Standex Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

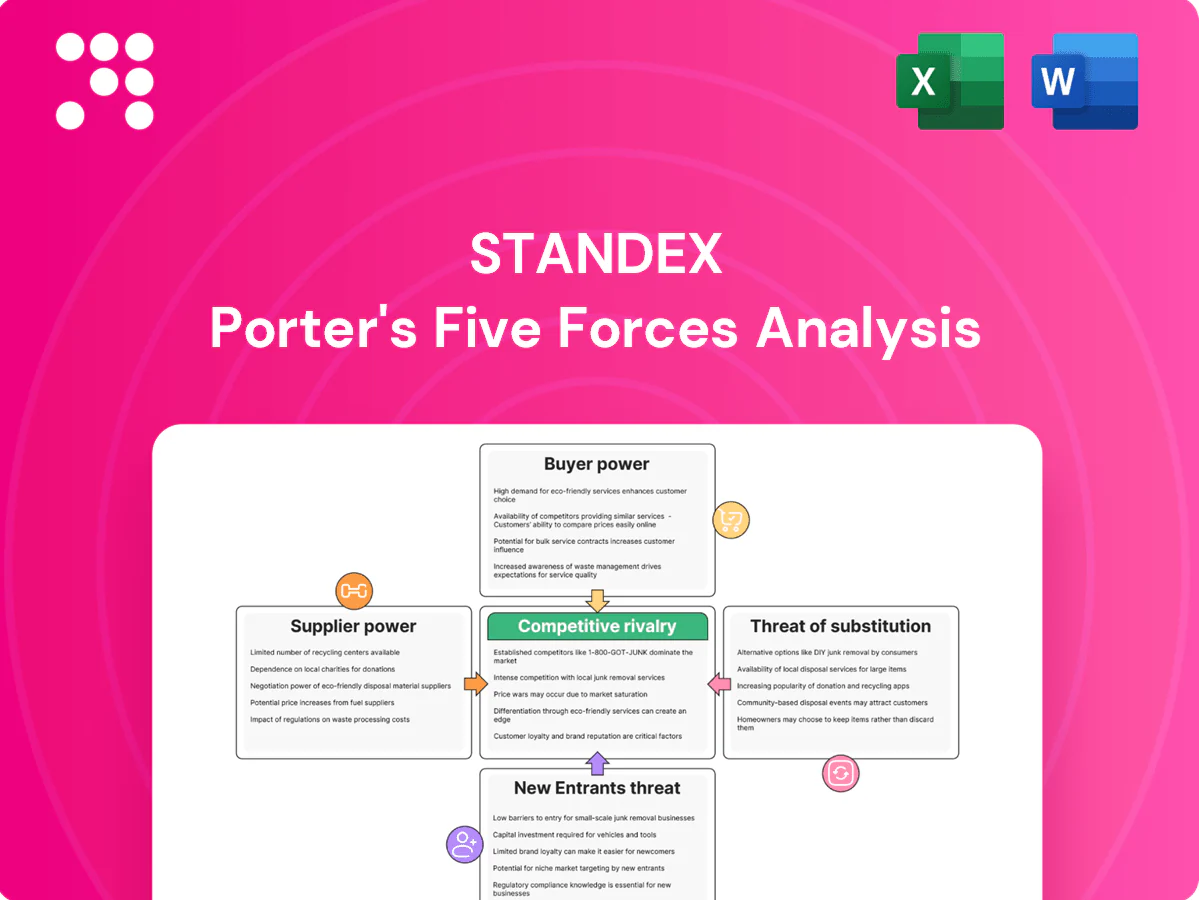

Standex faces moderate supplier power, niche customer segments, specialized substitutes, measured threat of new entrants, and intense industry rivalry shaping margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Standex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials dependence

Standex depends on specialty alloys, engineered polymers, rare-earth magnets and electronics that often have few qualified sources, with China supplying over 60% of refined rare earths (USGS 2024), raising supplier leverage during shortages. Long-term contracts and dual-sourcing partially offset exposure. Proactive inventory management is critical amid volatile commodity cycles.

Switching and qualification costs

Changing a materials or component supplier often requires requalification, testing and customer approvals, processes that typically take 3–12 months and can incur $50k–$250k in direct costs, elevating supplier power. Multi-year production programs (commonly 3–7 years) make midstream changes difficult and costly. Active supplier performance management and dual-sourcing reduce dependence and mitigate disruption risk.

