STMicroelectronics Porter's Five Forces Analysis

From Overview to Strategy Blueprint

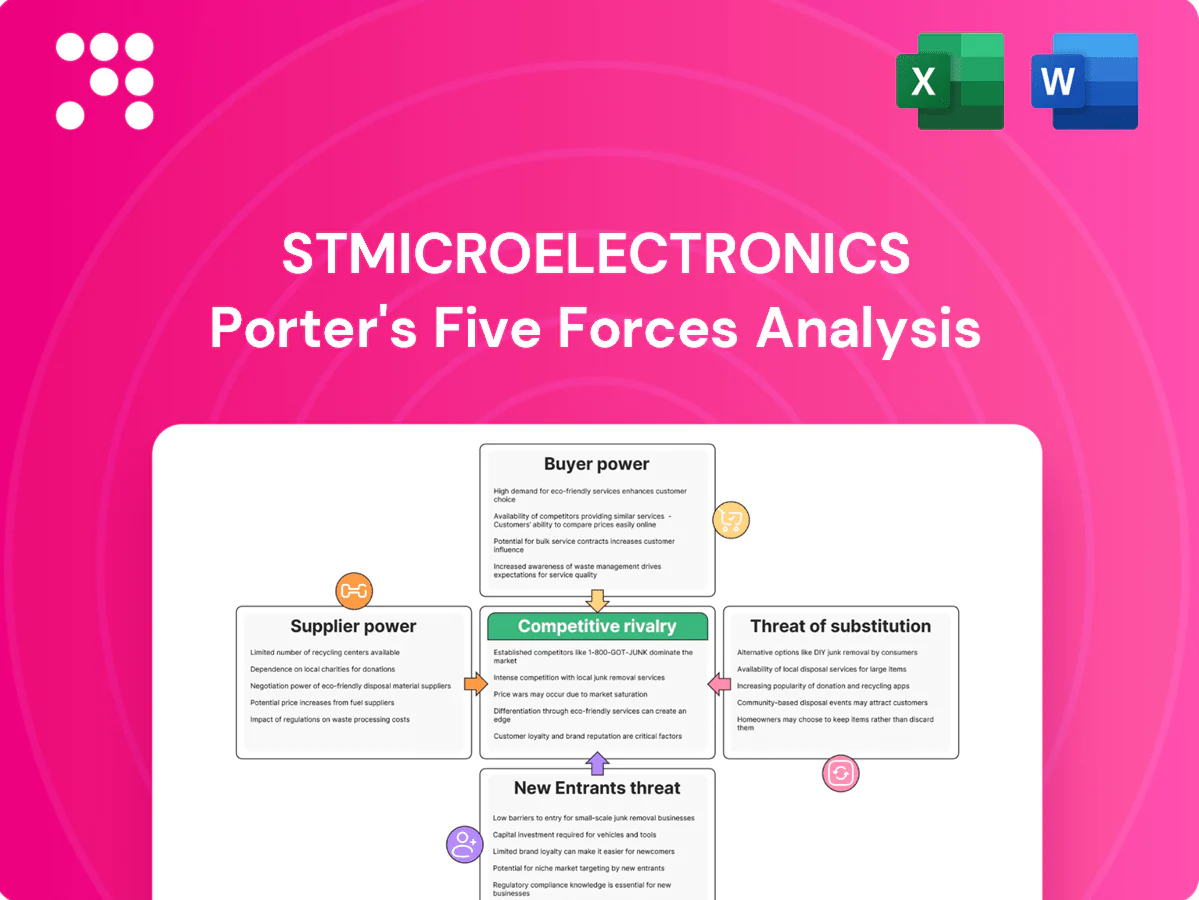

STMicroelectronics faces intense competitive rivalry amid cyclical semiconductor demand, moderate supplier leverage for specialized nodes, elevated buyer power from large OEMs, limited threat of new entrants due to high capital intensity, and moderate substitute risks from alternative technologies. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a complete, actionable breakdown.

Suppliers Bargaining Power

Concentrated equipment vendors

ST relies on a tiny set of critical toolmakers—ASML (greater than 90% share in EUV), Applied Materials and KLA—giving suppliers strong leverage; EUV/advanced DUV lead times commonly run 12–36 months and ASML backlog remains multi-year (2024), so any disruption or upgrade delay can bottleneck ramp plans and node transitions. Long service cycles and complex qualification make multi-sourcing largely impractical.

