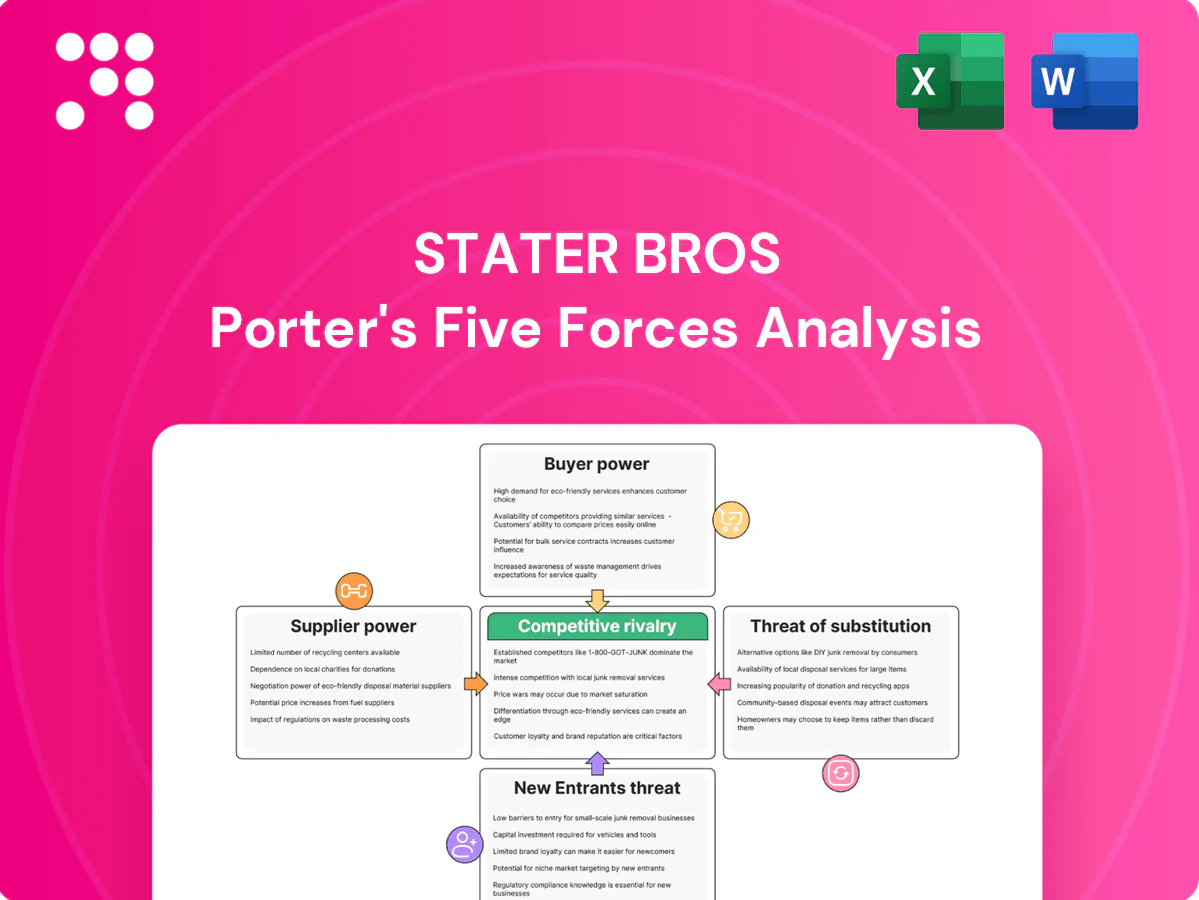

Stater Bros Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Stater Bros faces intense local competition, moderate supplier leverage, and rising substitute threats as shoppers shift to e-commerce and discount chains. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stater Bros’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Branded CPG leverage

Large national CPGs in snacks, beverages and household goods exert strong leverage via must-carry SKUs and marketing pull, giving suppliers pricing and placement power; Stater Bros operates about 172 stores (2024), far smaller than national chains, which limits rebate and slotting-fee negotiation. Private-label penetration (around 18% of US grocery volume in 2024) cushions margin pressure but cannot fully replace top brands, yielding moderate-to-high supplier power in key categories.

