Stem Porter's Five Forces Analysis

Don't Miss the Bigger Picture

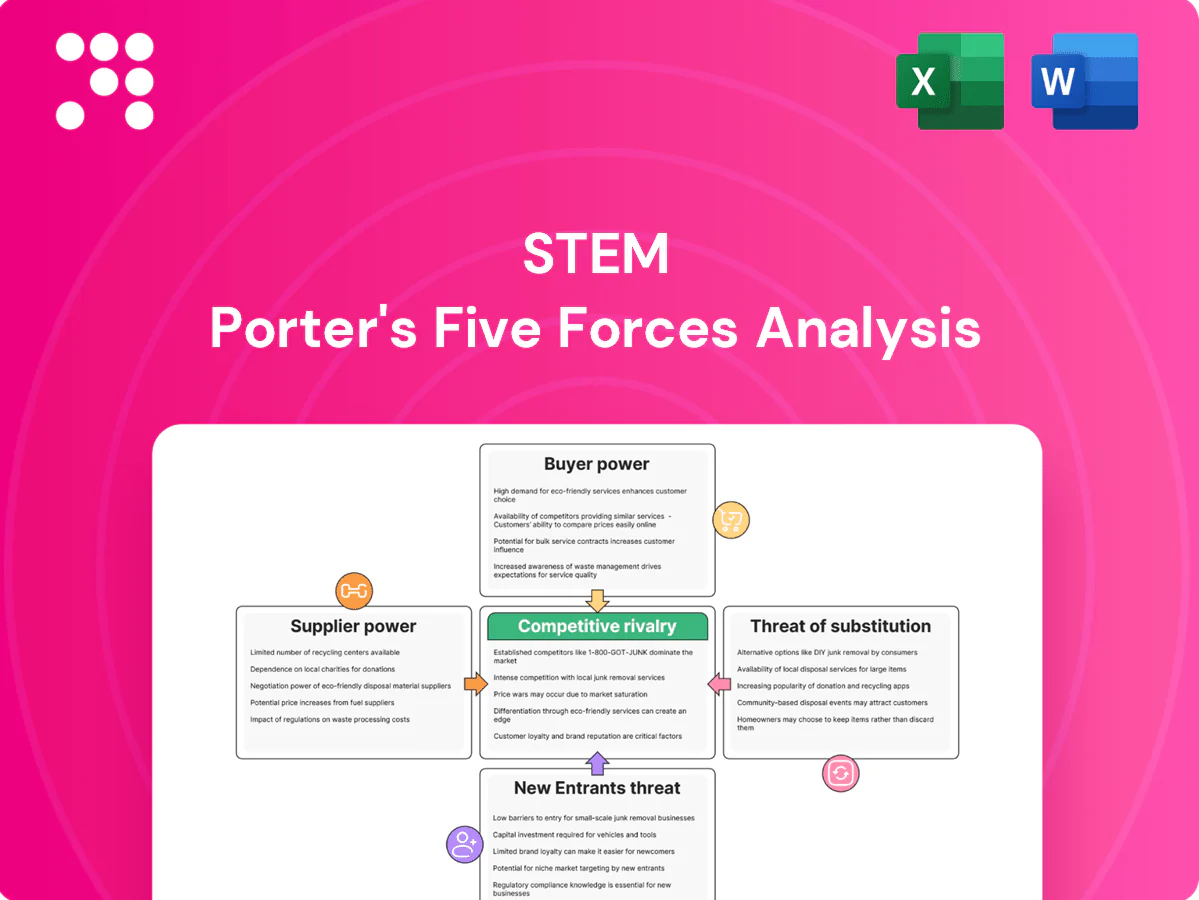

Stem’s Porter’s Five Forces snapshot outlines competitive intensity, supplier and buyer power, substitute threats, and barriers to entry in concise terms. This brief highlights key pressures shaping Stem’s strategic choices and market resilience. Want the full picture? Unlock the complete Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable implications to guide investment or strategy.

Suppliers Bargaining Power

DSP data dependence

Stem depends on DSPs for timely, accurate royalty data; API changes, rate limits or reporting delays can disrupt payouts and analytics, creating cash flow and reconciliation risk. Large DSPs like Spotify, Apple Music, Amazon and YouTube together held over 70% of global paid subscribers in 2024, enabling them to impose terms and fees with limited negotiation room. This concentration of supplier power heightens operational and pricing exposure for Stem.

Payments and banking

Payment processors and banking partners set settlement speed, fees (typically 1.5–3.5% for card rails) and compliance thresholds, giving them pricing power over Stem. Chargebacks and holds — often costing merchants $20–100 per dispute — plus 1–3% cross-border fees compress margins. Switching processors is complex due to KYC/AML and treasury integrations that can take weeks, increasing supplier leverage over Stem’s operations.

Cloud and infrastructure

Hosting, storage and data tooling are concentrated: AWS, Microsoft Azure and Google Cloud held roughly 66% of global IaaS/PaaS market in 2024, concentrating supplier power. Price hikes or multi-hour outages at these hyperscalers directly raise platform costs and reliability risk for Stem, with outages in 2023–24 disrupting millions of users. Data egress fees typically run about $0.09–$0.12 per GB ($90–$120 per TB), creating lock-in and switching friction, so suppliers wield clear pricing and performance influence.

Rights and metadata feeds

PROs, MLC, publishers and fingerprinting vendors supply essential rights and matching data; incomplete or delayed feeds often trigger disputes and higher support loads. Access terms and integration queues favor larger partners, creating onboarding delays for smaller services and elevating supplier bargaining power. Streaming represented ~65% of global music revenue in 2024, increasing dependency on accurate metadata.

- PROs: central rights holders

- MLC: mechanical claims hub

- Publishers: repertoire control

- Fingerprinting vendors: match accuracy

Compliance services

- Mandatory vendors: KYC/AML, sanctions, tax

- Market size 2024: $12.8B

- Regional vendor scarcity increases dependence

- Regulatory shifts enable fee increases

Suppliers wield leverage: DSPs, hyperscalers and processors drive costs and lock-in

Suppliers exert strong leverage: DSPs (Spotify/Apple/Amazon/YouTube >70% paid subs in 2024) and rights holders drive terms and payouts; hyperscalers (66% IaaS/PaaS 2024) and payment processors (fees 1.5–3.5%, chargebacks $20–$100) raise costs and lock-in; streaming = ~65% of music revenue (2024) increasing dependency; RegTech market ~$12.8B (2024) limits compliance alternatives.

| Supplier | Key 2024 stat |

|---|---|

| DSPs | >70% paid subs |

| Hyperscalers | 66% IaaS/PaaS |

| Streaming share | ~65% revenue |

| RegTech | $12.8B |

What is included in the product

Tailored Porter's Five Forces analysis for Stem that uncovers key drivers of competition, supplier and buyer power, substitutes and entrant threats, and identifies disruptive forces and strategic barriers protecting incumbency; delivered in a fully editable Word format for investor decks, business plans, or internal strategy use.

A concise, one-sheet Porter’s Five Forces summary tailored by Stem to instantly reveal competitive pressure points and guide strategic choices. Swap data, tweak scenarios, and export visuals for decks or reports—no technical skills required.

Customers Bargaining Power

Creator multi-homing

Artists and managers increasingly multi-home, with a 2024 MIDiA estimate that roughly 50% of independent creators use multiple distributors and finance tools simultaneously, raising churn risk. Low switching costs for SaaS distribution and payout services accelerate movement between rivals. Feature parity across platforms erodes differentiation, giving buyers leverage to negotiate lower fees and more favorable advance/royalty terms.

Catalog scale leverage

Larger indie labels and high-earning artists leverage catalog scale to demand lower take rates and bespoke reporting; with the Big Three and major indies controlling roughly 70% of recorded-music market share in 2024, revenue concentration makes their catalogs prime targets for competitors. Their ability to threaten catalog moves at renewal materially amplifies buyer bargaining power.

Price sensitivity

Independent creators watch net payout closely, with platforms like YouTube paying creators roughly 55% of ad revenue while payment processors (eg Stripe) charge 2.9% + $0.30 per transaction, making even small fee changes visible. Small fee shifts can erode trust and retention quickly. Transparent, predictable pricing is expected, and discounts plus tiered pricing have become table stakes.

Demand for transparency

Creators demand line-item detail, dispute workflows, and real-time dashboards; opacity drives scrutiny and platform switching—over 50 million creators worldwide heighten this pressure and competitors advertise instant splits and faster advances. Buyers exploit transparency gaps to negotiate concessions, eroding margin and increasing churn risk.

- line-item detail

- real-time dashboards

- instant splits/faster advances

- buyers push concessions

Support and UX expectations

Fast onboarding, self-serve tooling and responsive support drive purchase decisions; 2024 Salesforce data shows 76% of customers expect personalized, seamless experiences, and creators amplify both praise and complaints across forums, so poor UX spreads quickly and raises buyer power through reputational feedback loops.

- Fast onboarding

- Self-serve tooling

- Responsive support

- Social proof impact

Buyers gain leverage: multi-homing ~50%, big catalogs ~70%; creators seek real-time payouts

Buyers hold strong leverage: 2024 MIDiA finds ~50% of independents multi-home, low switching costs and feature parity drive fee negotiation. Big catalogs concentrate power—Big Three and major indies ~70% market share in 2024—enabling bespoke terms. Creators track payouts (YouTube ~55% ad share; Stripe 2.9%+ $0.30) and demand real-time detail, raising churn risk.

| Metric | 2024 Value |

|---|---|

| Multi-homing | ~50% |

| Market share (Big Three+maj. indies) | ~70% |

| YouTube ad payout | ~55% |

| Stripe fee | 2.9% + $0.30 |

| Personalized CX expectation (Salesforce) | 76% |

Same Document Delivered

Stem Porter's Five Forces Analysis

This preview shows the exact Stem Porter's Five Forces Analysis you'll receive after purchase—fully formatted, professional, and ready to use. It contains the complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. No placeholders or samples; download access is immediate upon payment.

Don't Miss the Bigger Picture

Stem’s Porter’s Five Forces snapshot outlines competitive intensity, supplier and buyer power, substitute threats, and barriers to entry in concise terms. This brief highlights key pressures shaping Stem’s strategic choices and market resilience. Want the full picture? Unlock the complete Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable implications to guide investment or strategy.

Suppliers Bargaining Power

DSP data dependence

Stem depends on DSPs for timely, accurate royalty data; API changes, rate limits or reporting delays can disrupt payouts and analytics, creating cash flow and reconciliation risk. Large DSPs like Spotify, Apple Music, Amazon and YouTube together held over 70% of global paid subscribers in 2024, enabling them to impose terms and fees with limited negotiation room. This concentration of supplier power heightens operational and pricing exposure for Stem.

Payments and banking

Payment processors and banking partners set settlement speed, fees (typically 1.5–3.5% for card rails) and compliance thresholds, giving them pricing power over Stem. Chargebacks and holds — often costing merchants $20–100 per dispute — plus 1–3% cross-border fees compress margins. Switching processors is complex due to KYC/AML and treasury integrations that can take weeks, increasing supplier leverage over Stem’s operations.

Cloud and infrastructure

Hosting, storage and data tooling are concentrated: AWS, Microsoft Azure and Google Cloud held roughly 66% of global IaaS/PaaS market in 2024, concentrating supplier power. Price hikes or multi-hour outages at these hyperscalers directly raise platform costs and reliability risk for Stem, with outages in 2023–24 disrupting millions of users. Data egress fees typically run about $0.09–$0.12 per GB ($90–$120 per TB), creating lock-in and switching friction, so suppliers wield clear pricing and performance influence.

Rights and metadata feeds

PROs, MLC, publishers and fingerprinting vendors supply essential rights and matching data; incomplete or delayed feeds often trigger disputes and higher support loads. Access terms and integration queues favor larger partners, creating onboarding delays for smaller services and elevating supplier bargaining power. Streaming represented ~65% of global music revenue in 2024, increasing dependency on accurate metadata.

- PROs: central rights holders

- MLC: mechanical claims hub

- Publishers: repertoire control

- Fingerprinting vendors: match accuracy

Compliance services

- Mandatory vendors: KYC/AML, sanctions, tax

- Market size 2024: $12.8B

- Regional vendor scarcity increases dependence

- Regulatory shifts enable fee increases

Suppliers wield leverage: DSPs, hyperscalers and processors drive costs and lock-in

Suppliers exert strong leverage: DSPs (Spotify/Apple/Amazon/YouTube >70% paid subs in 2024) and rights holders drive terms and payouts; hyperscalers (66% IaaS/PaaS 2024) and payment processors (fees 1.5–3.5%, chargebacks $20–$100) raise costs and lock-in; streaming = ~65% of music revenue (2024) increasing dependency; RegTech market ~$12.8B (2024) limits compliance alternatives.

| Supplier | Key 2024 stat |

|---|---|

| DSPs | >70% paid subs |

| Hyperscalers | 66% IaaS/PaaS |

| Streaming share | ~65% revenue |

| RegTech | $12.8B |

What is included in the product

Tailored Porter's Five Forces analysis for Stem that uncovers key drivers of competition, supplier and buyer power, substitutes and entrant threats, and identifies disruptive forces and strategic barriers protecting incumbency; delivered in a fully editable Word format for investor decks, business plans, or internal strategy use.

A concise, one-sheet Porter’s Five Forces summary tailored by Stem to instantly reveal competitive pressure points and guide strategic choices. Swap data, tweak scenarios, and export visuals for decks or reports—no technical skills required.

Customers Bargaining Power

Creator multi-homing

Artists and managers increasingly multi-home, with a 2024 MIDiA estimate that roughly 50% of independent creators use multiple distributors and finance tools simultaneously, raising churn risk. Low switching costs for SaaS distribution and payout services accelerate movement between rivals. Feature parity across platforms erodes differentiation, giving buyers leverage to negotiate lower fees and more favorable advance/royalty terms.

Catalog scale leverage

Larger indie labels and high-earning artists leverage catalog scale to demand lower take rates and bespoke reporting; with the Big Three and major indies controlling roughly 70% of recorded-music market share in 2024, revenue concentration makes their catalogs prime targets for competitors. Their ability to threaten catalog moves at renewal materially amplifies buyer bargaining power.

Price sensitivity

Independent creators watch net payout closely, with platforms like YouTube paying creators roughly 55% of ad revenue while payment processors (eg Stripe) charge 2.9% + $0.30 per transaction, making even small fee changes visible. Small fee shifts can erode trust and retention quickly. Transparent, predictable pricing is expected, and discounts plus tiered pricing have become table stakes.

Demand for transparency

Creators demand line-item detail, dispute workflows, and real-time dashboards; opacity drives scrutiny and platform switching—over 50 million creators worldwide heighten this pressure and competitors advertise instant splits and faster advances. Buyers exploit transparency gaps to negotiate concessions, eroding margin and increasing churn risk.

- line-item detail

- real-time dashboards

- instant splits/faster advances

- buyers push concessions

Support and UX expectations

Fast onboarding, self-serve tooling and responsive support drive purchase decisions; 2024 Salesforce data shows 76% of customers expect personalized, seamless experiences, and creators amplify both praise and complaints across forums, so poor UX spreads quickly and raises buyer power through reputational feedback loops.

- Fast onboarding

- Self-serve tooling

- Responsive support

- Social proof impact

Buyers gain leverage: multi-homing ~50%, big catalogs ~70%; creators seek real-time payouts

Buyers hold strong leverage: 2024 MIDiA finds ~50% of independents multi-home, low switching costs and feature parity drive fee negotiation. Big catalogs concentrate power—Big Three and major indies ~70% market share in 2024—enabling bespoke terms. Creators track payouts (YouTube ~55% ad share; Stripe 2.9%+ $0.30) and demand real-time detail, raising churn risk.

| Metric | 2024 Value |

|---|---|

| Multi-homing | ~50% |

| Market share (Big Three+maj. indies) | ~70% |

| YouTube ad payout | ~55% |

| Stripe fee | 2.9% + $0.30 |

| Personalized CX expectation (Salesforce) | 76% |

Same Document Delivered

Stem Porter's Five Forces Analysis

This preview shows the exact Stem Porter's Five Forces Analysis you'll receive after purchase—fully formatted, professional, and ready to use. It contains the complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. No placeholders or samples; download access is immediate upon payment.

Description

Don't Miss the Bigger Picture

Stem’s Porter’s Five Forces snapshot outlines competitive intensity, supplier and buyer power, substitute threats, and barriers to entry in concise terms. This brief highlights key pressures shaping Stem’s strategic choices and market resilience. Want the full picture? Unlock the complete Porter’s Five Forces Analysis for force-by-force ratings, visuals, and actionable implications to guide investment or strategy.

Suppliers Bargaining Power

DSP data dependence

Stem depends on DSPs for timely, accurate royalty data; API changes, rate limits or reporting delays can disrupt payouts and analytics, creating cash flow and reconciliation risk. Large DSPs like Spotify, Apple Music, Amazon and YouTube together held over 70% of global paid subscribers in 2024, enabling them to impose terms and fees with limited negotiation room. This concentration of supplier power heightens operational and pricing exposure for Stem.

Payments and banking

Payment processors and banking partners set settlement speed, fees (typically 1.5–3.5% for card rails) and compliance thresholds, giving them pricing power over Stem. Chargebacks and holds — often costing merchants $20–100 per dispute — plus 1–3% cross-border fees compress margins. Switching processors is complex due to KYC/AML and treasury integrations that can take weeks, increasing supplier leverage over Stem’s operations.

Cloud and infrastructure

Hosting, storage and data tooling are concentrated: AWS, Microsoft Azure and Google Cloud held roughly 66% of global IaaS/PaaS market in 2024, concentrating supplier power. Price hikes or multi-hour outages at these hyperscalers directly raise platform costs and reliability risk for Stem, with outages in 2023–24 disrupting millions of users. Data egress fees typically run about $0.09–$0.12 per GB ($90–$120 per TB), creating lock-in and switching friction, so suppliers wield clear pricing and performance influence.

Rights and metadata feeds

PROs, MLC, publishers and fingerprinting vendors supply essential rights and matching data; incomplete or delayed feeds often trigger disputes and higher support loads. Access terms and integration queues favor larger partners, creating onboarding delays for smaller services and elevating supplier bargaining power. Streaming represented ~65% of global music revenue in 2024, increasing dependency on accurate metadata.

- PROs: central rights holders

- MLC: mechanical claims hub

- Publishers: repertoire control

- Fingerprinting vendors: match accuracy

Compliance services

- Mandatory vendors: KYC/AML, sanctions, tax

- Market size 2024: $12.8B

- Regional vendor scarcity increases dependence

- Regulatory shifts enable fee increases

Suppliers wield leverage: DSPs, hyperscalers and processors drive costs and lock-in

Suppliers exert strong leverage: DSPs (Spotify/Apple/Amazon/YouTube >70% paid subs in 2024) and rights holders drive terms and payouts; hyperscalers (66% IaaS/PaaS 2024) and payment processors (fees 1.5–3.5%, chargebacks $20–$100) raise costs and lock-in; streaming = ~65% of music revenue (2024) increasing dependency; RegTech market ~$12.8B (2024) limits compliance alternatives.

| Supplier | Key 2024 stat |

|---|---|

| DSPs | >70% paid subs |

| Hyperscalers | 66% IaaS/PaaS |

| Streaming share | ~65% revenue |

| RegTech | $12.8B |

What is included in the product

Tailored Porter's Five Forces analysis for Stem that uncovers key drivers of competition, supplier and buyer power, substitutes and entrant threats, and identifies disruptive forces and strategic barriers protecting incumbency; delivered in a fully editable Word format for investor decks, business plans, or internal strategy use.

A concise, one-sheet Porter’s Five Forces summary tailored by Stem to instantly reveal competitive pressure points and guide strategic choices. Swap data, tweak scenarios, and export visuals for decks or reports—no technical skills required.

Customers Bargaining Power

Creator multi-homing

Artists and managers increasingly multi-home, with a 2024 MIDiA estimate that roughly 50% of independent creators use multiple distributors and finance tools simultaneously, raising churn risk. Low switching costs for SaaS distribution and payout services accelerate movement between rivals. Feature parity across platforms erodes differentiation, giving buyers leverage to negotiate lower fees and more favorable advance/royalty terms.

Catalog scale leverage

Larger indie labels and high-earning artists leverage catalog scale to demand lower take rates and bespoke reporting; with the Big Three and major indies controlling roughly 70% of recorded-music market share in 2024, revenue concentration makes their catalogs prime targets for competitors. Their ability to threaten catalog moves at renewal materially amplifies buyer bargaining power.

Price sensitivity

Independent creators watch net payout closely, with platforms like YouTube paying creators roughly 55% of ad revenue while payment processors (eg Stripe) charge 2.9% + $0.30 per transaction, making even small fee changes visible. Small fee shifts can erode trust and retention quickly. Transparent, predictable pricing is expected, and discounts plus tiered pricing have become table stakes.

Demand for transparency

Creators demand line-item detail, dispute workflows, and real-time dashboards; opacity drives scrutiny and platform switching—over 50 million creators worldwide heighten this pressure and competitors advertise instant splits and faster advances. Buyers exploit transparency gaps to negotiate concessions, eroding margin and increasing churn risk.

- line-item detail

- real-time dashboards

- instant splits/faster advances

- buyers push concessions

Support and UX expectations

Fast onboarding, self-serve tooling and responsive support drive purchase decisions; 2024 Salesforce data shows 76% of customers expect personalized, seamless experiences, and creators amplify both praise and complaints across forums, so poor UX spreads quickly and raises buyer power through reputational feedback loops.

- Fast onboarding

- Self-serve tooling

- Responsive support

- Social proof impact

Buyers gain leverage: multi-homing ~50%, big catalogs ~70%; creators seek real-time payouts

Buyers hold strong leverage: 2024 MIDiA finds ~50% of independents multi-home, low switching costs and feature parity drive fee negotiation. Big catalogs concentrate power—Big Three and major indies ~70% market share in 2024—enabling bespoke terms. Creators track payouts (YouTube ~55% ad share; Stripe 2.9%+ $0.30) and demand real-time detail, raising churn risk.

| Metric | 2024 Value |

|---|---|

| Multi-homing | ~50% |

| Market share (Big Three+maj. indies) | ~70% |

| YouTube ad payout | ~55% |

| Stripe fee | 2.9% + $0.30 |

| Personalized CX expectation (Salesforce) | 76% |

Same Document Delivered

Stem Porter's Five Forces Analysis

This preview shows the exact Stem Porter's Five Forces Analysis you'll receive after purchase—fully formatted, professional, and ready to use. It contains the complete evaluation of competitive rivalry, supplier and buyer power, threats of entry and substitution, and strategic implications. No placeholders or samples; download access is immediate upon payment.