STMicroelectronics SWOT Analysis

Your Strategic Toolkit Starts Here

STMicroelectronics' SWOT analysis highlights strengths like diversified product lines and manufacturing scale, balanced against risks from semiconductor cyclicality and fierce competition. Growth drivers include EVs, IoT, and industrial automation. Purchase the full SWOT for a professionally formatted Word and editable Excel report to plan, pitch, or invest with confidence.

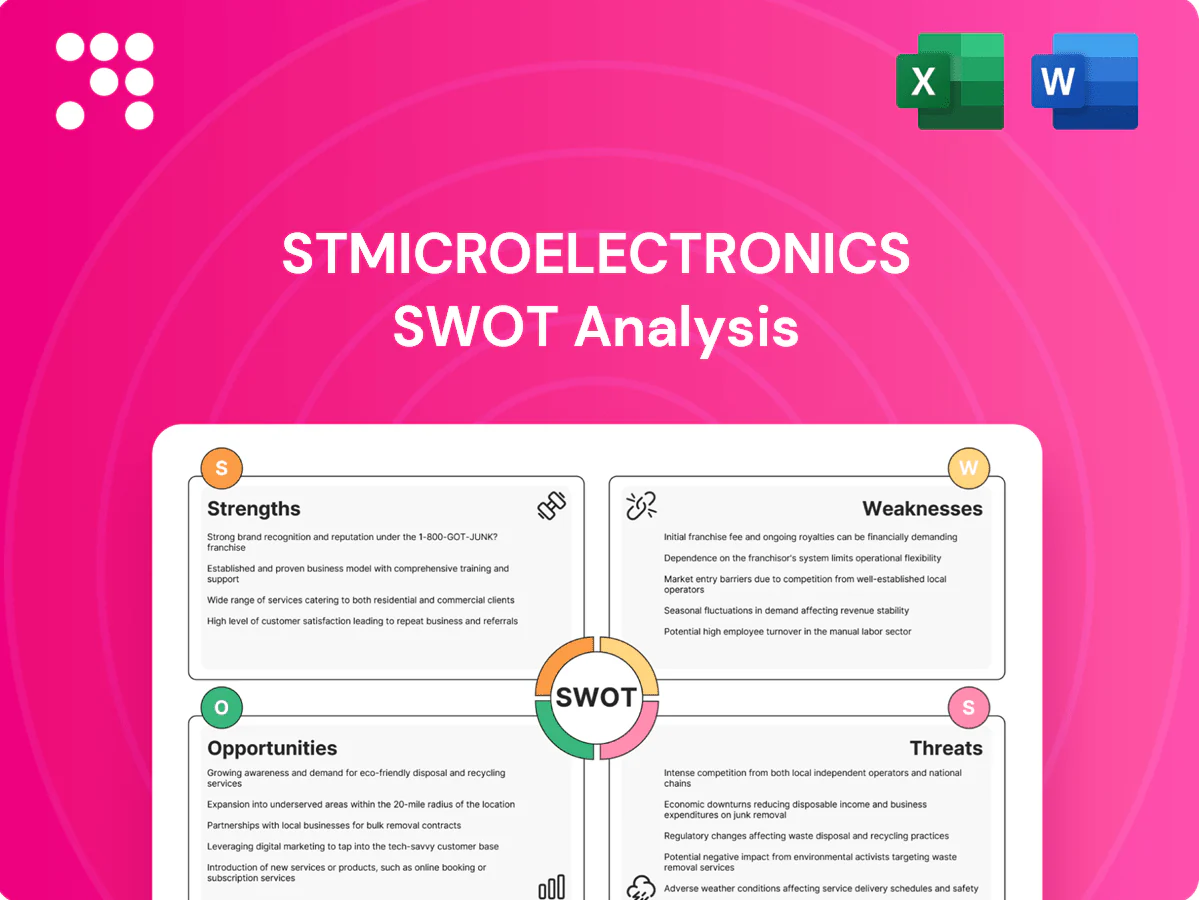

Strengths

Diversified end-market mix

Serving automotive, industrial, personal electronics and communications smooths revenue volatility across cycles, with automotive representing roughly one-quarter of sales. Broad application exposure enables cross-selling and platform reuse across MCUs, sensors and power devices. This diversification reduces dependency on any single customer or vertical and supports more balanced R&D allocation—about 9% of revenue directed to R&D.