Perishables concentration

Produce, meat and seafood for Stater Bros rely heavily on regional growers and processors, with California supplying over half of U.S. fruits and vegetables, making seasonality and compliance rules critical. Droughts in 2021–2023 and disease outbreaks have periodically tightened availability and raised costs, while Prop 12-like mandates have increased compliance expense for suppliers. Limited alternate sources in off-seasons boost vendor leverage, and perishables' short shelf life—with ~30% of food lost or wasted globally—reduces buyers' negotiating power.

Switching costs and quality specs

Switching vendors is feasible for Stater Bros but constrained by food-safety audits and strict quality specs, and in 2024 fresh-category onboarding timelines and verification raise operational risk. Bringing new suppliers online takes weeks to months, increasing cost and spoilage exposure. For commodity center-store items switching is easier, lowering supplier power, while overall switching costs skew higher in perimeter departments.

Distribution and logistics

Distribution and logistics tighten supplier power for Stater Bros: limited cold‑chain capacity (U.S. cold‑storage vacancy near 6% in 2024, CBRE) plus trucking constraints and diesel near $4/gal (EIA 2024) raise landed costs; California carrier scarcity and port congestion can amplify supplier leverage and cause allocations; vendor‑managed inventory often favors larger chains, so Stater Bros must plan buys and hold buffer inventory.

- Cold‑chain vacancy ~6% (2024, CBRE)

- Diesel ≈ $4/gal (2024, EIA)

- Carrier scarcity/port delays increase supplier bargaining

- VMI/allocations favor larger chains — buffer inventory required

Local sourcing offsets

Strong ties to Southern California growers and regional producers across Stater Bros' ~171 stores diversify supply and reduce single-vendor risk; shorter lead times (days vs. weeks) and collaborative planning lower effective supplier power. Co-developing private-label lines with manufacturers secures better terms; these offsets moderate but do not eliminate supplier leverage.

- Regional sourcing reduces disruption risk

- Faster replenishment cuts buying leverage

- Private-label partnerships improve margins

Grocery chain squeezed by national brands, drought-driven produce costs and cold-chain strain

National CPGs exert high leverage via must‑carry SKUs and marketing; Stater Bros (172 stores, 2024) has limited slotting/rebate clout, keeping supplier power moderate‑high. Perishables sourcing from CA (over 50% of US produce) plus recent droughts (2021–23) and cold‑chain tightness raise costs. Private‑label (~18% US grocery volume, 2024) and regional sourcing partially offset pressure.

| Metric | Value (2024) |

|---|---|

| Stores | 172 |

| Private‑label share | ~18% |

| Cold‑chain vacancy | ~6% |

| Diesel | ≈ $4/gal |

What is included in the product

Concise Porter's Five Forces analysis of Stater Bros, uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and disruptive trends that influence its pricing, margins and market resilience.

A concise, slide-ready Porter's Five Forces summary for Stater Bros that visualizes competitive pressure with an editable radar chart—customize force levels, swap in your data, and drop directly into pitch decks to resolve strategic uncertainty quickly.

Customers Bargaining Power

High price sensitivity

Consumers in grocery are highly value-driven, with promotions shaping the majority of trips; NielsenIQ 2024 found promotions influenced over 60% of U.S. grocery purchases. Inflation-driven trade-down elevated private-label share to roughly 20% in 2024, while small price gaps shift baskets rapidly, reinforcing strong buyer power against Stater Bros.

Low switching costs

Shoppers face minimal friction to try competing supermarkets or online options, with U.S. online grocery penetration around 11% in 2024 and delivery apps (Instacart, DoorDash, Uber Eats) expanding grocery partnerships. Proximity and weekly ads make store hopping easy. Delivery apps further lower barriers. Loyalty programs increase frequency but do not fully lock in customers.

