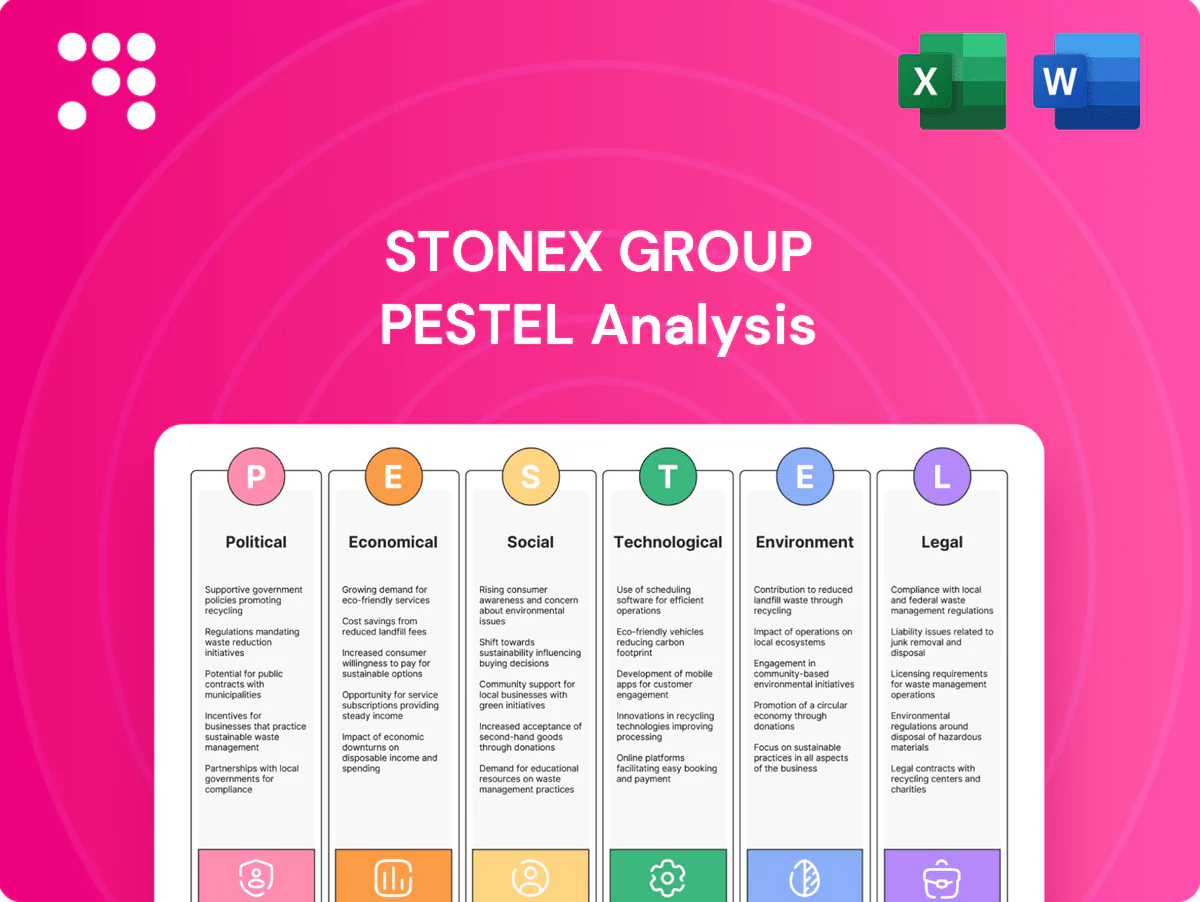

StoneX Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political, economic, social, technological, legal and environmental forces are reshaping StoneX Group’s prospects in our concise PESTLE overview; this 3–5 sentence snapshot highlights key risks and opportunities—purchase the full analysis for a complete, actionable briefing ready for strategy or investment use.

Political factors

Geopolitical risk and sanctions

Volatility from conflicts and sanctions reshapes commodity and FX flows that StoneX intermediates, affecting markets with global FX turnover of about 7.5 trillion USD per day (BIS 2022) and oil flows near 100 million barrels/day. Rapid rule changes can restrict counterparties and instruments, altering revenue mix and raising compliance costs. Proactive sanctions screening and rerouting liquidity are critical operational controls. Diversified geography helps buffer localized shocks.