Leadership in power, analog, and MCUs

STMicroelectronics' strong positions in power management, analog, and 32-bit MCUs underpin sticky, high-margin franchises, with STM32 ecosystem reported at over 2.5 million developers and power/analog leading automotive content growth in 2024.

These product lines are critical for efficiency and control in EVs, industrial automation, and IoT, contributing to ST's sizable automotive and industrial revenue mix (multi‑billion euros in 2024).

Long product lifecycles and high switching costs create resilience, with design wins translating into multi-year revenue streams and supporting a multi‑year automotive backlog reported in 2024.

Manufacturing depth in SiC, GaN, and 300mm

STMicroelectronics leverages vertical SiC and GaN device expertise with internal fabs in Catania (SiC) and Crolles (300mm analog), giving tighter quality and automotive-grade supply assurance. Ownership of 300mm capacity and in-house power wafer processing supports superior cost and performance control versus fabless peers. Scale advantages from integrated manufacturing underpin unit-economics competitiveness and differentiation in fast-growing electrification markets.

Strong automotive footprint and Tier-1 relationships

Established ties with OEMs and Tier-1s in powertrain, ADAS and body electronics drive growing content per vehicle; automotive represents roughly one-third of STMicroelectronics revenue. Automotive quality systems and AEC-Q certifications create high barriers and long 18–36 month qualification cycles that protect share once designed in. The EV transition, with rising silicon per vehicle, positions ST to capture incremental content.

- Deep OEM/Tier-1 integrations

- AEC-Q & automotive QS barriers

- 18–36 month qualification moat

- EV tailwinds for silicon content

Global footprint and resilient supply chain

STMicroelectronics' global R&D, manufacturing and logistics hubs across Europe, Asia and the Americas reduce single-point failures and sustained operations through 2023–24 supply shocks. Proximity to customers supports co-development and faster ramps for new products. Operating in 35+ countries with over 46,000 employees balances regional risk and helps maintain delivery during demand surges.

- Global footprint: 35+ countries

- Workforce: 46,000+ employees

- Benefit: faster ramps, reduced single-point failure risk

~25% auto, 9% R&D, > 2.5M MCU devs, in-house SiC/GaN

Diversified end-markets (automotive ~one-quarter of sales) and 9% R&D intensity support cross-selling across MCUs, sensors and power; STM32 ecosystem exceeds 2.5M developers. In-house SiC/GaN and 300mm fabs plus 46,000+ employees enable automotive-grade supply and multi-year design-win visibility.

| Metric | Value |

|---|---|

| R&D | ~9% rev |

| STM32 devs | >2.5M |

| Employees | 46,000+ |

What is included in the product

Delivers a strategic overview of STMicroelectronics’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, growth drivers, operational gaps, and future risks.

Provides a concise SWOT matrix for STMicroelectronics to quickly align strategy, highlight tech strengths and supply-chain risks, and speed stakeholder briefings and decision-making.

Weaknesses

Cyclical exposure and inventory swings

Semi demand is highly cyclical, causing STMicroelectronics' utilization and pricing to swing with end-market cycles, which has historically led to volatile quarterly margins.

Channel inventory corrections have previously pressured ST's revenue recognition and margins as distributors destock, reducing near-term sales visibility.

When macro conditions deteriorate visibility narrows and working capital needs rise due to longer receivable and inventory turns, squeezing cash flow and operational flexibility.

