StoneX Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

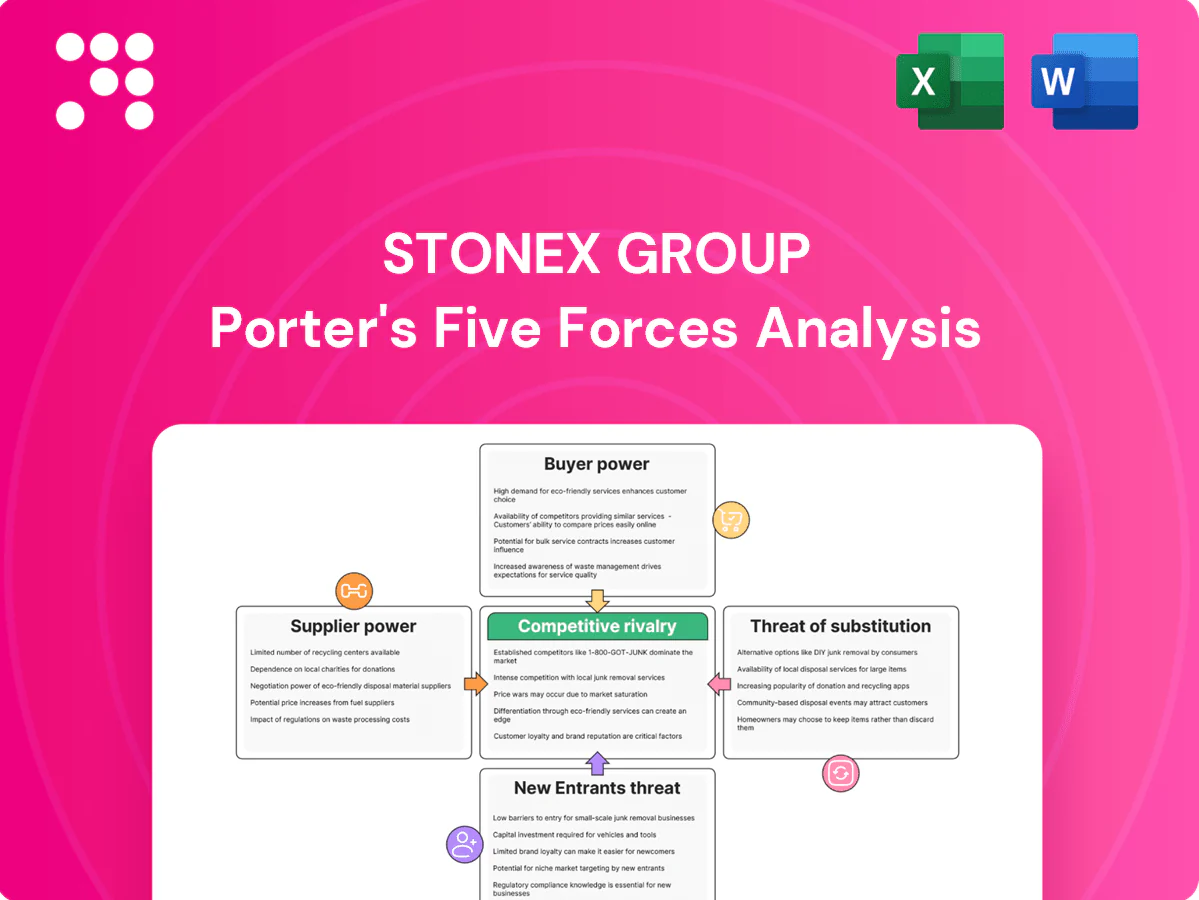

StoneX Group faces varied competitive pressures—from concentrated buyer power and regulatory demands to moderate threat of new entrants and disruptive substitutes—shaping margins and strategic choices. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to explore StoneX’s competitive dynamics and actionable recommendations in detail.

Suppliers Bargaining Power

Exchange and clearing venues

StoneX depends on regulated exchanges and clearinghouses for market access and settlement, and concentration among major venues gives those suppliers leverage over fees and rule changes. Mandatory margining and clearing standards further increase supplier bargaining power, though StoneX’s multi-venue connectivity and membership across major exchanges provide partial substitution and routing flexibility. Volume commitments and membership status allow StoneX to negotiate fee discounts and rebate arrangements to mitigate fee pressure.