Trade policy and tariffs

Shifts in tariffs and export controls, such as US Section 301 measures covering about $370 billion of Chinese imports, materially alter hedging demand for commodities and currencies. Clients exposed to fragmented supply chains increasingly seek risk management, boosting clearing and execution volumes for brokers. Policy fragmentation raises basis risks across venues, widening cross-venue spreads. StoneX can monetize advisory and structured hedges to bridge these policy gaps.

Government support for financial infrastructure

National priorities on market development determine clearing access and licensing corridors, affecting StoneX's entry timelines and fee structures. Public investment in payment rails and CCPs expands addressable flow; BIS data show over 70% of standardized OTC derivatives were centrally cleared as of 2024. Active engagement in policy consultations influences microstructure rules, while alignment with development banks—which committed more than $100 billion annually to MDB programs in 2023–24—opens emerging market corridors.

Emerging market political stability

Political turnover in emerging markets can trigger capital controls, tax changes and restricted market access, forcing firms like StoneX to adapt pricing and liquidity; MSCI Emerging Markets represented about 11% of global equity markets in 2024, underscoring material exposure. Local volatility tends to increase hedging volumes but elevates credit and settlement risk; robust local partnerships and on‑the‑ground compliance materially reduce operational disruption. Country risk pricing must be dynamic and data‑driven, integrating FX, sovereign spreads and real‑time political indicators.

- Capital controls: monitor policy shifts

- Hedging: volumes rise with volatility

- Risk: credit/settlement exposure increases

- Mitigation: local partners + compliance

- Pricing: dynamic, data-driven country risk

Commodity policy and strategic reserves

Government interventions in energy, agriculture and metals (eg. US Strategic Petroleum Reserve ~360m barrels end‑2024) shift term structures and liquidity, prompting client repositioning and hedging flows; releases or stockpiling create abrupt risk‑transfer needs that widen spreads and impact margins.

- Policy calendars → routing/margin models

- StoneX intelligence → client guidance on policy moves

- Reserves/releases drive short‑dated volatility

Political shocks drive FX and oil flow volatility, raising compliance and clearing costs

Political risks—conflict, sanctions and tariff shifts—drive FX/commodity flow volatility (FX ~7.5tn/day BIS 2022; oil ~100mbd) and raise compliance costs. Market development and clearing policies (70% OTC centrally cleared 2024) affect access and fees. Emerging-market turnover (MSCI EM ~11% 2024) creates capital‑control and pricing risk; dynamic, data‑driven country risk and local partners mitigate impact.

| Risk | Metric | Impact |

|---|---|---|

| Sanctions/conflict | FX 7.5tn/day; oil 100mbd | Flow rerouting, compliance |

| Clearing policy | 70% OTC cleared (2024) | Access/fee shifts |

| EM turnover | MSCI EM 11% (2024) | Capital controls, pricing |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact StoneX Group, combining data-driven trends and regulatory context to identify risks and opportunities; designed for executives and investors with forward-looking insights for strategy and scenario planning.

Condensed StoneX Group PESTLE that highlights key political, economic, regulatory, technological, environmental and social risks/opportunities for quick alignment in meetings, editable for region- or business-specific notes and easily dropped into presentations.

Economic factors

Monetary policy and interest rates

Rate cycles drive FX, fixed income and collateral costs, compressing spreads and client leverage; with policy rates at multi-decade highs (US fed funds ~5.25–5.50% in 2024, ECB ~3.75–4.00%), funding costs rose materially. Higher rates lift net interest income on client balances but pressure trading volumes. Volatility spikes expand execution revenue, making dynamic margining and collateral optimization key differentiators.

Global growth and trade volumes

Commodity demand, cross-border payments and hedging move with trade intensity: WTO projected world merchandise trade volume growth near 1.7% in 2024 while BIS reports cross-border payment flows exceeded 200 trillion dollars annually, highlighting scale and sensitivity. Slowdowns compress volumes but raise demand for risk management as volatility spikes. Cyclical rotations between energy, agriculture and metals shift client needs, and StoneX can counter-cyclically scale advisory and structured solutions to capture higher-margin hedging demand.

Liquidity and market microstructure

Dealer balance sheet constraints and market fragmentation have shifted execution quality, with roughly 45% of US equity volume executed off-exchange in 2024, increasing reliance on internalization. Access to multiple venues and liquidity pools improves client outcomes by expanding fill options. Smart order routing and internalization reduce realized slippage, while the balance between agency execution and risk warehousing materially influences StoneX margins.

Credit cycles and counterparty risk

Tighter credit since 2023–24 has raised default probabilities for corporates and financial institutions, reflected in repeated net tightening in the Fed Senior Loan Officer Opinion Survey through 2024.

Enhanced onboarding, higher collateral and stricter hedging limits have reduced loss severity; major CCPs increased margining and stress frameworks in 2024 per industry disclosures.

Ongoing stress-testing of clearing membership and transparent pricing sustain client stickiness during market stress.

- Fed SLOOS: net tightening persisted into 2024

- CCPs increased margining and stress tests in 2024

- Transparent pricing preserves client retention under stress

Commodity price cycles and volatility

Commodity price cycles in 2024–25 — notably energy and agriculture — amplified hedging flows, lifted margin requirements and increased working capital needs; realized volatility (OVX/VCI spikes) boosted execution revenues while elevating operational and margin-call risk, and shifting cross-commodity correlations forced updates to risk models and stress-testing.

- Energy/ag cycles drive hedging, margins, working capital

- Higher realized volatility increases execution revenue and operational risk

- Correlation shifts require adaptive risk models

- Market intel monetizes volatility into advisory revenue

Political shocks drive FX and oil flow volatility, raising compliance and clearing costs

Higher policy rates (US fed funds ~5.25–5.50% in 2024) raised funding costs and NII tradeoffs, while volatility spikes boosted execution and hedging demand. Global trade growth was muted (~1.7% WTO 2024) as cross-border flows exceeded $200T (BIS), keeping FX and payments demand elevated. Market fragmentation (≈45% US equity off‑exchange 2024) and tighter credit/CCP margining compressed spreads but increased demand for risk solutions.

| Metric | Value |

|---|---|

| US policy rate (2024) | 5.25–5.50% |

| World trade vol growth (2024) | ~1.7% |

| Cross‑border flows (annual) | >$200T |

| US off‑exchange equity (2024) | ≈45% |

What You See Is What You Get

StoneX Group PESTLE Analysis

The preview shown here is the exact StoneX Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes comprehensive political, economic, social, technological, legal and environmental assessments tailored to StoneX. No placeholders or teasers: the layout, charts and conclusions match the downloadable file. Purchase delivers this same final document instantly.

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political, economic, social, technological, legal and environmental forces are reshaping StoneX Group’s prospects in our concise PESTLE overview; this 3–5 sentence snapshot highlights key risks and opportunities—purchase the full analysis for a complete, actionable briefing ready for strategy or investment use.

Political factors

Geopolitical risk and sanctions

Volatility from conflicts and sanctions reshapes commodity and FX flows that StoneX intermediates, affecting markets with global FX turnover of about 7.5 trillion USD per day (BIS 2022) and oil flows near 100 million barrels/day. Rapid rule changes can restrict counterparties and instruments, altering revenue mix and raising compliance costs. Proactive sanctions screening and rerouting liquidity are critical operational controls. Diversified geography helps buffer localized shocks.

Trade policy and tariffs

Shifts in tariffs and export controls, such as US Section 301 measures covering about $370 billion of Chinese imports, materially alter hedging demand for commodities and currencies. Clients exposed to fragmented supply chains increasingly seek risk management, boosting clearing and execution volumes for brokers. Policy fragmentation raises basis risks across venues, widening cross-venue spreads. StoneX can monetize advisory and structured hedges to bridge these policy gaps.

Government support for financial infrastructure

National priorities on market development determine clearing access and licensing corridors, affecting StoneX's entry timelines and fee structures. Public investment in payment rails and CCPs expands addressable flow; BIS data show over 70% of standardized OTC derivatives were centrally cleared as of 2024. Active engagement in policy consultations influences microstructure rules, while alignment with development banks—which committed more than $100 billion annually to MDB programs in 2023–24—opens emerging market corridors.

Emerging market political stability

Political turnover in emerging markets can trigger capital controls, tax changes and restricted market access, forcing firms like StoneX to adapt pricing and liquidity; MSCI Emerging Markets represented about 11% of global equity markets in 2024, underscoring material exposure. Local volatility tends to increase hedging volumes but elevates credit and settlement risk; robust local partnerships and on‑the‑ground compliance materially reduce operational disruption. Country risk pricing must be dynamic and data‑driven, integrating FX, sovereign spreads and real‑time political indicators.

- Capital controls: monitor policy shifts

- Hedging: volumes rise with volatility

- Risk: credit/settlement exposure increases

- Mitigation: local partners + compliance

- Pricing: dynamic, data-driven country risk

Commodity policy and strategic reserves

Government interventions in energy, agriculture and metals (eg. US Strategic Petroleum Reserve ~360m barrels end‑2024) shift term structures and liquidity, prompting client repositioning and hedging flows; releases or stockpiling create abrupt risk‑transfer needs that widen spreads and impact margins.

- Policy calendars → routing/margin models

- StoneX intelligence → client guidance on policy moves

- Reserves/releases drive short‑dated volatility

Political shocks drive FX and oil flow volatility, raising compliance and clearing costs

Political risks—conflict, sanctions and tariff shifts—drive FX/commodity flow volatility (FX ~7.5tn/day BIS 2022; oil ~100mbd) and raise compliance costs. Market development and clearing policies (70% OTC centrally cleared 2024) affect access and fees. Emerging-market turnover (MSCI EM ~11% 2024) creates capital‑control and pricing risk; dynamic, data‑driven country risk and local partners mitigate impact.

| Risk | Metric | Impact |

|---|---|---|

| Sanctions/conflict | FX 7.5tn/day; oil 100mbd | Flow rerouting, compliance |

| Clearing policy | 70% OTC cleared (2024) | Access/fee shifts |

| EM turnover | MSCI EM 11% (2024) | Capital controls, pricing |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact StoneX Group, combining data-driven trends and regulatory context to identify risks and opportunities; designed for executives and investors with forward-looking insights for strategy and scenario planning.

Condensed StoneX Group PESTLE that highlights key political, economic, regulatory, technological, environmental and social risks/opportunities for quick alignment in meetings, editable for region- or business-specific notes and easily dropped into presentations.

Economic factors

Monetary policy and interest rates

Rate cycles drive FX, fixed income and collateral costs, compressing spreads and client leverage; with policy rates at multi-decade highs (US fed funds ~5.25–5.50% in 2024, ECB ~3.75–4.00%), funding costs rose materially. Higher rates lift net interest income on client balances but pressure trading volumes. Volatility spikes expand execution revenue, making dynamic margining and collateral optimization key differentiators.

Global growth and trade volumes

Commodity demand, cross-border payments and hedging move with trade intensity: WTO projected world merchandise trade volume growth near 1.7% in 2024 while BIS reports cross-border payment flows exceeded 200 trillion dollars annually, highlighting scale and sensitivity. Slowdowns compress volumes but raise demand for risk management as volatility spikes. Cyclical rotations between energy, agriculture and metals shift client needs, and StoneX can counter-cyclically scale advisory and structured solutions to capture higher-margin hedging demand.

Liquidity and market microstructure

Dealer balance sheet constraints and market fragmentation have shifted execution quality, with roughly 45% of US equity volume executed off-exchange in 2024, increasing reliance on internalization. Access to multiple venues and liquidity pools improves client outcomes by expanding fill options. Smart order routing and internalization reduce realized slippage, while the balance between agency execution and risk warehousing materially influences StoneX margins.

Credit cycles and counterparty risk

Tighter credit since 2023–24 has raised default probabilities for corporates and financial institutions, reflected in repeated net tightening in the Fed Senior Loan Officer Opinion Survey through 2024.

Enhanced onboarding, higher collateral and stricter hedging limits have reduced loss severity; major CCPs increased margining and stress frameworks in 2024 per industry disclosures.

Ongoing stress-testing of clearing membership and transparent pricing sustain client stickiness during market stress.

- Fed SLOOS: net tightening persisted into 2024

- CCPs increased margining and stress tests in 2024

- Transparent pricing preserves client retention under stress

Commodity price cycles and volatility

Commodity price cycles in 2024–25 — notably energy and agriculture — amplified hedging flows, lifted margin requirements and increased working capital needs; realized volatility (OVX/VCI spikes) boosted execution revenues while elevating operational and margin-call risk, and shifting cross-commodity correlations forced updates to risk models and stress-testing.

- Energy/ag cycles drive hedging, margins, working capital

- Higher realized volatility increases execution revenue and operational risk

- Correlation shifts require adaptive risk models

- Market intel monetizes volatility into advisory revenue

Political shocks drive FX and oil flow volatility, raising compliance and clearing costs

Higher policy rates (US fed funds ~5.25–5.50% in 2024) raised funding costs and NII tradeoffs, while volatility spikes boosted execution and hedging demand. Global trade growth was muted (~1.7% WTO 2024) as cross-border flows exceeded $200T (BIS), keeping FX and payments demand elevated. Market fragmentation (≈45% US equity off‑exchange 2024) and tighter credit/CCP margining compressed spreads but increased demand for risk solutions.

| Metric | Value |

|---|---|

| US policy rate (2024) | 5.25–5.50% |

| World trade vol growth (2024) | ~1.7% |

| Cross‑border flows (annual) | >$200T |

| US off‑exchange equity (2024) | ≈45% |

What You See Is What You Get

StoneX Group PESTLE Analysis

The preview shown here is the exact StoneX Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes comprehensive political, economic, social, technological, legal and environmental assessments tailored to StoneX. No placeholders or teasers: the layout, charts and conclusions match the downloadable file. Purchase delivers this same final document instantly.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Uncover how political, economic, social, technological, legal and environmental forces are reshaping StoneX Group’s prospects in our concise PESTLE overview; this 3–5 sentence snapshot highlights key risks and opportunities—purchase the full analysis for a complete, actionable briefing ready for strategy or investment use.

Political factors

Geopolitical risk and sanctions

Volatility from conflicts and sanctions reshapes commodity and FX flows that StoneX intermediates, affecting markets with global FX turnover of about 7.5 trillion USD per day (BIS 2022) and oil flows near 100 million barrels/day. Rapid rule changes can restrict counterparties and instruments, altering revenue mix and raising compliance costs. Proactive sanctions screening and rerouting liquidity are critical operational controls. Diversified geography helps buffer localized shocks.

Trade policy and tariffs

Shifts in tariffs and export controls, such as US Section 301 measures covering about $370 billion of Chinese imports, materially alter hedging demand for commodities and currencies. Clients exposed to fragmented supply chains increasingly seek risk management, boosting clearing and execution volumes for brokers. Policy fragmentation raises basis risks across venues, widening cross-venue spreads. StoneX can monetize advisory and structured hedges to bridge these policy gaps.

Government support for financial infrastructure

National priorities on market development determine clearing access and licensing corridors, affecting StoneX's entry timelines and fee structures. Public investment in payment rails and CCPs expands addressable flow; BIS data show over 70% of standardized OTC derivatives were centrally cleared as of 2024. Active engagement in policy consultations influences microstructure rules, while alignment with development banks—which committed more than $100 billion annually to MDB programs in 2023–24—opens emerging market corridors.

Emerging market political stability

Political turnover in emerging markets can trigger capital controls, tax changes and restricted market access, forcing firms like StoneX to adapt pricing and liquidity; MSCI Emerging Markets represented about 11% of global equity markets in 2024, underscoring material exposure. Local volatility tends to increase hedging volumes but elevates credit and settlement risk; robust local partnerships and on‑the‑ground compliance materially reduce operational disruption. Country risk pricing must be dynamic and data‑driven, integrating FX, sovereign spreads and real‑time political indicators.

- Capital controls: monitor policy shifts

- Hedging: volumes rise with volatility

- Risk: credit/settlement exposure increases

- Mitigation: local partners + compliance

- Pricing: dynamic, data-driven country risk

Commodity policy and strategic reserves

Government interventions in energy, agriculture and metals (eg. US Strategic Petroleum Reserve ~360m barrels end‑2024) shift term structures and liquidity, prompting client repositioning and hedging flows; releases or stockpiling create abrupt risk‑transfer needs that widen spreads and impact margins.

- Policy calendars → routing/margin models

- StoneX intelligence → client guidance on policy moves

- Reserves/releases drive short‑dated volatility

Political shocks drive FX and oil flow volatility, raising compliance and clearing costs

Political risks—conflict, sanctions and tariff shifts—drive FX/commodity flow volatility (FX ~7.5tn/day BIS 2022; oil ~100mbd) and raise compliance costs. Market development and clearing policies (70% OTC centrally cleared 2024) affect access and fees. Emerging-market turnover (MSCI EM ~11% 2024) creates capital‑control and pricing risk; dynamic, data‑driven country risk and local partners mitigate impact.

| Risk | Metric | Impact |

|---|---|---|

| Sanctions/conflict | FX 7.5tn/day; oil 100mbd | Flow rerouting, compliance |

| Clearing policy | 70% OTC cleared (2024) | Access/fee shifts |

| EM turnover | MSCI EM 11% (2024) | Capital controls, pricing |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact StoneX Group, combining data-driven trends and regulatory context to identify risks and opportunities; designed for executives and investors with forward-looking insights for strategy and scenario planning.

Condensed StoneX Group PESTLE that highlights key political, economic, regulatory, technological, environmental and social risks/opportunities for quick alignment in meetings, editable for region- or business-specific notes and easily dropped into presentations.

Economic factors

Monetary policy and interest rates

Rate cycles drive FX, fixed income and collateral costs, compressing spreads and client leverage; with policy rates at multi-decade highs (US fed funds ~5.25–5.50% in 2024, ECB ~3.75–4.00%), funding costs rose materially. Higher rates lift net interest income on client balances but pressure trading volumes. Volatility spikes expand execution revenue, making dynamic margining and collateral optimization key differentiators.

Global growth and trade volumes

Commodity demand, cross-border payments and hedging move with trade intensity: WTO projected world merchandise trade volume growth near 1.7% in 2024 while BIS reports cross-border payment flows exceeded 200 trillion dollars annually, highlighting scale and sensitivity. Slowdowns compress volumes but raise demand for risk management as volatility spikes. Cyclical rotations between energy, agriculture and metals shift client needs, and StoneX can counter-cyclically scale advisory and structured solutions to capture higher-margin hedging demand.

Liquidity and market microstructure

Dealer balance sheet constraints and market fragmentation have shifted execution quality, with roughly 45% of US equity volume executed off-exchange in 2024, increasing reliance on internalization. Access to multiple venues and liquidity pools improves client outcomes by expanding fill options. Smart order routing and internalization reduce realized slippage, while the balance between agency execution and risk warehousing materially influences StoneX margins.

Credit cycles and counterparty risk

Tighter credit since 2023–24 has raised default probabilities for corporates and financial institutions, reflected in repeated net tightening in the Fed Senior Loan Officer Opinion Survey through 2024.

Enhanced onboarding, higher collateral and stricter hedging limits have reduced loss severity; major CCPs increased margining and stress frameworks in 2024 per industry disclosures.

Ongoing stress-testing of clearing membership and transparent pricing sustain client stickiness during market stress.

- Fed SLOOS: net tightening persisted into 2024

- CCPs increased margining and stress tests in 2024

- Transparent pricing preserves client retention under stress

Commodity price cycles and volatility

Commodity price cycles in 2024–25 — notably energy and agriculture — amplified hedging flows, lifted margin requirements and increased working capital needs; realized volatility (OVX/VCI spikes) boosted execution revenues while elevating operational and margin-call risk, and shifting cross-commodity correlations forced updates to risk models and stress-testing.

- Energy/ag cycles drive hedging, margins, working capital

- Higher realized volatility increases execution revenue and operational risk

- Correlation shifts require adaptive risk models

- Market intel monetizes volatility into advisory revenue

Political shocks drive FX and oil flow volatility, raising compliance and clearing costs

Higher policy rates (US fed funds ~5.25–5.50% in 2024) raised funding costs and NII tradeoffs, while volatility spikes boosted execution and hedging demand. Global trade growth was muted (~1.7% WTO 2024) as cross-border flows exceeded $200T (BIS), keeping FX and payments demand elevated. Market fragmentation (≈45% US equity off‑exchange 2024) and tighter credit/CCP margining compressed spreads but increased demand for risk solutions.

| Metric | Value |

|---|---|

| US policy rate (2024) | 5.25–5.50% |

| World trade vol growth (2024) | ~1.7% |

| Cross‑border flows (annual) | >$200T |

| US off‑exchange equity (2024) | ≈45% |

What You See Is What You Get

StoneX Group PESTLE Analysis

The preview shown here is the exact StoneX Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It includes comprehensive political, economic, social, technological, legal and environmental assessments tailored to StoneX. No placeholders or teasers: the layout, charts and conclusions match the downloadable file. Purchase delivers this same final document instantly.