StepStone Boston Consulting Group Matrix

Unlock Strategic Clarity

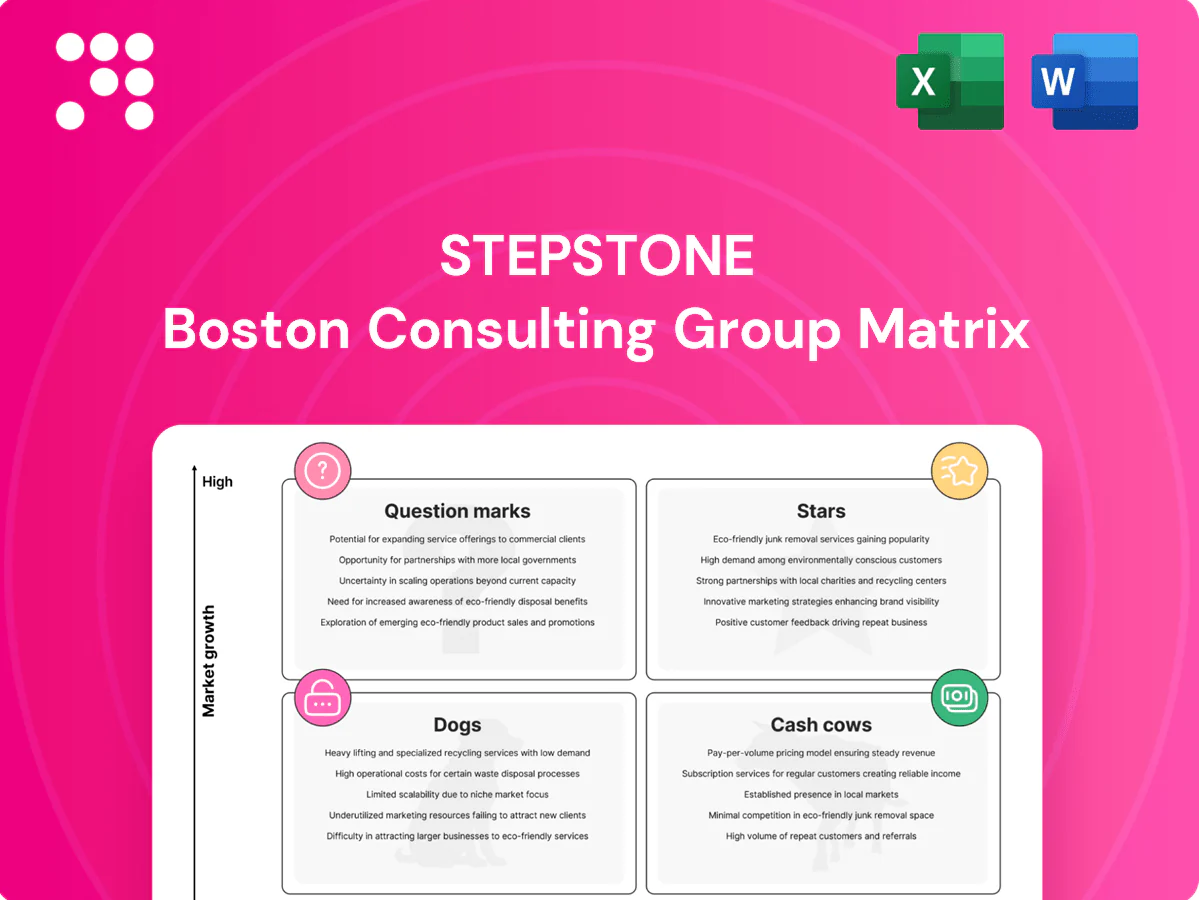

Want the full picture on StepStone’s portfolio? This preview shows the outlines—Stars, Cash Cows, Dogs, Question Marks—but the complete BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and clear moves you can act on. Buy the full report for a Word deep-dive plus an Excel summary you can plug into presentations and models. Skip the guesswork—get strategic clarity and a ready-to-use plan today.