Tooling and process know-how

Engraving and engineered components rely heavily on supplier tooling, surface treatments, and proprietary processes. Suppliers with unique capabilities can command better terms and pressure margins; Standex reported $1.44 billion in net sales in FY2024, so supplier costs are material. Knowledge lock-in raises switching barriers, while joint development and strategic sourcing can rebalance supplier influence and lower cost volatility.

Global supply chain constraints

Electronics and aerospace inputs for Standex face heightened geopolitical, logistics and compliance risk as 2024 saw expanded US export controls on advanced semiconductors and persistent EU REACH/RoHS constraints that limit substitute sources; short-term disruptions have amplified supplier bargaining power and pushed spot premiums higher, while regionalization and 3–6 months of safety stock remain primary mitigants.

- Export controls: tighter 2023–2024 limits on advanced chips

- Compliance: REACH/RoHS restricts alternatives

- Mitigation: regional sourcing, safety stock (3–6 months)

Scale versus niche volumes

Niche products produce lower aggregate volumes per SKU, reducing buyer leverage with large suppliers and raising per-unit costs; Standex’s FY2024 portfolio mix increased specialty SKU share, accentuating this pressure. Aggregating volumes across segments and platforms can recover scale benefits and improve procurement leverage. Vendor scorecards, should-cost analyses and joint cost-down programs align incentives and strengthen negotiations.

- Scale loss from niche SKUs — FY2024 portfolio shift

- Volume aggregation restores bargaining power

- Vendor scorecards + should-cost = better terms

- Collaborative cost-downs align incentives

Supplier-power risk: China >60% rare-earths; FY2024 sales $1.44B

Standex faces elevated supplier power due to reliance on specialty alloys, rare-earths (China >60% refined supply, USGS 2024) and niche tooling; FY2024 sales $1.44B make input costs material. Switching suppliers typically requires 3–12 months and $50k–$250k, while programs run 3–7 years. Mitigants: dual-sourcing, 3–6 months safety stock, regionalization and joint cost-downs.

| Metric | Value |

|---|---|

| FY2024 Sales | $1.44B |

| Rare-earths share (China) | >60% (USGS 2024) |

| Switch time/cost | 3–12 months / $50k–$250k |

| Safety stock | 3–6 months |

What is included in the product

Concise Porter's Five Forces analysis tailored to Standex that uncovers competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers affecting its pricing and profitability. Fully editable for reports, investor decks, or strategic planning to highlight emerging threats and defensive opportunities.

A concise one-sheet Porter’s Five Forces for Standex — editable pressure levels and an instant radar visualization relieve analysis pain, producing slide-ready summaries for fast strategic decisions.

Customers Bargaining Power

Concentrated OEM/ Tier-1 customers

Automotive, aerospace and electronics OEMs/Tier-1s are large, sophisticated buyers; consolidation means the top 10 global automakers account for over half of industry output in 2024, intensifying bidding and price pressure. Framework agreements and routine annual cost-reduction targets of roughly 2–4% are common; Standex offsets pressure via tailored customization and demonstrated performance value.

High qualification and switching frictions

Custom engineered solutions at Standex create high switching frictions because design-in, testing, and certifications commonly require 6–18 months, making awarded contracts sticky and limiting quick buyer switching despite initial pricing leverage. Lifecycle support and spare-parts programs further increase retention by reducing downtime risk. Performance and reliability drive renewal rates, often supporting multi-year repeat business.

Price transparency and should-cost

Industrial buyers deploy should-cost models and benchmark alternatives, increasing negotiating leverage on mature parts and pressuring Standex’s spot pricing in 2024. Rigorous value engineering and total cost of ownership framing have delivered documented part-level savings—often 10–20%—that help defend margins. Long-term, multi-year productivity roadmaps (typically 3–5 years) sustain partnerships and lock in joint improvement targets. Buyers’ price transparency shortens decision cycles and amplifies leverage.

Demand cyclicality

End markets such as automotive and electronics are highly cyclical, driving volume swings and frequent re-bids that increase customer bargaining pressure and push for price concessions in downturns; buyers intensify demands when OEM production softens. Standex mitigates this through flexible capacity and variable-cost structures that protect margins, while diversified end-markets smooth demand volatility.

Customization and co-development

Co-designed components embed Standex IP and tooling directly into customer systems, raising switching costs and eroding buyer leverage over time; by 2024 this strategic embedding accelerated account stickiness across engineered solutions. Service, engineering support and delivery reliability become clear differentiators, shifting negotiations from price to performance. Tight performance specs and integration reduce pure price focus and favor long-term contracts.