Scarce advanced materials

Silicon carbide wafers, specialty gases, photoresists and advanced substrates remain concentrated among fewer than 10 global suppliers, creating capacity constraints and supplier pricing power. SiC supply is especially tight with lead times commonly 6–12 months and industry reports spot wafer prices rising about 20% between 2022–24. Long-term take-or-pay contracts are widely used to secure volumes, and new-source qualification typically requires 12–24 months due to strict reliability demands.

EDA/IP tool dependence

Design flows rely on a few EDA/IP vendors—top three EDA suppliers hold over 70% market share—creating material switching costs and license exposure for STMicroelectronics. ARM IP underpins roughly 90% of smartphones, reinforcing architectural lock-in, while foundry PDK alignment with TSMC (over 50% global foundry share) tightens dependency. Price hikes, license limits or US export controls since 2022 can delay projects and restrict vendor choice.

Geopolitical and compliance risks

Geopolitical and compliance risks raise supplier leverage over STMicroelectronics as 2024 expansions of US and allied export controls and ongoing China trade tensions constrain tool and material availability, especially for advanced packaging and specialty chemicals. Region-specific approvals and certification requirements repeatedly delay shipments or force redesigns, while tight markets see suppliers prioritizing strategic regions. Compliance and carbon-related regulation costs are typically passed through to device makers like ST, squeezing margins.

- Export controls 2024: reduced access to advanced tooling in constrained markets

- Region approvals: cause shipment delays and redesigns

- Priority allocation: suppliers favor key regions in shortages

- Cost pass-through: compliance and environmental costs borne by device makers

Mitigation via partial vertical integration

ST’s partial vertical integration — six internal wafer fabs and in-house SiC device manufacturing — plus multi-year supply agreements in 2024 reduce some supplier leverage; co-development with key vendors aligns roadmaps and improves production priority. Upstream concentration in SiC substrates (few suppliers such as Wolfspeed and II‑VI) keeps supplier bargaining power moderately high, and diversification programs will take several years to materially shift leverage.

- Internal fabs: six sites (2024)

- SiC: in-house device production

- Long-term contracts: lower short-term risk

- Upstream concentration: supplier-centric

- Diversification: multi-year impact

Supplier concentration drives leverage: EUV > 90%, foundry ~50%

Suppliers hold high leverage: ASML >90% EUV share, EUV lead times 12–36 months (2024); top three EDA vendors >70% share; TSMC ~50% foundry share. SiC wafers tight with 6–12 month lead times and ~20% spot price rise 2022–24. ST’s six fabs and long-term contracts mitigate but upstream concentration leaves bargaining power moderately high.

| Supplier | Concentration | Lead time | 2022–24 change |

|---|---|---|---|

| ASML (EUV) | >90% | 12–36m | backlog multi‑year (2024) |

| EDA vendors | >70% (top3) | n/a | license cost up |

| SiC wafers | few suppliers | 6–12m | +≈20% price |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for STMicroelectronics, identifying disruptive forces, supplier and buyer power, substitutes, and barriers shaping its pricing, profitability and strategic positioning.

A clear, one-sheet Porter's Five Forces summary tailored to STMicroelectronics—perfect for quick strategic decisions and investor briefings; customize pressure levels as market or technology risks evolve.

Customers Bargaining Power

Large OEMs with scale

Large OEMs in automotive, industrial and consumer electronics buy at scale—the global semiconductor market reached about $600B in 2024 and the automotive segment was roughly $70B—giving these buyers strong price negotiation and strict SLA demands. Dual-sourcing by OEMs forces suppliers like STMicroelectronics into competitive pricing and capacity allocation. Consolidation among Tier-1s increases buyer leverage, and volume commitments often come with downward ASP pressure.

High switching costs in auto/industrial

Long qualification cycles (AEC-Q commonly 6–18 months) and safety certification tracks (ISO 26262/functional safety often 12–24 months) plus firmware/software dependencies lock designs to STMicro, making redesigns costly and revalidation often >$100,000 and time-consuming, which dampens buyer switching and weakens buyer power after a design-win; however OEMs still use upfront bidding to compress pricing before lock-in.

