Suppliers Bargaining Power

Concentrated aircraft and engine makers

Spirit relies on the Airbus/Boeing duopoly and a small set of engine OEMs like CFM and Pratt & Whitney; Airbus and Boeing together account for over 95% of large commercial jet deliveries, concentrating upstream leverage.

Limited airframe and engine alternatives give manufacturers pricing, delivery-slot and support power, while supply disruptions quickly create capacity shortfalls and higher maintenance or lease costs.

Given ULCCs operate on very thin unit margins, these upstream pressures can materially compress yields and profitability.

Fuel suppliers and price volatility

Jet fuel is a major cost for Spirit, accounting for roughly 25% of operating expenses in 2024; US Gulf Coast jet fuel averaged about $2.90/gal in 2024 (EIA). Refinery and pipeline constraints create regional premiums and limited hedging capacity raises costs. Suppliers face low switching risk but high pricing power, and price spikes compress ULCC fare flexibility and margins.

Airport authorities and gate/slot access

Airports control gates, slots and fees that directly shape Spirit's schedules and unit costs. Congested hubs and the 17 US slot-controlled airports raise airport bargaining power through limited access. ULCCs favor secondary airports for lower fees, but availability tightens in growth markets. Lease terms and infrastructure charges materially alter route economics and margins.

Skilled labor and union dynamics

MRO, parts, and lessor dependence

Maintenance providers and OEMs control airworthiness parts with lead times that have in 2024 driven higher turnaround risk for Spirit, raising AOG costs and deferments. Lessors dictate fleet flexibility, lease rates and residual-value exposure after accelerated retirements, constraining Spirit’s ULCC utilization model. Supply shortages increase check-in-to-service times and maintenance costs, directly limiting block-hour availability.

- Lead-time risk: parts/OEM control

- Lessor power: fleet flexibility & lease rates

- Shortages: higher costs, longer turnarounds

- Impact: reduced utilization, ULCC margin pressure

Supplier squeeze hits ULCC: airframes >95%, fuel ~25%

Spirit faces concentrated airframe/engine suppliers (Airbus+Boeing >95% deliveries) and limited lessor/parts options; 2024 jet fuel ~25% of opex and US Gulf Coast ~$2.90/gal. Pilot shortage (Boeing 2024: ~248,000 needed) and airport slot constraints raise labor and access costs. These supplier pressures transmit directly to yields and ULCC margins.

| Supplier | 2024 metric |

|---|---|

| Airframe | Airbus+Boeing >95% |

| Fuel | ~25% opex; $2.90/gal GCC |

| Pilots | ~248,000 global need |

What is included in the product

Bespoke Porter’s Five Forces analysis for Spirit Airlines uncovering competitive intensity, buyer and supplier bargaining power, threat of new entrants and substitutes, and regulatory/operational barriers, identifying disruptive risks and strategic levers that influence pricing, margins, and market share.

One-sheet Porter's Five Forces for Spirit Airlines that visualizes competitive pressure in a clean spider chart and lets you customize force levels, swap in updated data, and drop straight into pitch decks or dashboards—no macros or finance expertise required.

Customers Bargaining Power

Extreme price sensitivity

Spirit’s customers are highly value-driven, prioritizing lowest total trip cost and often choosing fares advertised as low as $19 one-way in 2024, so small fare differences of $10–20 can trigger switching and reduce pricing power. This compresses margins and elevates elasticity, with promotions and fare sales producing double-digit spikes in short-term bookings and materially shifting demand.

Low switching costs and high transparency

Online travel agencies and metasearch show side-by-side fares and fees, enabling shoppers to compare Spirit with ULCC peers, LCCs, and legacy basic-economy options in seconds. Transparency amplifies buyer power across routes—customers can switch carriers with minimal friction and often lower out-of-pocket cost. In 2024 Spirit’s ancillary revenue remained a critical lever (roughly 30% of revenue and about $72 ancillary per passenger), so unbundling must stay competitive to avoid churn.

Limited loyalty lock-in

ULCC loyalty programs exert limited pull versus legacy carriers’ elite perks and global networks, and Free Spirit’s benefits remain low-friction; ancillaries accounted for roughly 40% of Spirit’s revenue in 2024, underscoring price-led demand. Irregular travelers dominate Spirit’s mix, reducing stickiness and repeat bookings. Co-branded credit card tie-ins boost retention but are less decisive for budget segments, so minimal lock-in raises buyer leverage.

Sensitivity to total price including ancillaries

Customers judge Spirit by all-in cost—base fare plus baggage, seat selection and change fees—and in 2024 ancillaries account for roughly 40% of Spirit’s revenue, raising sensitivity to perceived nickel-and-diming. If competitors’ bundles appear cheaper, churn rises; transparent pricing and dynamic bundles reduce pushback while ancillary pricing must balance yield with perceived fairness.

- All-in cost focus

- 40% ancillaries (2024)

- Bundling lowers churn

- Transparency + dynamic offers

Social proof and service perception

- Reviews drive rapid booking changes

- Disruptions/fees deter purchases

- Reputation shifts boost rival bookings

$19 fares, $72 ancillaries, $10-20 churn

Customers are highly price-sensitive; advertised $19 one-way fares in 2024 mean $10–20 fare differences trigger switching, compressing margins and raising elasticity. Ancillaries (≈40% of revenue in 2024; about $72 per passenger) are critical yet increase churn risk if perceived as nickel-and-diming. OTA/metasearch transparency and low switching costs amplify buyer power and reputation-driven demand swings.

| Metric | 2024 Value |

|---|---|

| Ancillary share | ≈40% |

| Ancillary per passenger | $72 |

| Lowest advertised fare | $19 one-way |

| Switch trigger | $10–20 |

Preview the Actual Deliverable

Spirit Airlines Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Spirit Airlines you'll receive immediately after purchase—no surprises or placeholders. The document is fully formatted, professionally written and ready for immediate download and use. You’re previewing the final deliverable.