Liquidity providers and banks

Prime brokers, OTC dealers and banks supply lines, credit and pricing; the 2023–24 tightening cycle—with Fed funds near 5.25–5.50%—pushed funding costs and dealer spreads higher, raising StoneX’s cost base. Diversified counterparties and strong risk controls improve bargaining position. Deeper relationships and higher-quality collateral materially sharpen negotiation levers.

Market data and infrastructure vendors

Proprietary data feeds, analytics and co-location create high stickiness—Bloomberg’s ~325,000 terminals and microsecond latency needs make switching costly; co‑location rack fees commonly run $5,000–$20,000/month. Vendor licensing and lock‑in can push market data spend into double digits of operating budgets, so StoneX negotiates enterprise agreements and deploys open‑source/internal tools where feasible, though performance SLAs limit easy substitution.

Technology platforms and connectivity

Order management systems, APIs and connectivity networks underpin execution and create integration complexity that raises switching costs in suppliers’ favor; industry-grade SLAs target 99.99% uptime, amplifying supplier leverage during integration friction. StoneX’s in-house engineering and modular architecture reduce dependence on single vendors, while multi-provider redundancy limits outage and pricing risk.

- Integration complexity → higher switching costs

- 99.99% SLA norms increase supplier leverage

- In-house engineering lowers vendor dependence

- Redundancy across providers cuts outage/pricing risk

Regulatory and compliance services

Regulatory and compliance services function as quasi-suppliers for StoneX, with 2024 rule shifts like the US BOI reporting (effective Jan 2024) and the EU AMLA operationalizing new standards driving non-negotiable cost increases for reporting utilities, KYC/AML tools and audits.

Scale enables StoneX to absorb fixed compliance spend and negotiate volume pricing, while consistent controls reduce remediation and penalty risk.

- BOI reporting: US effective Jan 2024

- EU AMLA: operational 2024

- Scale cuts per-unit compliance cost

- Consistent controls lower fines/remediation

Margining, co-location and sticky data raise supplier leverage; funding at 5.25–5.50%

Concentrated exchanges/clearinghouses and mandatory margining give suppliers pricing leverage, though StoneX’s multi-venue memberships and volume discounts mitigate fee pressure. Funding squeeze (Fed funds ~5.25–5.50% in 2023–24) raised dealer spreads; diversified counterparties and strong collateral improve negotiation power. Sticky market data, co‑location (325,000 Bloomberg terminals; $5k–$20k/mo racks) and 99.99% SLAs raise switching costs, offset by in-house engineering.

| Supplier | Leverage | 2024 metric |

|---|---|---|

| Exchanges | High | Fee rebates, memberships |

| Prime brokers | Medium | Fed funds 5.25–5.50% |

| Data/colocation | High | 325k terminals; $5k–$20k/mo |

What is included in the product

Provides a tailored Porter's Five Forces analysis for StoneX Group, uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory risks, while identifying disruptive trends and strategic levers to protect market share and pricing power.

A clear, one-sheet summary of StoneX Group's five competitive forces—perfect for quick strategic decisions and investor briefings; customize pressure levels with live market data and export-ready visuals for decks or boardrooms.

Customers Bargaining Power

Diversified institutional client base

Diversified institutional clients—corporates, financial institutions and professional traders—can readily benchmark fees across brokers, leading larger accounts to use RFPs and volume commitments to compress pricing. StoneX offsets pressure by packaging execution, clearing, research and bespoke risk solutions into bundled contracts. Strong relationship tenure and proven execution quality often shift decisions away from price alone, preserving margins for tailored services.

Multi-homing and low differentiation

Clients often multi-home—industry surveys show roughly 70% of active institutional traders use multiple brokers—so comparable execution and clearing raise buyer leverage; StoneX reported 2024 net revenue of $1.6 billion and operates in 38 countries, competing on breadth across asset classes and global access. Integration, consolidated reporting and API connectivity increase switching frictions, preserving client share despite low product differentiation.