Design influence and customization

Buyers demand tailored reference designs, firmware and white‑glove support, raising service burden and push costs higher; in 2024 STMicroelectronics reported ~€16.4B revenue, making design wins critical to margins. Early customer engagement gives powerful leverage over roadmaps and pricing, and failure to hit performance‑per‑watt targets can forfeit sockets to competitors. Value‑added support helps recover pricing pressure but only partially offsets lost ASPs.

Transparency and benchmark pricing

Market visibility on node, die size and device benchmarks gives buyers leverage in negotiations; STMicroelectronics reported 2024 revenue of $15.8B, exposing commodity discretes to tight price comparisons while complex analog/MEMS and power modules retain better margin defensibility. LTAs indexed to metal/CPI or quarterly ASPs help balance volatility with buyer expectations.

- Transparency enables benchmark-driven price pressure

- Discretes behave like commodities; margins compress

- Analog/MEMS, power modules offer higher stickiness

- Indexed LTAs mitigate short-term volatility

Aftermarket and lifecycle demands

Long product lifecycles in automotive and industrial segments (often 10+ years) force ST to offer extended supply and last-time-buy flexibility, with buyers demanding longevity commitments and PPAP-level quality rigor that can compress margins. These aftermarket obligations increase inventory and testing costs, though STs reliable delivery performance can blunt buyer leverage by ensuring continuity for OEM production.

OEM scale and long qualifications lock buyers while tendering compresses ASPs

Large OEMs (auto, industrial, consumer) buy at scale—global sem market ~$600B (2024), automotive ~$70B—giving strong price/SLA leverage over ST (revenue €16.4B in 2024). Long qualification (AEC‑Q 6–18m, ISO26262 12–24m) and redesign costs >€100k reduce switching but OEM bidding compresses ASPs. Discretes face commodity pricing; analog/MEMS and power modules retain higher stickiness. LTAs/indexing mitigate volatility.

| Metric | Value (2024) |

|---|---|

| Global semiconductor market | $600B |

| Automotive segment | $70B |

| STMicroelectronics revenue | €16.4B |

| AEC‑Q qualification | 6–18 months |

| ISO 26262 | 12–24 months |

| Redesign/revalidation cost | >€100k |

| Product lifecycle | 10+ years |

What You See Is What You Get

STMicroelectronics Porter's Five Forces Analysis

This preview shows the exact STMicroelectronics Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, ready to download and use, and contains the complete strategic assessment you see here. Instant access upon payment.

From Overview to Strategy Blueprint

STMicroelectronics faces intense competitive rivalry amid cyclical semiconductor demand, moderate supplier leverage for specialized nodes, elevated buyer power from large OEMs, limited threat of new entrants due to high capital intensity, and moderate substitute risks from alternative technologies. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a complete, actionable breakdown.

Suppliers Bargaining Power

Concentrated equipment vendors

ST relies on a tiny set of critical toolmakers—ASML (greater than 90% share in EUV), Applied Materials and KLA—giving suppliers strong leverage; EUV/advanced DUV lead times commonly run 12–36 months and ASML backlog remains multi-year (2024), so any disruption or upgrade delay can bottleneck ramp plans and node transitions. Long service cycles and complex qualification make multi-sourcing largely impractical.

Scarce advanced materials

Silicon carbide wafers, specialty gases, photoresists and advanced substrates remain concentrated among fewer than 10 global suppliers, creating capacity constraints and supplier pricing power. SiC supply is especially tight with lead times commonly 6–12 months and industry reports spot wafer prices rising about 20% between 2022–24. Long-term take-or-pay contracts are widely used to secure volumes, and new-source qualification typically requires 12–24 months due to strict reliability demands.

EDA/IP tool dependence

Design flows rely on a few EDA/IP vendors—top three EDA suppliers hold over 70% market share—creating material switching costs and license exposure for STMicroelectronics. ARM IP underpins roughly 90% of smartphones, reinforcing architectural lock-in, while foundry PDK alignment with TSMC (over 50% global foundry share) tightens dependency. Price hikes, license limits or US export controls since 2022 can delay projects and restrict vendor choice.