Stars

Scaled private equity secondaries

Scaled private equity secondaries sit in High Growth with StepStone holding meaningful share, behaving like a classic Star as global secondary volumes exceed $100bn annually and GP-leds now account for roughly two-thirds of deal value.

Deal flow and GP-led complexity demand heavy origination, analytics, and capital — true cash in, cash out — so StepStone must keep feeding the engine or share slips.

Sustain leadership now and, as market growth normalizes, this Star can mature into a Cash Cow.

Global co‑investment platform

Strong sponsor access plus rapid underwriting places the global co‑investment platform in the high‑share, fast‑growing Stars quadrant; industry co‑investment deal volume exceeded $140bn in 2024, underlining momentum. It requires constant sourcing, deep diligence teams and active LP mobilization, so operating costs and capital for deal flow are substantial. Competitive edge is speed and sponsor relationships—both demand ongoing investment. Maintain pace and it compounds into a durable fee and carry franchise.

Infrastructure energy transition

Secular tailwinds—grid upgrades, renewables and decarbonization—are accelerating: US policy via the Inflation Reduction Act channels roughly 369 billion USD toward clean energy incentives, boosting market scale and StepStone’s strategic runway. StepStone’s expanding presence and pipeline-building, technical diligence and new GP relationships absorb cash today but secure access in a market growing faster than average. Nurture this share and it becomes a long-run profit center.

Real estate secondaries & GP‑led solutions

Real estate secondaries and GP‑led solutions are a Stars quadrant play as liquidity needs in property funds spiked amid 2023–24 repricing; private markets secondaries hit about $85bn in 2023 (Preqin), and few firms can price the complexity reliably. StepStone’s cross‑asset insights shorten learning curves but success still demands capital, granular data and structuring talent. The category is scaling fast so continued reinvestment is required to defend and grow the lead; hold share through the growth curve and it should mature attractively.

- Liquidity spike: 2023 secondaries ≈ $85bn (Preqin)

- Key advantages: cross‑asset insights + structuring teams

- Requires: capital, data, talent, reinvestment to defend share

Proprietary data & analytics engine

StepStone’s proprietary data and analytics engine underpins origination and selection across strategies, creating a defensible moat as private markets AUM surpassed 10 trillion USD in 2024; continuous model tuning and data ingestion absorb material investment yet drive higher win‑rates and improved deal pacing, reinforcing share. Keep investing: operating leverage today converts to future free cash flow and retention advantages.

- Moat: data-driven origination

- Cost: ongoing model/tooling spend

- Benefit: higher win‑rates, better pacing

- Outcome: operating leverage → future cash flow

Secondaries & co-invest: >100bn sec, ≈140bn co-invest, >10tn AUM

Scaled secondaries and co‑investment sit as Stars: high growth, high share but cash‑hungry; global secondary volumes >100bn (annual) and co‑investment ≈140bn in 2024. StepStone’s data moat (private markets AUM >10tn in 2024) and sponsor access are advantages; continuous origination, diligence and capital reinvestment are required to sustain leadership and convert to a Cash Cow.

| Metric | 2023/24 | Note |

|---|---|---|

| Secondary volumes | >100bn | annual |

| Co‑investment | ≈140bn | 2024 |

| Private markets AUM | >10tn | 2024 |

What is included in the product

Comprehensive BCG Matrix review of StepStone’s units with strategic moves: invest, hold, divest, and trends per quadrant.

One-page StepStone BCG Matrix highlights priorities fast, export-ready for C-level decks and quick PowerPoint drop-in.

Cash Cows

Advisory mandates for institutions

Advisory mandates for institutions are a classic Cash Cow: mature, sticky relationships with recurring fees and retention typically above 90% (2024 industry surveys), delivering steady revenue even in low market growth. Strong share and client trust support solid operating margins (commonly 20–30%), while incremental cost to serve falls once team and processes are established. Priorities: maintain service quality, expand wallet share, and milk predictable cash flows.