Price sensitivity in commoditized flows

High-frequency, standardized flows face tight spreads often below 1 basis point, driving clients to demand pass-through of exchange rebates (industry rebates commonly around $0.001–$0.003 per share) and full fee transparency; StoneX defends margins by selling value-added intelligence and hedging advisory that industry data show can command premium pricing of roughly 10–30% versus commoditized execution. Tiered pricing and SLA differentiation segment willingness to pay, increasing ARPU among top-tier clients.

Switching costs and integration

Onboarding, KYC, and workflow integration create moderate frictions for StoneX clients in 2024; complex hedging program migrations impose meaningful costs, raising client retention. StoneX leverages tooling, APIs and data portability to embed deeply, and high service reliability lowers propensity to switch.

- Onboarding friction: moderate

- Migration cost: meaningful for complex hedging

- Retention levers: APIs, tooling, data portability

- Reliability: reduces switching

Demand cyclicality and risk appetite

Demand cyclicality drives client volumes at StoneX (NASDAQ: SNEX), with trading and commodity flows rising sharply during stress and falling in calm markets; buyers trim spend in low-volatility periods while demanding liquidity and margin capacity in spikes. StoneX’s diversified product mix and risk-management services—supporting clients across 65+ countries—help smooth revenue swings and keep engagement beyond trading peaks.

- NASDAQ: SNEX

- 65+ countries served

- Diversified product mix mitigates cyclicality

- Risk solutions sustain off-peak engagement

Bundled execution, SLAs and APIs protect $1.6B revenue amid 70% multi-homing

Institutional clients have high bargaining power—~70% multi-home and frequent fee benchmarking—pressuring spreads and commissions. StoneX (2024 net revenue $1.6B) defends via bundled execution, clearing, research and APIs that raise switching costs. Tiered SLAs, risk solutions and integrations preserve margins despite commoditized high-frequency flows.

| Metric | Value |

|---|---|

| 2024 net revenue | $1.6B |

| Multi-home rate | ~70% |

| Geographic reach | 65+ countries |

Same Document Delivered

StoneX Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of StoneX Group you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted and ready for download and use the moment you buy. You’re looking at the actual, final deliverable: complete, professional, and ready to inform your strategic or investment decisions.

From Overview to Strategy Blueprint

StoneX Group faces varied competitive pressures—from concentrated buyer power and regulatory demands to moderate threat of new entrants and disruptive substitutes—shaping margins and strategic choices. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to explore StoneX’s competitive dynamics and actionable recommendations in detail.

Suppliers Bargaining Power

Exchange and clearing venues

StoneX depends on regulated exchanges and clearinghouses for market access and settlement, and concentration among major venues gives those suppliers leverage over fees and rule changes. Mandatory margining and clearing standards further increase supplier bargaining power, though StoneX’s multi-venue connectivity and membership across major exchanges provide partial substitution and routing flexibility. Volume commitments and membership status allow StoneX to negotiate fee discounts and rebate arrangements to mitigate fee pressure.

Liquidity providers and banks

Prime brokers, OTC dealers and banks supply lines, credit and pricing; the 2023–24 tightening cycle—with Fed funds near 5.25–5.50%—pushed funding costs and dealer spreads higher, raising StoneX’s cost base. Diversified counterparties and strong risk controls improve bargaining position. Deeper relationships and higher-quality collateral materially sharpen negotiation levers.

Market data and infrastructure vendors

Proprietary data feeds, analytics and co-location create high stickiness—Bloomberg’s ~325,000 terminals and microsecond latency needs make switching costly; co‑location rack fees commonly run $5,000–$20,000/month. Vendor licensing and lock‑in can push market data spend into double digits of operating budgets, so StoneX negotiates enterprise agreements and deploys open‑source/internal tools where feasible, though performance SLAs limit easy substitution.

Technology platforms and connectivity

Order management systems, APIs and connectivity networks underpin execution and create integration complexity that raises switching costs in suppliers’ favor; industry-grade SLAs target 99.99% uptime, amplifying supplier leverage during integration friction. StoneX’s in-house engineering and modular architecture reduce dependence on single vendors, while multi-provider redundancy limits outage and pricing risk.

