STAAR Surgical Porter's Five Forces Analysis

From Overview to Strategy Blueprint

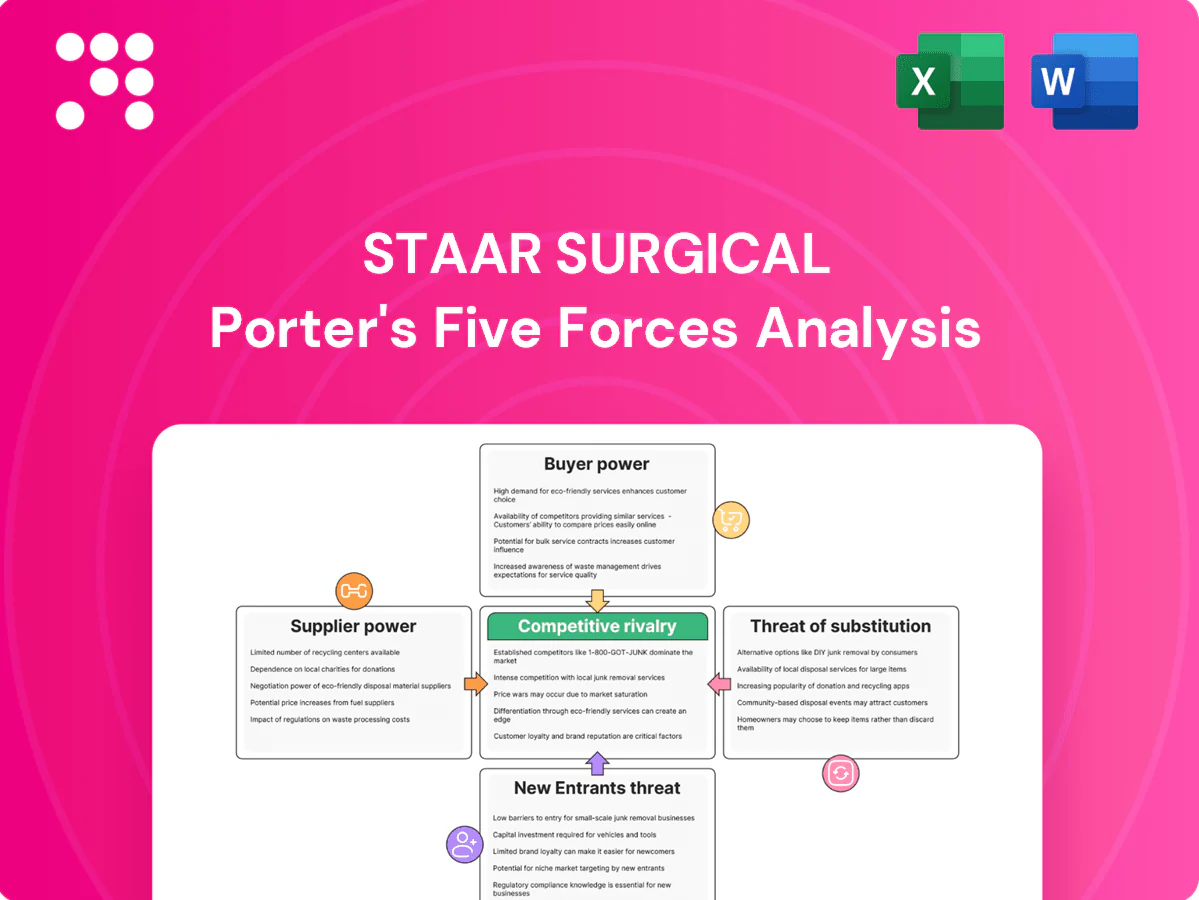

STAAR Surgical faces moderate supplier power from specialized component providers and strong buyer expectations driven by reimbursement and clinical outcomes, while regulatory hurdles and IP create significant barriers to new entrants. Competitive rivalry and substitute technologies pressure pricing and innovation-led differentiation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore STAAR Surgical’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Specialized biomaterials concentration

STAAR depends on proprietary collamer and optical‑grade polymers from very few qualified suppliers, concentrating supplier power. Limited options (often under five) raise bargaining leverage and switching costs as revalidation commonly takes 6–12 months. Disruptions can depress yields and lengthen lead times by 3–6 months. Long‑term contracts and selective dual‑sourcing mitigate but do not eliminate the risk.

