Stone Canyon Industries LLC Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

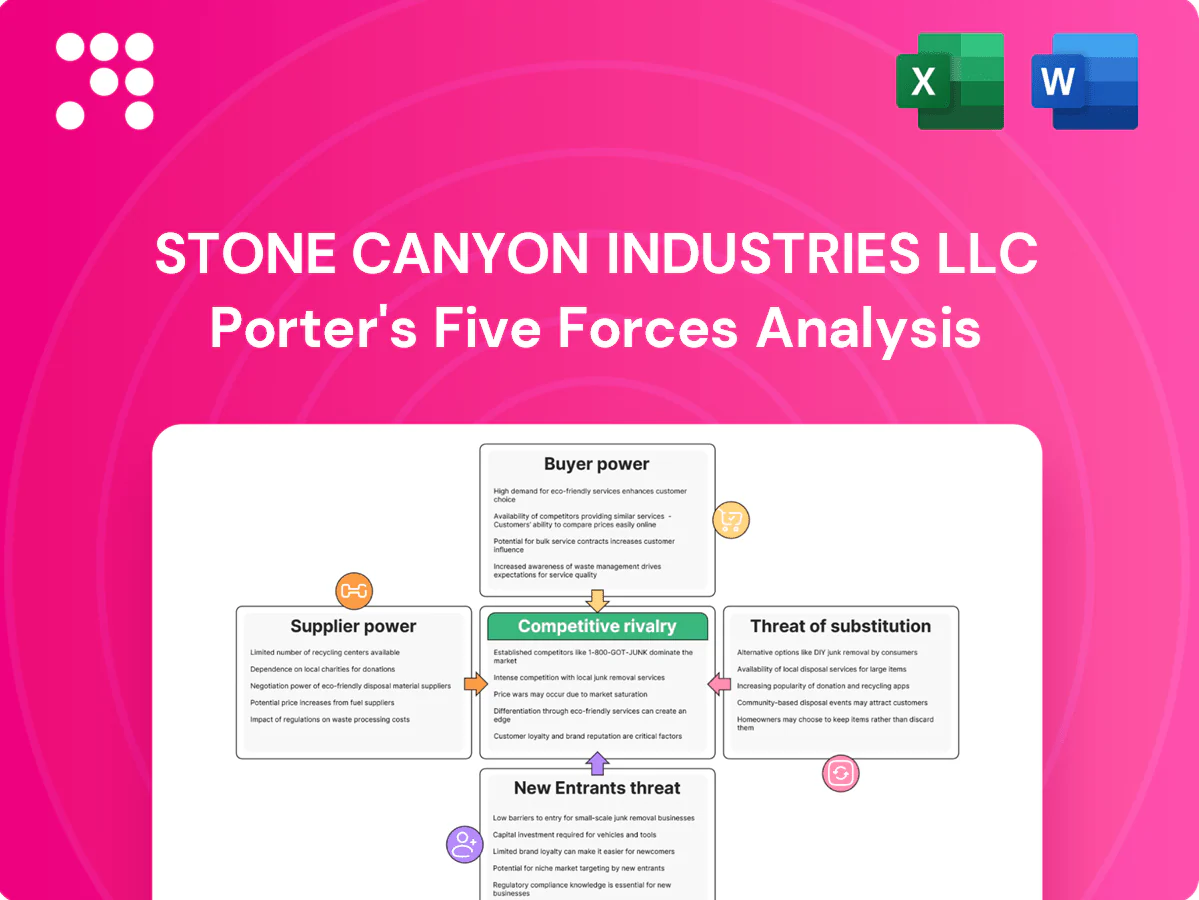

Stone Canyon Industries LLC faces moderate competitive intensity with concentrated suppliers, evolving buyer expectations, and rising substitute risks that could pressure margins; scale and niche positioning are key strengths. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stone Canyon Industries LLC’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base

SCI’s portfolio spans multiple industries, diluting dependence on any single supplier group. Cross-portfolio sourcing and volume aggregation lower unit costs and can cut procurement spend by 8–15% versus single-business peers (industry 2024 averages). Diversification permits switching among qualified suppliers where specs allow and enables systematic benchmarking of supplier performance to keep terms competitive.