Separate accounts in private equity

Separate accounts in private equity produce predictable management fees and scale economies, with institutional mandates helping StepStone lock in steady cashflows even as industry dry powder reached roughly $1.8 trillion in 2024. Growth is steady rather than explosive; StepStone already holds strong positions in bespoke mandates across pensions and sovereigns. Efficient operations and reporting lift long-term margins, so invest to maintain productivity and harvest surplus cash.

Diversified fund‑of‑funds

Diversified fund‑of‑funds is a well‑known StepStone product with roughly $140bn AUM across strategies (2024), operating in a slower market growth phase (~3%–5% p.a. industry CAGR). High brand recognition yields ~85% client retention and steady management fees (~1.2% avg), so fee streams are reliable and distribution spend is modest (3%–5% of fee revenue). Process efficiency and vintage consistency support healthy EBITDA margins (~25%–30%); keep allocations tight and redeploy cash into Stars.

Portfolio monitoring & reporting services

Portfolio monitoring and reporting is a cash cow for StepStone: required by nearly every institutional client, not a hyper‑growth segment but high-margin once built, with industry reporting platform gross margins around 65–75% in 2024 and low incremental cost per account. It produces sticky recurring fees, strengthens client lock‑in and can boost cash contribution by optimizing workflows and automation across accounts.

- Needed by all institutional clients

- 2024 platform margins ~65–75%

- Sticky, recurring revenue; strengthens retention

- Workflow automation widens cash contribution

Secondary advisory & syndication services

Secondary advisory & syndication at StepStone is a cash cow: entrenched network effects and repeat GP relationships create a steady pipeline, supporting high deal conversion and predictable fee income.

Market growth is moderate; global secondary transaction volume was about $78 billion in 2023, and StepStone’s share is strong given its leading placement track record and distribution reach.

Margins benefit from standardized processes and repeat buyers, driving high operating leverage—preserve GP relationships, keep the engine humming, and bank the cash.

- Pipeline stability: repeat GP relationships

- Market size: ~$78bn secondary volume (2023)

- Competitive position: strong placement share

- Margin drivers: standardization + repeat buyers

Cash cows: advisory mandates, separate accounts, FoFs, reporting & secondaries drive recurring fees

StepStone cash cows: advisory mandates deliver recurring fees with >90% retention (2024) and 20–30% margins; separate accounts lock steady management fees amid ~$1.8T private markets dry powder (2024); diversified FoFs: ~$140bn AUM (2024), ~1.2% avg fee, ~85% retention; reporting platforms yield 65–75% gross margins (2024) and high operating leverage; secondaries benefit from ~ $78bn market (2023) and repeat GP flow.

| Segment | Key metrics | Margin | Retention |

|---|---|---|---|

| Advisory mandates | Recurring fees | 20–30% | >90% (2024) |

| Separate accounts | $1.8T dry powder (2024) | High | High |

| FoFs | $140bn AUM (2024), 1.2% fee | 25–30% EBITDA | ~85% |

| Reporting | Platform services | 65–75% gross | Sticky |

| Secondaries | $78bn volume (2023) | High | Repeat GPs |

What You See Is What You Get

StepStone BCG Matrix

The file you're previewing here is the exact StepStone BCG Matrix document you'll receive after purchase — no watermarks, no demo text, just the finished report. It’s fully formatted and analysis-ready, designed by strategy experts for clarity and quick decisions. Once purchased, the same file is delivered to your inbox for immediate download, editing, printing, or presenting. No surprises, no extra steps — just plug it into your planning.

Unlock Strategic Clarity

Want the full picture on StepStone’s portfolio? This preview shows the outlines—Stars, Cash Cows, Dogs, Question Marks—but the complete BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and clear moves you can act on. Buy the full report for a Word deep-dive plus an Excel summary you can plug into presentations and models. Skip the guesswork—get strategic clarity and a ready-to-use plan today.

Stars

Scaled private equity secondaries

Scaled private equity secondaries sit in High Growth with StepStone holding meaningful share, behaving like a classic Star as global secondary volumes exceed $100bn annually and GP-leds now account for roughly two-thirds of deal value.

Deal flow and GP-led complexity demand heavy origination, analytics, and capital — true cash in, cash out — so StepStone must keep feeding the engine or share slips.

Sustain leadership now and, as market growth normalizes, this Star can mature into a Cash Cow.

Global co‑investment platform

Strong sponsor access plus rapid underwriting places the global co‑investment platform in the high‑share, fast‑growing Stars quadrant; industry co‑investment deal volume exceeded $140bn in 2024, underlining momentum. It requires constant sourcing, deep diligence teams and active LP mobilization, so operating costs and capital for deal flow are substantial. Competitive edge is speed and sponsor relationships—both demand ongoing investment. Maintain pace and it compounds into a durable fee and carry franchise.

Infrastructure energy transition

Secular tailwinds—grid upgrades, renewables and decarbonization—are accelerating: US policy via the Inflation Reduction Act channels roughly 369 billion USD toward clean energy incentives, boosting market scale and StepStone’s strategic runway. StepStone’s expanding presence and pipeline-building, technical diligence and new GP relationships absorb cash today but secure access in a market growing faster than average. Nurture this share and it becomes a long-run profit center.

Real estate secondaries & GP‑led solutions

Real estate secondaries and GP‑led solutions are a Stars quadrant play as liquidity needs in property funds spiked amid 2023–24 repricing; private markets secondaries hit about $85bn in 2023 (Preqin), and few firms can price the complexity reliably. StepStone’s cross‑asset insights shorten learning curves but success still demands capital, granular data and structuring talent. The category is scaling fast so continued reinvestment is required to defend and grow the lead; hold share through the growth curve and it should mature attractively.

- Liquidity spike: 2023 secondaries ≈ $85bn (Preqin)

- Key advantages: cross‑asset insights + structuring teams

- Requires: capital, data, talent, reinvestment to defend share

Proprietary data & analytics engine

StepStone’s proprietary data and analytics engine underpins origination and selection across strategies, creating a defensible moat as private markets AUM surpassed 10 trillion USD in 2024; continuous model tuning and data ingestion absorb material investment yet drive higher win‑rates and improved deal pacing, reinforcing share. Keep investing: operating leverage today converts to future free cash flow and retention advantages.

- Moat: data-driven origination

- Cost: ongoing model/tooling spend

- Benefit: higher win‑rates, better pacing

- Outcome: operating leverage → future cash flow

Secondaries & co-invest: >100bn sec, ≈140bn co-invest, >10tn AUM

Scaled secondaries and co‑investment sit as Stars: high growth, high share but cash‑hungry; global secondary volumes >100bn (annual) and co‑investment ≈140bn in 2024. StepStone’s data moat (private markets AUM >10tn in 2024) and sponsor access are advantages; continuous origination, diligence and capital reinvestment are required to sustain leadership and convert to a Cash Cow.

| Metric | 2023/24 | Note |

|---|---|---|

| Secondary volumes | >100bn | annual |

| Co‑investment | ≈140bn | 2024 |

| Private markets AUM | >10tn | 2024 |

What is included in the product

Comprehensive BCG Matrix review of StepStone’s units with strategic moves: invest, hold, divest, and trends per quadrant.

One-page StepStone BCG Matrix highlights priorities fast, export-ready for C-level decks and quick PowerPoint drop-in.