Precision equipment and sterilization

Ultra-precision lathing, polishing and sterilization suppliers are highly specialized and regulated, subject to FDA quality system regulations (21 CFR 820) and ISO 11137 validation requirements, making qualification and process validation slow and costly. This raises switching barriers and lets vendors pass through compliance- and capacity-driven price increases. STAAR’s scale and production planning, however, enable negotiation for priority slots and volume discounts.

Regulatory and quality dependencies

Class III implantables require PMA-level validated materials and documented change control under FDA 21 CFR 814 and quality system regs 21 CFR 820, giving suppliers leverage since any component change can trigger PMA supplements with FDA review timelines often around 180 days. Suppliers with clean compliance histories command price premiums, while STAAR mitigates risk through strict QA, supplier audits, and joint technical development.

Volume leverage is moderate

STAAR reported 2024 revenue of $262.4M; volumes remain smaller than large cataract IOL peers, limiting scale leverage. Suppliers may favor larger medtech customers during component shortages. Multi‑year volume commitments and rising demand in Asia should incrementally strengthen STAAR’s bargaining position.

- Smaller scale vs top peers — limits discounting

- Supply shortages: higher-priority customers first

- Multi-year contracts unlock better pricing

- Asia growth could improve leverage over time

Geographic and logistics risks

- Resin shortages: supply tightness in 2024

- Shipping volatility: peak surcharges ~40%

- Cold chain adds 10–20% cost

- Mitigation: inventory buffers, regional redundancy

Supplier concentration, 6-12m revalidation; $262.4M, peak surcharges ~40%

STAAR relies on <5 qualified polymer and ultra‑precision suppliers, raising switching costs (revalidation 6–12 months) and enabling price pass‑through; PMA change controls add ~180‑day FDA review risk. 2024 revenue $262.4M limits scale leverage vs peers; suppliers favored larger customers during 2024 shortages. Peak surcharges hit ~40%; cold‑chain adds 10–20%.

| Metric | Value (2024) |

|---|---|

| Revenue | $262.4M |

| Qualified suppliers | <5 |

| Revalidation | 6–12 months |

| FDA review | ~180 days |

| Peak surcharges | ~40% |

| Cold‑chain cost | 10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for STAAR Surgical revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces shaping pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces for STAAR Surgical that turns complex competitive pressures into instant, slide-ready insights—customize force levels, swap in your own data, and export spider charts without macros for fast boardroom decisions.

Customers Bargaining Power

Surgeons and ASCs as key buyers

Ophthalmic surgeons and ambulatory surgery centers (ASCs) are the primary adopters of ICLs and thus hold strong purchasing influence over STAAR Surgical’s EVO/Visian ICL offerings.

Their clinical expertise and case volumes confer negotiation leverage on pricing, training support, and inventory terms, while demonstrated outcomes and ease of use blunt price sensitivity.

KOL advocacy, supported by over 1 million ICLs implanted globally, can shift surgeon preference toward STAAR’s products.

Distributor and hospital procurement

In many markets distributors and hospital groups aggregate demand via group purchasing organizations and tenders, creating significant price pressure and longer payment cycles—often extending to around 90 days. Bundling and tender strategies can compress margins, sometimes causing double-digit price concessions, so STAAR must offer competitive contracts and strong service levels. Exclusive distributor agreements can concentrate purchasing but also stabilize volumes and forecasting.