- Integration complexity → higher switching costs

- 99.99% SLA norms increase supplier leverage

- In-house engineering lowers vendor dependence

- Redundancy across providers cuts outage/pricing risk

Regulatory and compliance services

Regulatory and compliance services function as quasi-suppliers for StoneX, with 2024 rule shifts like the US BOI reporting (effective Jan 2024) and the EU AMLA operationalizing new standards driving non-negotiable cost increases for reporting utilities, KYC/AML tools and audits.

Scale enables StoneX to absorb fixed compliance spend and negotiate volume pricing, while consistent controls reduce remediation and penalty risk.

- BOI reporting: US effective Jan 2024

- EU AMLA: operational 2024

- Scale cuts per-unit compliance cost

- Consistent controls lower fines/remediation

Margining, co-location and sticky data raise supplier leverage; funding at 5.25–5.50%

Concentrated exchanges/clearinghouses and mandatory margining give suppliers pricing leverage, though StoneX’s multi-venue memberships and volume discounts mitigate fee pressure. Funding squeeze (Fed funds ~5.25–5.50% in 2023–24) raised dealer spreads; diversified counterparties and strong collateral improve negotiation power. Sticky market data, co‑location (325,000 Bloomberg terminals; $5k–$20k/mo racks) and 99.99% SLAs raise switching costs, offset by in-house engineering.

| Supplier | Leverage | 2024 metric |

|---|---|---|

| Exchanges | High | Fee rebates, memberships |

| Prime brokers | Medium | Fed funds 5.25–5.50% |

| Data/colocation | High | 325k terminals; $5k–$20k/mo |

What is included in the product

Provides a tailored Porter's Five Forces analysis for StoneX Group, uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory risks, while identifying disruptive trends and strategic levers to protect market share and pricing power.

A clear, one-sheet summary of StoneX Group's five competitive forces—perfect for quick strategic decisions and investor briefings; customize pressure levels with live market data and export-ready visuals for decks or boardrooms.

Customers Bargaining Power

Diversified institutional client base

Diversified institutional clients—corporates, financial institutions and professional traders—can readily benchmark fees across brokers, leading larger accounts to use RFPs and volume commitments to compress pricing. StoneX offsets pressure by packaging execution, clearing, research and bespoke risk solutions into bundled contracts. Strong relationship tenure and proven execution quality often shift decisions away from price alone, preserving margins for tailored services.

Multi-homing and low differentiation

Clients often multi-home—industry surveys show roughly 70% of active institutional traders use multiple brokers—so comparable execution and clearing raise buyer leverage; StoneX reported 2024 net revenue of $1.6 billion and operates in 38 countries, competing on breadth across asset classes and global access. Integration, consolidated reporting and API connectivity increase switching frictions, preserving client share despite low product differentiation.

Price sensitivity in commoditized flows

High-frequency, standardized flows face tight spreads often below 1 basis point, driving clients to demand pass-through of exchange rebates (industry rebates commonly around $0.001–$0.003 per share) and full fee transparency; StoneX defends margins by selling value-added intelligence and hedging advisory that industry data show can command premium pricing of roughly 10–30% versus commoditized execution. Tiered pricing and SLA differentiation segment willingness to pay, increasing ARPU among top-tier clients.

Switching costs and integration

Onboarding, KYC, and workflow integration create moderate frictions for StoneX clients in 2024; complex hedging program migrations impose meaningful costs, raising client retention. StoneX leverages tooling, APIs and data portability to embed deeply, and high service reliability lowers propensity to switch.

- Onboarding friction: moderate

- Migration cost: meaningful for complex hedging

- Retention levers: APIs, tooling, data portability

- Reliability: reduces switching

Demand cyclicality and risk appetite

Demand cyclicality drives client volumes at StoneX (NASDAQ: SNEX), with trading and commodity flows rising sharply during stress and falling in calm markets; buyers trim spend in low-volatility periods while demanding liquidity and margin capacity in spikes. StoneX’s diversified product mix and risk-management services—supporting clients across 65+ countries—help smooth revenue swings and keep engagement beyond trading peaks.