Abundant alternatives

Rivals from Ralphs, Vons, Walmart (≈25% of U.S. grocery sales), Target, Costco, Trader Joe’s, Sprouts and Amazon/Whole Foods (500+ U.S. stores) give shoppers many options. Convenience and dollar stores increasingly capture fill-in trips, while restaurants and meal-kit services act as meaningful substitutes. U.S. grocery e-commerce penetration rose toward ~10% in 2024, boosting switching ease. This abundance of choice raises buyer bargaining power.

Information transparency

Digital flyers, price-matching culture and review platforms make Stater Bros customers highly price-aware; with about 171 stores (2024) this transparency forces instant comparisons via apps that highlight deals and substitutions. Margin compression is severe on KVIs, pushing competition toward clear, communicated value rather than hidden promotions. Stater Bros must emphasize upfront everyday value and loyalty perks to defend share.

- Digital flyers: instant price visibility

- Apps: real-time deals and substitutions

- KVIs: squeezed margins, must show clear value

Loyalty and community ties

Stater Bros' neighborhood presence and service tradition—operating 172 stores in Southern California in 2024—builds trust and drives repeat visits. Targeted offers and growing private-label penetration improve perceived value. Loyalty is conditional on price and convenience, so buyer power remains high despite relational strengths.

- 172 stores (2024)

- Loyalty strong but price-sensitive

Promotions (>60%) and private-label (~20%) force visible value, tighten margins

Buyers wield strong power: promotions drive >60% of trips (NielsenIQ 2024), private-label share ~20% and online grocery ~11% (2024), so price-sensitive shoppers switch readily; Stater Bros operates 172 stores (2024) amid competitors (Walmart ≈25% share, Amazon/Whole Foods 500+ stores), forcing visible everyday value and tightened KVI margins.

| Metric | Value (2024) |

|---|---|

| Promo influence | >60% |

| Private-label share | ~20% |

| Online grocery | ~11% |

| Stater Bros stores | 172 |

| Walmart grocery share | ≈25% |

| Amazon/Whole Foods U.S. | 500+ |

Preview Before You Purchase

Stater Bros Porter's Five Forces Analysis

This preview shows the exact Stater Bros Porter’s Five Forces analysis you’ll receive—no placeholders. It provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications. The full file is formatted and ready for immediate download after purchase.

Go Beyond the Preview—Access the Full Strategic Report

Stater Bros faces intense local competition, moderate supplier leverage, and rising substitute threats as shoppers shift to e-commerce and discount chains. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stater Bros’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Branded CPG leverage

Large national CPGs in snacks, beverages and household goods exert strong leverage via must-carry SKUs and marketing pull, giving suppliers pricing and placement power; Stater Bros operates about 172 stores (2024), far smaller than national chains, which limits rebate and slotting-fee negotiation. Private-label penetration (around 18% of US grocery volume in 2024) cushions margin pressure but cannot fully replace top brands, yielding moderate-to-high supplier power in key categories.

Perishables concentration

Produce, meat and seafood for Stater Bros rely heavily on regional growers and processors, with California supplying over half of U.S. fruits and vegetables, making seasonality and compliance rules critical. Droughts in 2021–2023 and disease outbreaks have periodically tightened availability and raised costs, while Prop 12-like mandates have increased compliance expense for suppliers. Limited alternate sources in off-seasons boost vendor leverage, and perishables' short shelf life—with ~30% of food lost or wasted globally—reduces buyers' negotiating power.

Switching costs and quality specs

Switching vendors is feasible for Stater Bros but constrained by food-safety audits and strict quality specs, and in 2024 fresh-category onboarding timelines and verification raise operational risk. Bringing new suppliers online takes weeks to months, increasing cost and spoilage exposure. For commodity center-store items switching is easier, lowering supplier power, while overall switching costs skew higher in perimeter departments.