Patient pay and reimbursement dynamics

Most refractive ICLs are cash‑pay, with typical 2024 market prices around $4,000–$6,000 per eye versus LASIK/S MILE $2,000–$3,000, making patients more price sensitive. Perceived value—improved night vision, reversibility, range to treat high myopia—supports premium pricing. Widespread financing and DTC education lower sticker shock and raise conversion. Where reimbursed (limited indications), payer formularies and rules can effectively cap net prices.

Switching costs and training

Once surgeons are trained and inventories are organized, switching costs rise as customized sizing and integrated preoperative workflows embed STAAR devices into daily practice, progressively reducing buyer power. Over time this clinical and logistical entrenchment creates stickiness, though targeted competitor training programs and financial incentives can still prompt conversions. The net effect is weakening customer bargaining power, tempered by active rival outreach.

- Training-driven lock-in

- Customized sizing embeds supplier

- Preop workflow integration reduces churn

- Competitor incentives can erode loyalty

Outcome data and brand reputation

Clinical outcomes, safety profile and regulatory approvals (EVO ICL FDA approval 2022) drive buyer trust and reduce price sensitivity. Robust post‑market evidence shifts negotiations toward value rather than cost. Adverse events or recalls would rapidly raise customer bargaining power, while continuous evidence generation sustains STAAR’s pricing power.

- FDA approval 2022

- Post‑market data = value leverage

- Adverse events → higher buyer power

- Ongoing evidence sustains pricing

Surgeons' leverage and >1M ICLs reshape pricing, payments and value

Surgeons and ASCs hold strong bargaining power due to clinical influence, volume purchasing and ability to demand training, pricing and inventory terms.

Distributor tenders and GPOs compress prices and extend payment cycles (≈90 days), while patient cash-pay pricing ($4,000–$6,000/eye in 2024) raises end‑user sensitivity.

Clinical outcomes, >1M ICLs implanted and FDA approval (EVO 2022) shift negotiations toward value, creating gradual lock‑in through training and workflow integration.

| Metric | 2024 Value |

|---|---|

| Global ICLs implanted | >1,000,000 |

| Price per eye (typical) | $4,000–$6,000 |

| Typical payment cycle | ≈90 days |

What You See Is What You Get

STAAR Surgical Porter's Five Forces Analysis

This STAAR Surgical Porter's Five Forces analysis preview is the exact document you'll receive upon purchase—fully written, formatted and ready for immediate download. No placeholders or samples; the content shown is the final deliverable. Use it as-is for research, presentations or strategic decisions.

From Overview to Strategy Blueprint

STAAR Surgical faces moderate supplier power from specialized component providers and strong buyer expectations driven by reimbursement and clinical outcomes, while regulatory hurdles and IP create significant barriers to new entrants. Competitive rivalry and substitute technologies pressure pricing and innovation-led differentiation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore STAAR Surgical’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Specialized biomaterials concentration

STAAR depends on proprietary collamer and optical‑grade polymers from very few qualified suppliers, concentrating supplier power. Limited options (often under five) raise bargaining leverage and switching costs as revalidation commonly takes 6–12 months. Disruptions can depress yields and lengthen lead times by 3–6 months. Long‑term contracts and selective dual‑sourcing mitigate but do not eliminate the risk.

Precision equipment and sterilization

Ultra-precision lathing, polishing and sterilization suppliers are highly specialized and regulated, subject to FDA quality system regulations (21 CFR 820) and ISO 11137 validation requirements, making qualification and process validation slow and costly. This raises switching barriers and lets vendors pass through compliance- and capacity-driven price increases. STAAR’s scale and production planning, however, enable negotiation for priority slots and volume discounts.

Regulatory and quality dependencies

Class III implantables require PMA-level validated materials and documented change control under FDA 21 CFR 814 and quality system regs 21 CFR 820, giving suppliers leverage since any component change can trigger PMA supplements with FDA review timelines often around 180 days. Suppliers with clean compliance histories command price premiums, while STAAR mitigates risk through strict QA, supplier audits, and joint technical development.