Geopolitical and compliance risks

Geopolitical and compliance risks raise supplier leverage over STMicroelectronics as 2024 expansions of US and allied export controls and ongoing China trade tensions constrain tool and material availability, especially for advanced packaging and specialty chemicals. Region-specific approvals and certification requirements repeatedly delay shipments or force redesigns, while tight markets see suppliers prioritizing strategic regions. Compliance and carbon-related regulation costs are typically passed through to device makers like ST, squeezing margins.

- Export controls 2024: reduced access to advanced tooling in constrained markets

- Region approvals: cause shipment delays and redesigns

- Priority allocation: suppliers favor key regions in shortages

- Cost pass-through: compliance and environmental costs borne by device makers

Mitigation via partial vertical integration

ST’s partial vertical integration — six internal wafer fabs and in-house SiC device manufacturing — plus multi-year supply agreements in 2024 reduce some supplier leverage; co-development with key vendors aligns roadmaps and improves production priority. Upstream concentration in SiC substrates (few suppliers such as Wolfspeed and II‑VI) keeps supplier bargaining power moderately high, and diversification programs will take several years to materially shift leverage.

- Internal fabs: six sites (2024)

- SiC: in-house device production

- Long-term contracts: lower short-term risk

- Upstream concentration: supplier-centric

- Diversification: multi-year impact

Supplier concentration drives leverage: EUV > 90%, foundry ~50%

Suppliers hold high leverage: ASML >90% EUV share, EUV lead times 12–36 months (2024); top three EDA vendors >70% share; TSMC ~50% foundry share. SiC wafers tight with 6–12 month lead times and ~20% spot price rise 2022–24. ST’s six fabs and long-term contracts mitigate but upstream concentration leaves bargaining power moderately high.

| Supplier | Concentration | Lead time | 2022–24 change |

|---|---|---|---|

| ASML (EUV) | >90% | 12–36m | backlog multi‑year (2024) |

| EDA vendors | >70% (top3) | n/a | license cost up |

| SiC wafers | few suppliers | 6–12m | +≈20% price |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for STMicroelectronics, identifying disruptive forces, supplier and buyer power, substitutes, and barriers shaping its pricing, profitability and strategic positioning.

A clear, one-sheet Porter's Five Forces summary tailored to STMicroelectronics—perfect for quick strategic decisions and investor briefings; customize pressure levels as market or technology risks evolve.

Customers Bargaining Power

Large OEMs with scale

Large OEMs in automotive, industrial and consumer electronics buy at scale—the global semiconductor market reached about $600B in 2024 and the automotive segment was roughly $70B—giving these buyers strong price negotiation and strict SLA demands. Dual-sourcing by OEMs forces suppliers like STMicroelectronics into competitive pricing and capacity allocation. Consolidation among Tier-1s increases buyer leverage, and volume commitments often come with downward ASP pressure.

High switching costs in auto/industrial

Long qualification cycles (AEC-Q commonly 6–18 months) and safety certification tracks (ISO 26262/functional safety often 12–24 months) plus firmware/software dependencies lock designs to STMicro, making redesigns costly and revalidation often >$100,000 and time-consuming, which dampens buyer switching and weakens buyer power after a design-win; however OEMs still use upfront bidding to compress pricing before lock-in.

Design influence and customization

Buyers demand tailored reference designs, firmware and white‑glove support, raising service burden and push costs higher; in 2024 STMicroelectronics reported ~€16.4B revenue, making design wins critical to margins. Early customer engagement gives powerful leverage over roadmaps and pricing, and failure to hit performance‑per‑watt targets can forfeit sockets to competitors. Value‑added support helps recover pricing pressure but only partially offsets lost ASPs.

Transparency and benchmark pricing

Market visibility on node, die size and device benchmarks gives buyers leverage in negotiations; STMicroelectronics reported 2024 revenue of $15.8B, exposing commodity discretes to tight price comparisons while complex analog/MEMS and power modules retain better margin defensibility. LTAs indexed to metal/CPI or quarterly ASPs help balance volatility with buyer expectations.

- Transparency enables benchmark-driven price pressure

- Discretes behave like commodities; margins compress

- Analog/MEMS, power modules offer higher stickiness

- Indexed LTAs mitigate short-term volatility

Aftermarket and lifecycle demands

Long product lifecycles in automotive and industrial segments (often 10+ years) force ST to offer extended supply and last-time-buy flexibility, with buyers demanding longevity commitments and PPAP-level quality rigor that can compress margins. These aftermarket obligations increase inventory and testing costs, though STs reliable delivery performance can blunt buyer leverage by ensuring continuity for OEM production.