High capex and long payback

Expanding SiC, GaN and 300mm capacity requires sustained multi‑year investments running into several billions; SiC market was >$1.5B in 2023 and is forecast by analysts to exceed $6B by 2030. Returns hinge on EV and industrial adoption rates, so slower EV penetration delays payback. Underutilization of new fabs would compress gross margins and the high capital intensity limits ST’s pricing and capacity flexibility in weak cycles.

Digital leading-edge gap

Compared with top foundries—TSMC holding roughly 55–60% of the foundry market and volume-producing 3nm/2nm nodes—STMicro focuses less on bleeding-edge logic, limiting its ability to participate in certain high-performance compute segments. Reliance on external partners for advanced nodes adds cost and timing risks, and can weaken competitive perception in AI-centric bids where 5nm/3nm process availability is often required.

Customer and platform concentration risk

Customer and platform concentration exposes STMicroelectronics: large smartphone or automotive programs can dominate revenue, so losing a design win or facing insourcing by a key account would be material. Pricing pressure intensifies when a few customers drive volumes, and negotiating leverage can shift rapidly with market or product changes.

- High revenue dependency on major programs

- Material impact from single-customer design loss

- Pricing pressure when volumes concentrated

- Rapid shifts in customer negotiating leverage

Complex product qualification cycles

Complex product qualification cycles for STMicroelectronics, driven by stringent automotive and industrial certifications, extend time-to-revenue and tie up engineering resources in long validation periods; any quality excursion can be costly to remediate and slows pivoting to new opportunities.

- Long certification timelines

- Engineering capacity locked in validation

- High remediation costs for quality issues

- Reduced agility to seize new markets

Semi cyclicality and heavy SiC/300mm capex squeeze margins, cash flow, utilization

Semi cyclicality drives volatile margins and utilization swings. Channel destocking and narrow macro visibility raise working‑capital strain and compress cash flow. Heavy multi‑year SiC/300mm capex (~multi‑billion) risks underutilization while ST lags bleeding‑edge foundries (TSMC ~55–60% share), limiting AI/high‑perf logic exposure.

| Metric | Value |

|---|---|

| SiC market 2023 | >$1.5B |

| SiC forecast 2030 | >$6B |

| TSMC foundry share | ~55–60% |

Full Version Awaits

STMicroelectronics SWOT Analysis

This is the actual SWOT analysis you'll receive upon purchase—comprehensive, professional, and ready to use. The preview below is taken directly from the full report, so there are no surprises after checkout. Buy to unlock the complete, editable STMicroelectronics SWOT with strengths, weaknesses, opportunities and threats fully detailed.

Your Strategic Toolkit Starts Here

STMicroelectronics' SWOT analysis highlights strengths like diversified product lines and manufacturing scale, balanced against risks from semiconductor cyclicality and fierce competition. Growth drivers include EVs, IoT, and industrial automation. Purchase the full SWOT for a professionally formatted Word and editable Excel report to plan, pitch, or invest with confidence.

Strengths

Diversified end-market mix

Serving automotive, industrial, personal electronics and communications smooths revenue volatility across cycles, with automotive representing roughly one-quarter of sales. Broad application exposure enables cross-selling and platform reuse across MCUs, sensors and power devices. This diversification reduces dependency on any single customer or vertical and supports more balanced R&D allocation—about 9% of revenue directed to R&D.

Leadership in power, analog, and MCUs

STMicroelectronics' strong positions in power management, analog, and 32-bit MCUs underpin sticky, high-margin franchises, with STM32 ecosystem reported at over 2.5 million developers and power/analog leading automotive content growth in 2024.

These product lines are critical for efficiency and control in EVs, industrial automation, and IoT, contributing to ST's sizable automotive and industrial revenue mix (multi‑billion euros in 2024).

Long product lifecycles and high switching costs create resilience, with design wins translating into multi-year revenue streams and supporting a multi‑year automotive backlog reported in 2024.

Manufacturing depth in SiC, GaN, and 300mm

STMicroelectronics leverages vertical SiC and GaN device expertise with internal fabs in Catania (SiC) and Crolles (300mm analog), giving tighter quality and automotive-grade supply assurance. Ownership of 300mm capacity and in-house power wafer processing supports superior cost and performance control versus fabless peers. Scale advantages from integrated manufacturing underpin unit-economics competitiveness and differentiation in fast-growing electrification markets.