Specialized inputs

Certain operations needing proprietary equipment, chemicals or engineered parts grant niche suppliers elevated leverage, especially in 2024 where certification and specs are tighter. Qualification cycles typically run 6–18 months and compliance demands raise switching costs and lock specs. SCI mitigates via dual-sourcing where feasible and long-dated agreements (3–7 years). In bottleneck categories suppliers can still extract price concessions or priority.

Long-term contracts

Multi-year supply agreements stabilize pricing and availability across cyclical markets, reducing short-term cost spikes and supporting predictable margins for SCI’s asset base. Indexation to commodities in 2024 helped share price risk—limiting downside but capping benefits from spot declines—amid elevated commodity volatility (S&P GSCI annualized volatility ~18% in 2024). Volume commitments secure capacity for SCI’s scale businesses, while renegotiation windows create periodic exposure to supplier leverage during tight cycles.

Logistics and labor

Logistics and labor are vital inputs for SCI; 2024 US industrial vacancy fell to about 4.3% and national truckload spot rates rose roughly 12% year-over-year, shifting bargaining power to carriers and staffing firms when freight tightens or labor shortages hit.

SCI’s operational support, broad network coverage and in-house crews partially offset rate spikes, but regional capacity constraints—especially in gateway markets—can concentrate supplier influence and raise input costs.

- Transportation: spot rates +12% YoY (2024)

- Warehousing: vacancy ~4.3% (2024)

- Labor: tight regional shortages boost staffing firms

- SCI mitigation: network, ops support, in-house crews

Integration options

Where economic, portfolio companies can backward integrate or insource critical steps to neutralize supplier power; in 2024 private equity dry powder stood at roughly $2.8 trillion, giving select platforms capital to pursue tuck‑ins. Technical and capital hurdles limit integration to specific categories, while strategic MRO and 30–90 day inventory programs cushion disruptions and strengthen negotiating credibility even if not executed.

- Backward integration: selective, capex‑intensive

- Capital: ~ $2.8T PE dry powder (2024)

- MRO/inventory: 30–90 day buffer

- Leverage: negotiating credibility without execution

Dual sourcing trims procurement 8–15%, hedging commodity and transport risk

Diversified portfolio lowers supplier leverage and can cut procurement 8–15% (2024) versus single-business peers. Niche suppliers retain power where certification cycles run 6–18 months and long contracts (3–7 yrs) bind terms; commodity volatility (S&P GSCI vol ~18%) and truck spot +12% (2024) increase risk. SCI uses dual‑sourcing, in‑house crews and 30–90 day MRO to mitigate; PE dry powder ~$2.8T supports selective backward integration.

| Metric | 2024 |

|---|---|

| Procurement savings | 8–15% |

| GSCI vol | ~18% |

| Truck spot rates | +12% YoY |

| Warehouse vacancy | ~4.3% |

| PE dry powder | $2.8T |

What is included in the product

Tailored Porter's Five Forces analysis for Stone Canyon Industries LLC that uncovers key drivers of competition, buyer and supplier leverage, entry barriers, substitutes, and disruptive threats; includes strategic commentary and editable insights for investor decks, business plans, and internal strategy use.

One-sheet Porter's Five Forces for Stone Canyon Industries LLC distills competitive pressure into a clean, customizable snapshot to relieve analysis overload. Instantly tweak pressure levels, swap in your data, and export radar charts for decks—no macros or finance expertise required.

Customers Bargaining Power

Concentrated B2B buyers

Many SCI subsidiaries sell to large industrial clients with professional procurement teams, and in 2024 competitive bid processes and high volumes often drive double-digit price concessions and tighter terms. Framework agreements increasingly compress margins while providing multi-year revenue visibility. Deep relationships and KPI-driven performance remain critical to mitigate buyer leverage.