- Embedded IP increases switching costs

- Service & delivery drive competitive differentiation

- Performance specs lower pure price sensitivity

OEMs: 2–4% p.a., 6–18m design-in

Large OEMs/Tier-1 buyers (top 10 automakers >50% industry output in 2024) exert strong price pressure with routine 2–4% annual cost-reduction targets; Standex counters via customization and proven performance. Design-in and certification timelines of 6–18 months raise switching costs, supporting multi-year renewals. Buyers use should-cost models, driving 10–20% value-engineering savings on mature parts.

| Metric | 2024 Value |

|---|---|

| Top10 automakers share | >50% |

| Cost-reduction targets | 2–4% p.a. |

| Design-in time | 6–18 months |

| VE savings | 10–20% |

What You See Is What You Get

Standex Porter's Five Forces Analysis

This preview shows the exact Standex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis, ready for download and immediate use. You’ll get this same file instantly upon payment, complete and ready to support decision-making.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Standex faces moderate supplier power, niche customer segments, specialized substitutes, measured threat of new entrants, and intense industry rivalry shaping margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Standex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials dependence

Standex depends on specialty alloys, engineered polymers, rare-earth magnets and electronics that often have few qualified sources, with China supplying over 60% of refined rare earths (USGS 2024), raising supplier leverage during shortages. Long-term contracts and dual-sourcing partially offset exposure. Proactive inventory management is critical amid volatile commodity cycles.

Switching and qualification costs

Changing a materials or component supplier often requires requalification, testing and customer approvals, processes that typically take 3–12 months and can incur $50k–$250k in direct costs, elevating supplier power. Multi-year production programs (commonly 3–7 years) make midstream changes difficult and costly. Active supplier performance management and dual-sourcing reduce dependence and mitigate disruption risk.

Tooling and process know-how

Engraving and engineered components rely heavily on supplier tooling, surface treatments, and proprietary processes. Suppliers with unique capabilities can command better terms and pressure margins; Standex reported $1.44 billion in net sales in FY2024, so supplier costs are material. Knowledge lock-in raises switching barriers, while joint development and strategic sourcing can rebalance supplier influence and lower cost volatility.

Global supply chain constraints

Electronics and aerospace inputs for Standex face heightened geopolitical, logistics and compliance risk as 2024 saw expanded US export controls on advanced semiconductors and persistent EU REACH/RoHS constraints that limit substitute sources; short-term disruptions have amplified supplier bargaining power and pushed spot premiums higher, while regionalization and 3–6 months of safety stock remain primary mitigants.

- Export controls: tighter 2023–2024 limits on advanced chips

- Compliance: REACH/RoHS restricts alternatives

- Mitigation: regional sourcing, safety stock (3–6 months)

Scale versus niche volumes

Niche products produce lower aggregate volumes per SKU, reducing buyer leverage with large suppliers and raising per-unit costs; Standex’s FY2024 portfolio mix increased specialty SKU share, accentuating this pressure. Aggregating volumes across segments and platforms can recover scale benefits and improve procurement leverage. Vendor scorecards, should-cost analyses and joint cost-down programs align incentives and strengthen negotiations.

- Scale loss from niche SKUs — FY2024 portfolio shift

- Volume aggregation restores bargaining power

- Vendor scorecards + should-cost = better terms

- Collaborative cost-downs align incentives

Supplier-power risk: China >60% rare-earths; FY2024 sales $1.44B

Standex faces elevated supplier power due to reliance on specialty alloys, rare-earths (China >60% refined supply, USGS 2024) and niche tooling; FY2024 sales $1.44B make input costs material. Switching suppliers typically requires 3–12 months and $50k–$250k, while programs run 3–7 years. Mitigants: dual-sourcing, 3–6 months safety stock, regionalization and joint cost-downs.

| Metric | Value |

|---|---|

| FY2024 Sales | $1.44B |

| Rare-earths share (China) | >60% (USGS 2024) |

| Switch time/cost | 3–12 months / $50k–$250k |

| Safety stock | 3–6 months |

What is included in the product

Concise Porter's Five Forces analysis tailored to Standex that uncovers competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers affecting its pricing and profitability. Fully editable for reports, investor decks, or strategic planning to highlight emerging threats and defensive opportunities.

A concise one-sheet Porter’s Five Forces for Standex — editable pressure levels and an instant radar visualization relieve analysis pain, producing slide-ready summaries for fast strategic decisions.

Customers Bargaining Power

Concentrated OEM/ Tier-1 customers

Automotive, aerospace and electronics OEMs/Tier-1s are large, sophisticated buyers; consolidation means the top 10 global automakers account for over half of industry output in 2024, intensifying bidding and price pressure. Framework agreements and routine annual cost-reduction targets of roughly 2–4% are common; Standex offsets pressure via tailored customization and demonstrated performance value.