Cash Cows

Advisory mandates for institutions

Advisory mandates for institutions are a classic Cash Cow: mature, sticky relationships with recurring fees and retention typically above 90% (2024 industry surveys), delivering steady revenue even in low market growth. Strong share and client trust support solid operating margins (commonly 20–30%), while incremental cost to serve falls once team and processes are established. Priorities: maintain service quality, expand wallet share, and milk predictable cash flows.

Separate accounts in private equity

Separate accounts in private equity produce predictable management fees and scale economies, with institutional mandates helping StepStone lock in steady cashflows even as industry dry powder reached roughly $1.8 trillion in 2024. Growth is steady rather than explosive; StepStone already holds strong positions in bespoke mandates across pensions and sovereigns. Efficient operations and reporting lift long-term margins, so invest to maintain productivity and harvest surplus cash.

Diversified fund‑of‑funds

Diversified fund‑of‑funds is a well‑known StepStone product with roughly $140bn AUM across strategies (2024), operating in a slower market growth phase (~3%–5% p.a. industry CAGR). High brand recognition yields ~85% client retention and steady management fees (~1.2% avg), so fee streams are reliable and distribution spend is modest (3%–5% of fee revenue). Process efficiency and vintage consistency support healthy EBITDA margins (~25%–30%); keep allocations tight and redeploy cash into Stars.

Portfolio monitoring & reporting services

Portfolio monitoring and reporting is a cash cow for StepStone: required by nearly every institutional client, not a hyper‑growth segment but high-margin once built, with industry reporting platform gross margins around 65–75% in 2024 and low incremental cost per account. It produces sticky recurring fees, strengthens client lock‑in and can boost cash contribution by optimizing workflows and automation across accounts.

- Needed by all institutional clients

- 2024 platform margins ~65–75%

- Sticky, recurring revenue; strengthens retention

- Workflow automation widens cash contribution

Secondary advisory & syndication services

Secondary advisory & syndication at StepStone is a cash cow: entrenched network effects and repeat GP relationships create a steady pipeline, supporting high deal conversion and predictable fee income.

Market growth is moderate; global secondary transaction volume was about $78 billion in 2023, and StepStone’s share is strong given its leading placement track record and distribution reach.

Margins benefit from standardized processes and repeat buyers, driving high operating leverage—preserve GP relationships, keep the engine humming, and bank the cash.

- Pipeline stability: repeat GP relationships

- Market size: ~$78bn secondary volume (2023)

- Competitive position: strong placement share

- Margin drivers: standardization + repeat buyers

Cash cows: advisory mandates, separate accounts, FoFs, reporting & secondaries drive recurring fees

StepStone cash cows: advisory mandates deliver recurring fees with >90% retention (2024) and 20–30% margins; separate accounts lock steady management fees amid ~$1.8T private markets dry powder (2024); diversified FoFs: ~$140bn AUM (2024), ~1.2% avg fee, ~85% retention; reporting platforms yield 65–75% gross margins (2024) and high operating leverage; secondaries benefit from ~ $78bn market (2023) and repeat GP flow.

| Segment | Key metrics | Margin | Retention |

|---|---|---|---|

| Advisory mandates | Recurring fees | 20–30% | >90% (2024) |

| Separate accounts | $1.8T dry powder (2024) | High | High |

| FoFs | $140bn AUM (2024), 1.2% fee | 25–30% EBITDA | ~85% |

| Reporting | Platform services | 65–75% gross | Sticky |

| Secondaries | $78bn volume (2023) | High | Repeat GPs |

What You See Is What You Get

StepStone BCG Matrix

The file you're previewing here is the exact StepStone BCG Matrix document you'll receive after purchase — no watermarks, no demo text, just the finished report. It’s fully formatted and analysis-ready, designed by strategy experts for clarity and quick decisions. Once purchased, the same file is delivered to your inbox for immediate download, editing, printing, or presenting. No surprises, no extra steps — just plug it into your planning.