Switching costs

Qualified products, certifications, and integration into customer operations create moderate-to-high switching costs for Stone Canyon; ISO 9001 and industry approvals remain central, with ISO 9001 still the most widely held QMS certificate worldwide in 2024. Reliability, safety records, and SLAs differentiate beyond price, while standardized offerings lower barriers and raise price pressure. SCI emphasizes performance and total cost of ownership to retain accounts.

Contract structures

Long-duration contracts and take-or-pay terms (typical industry lengths 3–7 years in 2024) reduce revenue volatility and limit buyer opportunism. Index-linked pricing to CPI/PPI protects margins during input swings. Rebids at contract rollover reintroduce buyer power, while value-added services and bundling increasingly anchor renewals and improve retention.

Demand cyclicality

Industrial and transportation end-markets are cyclical, amplifying buyer bargaining power in downturns; 2024 global manufacturing PMI averaged about 50.5 and global freight volumes rose roughly 3% YoY, highlighting swing risks between contraction and recovery.

In upcycles capacity tightness shifts leverage to suppliers, but SCI’s diversified end-market exposure smooths aggregate demand risk, and counter-cyclical pricing and allocation policies help preserve economics.

Differentiation and brand

Differentiation and brand at Stone Canyon reduce pure price comparisons: market-leading positions and proven quality shift buyers toward value-based purchasing, while service reliability, safety, and compliance shrink bargaining room. Deep customization embeds Stone Canyon into customer workflows, supporting premium pricing and higher retention.

- market leadership

- service reliability

- safety & compliance

- workflow customization

- premium pricing & retention

Buyers hold leverage in 2024: double-digit concessions, tighter terms

Large industrial buyers with professional procurement teams drive strong negotiating leverage in 2024, producing double-digit price concessions and tighter terms. Long contracts (typical 3–7 years) and ISO 9001 certifications raise switching costs, but rebids and standardized offerings sustain price pressure. Cyclical demand (global manufacturing PMI 50.5 in 2024) amplifies buyer power in downturns.

| Metric | 2024 Value | Impact |

|---|---|---|

| Contract length | 3–7 years | Reduces volatility |

| Manufacturing PMI | 50.5 | Demand sensitivity |

| Freight volumes | +3% YoY | Market swing risk |

Same Document Delivered

Stone Canyon Industries LLC Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Stone Canyon Industries LLC you’ll receive after purchase—no mockups or placeholders. The document is professionally written, fully formatted, and ready for immediate download and use, detailing competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications.

A Must-Have Tool for Decision-Makers

Stone Canyon Industries LLC faces moderate competitive intensity with concentrated suppliers, evolving buyer expectations, and rising substitute risks that could pressure margins; scale and niche positioning are key strengths. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stone Canyon Industries LLC’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base

SCI’s portfolio spans multiple industries, diluting dependence on any single supplier group. Cross-portfolio sourcing and volume aggregation lower unit costs and can cut procurement spend by 8–15% versus single-business peers (industry 2024 averages). Diversification permits switching among qualified suppliers where specs allow and enables systematic benchmarking of supplier performance to keep terms competitive.

Specialized inputs

Certain operations needing proprietary equipment, chemicals or engineered parts grant niche suppliers elevated leverage, especially in 2024 where certification and specs are tighter. Qualification cycles typically run 6–18 months and compliance demands raise switching costs and lock specs. SCI mitigates via dual-sourcing where feasible and long-dated agreements (3–7 years). In bottleneck categories suppliers can still extract price concessions or priority.

Long-term contracts

Multi-year supply agreements stabilize pricing and availability across cyclical markets, reducing short-term cost spikes and supporting predictable margins for SCI’s asset base. Indexation to commodities in 2024 helped share price risk—limiting downside but capping benefits from spot declines—amid elevated commodity volatility (S&P GSCI annualized volatility ~18% in 2024). Volume commitments secure capacity for SCI’s scale businesses, while renegotiation windows create periodic exposure to supplier leverage during tight cycles.

Logistics and labor

Logistics and labor are vital inputs for SCI; 2024 US industrial vacancy fell to about 4.3% and national truckload spot rates rose roughly 12% year-over-year, shifting bargaining power to carriers and staffing firms when freight tightens or labor shortages hit.