OEM scale and long qualifications lock buyers while tendering compresses ASPs

Large OEMs (auto, industrial, consumer) buy at scale—global sem market ~$600B (2024), automotive ~$70B—giving strong price/SLA leverage over ST (revenue €16.4B in 2024). Long qualification (AEC‑Q 6–18m, ISO26262 12–24m) and redesign costs >€100k reduce switching but OEM bidding compresses ASPs. Discretes face commodity pricing; analog/MEMS and power modules retain higher stickiness. LTAs/indexing mitigate volatility.

| Metric | Value (2024) |

|---|---|

| Global semiconductor market | $600B |

| Automotive segment | $70B |

| STMicroelectronics revenue | €16.4B |

| AEC‑Q qualification | 6–18 months |

| ISO 26262 | 12–24 months |

| Redesign/revalidation cost | >€100k |

| Product lifecycle | 10+ years |

What You See Is What You Get

STMicroelectronics Porter's Five Forces Analysis

This preview shows the exact STMicroelectronics Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, ready to download and use, and contains the complete strategic assessment you see here. Instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

STMicroelectronics faces intense competitive rivalry amid cyclical semiconductor demand, moderate supplier leverage for specialized nodes, elevated buyer power from large OEMs, limited threat of new entrants due to high capital intensity, and moderate substitute risks from alternative technologies. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for a complete, actionable breakdown.

Suppliers Bargaining Power

Concentrated equipment vendors

ST relies on a tiny set of critical toolmakers—ASML (greater than 90% share in EUV), Applied Materials and KLA—giving suppliers strong leverage; EUV/advanced DUV lead times commonly run 12–36 months and ASML backlog remains multi-year (2024), so any disruption or upgrade delay can bottleneck ramp plans and node transitions. Long service cycles and complex qualification make multi-sourcing largely impractical.

Scarce advanced materials

Silicon carbide wafers, specialty gases, photoresists and advanced substrates remain concentrated among fewer than 10 global suppliers, creating capacity constraints and supplier pricing power. SiC supply is especially tight with lead times commonly 6–12 months and industry reports spot wafer prices rising about 20% between 2022–24. Long-term take-or-pay contracts are widely used to secure volumes, and new-source qualification typically requires 12–24 months due to strict reliability demands.

EDA/IP tool dependence

Design flows rely on a few EDA/IP vendors—top three EDA suppliers hold over 70% market share—creating material switching costs and license exposure for STMicroelectronics. ARM IP underpins roughly 90% of smartphones, reinforcing architectural lock-in, while foundry PDK alignment with TSMC (over 50% global foundry share) tightens dependency. Price hikes, license limits or US export controls since 2022 can delay projects and restrict vendor choice.

Geopolitical and compliance risks

Geopolitical and compliance risks raise supplier leverage over STMicroelectronics as 2024 expansions of US and allied export controls and ongoing China trade tensions constrain tool and material availability, especially for advanced packaging and specialty chemicals. Region-specific approvals and certification requirements repeatedly delay shipments or force redesigns, while tight markets see suppliers prioritizing strategic regions. Compliance and carbon-related regulation costs are typically passed through to device makers like ST, squeezing margins.

- Export controls 2024: reduced access to advanced tooling in constrained markets

- Region approvals: cause shipment delays and redesigns

- Priority allocation: suppliers favor key regions in shortages

- Cost pass-through: compliance and environmental costs borne by device makers

Mitigation via partial vertical integration

ST’s partial vertical integration — six internal wafer fabs and in-house SiC device manufacturing — plus multi-year supply agreements in 2024 reduce some supplier leverage; co-development with key vendors aligns roadmaps and improves production priority. Upstream concentration in SiC substrates (few suppliers such as Wolfspeed and II‑VI) keeps supplier bargaining power moderately high, and diversification programs will take several years to materially shift leverage.