- NASDAQ: SNEX

- 65+ countries served

- Diversified product mix mitigates cyclicality

- Risk solutions sustain off-peak engagement

Bundled execution, SLAs and APIs protect $1.6B revenue amid 70% multi-homing

Institutional clients have high bargaining power—~70% multi-home and frequent fee benchmarking—pressuring spreads and commissions. StoneX (2024 net revenue $1.6B) defends via bundled execution, clearing, research and APIs that raise switching costs. Tiered SLAs, risk solutions and integrations preserve margins despite commoditized high-frequency flows.

| Metric | Value |

|---|---|

| 2024 net revenue | $1.6B |

| Multi-home rate | ~70% |

| Geographic reach | 65+ countries |

Same Document Delivered

StoneX Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of StoneX Group you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted and ready for download and use the moment you buy. You’re looking at the actual, final deliverable: complete, professional, and ready to inform your strategic or investment decisions.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

StoneX Group faces varied competitive pressures—from concentrated buyer power and regulatory demands to moderate threat of new entrants and disruptive substitutes—shaping margins and strategic choices. This snapshot highlights key tensions but omits force-by-force ratings, visuals, and tactical implications. Unlock the full Porter's Five Forces Analysis to explore StoneX’s competitive dynamics and actionable recommendations in detail.

Suppliers Bargaining Power

Exchange and clearing venues

StoneX depends on regulated exchanges and clearinghouses for market access and settlement, and concentration among major venues gives those suppliers leverage over fees and rule changes. Mandatory margining and clearing standards further increase supplier bargaining power, though StoneX’s multi-venue connectivity and membership across major exchanges provide partial substitution and routing flexibility. Volume commitments and membership status allow StoneX to negotiate fee discounts and rebate arrangements to mitigate fee pressure.

Liquidity providers and banks

Prime brokers, OTC dealers and banks supply lines, credit and pricing; the 2023–24 tightening cycle—with Fed funds near 5.25–5.50%—pushed funding costs and dealer spreads higher, raising StoneX’s cost base. Diversified counterparties and strong risk controls improve bargaining position. Deeper relationships and higher-quality collateral materially sharpen negotiation levers.

Market data and infrastructure vendors

Proprietary data feeds, analytics and co-location create high stickiness—Bloomberg’s ~325,000 terminals and microsecond latency needs make switching costly; co‑location rack fees commonly run $5,000–$20,000/month. Vendor licensing and lock‑in can push market data spend into double digits of operating budgets, so StoneX negotiates enterprise agreements and deploys open‑source/internal tools where feasible, though performance SLAs limit easy substitution.

Technology platforms and connectivity

Order management systems, APIs and connectivity networks underpin execution and create integration complexity that raises switching costs in suppliers’ favor; industry-grade SLAs target 99.99% uptime, amplifying supplier leverage during integration friction. StoneX’s in-house engineering and modular architecture reduce dependence on single vendors, while multi-provider redundancy limits outage and pricing risk.

- Integration complexity → higher switching costs

- 99.99% SLA norms increase supplier leverage

- In-house engineering lowers vendor dependence

- Redundancy across providers cuts outage/pricing risk

Regulatory and compliance services

Regulatory and compliance services function as quasi-suppliers for StoneX, with 2024 rule shifts like the US BOI reporting (effective Jan 2024) and the EU AMLA operationalizing new standards driving non-negotiable cost increases for reporting utilities, KYC/AML tools and audits.

Scale enables StoneX to absorb fixed compliance spend and negotiate volume pricing, while consistent controls reduce remediation and penalty risk.