Volume leverage is moderate

STAAR reported 2024 revenue of $262.4M; volumes remain smaller than large cataract IOL peers, limiting scale leverage. Suppliers may favor larger medtech customers during component shortages. Multi‑year volume commitments and rising demand in Asia should incrementally strengthen STAAR’s bargaining position.

- Smaller scale vs top peers — limits discounting

- Supply shortages: higher-priority customers first

- Multi-year contracts unlock better pricing

- Asia growth could improve leverage over time

Geographic and logistics risks

- Resin shortages: supply tightness in 2024

- Shipping volatility: peak surcharges ~40%

- Cold chain adds 10–20% cost

- Mitigation: inventory buffers, regional redundancy

Supplier concentration, 6-12m revalidation; $262.4M, peak surcharges ~40%

STAAR relies on <5 qualified polymer and ultra‑precision suppliers, raising switching costs (revalidation 6–12 months) and enabling price pass‑through; PMA change controls add ~180‑day FDA review risk. 2024 revenue $262.4M limits scale leverage vs peers; suppliers favored larger customers during 2024 shortages. Peak surcharges hit ~40%; cold‑chain adds 10–20%.

| Metric | Value (2024) |

|---|---|

| Revenue | $262.4M |

| Qualified suppliers | <5 |

| Revalidation | 6–12 months |

| FDA review | ~180 days |

| Peak surcharges | ~40% |

| Cold‑chain cost | 10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for STAAR Surgical revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces shaping pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces for STAAR Surgical that turns complex competitive pressures into instant, slide-ready insights—customize force levels, swap in your own data, and export spider charts without macros for fast boardroom decisions.

Customers Bargaining Power

Surgeons and ASCs as key buyers

Ophthalmic surgeons and ambulatory surgery centers (ASCs) are the primary adopters of ICLs and thus hold strong purchasing influence over STAAR Surgical’s EVO/Visian ICL offerings.

Their clinical expertise and case volumes confer negotiation leverage on pricing, training support, and inventory terms, while demonstrated outcomes and ease of use blunt price sensitivity.

KOL advocacy, supported by over 1 million ICLs implanted globally, can shift surgeon preference toward STAAR’s products.

Distributor and hospital procurement

In many markets distributors and hospital groups aggregate demand via group purchasing organizations and tenders, creating significant price pressure and longer payment cycles—often extending to around 90 days. Bundling and tender strategies can compress margins, sometimes causing double-digit price concessions, so STAAR must offer competitive contracts and strong service levels. Exclusive distributor agreements can concentrate purchasing but also stabilize volumes and forecasting.

Patient pay and reimbursement dynamics

Most refractive ICLs are cash‑pay, with typical 2024 market prices around $4,000–$6,000 per eye versus LASIK/S MILE $2,000–$3,000, making patients more price sensitive. Perceived value—improved night vision, reversibility, range to treat high myopia—supports premium pricing. Widespread financing and DTC education lower sticker shock and raise conversion. Where reimbursed (limited indications), payer formularies and rules can effectively cap net prices.

Switching costs and training

Once surgeons are trained and inventories are organized, switching costs rise as customized sizing and integrated preoperative workflows embed STAAR devices into daily practice, progressively reducing buyer power. Over time this clinical and logistical entrenchment creates stickiness, though targeted competitor training programs and financial incentives can still prompt conversions. The net effect is weakening customer bargaining power, tempered by active rival outreach.

- Training-driven lock-in

- Customized sizing embeds supplier

- Preop workflow integration reduces churn

- Competitor incentives can erode loyalty

Outcome data and brand reputation

Clinical outcomes, safety profile and regulatory approvals (EVO ICL FDA approval 2022) drive buyer trust and reduce price sensitivity. Robust post‑market evidence shifts negotiations toward value rather than cost. Adverse events or recalls would rapidly raise customer bargaining power, while continuous evidence generation sustains STAAR’s pricing power.