- Internal fabs: six sites (2024)

- SiC: in-house device production

- Long-term contracts: lower short-term risk

- Upstream concentration: supplier-centric

- Diversification: multi-year impact

Supplier concentration drives leverage: EUV > 90%, foundry ~50%

Suppliers hold high leverage: ASML >90% EUV share, EUV lead times 12–36 months (2024); top three EDA vendors >70% share; TSMC ~50% foundry share. SiC wafers tight with 6–12 month lead times and ~20% spot price rise 2022–24. ST’s six fabs and long-term contracts mitigate but upstream concentration leaves bargaining power moderately high.

| Supplier | Concentration | Lead time | 2022–24 change |

|---|---|---|---|

| ASML (EUV) | >90% | 12–36m | backlog multi‑year (2024) |

| EDA vendors | >70% (top3) | n/a | license cost up |

| SiC wafers | few suppliers | 6–12m | +≈20% price |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks tailored exclusively for STMicroelectronics, identifying disruptive forces, supplier and buyer power, substitutes, and barriers shaping its pricing, profitability and strategic positioning.

A clear, one-sheet Porter's Five Forces summary tailored to STMicroelectronics—perfect for quick strategic decisions and investor briefings; customize pressure levels as market or technology risks evolve.

Customers Bargaining Power

Large OEMs with scale

Large OEMs in automotive, industrial and consumer electronics buy at scale—the global semiconductor market reached about $600B in 2024 and the automotive segment was roughly $70B—giving these buyers strong price negotiation and strict SLA demands. Dual-sourcing by OEMs forces suppliers like STMicroelectronics into competitive pricing and capacity allocation. Consolidation among Tier-1s increases buyer leverage, and volume commitments often come with downward ASP pressure.

High switching costs in auto/industrial

Long qualification cycles (AEC-Q commonly 6–18 months) and safety certification tracks (ISO 26262/functional safety often 12–24 months) plus firmware/software dependencies lock designs to STMicro, making redesigns costly and revalidation often >$100,000 and time-consuming, which dampens buyer switching and weakens buyer power after a design-win; however OEMs still use upfront bidding to compress pricing before lock-in.

Design influence and customization

Buyers demand tailored reference designs, firmware and white‑glove support, raising service burden and push costs higher; in 2024 STMicroelectronics reported ~€16.4B revenue, making design wins critical to margins. Early customer engagement gives powerful leverage over roadmaps and pricing, and failure to hit performance‑per‑watt targets can forfeit sockets to competitors. Value‑added support helps recover pricing pressure but only partially offsets lost ASPs.

Transparency and benchmark pricing

Market visibility on node, die size and device benchmarks gives buyers leverage in negotiations; STMicroelectronics reported 2024 revenue of $15.8B, exposing commodity discretes to tight price comparisons while complex analog/MEMS and power modules retain better margin defensibility. LTAs indexed to metal/CPI or quarterly ASPs help balance volatility with buyer expectations.

- Transparency enables benchmark-driven price pressure

- Discretes behave like commodities; margins compress

- Analog/MEMS, power modules offer higher stickiness

- Indexed LTAs mitigate short-term volatility

Aftermarket and lifecycle demands

Long product lifecycles in automotive and industrial segments (often 10+ years) force ST to offer extended supply and last-time-buy flexibility, with buyers demanding longevity commitments and PPAP-level quality rigor that can compress margins. These aftermarket obligations increase inventory and testing costs, though STs reliable delivery performance can blunt buyer leverage by ensuring continuity for OEM production.

OEM scale and long qualifications lock buyers while tendering compresses ASPs

Large OEMs (auto, industrial, consumer) buy at scale—global sem market ~$600B (2024), automotive ~$70B—giving strong price/SLA leverage over ST (revenue €16.4B in 2024). Long qualification (AEC‑Q 6–18m, ISO26262 12–24m) and redesign costs >€100k reduce switching but OEM bidding compresses ASPs. Discretes face commodity pricing; analog/MEMS and power modules retain higher stickiness. LTAs/indexing mitigate volatility.

| Metric | Value (2024) |

|---|---|

| Global semiconductor market | $600B |

| Automotive segment | $70B |

| STMicroelectronics revenue | €16.4B |

| AEC‑Q qualification | 6–18 months |

| ISO 26262 | 12–24 months |

| Redesign/revalidation cost | >€100k |

| Product lifecycle | 10+ years |

What You See Is What You Get

STMicroelectronics Porter's Five Forces Analysis

This preview shows the exact STMicroelectronics Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The document is fully formatted, ready to download and use, and contains the complete strategic assessment you see here. Instant access upon payment.