- BOI reporting: US effective Jan 2024

- EU AMLA: operational 2024

- Scale cuts per-unit compliance cost

- Consistent controls lower fines/remediation

Margining, co-location and sticky data raise supplier leverage; funding at 5.25–5.50%

Concentrated exchanges/clearinghouses and mandatory margining give suppliers pricing leverage, though StoneX’s multi-venue memberships and volume discounts mitigate fee pressure. Funding squeeze (Fed funds ~5.25–5.50% in 2023–24) raised dealer spreads; diversified counterparties and strong collateral improve negotiation power. Sticky market data, co‑location (325,000 Bloomberg terminals; $5k–$20k/mo racks) and 99.99% SLAs raise switching costs, offset by in-house engineering.

| Supplier | Leverage | 2024 metric |

|---|---|---|

| Exchanges | High | Fee rebates, memberships |

| Prime brokers | Medium | Fed funds 5.25–5.50% |

| Data/colocation | High | 325k terminals; $5k–$20k/mo |

What is included in the product

Provides a tailored Porter's Five Forces analysis for StoneX Group, uncovering competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and regulatory risks, while identifying disruptive trends and strategic levers to protect market share and pricing power.

A clear, one-sheet summary of StoneX Group's five competitive forces—perfect for quick strategic decisions and investor briefings; customize pressure levels with live market data and export-ready visuals for decks or boardrooms.

Customers Bargaining Power

Diversified institutional client base

Diversified institutional clients—corporates, financial institutions and professional traders—can readily benchmark fees across brokers, leading larger accounts to use RFPs and volume commitments to compress pricing. StoneX offsets pressure by packaging execution, clearing, research and bespoke risk solutions into bundled contracts. Strong relationship tenure and proven execution quality often shift decisions away from price alone, preserving margins for tailored services.

Multi-homing and low differentiation

Clients often multi-home—industry surveys show roughly 70% of active institutional traders use multiple brokers—so comparable execution and clearing raise buyer leverage; StoneX reported 2024 net revenue of $1.6 billion and operates in 38 countries, competing on breadth across asset classes and global access. Integration, consolidated reporting and API connectivity increase switching frictions, preserving client share despite low product differentiation.

Price sensitivity in commoditized flows

High-frequency, standardized flows face tight spreads often below 1 basis point, driving clients to demand pass-through of exchange rebates (industry rebates commonly around $0.001–$0.003 per share) and full fee transparency; StoneX defends margins by selling value-added intelligence and hedging advisory that industry data show can command premium pricing of roughly 10–30% versus commoditized execution. Tiered pricing and SLA differentiation segment willingness to pay, increasing ARPU among top-tier clients.

Switching costs and integration

Onboarding, KYC, and workflow integration create moderate frictions for StoneX clients in 2024; complex hedging program migrations impose meaningful costs, raising client retention. StoneX leverages tooling, APIs and data portability to embed deeply, and high service reliability lowers propensity to switch.

- Onboarding friction: moderate

- Migration cost: meaningful for complex hedging

- Retention levers: APIs, tooling, data portability

- Reliability: reduces switching

Demand cyclicality and risk appetite

Demand cyclicality drives client volumes at StoneX (NASDAQ: SNEX), with trading and commodity flows rising sharply during stress and falling in calm markets; buyers trim spend in low-volatility periods while demanding liquidity and margin capacity in spikes. StoneX’s diversified product mix and risk-management services—supporting clients across 65+ countries—help smooth revenue swings and keep engagement beyond trading peaks.

- NASDAQ: SNEX

- 65+ countries served

- Diversified product mix mitigates cyclicality

- Risk solutions sustain off-peak engagement

Bundled execution, SLAs and APIs protect $1.6B revenue amid 70% multi-homing

Institutional clients have high bargaining power—~70% multi-home and frequent fee benchmarking—pressuring spreads and commissions. StoneX (2024 net revenue $1.6B) defends via bundled execution, clearing, research and APIs that raise switching costs. Tiered SLAs, risk solutions and integrations preserve margins despite commoditized high-frequency flows.

| Metric | Value |

|---|---|

| 2024 net revenue | $1.6B |

| Multi-home rate | ~70% |

| Geographic reach | 65+ countries |

Same Document Delivered

StoneX Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of StoneX Group you'll receive immediately after purchase—no placeholders or mockups. The document displayed is fully formatted and ready for download and use the moment you buy. You’re looking at the actual, final deliverable: complete, professional, and ready to inform your strategic or investment decisions.