High qualification and switching frictions

Custom engineered solutions at Standex create high switching frictions because design-in, testing, and certifications commonly require 6–18 months, making awarded contracts sticky and limiting quick buyer switching despite initial pricing leverage. Lifecycle support and spare-parts programs further increase retention by reducing downtime risk. Performance and reliability drive renewal rates, often supporting multi-year repeat business.

Price transparency and should-cost

Industrial buyers deploy should-cost models and benchmark alternatives, increasing negotiating leverage on mature parts and pressuring Standex’s spot pricing in 2024. Rigorous value engineering and total cost of ownership framing have delivered documented part-level savings—often 10–20%—that help defend margins. Long-term, multi-year productivity roadmaps (typically 3–5 years) sustain partnerships and lock in joint improvement targets. Buyers’ price transparency shortens decision cycles and amplifies leverage.

Demand cyclicality

End markets such as automotive and electronics are highly cyclical, driving volume swings and frequent re-bids that increase customer bargaining pressure and push for price concessions in downturns; buyers intensify demands when OEM production softens. Standex mitigates this through flexible capacity and variable-cost structures that protect margins, while diversified end-markets smooth demand volatility.

Customization and co-development

Co-designed components embed Standex IP and tooling directly into customer systems, raising switching costs and eroding buyer leverage over time; by 2024 this strategic embedding accelerated account stickiness across engineered solutions. Service, engineering support and delivery reliability become clear differentiators, shifting negotiations from price to performance. Tight performance specs and integration reduce pure price focus and favor long-term contracts.

- Embedded IP increases switching costs

- Service & delivery drive competitive differentiation

- Performance specs lower pure price sensitivity

OEMs: 2–4% p.a., 6–18m design-in

Large OEMs/Tier-1 buyers (top 10 automakers >50% industry output in 2024) exert strong price pressure with routine 2–4% annual cost-reduction targets; Standex counters via customization and proven performance. Design-in and certification timelines of 6–18 months raise switching costs, supporting multi-year renewals. Buyers use should-cost models, driving 10–20% value-engineering savings on mature parts.

| Metric | 2024 Value |

|---|---|

| Top10 automakers share | >50% |

| Cost-reduction targets | 2–4% p.a. |

| Design-in time | 6–18 months |

| VE savings | 10–20% |

What You See Is What You Get

Standex Porter's Five Forces Analysis

This preview shows the exact Standex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis, ready for download and immediate use. You’ll get this same file instantly upon payment, complete and ready to support decision-making.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Standex faces moderate supplier power, niche customer segments, specialized substitutes, measured threat of new entrants, and intense industry rivalry shaping margins and growth prospects. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Standex’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized materials dependence

Standex depends on specialty alloys, engineered polymers, rare-earth magnets and electronics that often have few qualified sources, with China supplying over 60% of refined rare earths (USGS 2024), raising supplier leverage during shortages. Long-term contracts and dual-sourcing partially offset exposure. Proactive inventory management is critical amid volatile commodity cycles.

Switching and qualification costs

Changing a materials or component supplier often requires requalification, testing and customer approvals, processes that typically take 3–12 months and can incur $50k–$250k in direct costs, elevating supplier power. Multi-year production programs (commonly 3–7 years) make midstream changes difficult and costly. Active supplier performance management and dual-sourcing reduce dependence and mitigate disruption risk.

Tooling and process know-how

Engraving and engineered components rely heavily on supplier tooling, surface treatments, and proprietary processes. Suppliers with unique capabilities can command better terms and pressure margins; Standex reported $1.44 billion in net sales in FY2024, so supplier costs are material. Knowledge lock-in raises switching barriers, while joint development and strategic sourcing can rebalance supplier influence and lower cost volatility.

Global supply chain constraints

Electronics and aerospace inputs for Standex face heightened geopolitical, logistics and compliance risk as 2024 saw expanded US export controls on advanced semiconductors and persistent EU REACH/RoHS constraints that limit substitute sources; short-term disruptions have amplified supplier bargaining power and pushed spot premiums higher, while regionalization and 3–6 months of safety stock remain primary mitigants.

- Export controls: tighter 2023–2024 limits on advanced chips

- Compliance: REACH/RoHS restricts alternatives

- Mitigation: regional sourcing, safety stock (3–6 months)

Scale versus niche volumes

Niche products produce lower aggregate volumes per SKU, reducing buyer leverage with large suppliers and raising per-unit costs; Standex’s FY2024 portfolio mix increased specialty SKU share, accentuating this pressure. Aggregating volumes across segments and platforms can recover scale benefits and improve procurement leverage. Vendor scorecards, should-cost analyses and joint cost-down programs align incentives and strengthen negotiations.