Strong automotive footprint and Tier-1 relationships

Established ties with OEMs and Tier-1s in powertrain, ADAS and body electronics drive growing content per vehicle; automotive represents roughly one-third of STMicroelectronics revenue. Automotive quality systems and AEC-Q certifications create high barriers and long 18–36 month qualification cycles that protect share once designed in. The EV transition, with rising silicon per vehicle, positions ST to capture incremental content.

- Deep OEM/Tier-1 integrations

- AEC-Q & automotive QS barriers

- 18–36 month qualification moat

- EV tailwinds for silicon content

Global footprint and resilient supply chain

STMicroelectronics' global R&D, manufacturing and logistics hubs across Europe, Asia and the Americas reduce single-point failures and sustained operations through 2023–24 supply shocks. Proximity to customers supports co-development and faster ramps for new products. Operating in 35+ countries with over 46,000 employees balances regional risk and helps maintain delivery during demand surges.

- Global footprint: 35+ countries

- Workforce: 46,000+ employees

- Benefit: faster ramps, reduced single-point failure risk

~25% auto, 9% R&D, > 2.5M MCU devs, in-house SiC/GaN

Diversified end-markets (automotive ~one-quarter of sales) and 9% R&D intensity support cross-selling across MCUs, sensors and power; STM32 ecosystem exceeds 2.5M developers. In-house SiC/GaN and 300mm fabs plus 46,000+ employees enable automotive-grade supply and multi-year design-win visibility.

| Metric | Value |

|---|---|

| R&D | ~9% rev |

| STM32 devs | >2.5M |

| Employees | 46,000+ |

What is included in the product

Delivers a strategic overview of STMicroelectronics’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, growth drivers, operational gaps, and future risks.

Provides a concise SWOT matrix for STMicroelectronics to quickly align strategy, highlight tech strengths and supply-chain risks, and speed stakeholder briefings and decision-making.

Weaknesses

Cyclical exposure and inventory swings

Semi demand is highly cyclical, causing STMicroelectronics' utilization and pricing to swing with end-market cycles, which has historically led to volatile quarterly margins.

Channel inventory corrections have previously pressured ST's revenue recognition and margins as distributors destock, reducing near-term sales visibility.

When macro conditions deteriorate visibility narrows and working capital needs rise due to longer receivable and inventory turns, squeezing cash flow and operational flexibility.

High capex and long payback

Expanding SiC, GaN and 300mm capacity requires sustained multi‑year investments running into several billions; SiC market was >$1.5B in 2023 and is forecast by analysts to exceed $6B by 2030. Returns hinge on EV and industrial adoption rates, so slower EV penetration delays payback. Underutilization of new fabs would compress gross margins and the high capital intensity limits ST’s pricing and capacity flexibility in weak cycles.

Digital leading-edge gap

Compared with top foundries—TSMC holding roughly 55–60% of the foundry market and volume-producing 3nm/2nm nodes—STMicro focuses less on bleeding-edge logic, limiting its ability to participate in certain high-performance compute segments. Reliance on external partners for advanced nodes adds cost and timing risks, and can weaken competitive perception in AI-centric bids where 5nm/3nm process availability is often required.

Customer and platform concentration risk

Customer and platform concentration exposes STMicroelectronics: large smartphone or automotive programs can dominate revenue, so losing a design win or facing insourcing by a key account would be material. Pricing pressure intensifies when a few customers drive volumes, and negotiating leverage can shift rapidly with market or product changes.

- High revenue dependency on major programs

- Material impact from single-customer design loss

- Pricing pressure when volumes concentrated

- Rapid shifts in customer negotiating leverage

Complex product qualification cycles

Complex product qualification cycles for STMicroelectronics, driven by stringent automotive and industrial certifications, extend time-to-revenue and tie up engineering resources in long validation periods; any quality excursion can be costly to remediate and slows pivoting to new opportunities.

- Long certification timelines

- Engineering capacity locked in validation

- High remediation costs for quality issues

- Reduced agility to seize new markets

Semi cyclicality and heavy SiC/300mm capex squeeze margins, cash flow, utilization

Semi cyclicality drives volatile margins and utilization swings. Channel destocking and narrow macro visibility raise working‑capital strain and compress cash flow. Heavy multi‑year SiC/300mm capex (~multi‑billion) risks underutilization while ST lags bleeding‑edge foundries (TSMC ~55–60% share), limiting AI/high‑perf logic exposure.

| Metric | Value |

|---|---|

| SiC market 2023 | >$1.5B |

| SiC forecast 2030 | >$6B |

| TSMC foundry share | ~55–60% |

Full Version Awaits

STMicroelectronics SWOT Analysis

This is the actual SWOT analysis you'll receive upon purchase—comprehensive, professional, and ready to use. The preview below is taken directly from the full report, so there are no surprises after checkout. Buy to unlock the complete, editable STMicroelectronics SWOT with strengths, weaknesses, opportunities and threats fully detailed.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

STMicroelectronics' SWOT analysis highlights strengths like diversified product lines and manufacturing scale, balanced against risks from semiconductor cyclicality and fierce competition. Growth drivers include EVs, IoT, and industrial automation. Purchase the full SWOT for a professionally formatted Word and editable Excel report to plan, pitch, or invest with confidence.

Strengths

Diversified end-market mix

Serving automotive, industrial, personal electronics and communications smooths revenue volatility across cycles, with automotive representing roughly one-quarter of sales. Broad application exposure enables cross-selling and platform reuse across MCUs, sensors and power devices. This diversification reduces dependency on any single customer or vertical and supports more balanced R&D allocation—about 9% of revenue directed to R&D.

Leadership in power, analog, and MCUs

STMicroelectronics' strong positions in power management, analog, and 32-bit MCUs underpin sticky, high-margin franchises, with STM32 ecosystem reported at over 2.5 million developers and power/analog leading automotive content growth in 2024.

These product lines are critical for efficiency and control in EVs, industrial automation, and IoT, contributing to ST's sizable automotive and industrial revenue mix (multi‑billion euros in 2024).

Long product lifecycles and high switching costs create resilience, with design wins translating into multi-year revenue streams and supporting a multi‑year automotive backlog reported in 2024.

Manufacturing depth in SiC, GaN, and 300mm

STMicroelectronics leverages vertical SiC and GaN device expertise with internal fabs in Catania (SiC) and Crolles (300mm analog), giving tighter quality and automotive-grade supply assurance. Ownership of 300mm capacity and in-house power wafer processing supports superior cost and performance control versus fabless peers. Scale advantages from integrated manufacturing underpin unit-economics competitiveness and differentiation in fast-growing electrification markets.

Strong automotive footprint and Tier-1 relationships

Established ties with OEMs and Tier-1s in powertrain, ADAS and body electronics drive growing content per vehicle; automotive represents roughly one-third of STMicroelectronics revenue. Automotive quality systems and AEC-Q certifications create high barriers and long 18–36 month qualification cycles that protect share once designed in. The EV transition, with rising silicon per vehicle, positions ST to capture incremental content.

- Deep OEM/Tier-1 integrations

- AEC-Q & automotive QS barriers

- 18–36 month qualification moat

- EV tailwinds for silicon content

Global footprint and resilient supply chain

STMicroelectronics' global R&D, manufacturing and logistics hubs across Europe, Asia and the Americas reduce single-point failures and sustained operations through 2023–24 supply shocks. Proximity to customers supports co-development and faster ramps for new products. Operating in 35+ countries with over 46,000 employees balances regional risk and helps maintain delivery during demand surges.

- Global footprint: 35+ countries

- Workforce: 46,000+ employees

- Benefit: faster ramps, reduced single-point failure risk

~25% auto, 9% R&D, > 2.5M MCU devs, in-house SiC/GaN

Diversified end-markets (automotive ~one-quarter of sales) and 9% R&D intensity support cross-selling across MCUs, sensors and power; STM32 ecosystem exceeds 2.5M developers. In-house SiC/GaN and 300mm fabs plus 46,000+ employees enable automotive-grade supply and multi-year design-win visibility.

| Metric | Value |

|---|---|

| R&D | ~9% rev |

| STM32 devs | >2.5M |

| Employees | 46,000+ |

What is included in the product

Delivers a strategic overview of STMicroelectronics’s internal and external business factors, outlining strengths, weaknesses, opportunities and threats to assess its competitive position, growth drivers, operational gaps, and future risks.

Provides a concise SWOT matrix for STMicroelectronics to quickly align strategy, highlight tech strengths and supply-chain risks, and speed stakeholder briefings and decision-making.

Weaknesses

Cyclical exposure and inventory swings

Semi demand is highly cyclical, causing STMicroelectronics' utilization and pricing to swing with end-market cycles, which has historically led to volatile quarterly margins.

Channel inventory corrections have previously pressured ST's revenue recognition and margins as distributors destock, reducing near-term sales visibility.

When macro conditions deteriorate visibility narrows and working capital needs rise due to longer receivable and inventory turns, squeezing cash flow and operational flexibility.

High capex and long payback

Expanding SiC, GaN and 300mm capacity requires sustained multi‑year investments running into several billions; SiC market was >$1.5B in 2023 and is forecast by analysts to exceed $6B by 2030. Returns hinge on EV and industrial adoption rates, so slower EV penetration delays payback. Underutilization of new fabs would compress gross margins and the high capital intensity limits ST’s pricing and capacity flexibility in weak cycles.

Digital leading-edge gap

Compared with top foundries—TSMC holding roughly 55–60% of the foundry market and volume-producing 3nm/2nm nodes—STMicro focuses less on bleeding-edge logic, limiting its ability to participate in certain high-performance compute segments. Reliance on external partners for advanced nodes adds cost and timing risks, and can weaken competitive perception in AI-centric bids where 5nm/3nm process availability is often required.

Customer and platform concentration risk

Customer and platform concentration exposes STMicroelectronics: large smartphone or automotive programs can dominate revenue, so losing a design win or facing insourcing by a key account would be material. Pricing pressure intensifies when a few customers drive volumes, and negotiating leverage can shift rapidly with market or product changes.

- High revenue dependency on major programs

- Material impact from single-customer design loss

- Pricing pressure when volumes concentrated

- Rapid shifts in customer negotiating leverage

Complex product qualification cycles

Complex product qualification cycles for STMicroelectronics, driven by stringent automotive and industrial certifications, extend time-to-revenue and tie up engineering resources in long validation periods; any quality excursion can be costly to remediate and slows pivoting to new opportunities.

- Long certification timelines

- Engineering capacity locked in validation

- High remediation costs for quality issues

- Reduced agility to seize new markets

Semi cyclicality and heavy SiC/300mm capex squeeze margins, cash flow, utilization

Semi cyclicality drives volatile margins and utilization swings. Channel destocking and narrow macro visibility raise working‑capital strain and compress cash flow. Heavy multi‑year SiC/300mm capex (~multi‑billion) risks underutilization while ST lags bleeding‑edge foundries (TSMC ~55–60% share), limiting AI/high‑perf logic exposure.

| Metric | Value |

|---|---|

| SiC market 2023 | >$1.5B |

| SiC forecast 2030 | >$6B |

| TSMC foundry share | ~55–60% |

Full Version Awaits

STMicroelectronics SWOT Analysis

This is the actual SWOT analysis you'll receive upon purchase—comprehensive, professional, and ready to use. The preview below is taken directly from the full report, so there are no surprises after checkout. Buy to unlock the complete, editable STMicroelectronics SWOT with strengths, weaknesses, opportunities and threats fully detailed.