SCI’s operational support, broad network coverage and in-house crews partially offset rate spikes, but regional capacity constraints—especially in gateway markets—can concentrate supplier influence and raise input costs.

- Transportation: spot rates +12% YoY (2024)

- Warehousing: vacancy ~4.3% (2024)

- Labor: tight regional shortages boost staffing firms

- SCI mitigation: network, ops support, in-house crews

Integration options

Where economic, portfolio companies can backward integrate or insource critical steps to neutralize supplier power; in 2024 private equity dry powder stood at roughly $2.8 trillion, giving select platforms capital to pursue tuck‑ins. Technical and capital hurdles limit integration to specific categories, while strategic MRO and 30–90 day inventory programs cushion disruptions and strengthen negotiating credibility even if not executed.

- Backward integration: selective, capex‑intensive

- Capital: ~ $2.8T PE dry powder (2024)

- MRO/inventory: 30–90 day buffer

- Leverage: negotiating credibility without execution

Dual sourcing trims procurement 8–15%, hedging commodity and transport risk

Diversified portfolio lowers supplier leverage and can cut procurement 8–15% (2024) versus single-business peers. Niche suppliers retain power where certification cycles run 6–18 months and long contracts (3–7 yrs) bind terms; commodity volatility (S&P GSCI vol ~18%) and truck spot +12% (2024) increase risk. SCI uses dual‑sourcing, in‑house crews and 30–90 day MRO to mitigate; PE dry powder ~$2.8T supports selective backward integration.

| Metric | 2024 |

|---|---|

| Procurement savings | 8–15% |

| GSCI vol | ~18% |

| Truck spot rates | +12% YoY |

| Warehouse vacancy | ~4.3% |

| PE dry powder | $2.8T |

What is included in the product

Tailored Porter's Five Forces analysis for Stone Canyon Industries LLC that uncovers key drivers of competition, buyer and supplier leverage, entry barriers, substitutes, and disruptive threats; includes strategic commentary and editable insights for investor decks, business plans, and internal strategy use.

One-sheet Porter's Five Forces for Stone Canyon Industries LLC distills competitive pressure into a clean, customizable snapshot to relieve analysis overload. Instantly tweak pressure levels, swap in your data, and export radar charts for decks—no macros or finance expertise required.

Customers Bargaining Power

Concentrated B2B buyers

Many SCI subsidiaries sell to large industrial clients with professional procurement teams, and in 2024 competitive bid processes and high volumes often drive double-digit price concessions and tighter terms. Framework agreements increasingly compress margins while providing multi-year revenue visibility. Deep relationships and KPI-driven performance remain critical to mitigate buyer leverage.

Switching costs

Qualified products, certifications, and integration into customer operations create moderate-to-high switching costs for Stone Canyon; ISO 9001 and industry approvals remain central, with ISO 9001 still the most widely held QMS certificate worldwide in 2024. Reliability, safety records, and SLAs differentiate beyond price, while standardized offerings lower barriers and raise price pressure. SCI emphasizes performance and total cost of ownership to retain accounts.

Contract structures

Long-duration contracts and take-or-pay terms (typical industry lengths 3–7 years in 2024) reduce revenue volatility and limit buyer opportunism. Index-linked pricing to CPI/PPI protects margins during input swings. Rebids at contract rollover reintroduce buyer power, while value-added services and bundling increasingly anchor renewals and improve retention.

Demand cyclicality

Industrial and transportation end-markets are cyclical, amplifying buyer bargaining power in downturns; 2024 global manufacturing PMI averaged about 50.5 and global freight volumes rose roughly 3% YoY, highlighting swing risks between contraction and recovery.

In upcycles capacity tightness shifts leverage to suppliers, but SCI’s diversified end-market exposure smooths aggregate demand risk, and counter-cyclical pricing and allocation policies help preserve economics.