Description

Unlock Strategic Clarity

Want the full picture on StepStone’s portfolio? This preview shows the outlines—Stars, Cash Cows, Dogs, Question Marks—but the complete BCG Matrix gives quadrant-by-quadrant placements, data-backed recommendations, and clear moves you can act on. Buy the full report for a Word deep-dive plus an Excel summary you can plug into presentations and models. Skip the guesswork—get strategic clarity and a ready-to-use plan today.

Stars

Scaled private equity secondaries

Scaled private equity secondaries sit in High Growth with StepStone holding meaningful share, behaving like a classic Star as global secondary volumes exceed $100bn annually and GP-leds now account for roughly two-thirds of deal value.

Deal flow and GP-led complexity demand heavy origination, analytics, and capital — true cash in, cash out — so StepStone must keep feeding the engine or share slips.

Sustain leadership now and, as market growth normalizes, this Star can mature into a Cash Cow.

Global co‑investment platform

Strong sponsor access plus rapid underwriting places the global co‑investment platform in the high‑share, fast‑growing Stars quadrant; industry co‑investment deal volume exceeded $140bn in 2024, underlining momentum. It requires constant sourcing, deep diligence teams and active LP mobilization, so operating costs and capital for deal flow are substantial. Competitive edge is speed and sponsor relationships—both demand ongoing investment. Maintain pace and it compounds into a durable fee and carry franchise.

Infrastructure energy transition

Secular tailwinds—grid upgrades, renewables and decarbonization—are accelerating: US policy via the Inflation Reduction Act channels roughly 369 billion USD toward clean energy incentives, boosting market scale and StepStone’s strategic runway. StepStone’s expanding presence and pipeline-building, technical diligence and new GP relationships absorb cash today but secure access in a market growing faster than average. Nurture this share and it becomes a long-run profit center.

Real estate secondaries & GP‑led solutions

Real estate secondaries and GP‑led solutions are a Stars quadrant play as liquidity needs in property funds spiked amid 2023–24 repricing; private markets secondaries hit about $85bn in 2023 (Preqin), and few firms can price the complexity reliably. StepStone’s cross‑asset insights shorten learning curves but success still demands capital, granular data and structuring talent. The category is scaling fast so continued reinvestment is required to defend and grow the lead; hold share through the growth curve and it should mature attractively.

- Liquidity spike: 2023 secondaries ≈ $85bn (Preqin)

- Key advantages: cross‑asset insights + structuring teams

- Requires: capital, data, talent, reinvestment to defend share

Proprietary data & analytics engine

StepStone’s proprietary data and analytics engine underpins origination and selection across strategies, creating a defensible moat as private markets AUM surpassed 10 trillion USD in 2024; continuous model tuning and data ingestion absorb material investment yet drive higher win‑rates and improved deal pacing, reinforcing share. Keep investing: operating leverage today converts to future free cash flow and retention advantages.

- Moat: data-driven origination

- Cost: ongoing model/tooling spend

- Benefit: higher win‑rates, better pacing

- Outcome: operating leverage → future cash flow

Secondaries & co-invest: >100bn sec, ≈140bn co-invest, >10tn AUM

Scaled secondaries and co‑investment sit as Stars: high growth, high share but cash‑hungry; global secondary volumes >100bn (annual) and co‑investment ≈140bn in 2024. StepStone’s data moat (private markets AUM >10tn in 2024) and sponsor access are advantages; continuous origination, diligence and capital reinvestment are required to sustain leadership and convert to a Cash Cow.

| Metric | 2023/24 | Note |

|---|---|---|

| Secondary volumes | >100bn | annual |

| Co‑investment | ≈140bn | 2024 |

| Private markets AUM | >10tn | 2024 |

What is included in the product

Comprehensive BCG Matrix review of StepStone’s units with strategic moves: invest, hold, divest, and trends per quadrant.

One-page StepStone BCG Matrix highlights priorities fast, export-ready for C-level decks and quick PowerPoint drop-in.

Cash Cows

Advisory mandates for institutions

Advisory mandates for institutions are a classic Cash Cow: mature, sticky relationships with recurring fees and retention typically above 90% (2024 industry surveys), delivering steady revenue even in low market growth. Strong share and client trust support solid operating margins (commonly 20–30%), while incremental cost to serve falls once team and processes are established. Priorities: maintain service quality, expand wallet share, and milk predictable cash flows.

Separate accounts in private equity

Separate accounts in private equity produce predictable management fees and scale economies, with institutional mandates helping StepStone lock in steady cashflows even as industry dry powder reached roughly $1.8 trillion in 2024. Growth is steady rather than explosive; StepStone already holds strong positions in bespoke mandates across pensions and sovereigns. Efficient operations and reporting lift long-term margins, so invest to maintain productivity and harvest surplus cash.

Diversified fund‑of‑funds

Diversified fund‑of‑funds is a well‑known StepStone product with roughly $140bn AUM across strategies (2024), operating in a slower market growth phase (~3%–5% p.a. industry CAGR). High brand recognition yields ~85% client retention and steady management fees (~1.2% avg), so fee streams are reliable and distribution spend is modest (3%–5% of fee revenue). Process efficiency and vintage consistency support healthy EBITDA margins (~25%–30%); keep allocations tight and redeploy cash into Stars.

Portfolio monitoring & reporting services

Portfolio monitoring and reporting is a cash cow for StepStone: required by nearly every institutional client, not a hyper‑growth segment but high-margin once built, with industry reporting platform gross margins around 65–75% in 2024 and low incremental cost per account. It produces sticky recurring fees, strengthens client lock‑in and can boost cash contribution by optimizing workflows and automation across accounts.

- Needed by all institutional clients

- 2024 platform margins ~65–75%

- Sticky, recurring revenue; strengthens retention

- Workflow automation widens cash contribution

Secondary advisory & syndication services

Secondary advisory & syndication at StepStone is a cash cow: entrenched network effects and repeat GP relationships create a steady pipeline, supporting high deal conversion and predictable fee income.

Market growth is moderate; global secondary transaction volume was about $78 billion in 2023, and StepStone’s share is strong given its leading placement track record and distribution reach.

Margins benefit from standardized processes and repeat buyers, driving high operating leverage—preserve GP relationships, keep the engine humming, and bank the cash.

- Pipeline stability: repeat GP relationships

- Market size: ~$78bn secondary volume (2023)

- Competitive position: strong placement share

- Margin drivers: standardization + repeat buyers

Cash cows: advisory mandates, separate accounts, FoFs, reporting & secondaries drive recurring fees

StepStone cash cows: advisory mandates deliver recurring fees with >90% retention (2024) and 20–30% margins; separate accounts lock steady management fees amid ~$1.8T private markets dry powder (2024); diversified FoFs: ~$140bn AUM (2024), ~1.2% avg fee, ~85% retention; reporting platforms yield 65–75% gross margins (2024) and high operating leverage; secondaries benefit from ~ $78bn market (2023) and repeat GP flow.

| Segment | Key metrics | Margin | Retention |

|---|---|---|---|

| Advisory mandates | Recurring fees | 20–30% | >90% (2024) |

| Separate accounts | $1.8T dry powder (2024) | High | High |

| FoFs | $140bn AUM (2024), 1.2% fee | 25–30% EBITDA | ~85% |

| Reporting | Platform services | 65–75% gross | Sticky |

| Secondaries | $78bn volume (2023) | High | Repeat GPs |

What You See Is What You Get

StepStone BCG Matrix

The file you're previewing here is the exact StepStone BCG Matrix document you'll receive after purchase — no watermarks, no demo text, just the finished report. It’s fully formatted and analysis-ready, designed by strategy experts for clarity and quick decisions. Once purchased, the same file is delivered to your inbox for immediate download, editing, printing, or presenting. No surprises, no extra steps — just plug it into your planning.