- FDA approval 2022

- Post‑market data = value leverage

- Adverse events → higher buyer power

- Ongoing evidence sustains pricing

Surgeons' leverage and >1M ICLs reshape pricing, payments and value

Surgeons and ASCs hold strong bargaining power due to clinical influence, volume purchasing and ability to demand training, pricing and inventory terms.

Distributor tenders and GPOs compress prices and extend payment cycles (≈90 days), while patient cash-pay pricing ($4,000–$6,000/eye in 2024) raises end‑user sensitivity.

Clinical outcomes, >1M ICLs implanted and FDA approval (EVO 2022) shift negotiations toward value, creating gradual lock‑in through training and workflow integration.

| Metric | 2024 Value |

|---|---|

| Global ICLs implanted | >1,000,000 |

| Price per eye (typical) | $4,000–$6,000 |

| Typical payment cycle | ≈90 days |

What You See Is What You Get

STAAR Surgical Porter's Five Forces Analysis

This STAAR Surgical Porter's Five Forces analysis preview is the exact document you'll receive upon purchase—fully written, formatted and ready for immediate download. No placeholders or samples; the content shown is the final deliverable. Use it as-is for research, presentations or strategic decisions.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

STAAR Surgical faces moderate supplier power from specialized component providers and strong buyer expectations driven by reimbursement and clinical outcomes, while regulatory hurdles and IP create significant barriers to new entrants. Competitive rivalry and substitute technologies pressure pricing and innovation-led differentiation. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore STAAR Surgical’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Specialized biomaterials concentration

STAAR depends on proprietary collamer and optical‑grade polymers from very few qualified suppliers, concentrating supplier power. Limited options (often under five) raise bargaining leverage and switching costs as revalidation commonly takes 6–12 months. Disruptions can depress yields and lengthen lead times by 3–6 months. Long‑term contracts and selective dual‑sourcing mitigate but do not eliminate the risk.

Precision equipment and sterilization

Ultra-precision lathing, polishing and sterilization suppliers are highly specialized and regulated, subject to FDA quality system regulations (21 CFR 820) and ISO 11137 validation requirements, making qualification and process validation slow and costly. This raises switching barriers and lets vendors pass through compliance- and capacity-driven price increases. STAAR’s scale and production planning, however, enable negotiation for priority slots and volume discounts.

Regulatory and quality dependencies

Class III implantables require PMA-level validated materials and documented change control under FDA 21 CFR 814 and quality system regs 21 CFR 820, giving suppliers leverage since any component change can trigger PMA supplements with FDA review timelines often around 180 days. Suppliers with clean compliance histories command price premiums, while STAAR mitigates risk through strict QA, supplier audits, and joint technical development.

Volume leverage is moderate

STAAR reported 2024 revenue of $262.4M; volumes remain smaller than large cataract IOL peers, limiting scale leverage. Suppliers may favor larger medtech customers during component shortages. Multi‑year volume commitments and rising demand in Asia should incrementally strengthen STAAR’s bargaining position.

- Smaller scale vs top peers — limits discounting

- Supply shortages: higher-priority customers first

- Multi-year contracts unlock better pricing

- Asia growth could improve leverage over time

Geographic and logistics risks

- Resin shortages: supply tightness in 2024

- Shipping volatility: peak surcharges ~40%

- Cold chain adds 10–20% cost

- Mitigation: inventory buffers, regional redundancy

Supplier concentration, 6-12m revalidation; $262.4M, peak surcharges ~40%

STAAR relies on <5 qualified polymer and ultra‑precision suppliers, raising switching costs (revalidation 6–12 months) and enabling price pass‑through; PMA change controls add ~180‑day FDA review risk. 2024 revenue $262.4M limits scale leverage vs peers; suppliers favored larger customers during 2024 shortages. Peak surcharges hit ~40%; cold‑chain adds 10–20%.

| Metric | Value (2024) |

|---|---|

| Revenue | $262.4M |

| Qualified suppliers | <5 |

| Revalidation | 6–12 months |

| FDA review | ~180 days |

| Peak surcharges | ~40% |

| Cold‑chain cost | 10–20% |

What is included in the product

Tailored Porter's Five Forces analysis for STAAR Surgical revealing competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces shaping pricing, margins, and strategic positioning.

A concise, one-sheet Porter's Five Forces for STAAR Surgical that turns complex competitive pressures into instant, slide-ready insights—customize force levels, swap in your own data, and export spider charts without macros for fast boardroom decisions.

Customers Bargaining Power

Surgeons and ASCs as key buyers

Ophthalmic surgeons and ambulatory surgery centers (ASCs) are the primary adopters of ICLs and thus hold strong purchasing influence over STAAR Surgical’s EVO/Visian ICL offerings.

Their clinical expertise and case volumes confer negotiation leverage on pricing, training support, and inventory terms, while demonstrated outcomes and ease of use blunt price sensitivity.

KOL advocacy, supported by over 1 million ICLs implanted globally, can shift surgeon preference toward STAAR’s products.

Distributor and hospital procurement

In many markets distributors and hospital groups aggregate demand via group purchasing organizations and tenders, creating significant price pressure and longer payment cycles—often extending to around 90 days. Bundling and tender strategies can compress margins, sometimes causing double-digit price concessions, so STAAR must offer competitive contracts and strong service levels. Exclusive distributor agreements can concentrate purchasing but also stabilize volumes and forecasting.

Patient pay and reimbursement dynamics

Most refractive ICLs are cash‑pay, with typical 2024 market prices around $4,000–$6,000 per eye versus LASIK/S MILE $2,000–$3,000, making patients more price sensitive. Perceived value—improved night vision, reversibility, range to treat high myopia—supports premium pricing. Widespread financing and DTC education lower sticker shock and raise conversion. Where reimbursed (limited indications), payer formularies and rules can effectively cap net prices.

Switching costs and training

Once surgeons are trained and inventories are organized, switching costs rise as customized sizing and integrated preoperative workflows embed STAAR devices into daily practice, progressively reducing buyer power. Over time this clinical and logistical entrenchment creates stickiness, though targeted competitor training programs and financial incentives can still prompt conversions. The net effect is weakening customer bargaining power, tempered by active rival outreach.

- Training-driven lock-in

- Customized sizing embeds supplier

- Preop workflow integration reduces churn

- Competitor incentives can erode loyalty

Outcome data and brand reputation

Clinical outcomes, safety profile and regulatory approvals (EVO ICL FDA approval 2022) drive buyer trust and reduce price sensitivity. Robust post‑market evidence shifts negotiations toward value rather than cost. Adverse events or recalls would rapidly raise customer bargaining power, while continuous evidence generation sustains STAAR’s pricing power.

- FDA approval 2022

- Post‑market data = value leverage

- Adverse events → higher buyer power

- Ongoing evidence sustains pricing

Surgeons' leverage and >1M ICLs reshape pricing, payments and value

Surgeons and ASCs hold strong bargaining power due to clinical influence, volume purchasing and ability to demand training, pricing and inventory terms.

Distributor tenders and GPOs compress prices and extend payment cycles (≈90 days), while patient cash-pay pricing ($4,000–$6,000/eye in 2024) raises end‑user sensitivity.

Clinical outcomes, >1M ICLs implanted and FDA approval (EVO 2022) shift negotiations toward value, creating gradual lock‑in through training and workflow integration.

| Metric | 2024 Value |

|---|---|

| Global ICLs implanted | >1,000,000 |

| Price per eye (typical) | $4,000–$6,000 |

| Typical payment cycle | ≈90 days |

What You See Is What You Get

STAAR Surgical Porter's Five Forces Analysis

This STAAR Surgical Porter's Five Forces analysis preview is the exact document you'll receive upon purchase—fully written, formatted and ready for immediate download. No placeholders or samples; the content shown is the final deliverable. Use it as-is for research, presentations or strategic decisions.