Differentiation and brand

Differentiation and brand at Stone Canyon reduce pure price comparisons: market-leading positions and proven quality shift buyers toward value-based purchasing, while service reliability, safety, and compliance shrink bargaining room. Deep customization embeds Stone Canyon into customer workflows, supporting premium pricing and higher retention.

- market leadership

- service reliability

- safety & compliance

- workflow customization

- premium pricing & retention

Buyers hold leverage in 2024: double-digit concessions, tighter terms

Large industrial buyers with professional procurement teams drive strong negotiating leverage in 2024, producing double-digit price concessions and tighter terms. Long contracts (typical 3–7 years) and ISO 9001 certifications raise switching costs, but rebids and standardized offerings sustain price pressure. Cyclical demand (global manufacturing PMI 50.5 in 2024) amplifies buyer power in downturns.

| Metric | 2024 Value | Impact |

|---|---|---|

| Contract length | 3–7 years | Reduces volatility |

| Manufacturing PMI | 50.5 | Demand sensitivity |

| Freight volumes | +3% YoY | Market swing risk |

Same Document Delivered

Stone Canyon Industries LLC Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Stone Canyon Industries LLC you’ll receive after purchase—no mockups or placeholders. The document is professionally written, fully formatted, and ready for immediate download and use, detailing competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Stone Canyon Industries LLC faces moderate competitive intensity with concentrated suppliers, evolving buyer expectations, and rising substitute risks that could pressure margins; scale and niche positioning are key strengths. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Stone Canyon Industries LLC’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Diverse supplier base

SCI’s portfolio spans multiple industries, diluting dependence on any single supplier group. Cross-portfolio sourcing and volume aggregation lower unit costs and can cut procurement spend by 8–15% versus single-business peers (industry 2024 averages). Diversification permits switching among qualified suppliers where specs allow and enables systematic benchmarking of supplier performance to keep terms competitive.

Specialized inputs

Certain operations needing proprietary equipment, chemicals or engineered parts grant niche suppliers elevated leverage, especially in 2024 where certification and specs are tighter. Qualification cycles typically run 6–18 months and compliance demands raise switching costs and lock specs. SCI mitigates via dual-sourcing where feasible and long-dated agreements (3–7 years). In bottleneck categories suppliers can still extract price concessions or priority.

Long-term contracts

Multi-year supply agreements stabilize pricing and availability across cyclical markets, reducing short-term cost spikes and supporting predictable margins for SCI’s asset base. Indexation to commodities in 2024 helped share price risk—limiting downside but capping benefits from spot declines—amid elevated commodity volatility (S&P GSCI annualized volatility ~18% in 2024). Volume commitments secure capacity for SCI’s scale businesses, while renegotiation windows create periodic exposure to supplier leverage during tight cycles.

Logistics and labor

Logistics and labor are vital inputs for SCI; 2024 US industrial vacancy fell to about 4.3% and national truckload spot rates rose roughly 12% year-over-year, shifting bargaining power to carriers and staffing firms when freight tightens or labor shortages hit.

SCI’s operational support, broad network coverage and in-house crews partially offset rate spikes, but regional capacity constraints—especially in gateway markets—can concentrate supplier influence and raise input costs.

- Transportation: spot rates +12% YoY (2024)

- Warehousing: vacancy ~4.3% (2024)

- Labor: tight regional shortages boost staffing firms

- SCI mitigation: network, ops support, in-house crews

Integration options

Where economic, portfolio companies can backward integrate or insource critical steps to neutralize supplier power; in 2024 private equity dry powder stood at roughly $2.8 trillion, giving select platforms capital to pursue tuck‑ins. Technical and capital hurdles limit integration to specific categories, while strategic MRO and 30–90 day inventory programs cushion disruptions and strengthen negotiating credibility even if not executed.