Distribution and logistics

Distribution and logistics tighten supplier power for Stater Bros: limited cold‑chain capacity (U.S. cold‑storage vacancy near 6% in 2024, CBRE) plus trucking constraints and diesel near $4/gal (EIA 2024) raise landed costs; California carrier scarcity and port congestion can amplify supplier leverage and cause allocations; vendor‑managed inventory often favors larger chains, so Stater Bros must plan buys and hold buffer inventory.

- Cold‑chain vacancy ~6% (2024, CBRE)

- Diesel ≈ $4/gal (2024, EIA)

- Carrier scarcity/port delays increase supplier bargaining

- VMI/allocations favor larger chains — buffer inventory required

Local sourcing offsets

Strong ties to Southern California growers and regional producers across Stater Bros' ~171 stores diversify supply and reduce single-vendor risk; shorter lead times (days vs. weeks) and collaborative planning lower effective supplier power. Co-developing private-label lines with manufacturers secures better terms; these offsets moderate but do not eliminate supplier leverage.

- Regional sourcing reduces disruption risk

- Faster replenishment cuts buying leverage

- Private-label partnerships improve margins

Grocery chain squeezed by national brands, drought-driven produce costs and cold-chain strain

National CPGs exert high leverage via must‑carry SKUs and marketing; Stater Bros (172 stores, 2024) has limited slotting/rebate clout, keeping supplier power moderate‑high. Perishables sourcing from CA (over 50% of US produce) plus recent droughts (2021–23) and cold‑chain tightness raise costs. Private‑label (~18% US grocery volume, 2024) and regional sourcing partially offset pressure.

| Metric | Value (2024) |

|---|---|

| Stores | 172 |

| Private‑label share | ~18% |

| Cold‑chain vacancy | ~6% |

| Diesel | ≈ $4/gal |

What is included in the product

Concise Porter's Five Forces analysis of Stater Bros, uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and disruptive trends that influence its pricing, margins and market resilience.

A concise, slide-ready Porter's Five Forces summary for Stater Bros that visualizes competitive pressure with an editable radar chart—customize force levels, swap in your data, and drop directly into pitch decks to resolve strategic uncertainty quickly.

Customers Bargaining Power

High price sensitivity

Consumers in grocery are highly value-driven, with promotions shaping the majority of trips; NielsenIQ 2024 found promotions influenced over 60% of U.S. grocery purchases. Inflation-driven trade-down elevated private-label share to roughly 20% in 2024, while small price gaps shift baskets rapidly, reinforcing strong buyer power against Stater Bros.

Low switching costs

Shoppers face minimal friction to try competing supermarkets or online options, with U.S. online grocery penetration around 11% in 2024 and delivery apps (Instacart, DoorDash, Uber Eats) expanding grocery partnerships. Proximity and weekly ads make store hopping easy. Delivery apps further lower barriers. Loyalty programs increase frequency but do not fully lock in customers.

Abundant alternatives

Rivals from Ralphs, Vons, Walmart (≈25% of U.S. grocery sales), Target, Costco, Trader Joe’s, Sprouts and Amazon/Whole Foods (500+ U.S. stores) give shoppers many options. Convenience and dollar stores increasingly capture fill-in trips, while restaurants and meal-kit services act as meaningful substitutes. U.S. grocery e-commerce penetration rose toward ~10% in 2024, boosting switching ease. This abundance of choice raises buyer bargaining power.

Information transparency

Digital flyers, price-matching culture and review platforms make Stater Bros customers highly price-aware; with about 171 stores (2024) this transparency forces instant comparisons via apps that highlight deals and substitutions. Margin compression is severe on KVIs, pushing competition toward clear, communicated value rather than hidden promotions. Stater Bros must emphasize upfront everyday value and loyalty perks to defend share.

- Digital flyers: instant price visibility

- Apps: real-time deals and substitutions

- KVIs: squeezed margins, must show clear value

Loyalty and community ties

Stater Bros' neighborhood presence and service tradition—operating 172 stores in Southern California in 2024—builds trust and drives repeat visits. Targeted offers and growing private-label penetration improve perceived value. Loyalty is conditional on price and convenience, so buyer power remains high despite relational strengths.

- 172 stores (2024)

- Loyalty strong but price-sensitive

Promotions (>60%) and private-label (~20%) force visible value, tighten margins

Buyers wield strong power: promotions drive >60% of trips (NielsenIQ 2024), private-label share ~20% and online grocery ~11% (2024), so price-sensitive shoppers switch readily; Stater Bros operates 172 stores (2024) amid competitors (Walmart ≈25% share, Amazon/Whole Foods 500+ stores), forcing visible everyday value and tightened KVI margins.

| Metric | Value (2024) |

|---|---|

| Promo influence | >60% |

| Private-label share | ~20% |

| Online grocery | ~11% |

| Stater Bros stores | 172 |

| Walmart grocery share | ≈25% |

| Amazon/Whole Foods U.S. | 500+ |

Preview Before You Purchase

Stater Bros Porter's Five Forces Analysis

This preview shows the exact Stater Bros Porter’s Five Forces analysis you’ll receive—no placeholders. It provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications. The full file is formatted and ready for immediate download after purchase.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Stater Bros faces intense local competition, moderate supplier leverage, and rising substitute threats as shoppers shift to e-commerce and discount chains. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stater Bros’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Branded CPG leverage

Large national CPGs in snacks, beverages and household goods exert strong leverage via must-carry SKUs and marketing pull, giving suppliers pricing and placement power; Stater Bros operates about 172 stores (2024), far smaller than national chains, which limits rebate and slotting-fee negotiation. Private-label penetration (around 18% of US grocery volume in 2024) cushions margin pressure but cannot fully replace top brands, yielding moderate-to-high supplier power in key categories.

Perishables concentration

Produce, meat and seafood for Stater Bros rely heavily on regional growers and processors, with California supplying over half of U.S. fruits and vegetables, making seasonality and compliance rules critical. Droughts in 2021–2023 and disease outbreaks have periodically tightened availability and raised costs, while Prop 12-like mandates have increased compliance expense for suppliers. Limited alternate sources in off-seasons boost vendor leverage, and perishables' short shelf life—with ~30% of food lost or wasted globally—reduces buyers' negotiating power.

Switching costs and quality specs

Switching vendors is feasible for Stater Bros but constrained by food-safety audits and strict quality specs, and in 2024 fresh-category onboarding timelines and verification raise operational risk. Bringing new suppliers online takes weeks to months, increasing cost and spoilage exposure. For commodity center-store items switching is easier, lowering supplier power, while overall switching costs skew higher in perimeter departments.

Distribution and logistics

Distribution and logistics tighten supplier power for Stater Bros: limited cold‑chain capacity (U.S. cold‑storage vacancy near 6% in 2024, CBRE) plus trucking constraints and diesel near $4/gal (EIA 2024) raise landed costs; California carrier scarcity and port congestion can amplify supplier leverage and cause allocations; vendor‑managed inventory often favors larger chains, so Stater Bros must plan buys and hold buffer inventory.

- Cold‑chain vacancy ~6% (2024, CBRE)

- Diesel ≈ $4/gal (2024, EIA)

- Carrier scarcity/port delays increase supplier bargaining

- VMI/allocations favor larger chains — buffer inventory required

Local sourcing offsets

Strong ties to Southern California growers and regional producers across Stater Bros' ~171 stores diversify supply and reduce single-vendor risk; shorter lead times (days vs. weeks) and collaborative planning lower effective supplier power. Co-developing private-label lines with manufacturers secures better terms; these offsets moderate but do not eliminate supplier leverage.

- Regional sourcing reduces disruption risk

- Faster replenishment cuts buying leverage

- Private-label partnerships improve margins

Grocery chain squeezed by national brands, drought-driven produce costs and cold-chain strain

National CPGs exert high leverage via must‑carry SKUs and marketing; Stater Bros (172 stores, 2024) has limited slotting/rebate clout, keeping supplier power moderate‑high. Perishables sourcing from CA (over 50% of US produce) plus recent droughts (2021–23) and cold‑chain tightness raise costs. Private‑label (~18% US grocery volume, 2024) and regional sourcing partially offset pressure.

| Metric | Value (2024) |

|---|---|

| Stores | 172 |

| Private‑label share | ~18% |

| Cold‑chain vacancy | ~6% |

| Diesel | ≈ $4/gal |

What is included in the product

Concise Porter's Five Forces analysis of Stater Bros, uncovering competitive rivalry, buyer and supplier power, threats from new entrants and substitutes, and disruptive trends that influence its pricing, margins and market resilience.

A concise, slide-ready Porter's Five Forces summary for Stater Bros that visualizes competitive pressure with an editable radar chart—customize force levels, swap in your data, and drop directly into pitch decks to resolve strategic uncertainty quickly.

Customers Bargaining Power

High price sensitivity

Consumers in grocery are highly value-driven, with promotions shaping the majority of trips; NielsenIQ 2024 found promotions influenced over 60% of U.S. grocery purchases. Inflation-driven trade-down elevated private-label share to roughly 20% in 2024, while small price gaps shift baskets rapidly, reinforcing strong buyer power against Stater Bros.

Low switching costs

Shoppers face minimal friction to try competing supermarkets or online options, with U.S. online grocery penetration around 11% in 2024 and delivery apps (Instacart, DoorDash, Uber Eats) expanding grocery partnerships. Proximity and weekly ads make store hopping easy. Delivery apps further lower barriers. Loyalty programs increase frequency but do not fully lock in customers.

Abundant alternatives

Rivals from Ralphs, Vons, Walmart (≈25% of U.S. grocery sales), Target, Costco, Trader Joe’s, Sprouts and Amazon/Whole Foods (500+ U.S. stores) give shoppers many options. Convenience and dollar stores increasingly capture fill-in trips, while restaurants and meal-kit services act as meaningful substitutes. U.S. grocery e-commerce penetration rose toward ~10% in 2024, boosting switching ease. This abundance of choice raises buyer bargaining power.

Information transparency

Digital flyers, price-matching culture and review platforms make Stater Bros customers highly price-aware; with about 171 stores (2024) this transparency forces instant comparisons via apps that highlight deals and substitutions. Margin compression is severe on KVIs, pushing competition toward clear, communicated value rather than hidden promotions. Stater Bros must emphasize upfront everyday value and loyalty perks to defend share.

- Digital flyers: instant price visibility

- Apps: real-time deals and substitutions

- KVIs: squeezed margins, must show clear value

Loyalty and community ties

Stater Bros' neighborhood presence and service tradition—operating 172 stores in Southern California in 2024—builds trust and drives repeat visits. Targeted offers and growing private-label penetration improve perceived value. Loyalty is conditional on price and convenience, so buyer power remains high despite relational strengths.

- 172 stores (2024)

- Loyalty strong but price-sensitive

Promotions (>60%) and private-label (~20%) force visible value, tighten margins

Buyers wield strong power: promotions drive >60% of trips (NielsenIQ 2024), private-label share ~20% and online grocery ~11% (2024), so price-sensitive shoppers switch readily; Stater Bros operates 172 stores (2024) amid competitors (Walmart ≈25% share, Amazon/Whole Foods 500+ stores), forcing visible everyday value and tightened KVI margins.

| Metric | Value (2024) |

|---|---|

| Promo influence | >60% |

| Private-label share | ~20% |

| Online grocery | ~11% |

| Stater Bros stores | 172 |

| Walmart grocery share | ≈25% |

| Amazon/Whole Foods U.S. | 500+ |

Preview Before You Purchase

Stater Bros Porter's Five Forces Analysis

This preview shows the exact Stater Bros Porter’s Five Forces analysis you’ll receive—no placeholders. It provides a concise evaluation of competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and strategic implications. The full file is formatted and ready for immediate download after purchase.