- Scale loss from niche SKUs — FY2024 portfolio shift

- Volume aggregation restores bargaining power

- Vendor scorecards + should-cost = better terms

- Collaborative cost-downs align incentives

Supplier-power risk: China >60% rare-earths; FY2024 sales $1.44B

Standex faces elevated supplier power due to reliance on specialty alloys, rare-earths (China >60% refined supply, USGS 2024) and niche tooling; FY2024 sales $1.44B make input costs material. Switching suppliers typically requires 3–12 months and $50k–$250k, while programs run 3–7 years. Mitigants: dual-sourcing, 3–6 months safety stock, regionalization and joint cost-downs.

| Metric | Value |

|---|---|

| FY2024 Sales | $1.44B |

| Rare-earths share (China) | >60% (USGS 2024) |

| Switch time/cost | 3–12 months / $50k–$250k |

| Safety stock | 3–6 months |

What is included in the product

Concise Porter's Five Forces analysis tailored to Standex that uncovers competitive drivers, supplier and buyer power, threat of substitutes, and entry barriers affecting its pricing and profitability. Fully editable for reports, investor decks, or strategic planning to highlight emerging threats and defensive opportunities.

A concise one-sheet Porter’s Five Forces for Standex — editable pressure levels and an instant radar visualization relieve analysis pain, producing slide-ready summaries for fast strategic decisions.

Customers Bargaining Power

Concentrated OEM/ Tier-1 customers

Automotive, aerospace and electronics OEMs/Tier-1s are large, sophisticated buyers; consolidation means the top 10 global automakers account for over half of industry output in 2024, intensifying bidding and price pressure. Framework agreements and routine annual cost-reduction targets of roughly 2–4% are common; Standex offsets pressure via tailored customization and demonstrated performance value.

High qualification and switching frictions

Custom engineered solutions at Standex create high switching frictions because design-in, testing, and certifications commonly require 6–18 months, making awarded contracts sticky and limiting quick buyer switching despite initial pricing leverage. Lifecycle support and spare-parts programs further increase retention by reducing downtime risk. Performance and reliability drive renewal rates, often supporting multi-year repeat business.

Price transparency and should-cost

Industrial buyers deploy should-cost models and benchmark alternatives, increasing negotiating leverage on mature parts and pressuring Standex’s spot pricing in 2024. Rigorous value engineering and total cost of ownership framing have delivered documented part-level savings—often 10–20%—that help defend margins. Long-term, multi-year productivity roadmaps (typically 3–5 years) sustain partnerships and lock in joint improvement targets. Buyers’ price transparency shortens decision cycles and amplifies leverage.

Demand cyclicality

End markets such as automotive and electronics are highly cyclical, driving volume swings and frequent re-bids that increase customer bargaining pressure and push for price concessions in downturns; buyers intensify demands when OEM production softens. Standex mitigates this through flexible capacity and variable-cost structures that protect margins, while diversified end-markets smooth demand volatility.

Customization and co-development

Co-designed components embed Standex IP and tooling directly into customer systems, raising switching costs and eroding buyer leverage over time; by 2024 this strategic embedding accelerated account stickiness across engineered solutions. Service, engineering support and delivery reliability become clear differentiators, shifting negotiations from price to performance. Tight performance specs and integration reduce pure price focus and favor long-term contracts.

- Embedded IP increases switching costs

- Service & delivery drive competitive differentiation

- Performance specs lower pure price sensitivity

OEMs: 2–4% p.a., 6–18m design-in

Large OEMs/Tier-1 buyers (top 10 automakers >50% industry output in 2024) exert strong price pressure with routine 2–4% annual cost-reduction targets; Standex counters via customization and proven performance. Design-in and certification timelines of 6–18 months raise switching costs, supporting multi-year renewals. Buyers use should-cost models, driving 10–20% value-engineering savings on mature parts.

| Metric | 2024 Value |

|---|---|

| Top10 automakers share | >50% |

| Cost-reduction targets | 2–4% p.a. |

| Design-in time | 6–18 months |

| VE savings | 10–20% |

What You See Is What You Get

Standex Porter's Five Forces Analysis

This preview shows the exact Standex Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or mockups. The document is the full, professionally formatted analysis, ready for download and immediate use. You’ll get this same file instantly upon payment, complete and ready to support decision-making.