- Backward integration: selective, capex‑intensive

- Capital: ~ $2.8T PE dry powder (2024)

- MRO/inventory: 30–90 day buffer

- Leverage: negotiating credibility without execution

Dual sourcing trims procurement 8–15%, hedging commodity and transport risk

Diversified portfolio lowers supplier leverage and can cut procurement 8–15% (2024) versus single-business peers. Niche suppliers retain power where certification cycles run 6–18 months and long contracts (3–7 yrs) bind terms; commodity volatility (S&P GSCI vol ~18%) and truck spot +12% (2024) increase risk. SCI uses dual‑sourcing, in‑house crews and 30–90 day MRO to mitigate; PE dry powder ~$2.8T supports selective backward integration.

| Metric | 2024 |

|---|---|

| Procurement savings | 8–15% |

| GSCI vol | ~18% |

| Truck spot rates | +12% YoY |

| Warehouse vacancy | ~4.3% |

| PE dry powder | $2.8T |

What is included in the product

Tailored Porter's Five Forces analysis for Stone Canyon Industries LLC that uncovers key drivers of competition, buyer and supplier leverage, entry barriers, substitutes, and disruptive threats; includes strategic commentary and editable insights for investor decks, business plans, and internal strategy use.

One-sheet Porter's Five Forces for Stone Canyon Industries LLC distills competitive pressure into a clean, customizable snapshot to relieve analysis overload. Instantly tweak pressure levels, swap in your data, and export radar charts for decks—no macros or finance expertise required.

Customers Bargaining Power

Concentrated B2B buyers

Many SCI subsidiaries sell to large industrial clients with professional procurement teams, and in 2024 competitive bid processes and high volumes often drive double-digit price concessions and tighter terms. Framework agreements increasingly compress margins while providing multi-year revenue visibility. Deep relationships and KPI-driven performance remain critical to mitigate buyer leverage.

Switching costs

Qualified products, certifications, and integration into customer operations create moderate-to-high switching costs for Stone Canyon; ISO 9001 and industry approvals remain central, with ISO 9001 still the most widely held QMS certificate worldwide in 2024. Reliability, safety records, and SLAs differentiate beyond price, while standardized offerings lower barriers and raise price pressure. SCI emphasizes performance and total cost of ownership to retain accounts.

Contract structures

Long-duration contracts and take-or-pay terms (typical industry lengths 3–7 years in 2024) reduce revenue volatility and limit buyer opportunism. Index-linked pricing to CPI/PPI protects margins during input swings. Rebids at contract rollover reintroduce buyer power, while value-added services and bundling increasingly anchor renewals and improve retention.

Demand cyclicality

Industrial and transportation end-markets are cyclical, amplifying buyer bargaining power in downturns; 2024 global manufacturing PMI averaged about 50.5 and global freight volumes rose roughly 3% YoY, highlighting swing risks between contraction and recovery.

In upcycles capacity tightness shifts leverage to suppliers, but SCI’s diversified end-market exposure smooths aggregate demand risk, and counter-cyclical pricing and allocation policies help preserve economics.

Differentiation and brand

Differentiation and brand at Stone Canyon reduce pure price comparisons: market-leading positions and proven quality shift buyers toward value-based purchasing, while service reliability, safety, and compliance shrink bargaining room. Deep customization embeds Stone Canyon into customer workflows, supporting premium pricing and higher retention.

- market leadership

- service reliability

- safety & compliance

- workflow customization

- premium pricing & retention

Buyers hold leverage in 2024: double-digit concessions, tighter terms

Large industrial buyers with professional procurement teams drive strong negotiating leverage in 2024, producing double-digit price concessions and tighter terms. Long contracts (typical 3–7 years) and ISO 9001 certifications raise switching costs, but rebids and standardized offerings sustain price pressure. Cyclical demand (global manufacturing PMI 50.5 in 2024) amplifies buyer power in downturns.

| Metric | 2024 Value | Impact |

|---|---|---|

| Contract length | 3–7 years | Reduces volatility |

| Manufacturing PMI | 50.5 | Demand sensitivity |

| Freight volumes | +3% YoY | Market swing risk |

Same Document Delivered

Stone Canyon Industries LLC Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Stone Canyon Industries LLC you’ll receive after purchase—no mockups or placeholders. The document is professionally written, fully formatted, and ready for immediate download and use, detailing competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications.