STRABAG Porter's Five Forces Analysis

Don't Miss the Bigger Picture

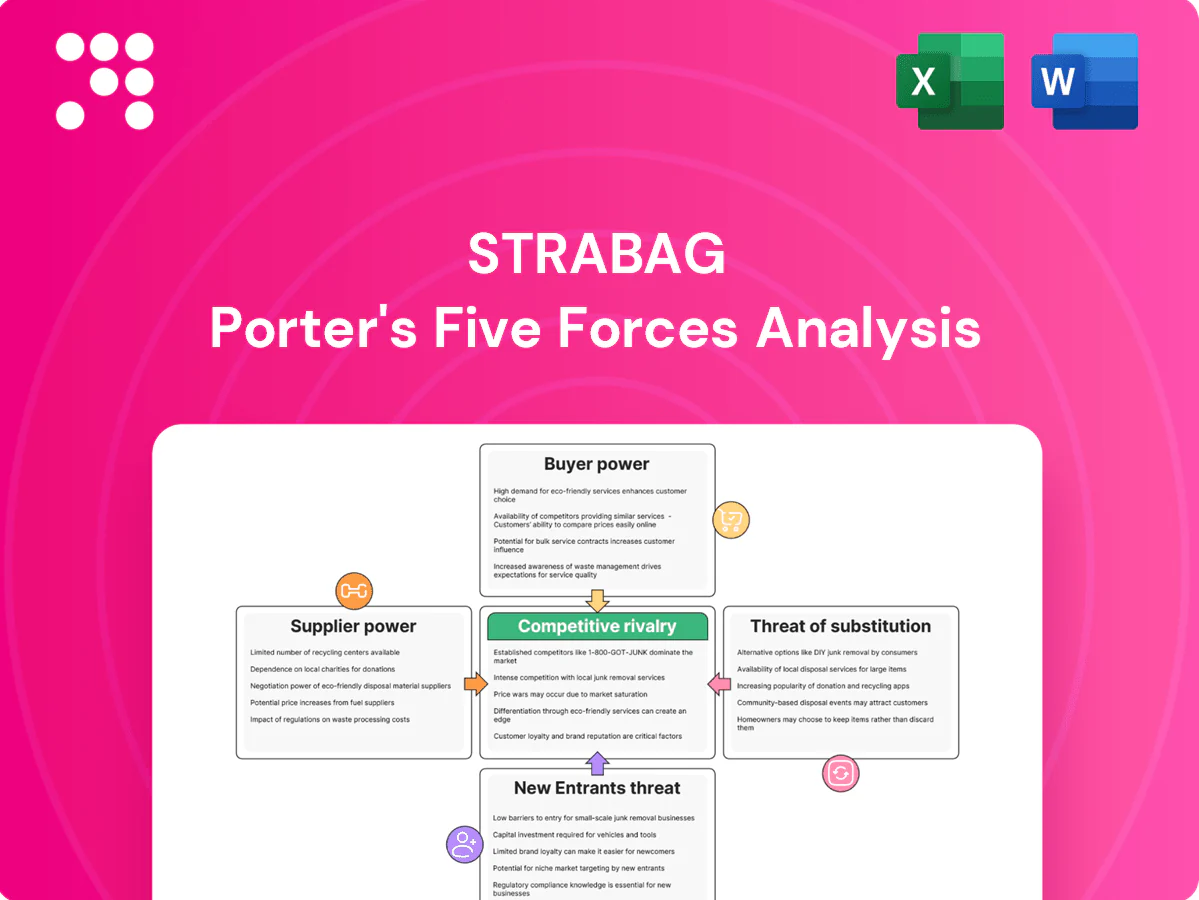

STRABAG faces intense project-based competition, moderate supplier leverage for specialized inputs, growing buyer bargaining from large clients, and steady threat from substitutes like modular construction, while regulatory and capital barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore STRABAG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical materials volatility

In 2024 STRABAG remains heavily dependent on cement, steel, bitumen and aggregates, markets that have shown cyclical and geopolitical price swings; commodity suppliers can pass through cost increases rapidly, squeezing margins on fixed-price contracts. Long-term framework agreements and hedging programs partially mitigate exposure, while careful project timing and indexation clauses are crucial tools to rebalance supplier leverage.

Equipment OEM concentration

Heavy machinery and specialized tunneling/foundation equipment come from a concentrated set of OEMs (e.g., Herrenknecht, Bauer, Liebherr), giving suppliers pricing and uptime leverage through parts and service contracts. STRABAG mitigates this with a large owned fleet and in-house maintenance capabilities that lower dependence on OEM service windows. Active multi-sourcing and equipment standardization further strengthen STRABAG’s negotiating position.

Specialist subcontractors

Geotechnical, MEP and façade specialists can become critical bottlenecks on complex projects, raising mid-project switching costs and delaying schedules. STRABAG’s integrated capabilities and preferred-partner networks mitigate this supplier power, supported by a 2024 order backlog of about €22bn which strengthens procurement leverage. Early contractor involvement broadens the specialist pool and locks pricing, reducing variation risk and exposure to niche premium rates.

Skilled labor scarcity

Regional shortages in skilled trades and engineers drive wage inflation and raise supplier bargaining power, with STRABAG facing competition for talent amid a workforce of about 75,000 (2023) and rising industry wage costs in 2023–24.

Unions and cross-border mobility rules in the EU affect availability and rates, while STRABAG’s training pipelines and employer brand partially mitigate exposure.

Adoption of automation, BIM and lean methods boosts productivity, lowering per-unit labor dependency and negotiating leverage of scarce trades.

- Skilled labor scarcity: raises wage pressure

- Unions/mobility: constrain supply and increase rates

- STRABAG training/employer brand: reduces vulnerability

- Automation/BIM/lean: improves productivity, lowers supplier power

Logistics and permitting

Logistics and permitting drive supplier leverage for STRABAG: quarry access limits and haulage constraints can add 3–12 months to schedules and raise onsite cost per tonne-km, while complex site logistics amplify variability in margins.

Local regulators and utilities act as quasi-suppliers with timing power—2024 project reports show permitting delays remain a top-three schedule risk.

Early stakeholder engagement, permitting expertise, staging, just-in-time deliveries and digital planning (BIM/supply-chain tools) materially cut disruption and buffer costs.

- Quarry access: material flow bottlenecks

- Haulage constraints: cost/time volatility

- Regulators/utilities: critical timing power

- Mitigations: stakeholder mgmt, JIT, digital planning

Margins vulnerable to commodity swings; €22bn backlog strengthens procurement leverage

STRABAG remains dependent on cement, steel, bitumen and aggregates, exposing margins to commodity swings; 2024 order backlog ~€22bn gives procurement leverage. OEM concentration (Herrenknecht, Bauer, Liebherr) raises equipment service risk, mitigated by a large owned fleet and in‑house maintenance. Skilled labor scarcity (workforce ~75,000 in 2023) and permitting delays are material schedule/cost risks.

| Supplier category | 2024 impact | STRABAG metric |

|---|---|---|

| Commodities | Price volatility | Order backlog €22bn |

| OEMs | Service/parts leverage | Owned fleet/in-house maintenance |

| Labor | Wage pressure | Workforce ~75,000 (2023) |

| Permitting/logistics | Schedule risk | Top‑3 project risk 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for STRABAG that uncovers competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic insights to inform investor presentations and internal strategy.

Clear one-sheet Porter's Five Forces for STRABAG—instantly visualise competitive pressure with a customizable spider chart, tweak force levels for market shifts, and drop the clean layout straight into pitch decks or boardroom slides.

Customers Bargaining Power

Public tender dominance

Governments and municipalities procure via competitive tenders with strict specs and transparency, a market that in the EU represents about €2 trillion annually (≈15% of GDP), making bids highly comparable and increasing buyer leverage on price and contract terms. STRABAG (group revenue ~€19bn in 2024) must differentiate through demonstrable lifecycle value, reliability and lower total cost of ownership to protect margins. Prequalification status and past performance are critical determinants of win rates in this environment.

Large private developers

Institutional developers and infrastructure funds bundle projects often exceeding €100m to secure volume discounts, demanding turnkey delivery, compressed schedules and transfer of construction risk. STRABAG’s end-to-end offering and PPP track record allow it to command time-and-risk premiums versus pure contractors. Focused key-account management in 2024 reduced churn and mitigated price pressure on major clients.

Price-driven procurement

Many buyers prioritize the lowest bid over best value, intensifying margin pressure and increasing change-order risk; STRABAG, active in over 60 countries, faces compressed bid margins in such tenders. Using design-build and systematic value engineering reframes choices toward life-cycle cost. Tying contracts to performance guarantees and clear KPIs shifts procurement focus from price to outcomes.

Performance-based contracts

Performance-based contracts shift downside to contractors through outcome-linked payments and penalties, giving buyers greater leverage via service-level enforcement over long concessions; in 2024 STRABAG reported expanding O&M portfolios that provide richer asset performance datasets. Robust risk pricing and contingency planning are essential as penalties and availability clauses materially affect margins, and STRABAG’s facility management data improve predictability of lifecycle costs.

- Outcome-linked payments/penalties shift risk to contractors

- Long concessions increase buyer enforcement power

- STRABAG 2024 O&M data boosts predictability; robust risk pricing required

One-stop solutions leverage

Clients increasingly favor integrated planning-to-O&M partners to cut interface risk, and STRABAG’s bundled offerings raise switching costs and help capture share; STRABAG reported group revenue ~€20bn in 2024 and an order backlog north of €20bn, underscoring scale advantages. Reference projects such as Vienna Hauptbahnhof and growing use of digital twins strengthen trust and reduce buyer power where breadth matters.

- Reduced buyer power via end-to-end contracts

- Higher switching costs from bundled services

- Digital twins + flagship projects boost credibility

Buyers wield leverage in €2tn EU tenders; contractors must sell lifecycle value

Buyers wield strong leverage via transparent EU tenders (~€2tn pa) and low‑price bias, compressing margins; STRABAG (group revenue €19bn in 2024) must sell lifecycle value and reliability. Turnkey/integrated offers and O&M scale (order backlog €20bn+) raise switching costs and reduce buyer power. Outcome‑linked contracts transfer risk to contractors, requiring disciplined risk pricing.

| Metric | Value (2024) |

|---|---|

| Group revenue | €19bn |

| Order backlog | €20bn+ |

| EU public procurement | ≈€2tn pa |

Preview the Actual Deliverable

STRABAG Porter's Five Forces Analysis

This preview shows the exact STRABAG Porter’s Five Forces Analysis you'll receive after purchase—fully formatted and ready to use. It contains the complete competitive assessment, forces' ratings, supporting evidence and strategic implications. No placeholders or samples; instant access and download upon payment.

Don't Miss the Bigger Picture

STRABAG faces intense project-based competition, moderate supplier leverage for specialized inputs, growing buyer bargaining from large clients, and steady threat from substitutes like modular construction, while regulatory and capital barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore STRABAG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical materials volatility

In 2024 STRABAG remains heavily dependent on cement, steel, bitumen and aggregates, markets that have shown cyclical and geopolitical price swings; commodity suppliers can pass through cost increases rapidly, squeezing margins on fixed-price contracts. Long-term framework agreements and hedging programs partially mitigate exposure, while careful project timing and indexation clauses are crucial tools to rebalance supplier leverage.

Equipment OEM concentration

Heavy machinery and specialized tunneling/foundation equipment come from a concentrated set of OEMs (e.g., Herrenknecht, Bauer, Liebherr), giving suppliers pricing and uptime leverage through parts and service contracts. STRABAG mitigates this with a large owned fleet and in-house maintenance capabilities that lower dependence on OEM service windows. Active multi-sourcing and equipment standardization further strengthen STRABAG’s negotiating position.

Specialist subcontractors

Geotechnical, MEP and façade specialists can become critical bottlenecks on complex projects, raising mid-project switching costs and delaying schedules. STRABAG’s integrated capabilities and preferred-partner networks mitigate this supplier power, supported by a 2024 order backlog of about €22bn which strengthens procurement leverage. Early contractor involvement broadens the specialist pool and locks pricing, reducing variation risk and exposure to niche premium rates.

Skilled labor scarcity

Regional shortages in skilled trades and engineers drive wage inflation and raise supplier bargaining power, with STRABAG facing competition for talent amid a workforce of about 75,000 (2023) and rising industry wage costs in 2023–24.

Unions and cross-border mobility rules in the EU affect availability and rates, while STRABAG’s training pipelines and employer brand partially mitigate exposure.

Adoption of automation, BIM and lean methods boosts productivity, lowering per-unit labor dependency and negotiating leverage of scarce trades.

- Skilled labor scarcity: raises wage pressure

- Unions/mobility: constrain supply and increase rates

- STRABAG training/employer brand: reduces vulnerability

- Automation/BIM/lean: improves productivity, lowers supplier power

Logistics and permitting

Logistics and permitting drive supplier leverage for STRABAG: quarry access limits and haulage constraints can add 3–12 months to schedules and raise onsite cost per tonne-km, while complex site logistics amplify variability in margins.

Local regulators and utilities act as quasi-suppliers with timing power—2024 project reports show permitting delays remain a top-three schedule risk.

Early stakeholder engagement, permitting expertise, staging, just-in-time deliveries and digital planning (BIM/supply-chain tools) materially cut disruption and buffer costs.

- Quarry access: material flow bottlenecks

- Haulage constraints: cost/time volatility

- Regulators/utilities: critical timing power

- Mitigations: stakeholder mgmt, JIT, digital planning

Margins vulnerable to commodity swings; €22bn backlog strengthens procurement leverage

STRABAG remains dependent on cement, steel, bitumen and aggregates, exposing margins to commodity swings; 2024 order backlog ~€22bn gives procurement leverage. OEM concentration (Herrenknecht, Bauer, Liebherr) raises equipment service risk, mitigated by a large owned fleet and in‑house maintenance. Skilled labor scarcity (workforce ~75,000 in 2023) and permitting delays are material schedule/cost risks.

| Supplier category | 2024 impact | STRABAG metric |

|---|---|---|

| Commodities | Price volatility | Order backlog €22bn |

| OEMs | Service/parts leverage | Owned fleet/in-house maintenance |

| Labor | Wage pressure | Workforce ~75,000 (2023) |

| Permitting/logistics | Schedule risk | Top‑3 project risk 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for STRABAG that uncovers competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic insights to inform investor presentations and internal strategy.

Clear one-sheet Porter's Five Forces for STRABAG—instantly visualise competitive pressure with a customizable spider chart, tweak force levels for market shifts, and drop the clean layout straight into pitch decks or boardroom slides.

Customers Bargaining Power

Public tender dominance

Governments and municipalities procure via competitive tenders with strict specs and transparency, a market that in the EU represents about €2 trillion annually (≈15% of GDP), making bids highly comparable and increasing buyer leverage on price and contract terms. STRABAG (group revenue ~€19bn in 2024) must differentiate through demonstrable lifecycle value, reliability and lower total cost of ownership to protect margins. Prequalification status and past performance are critical determinants of win rates in this environment.

Large private developers

Institutional developers and infrastructure funds bundle projects often exceeding €100m to secure volume discounts, demanding turnkey delivery, compressed schedules and transfer of construction risk. STRABAG’s end-to-end offering and PPP track record allow it to command time-and-risk premiums versus pure contractors. Focused key-account management in 2024 reduced churn and mitigated price pressure on major clients.

Price-driven procurement

Many buyers prioritize the lowest bid over best value, intensifying margin pressure and increasing change-order risk; STRABAG, active in over 60 countries, faces compressed bid margins in such tenders. Using design-build and systematic value engineering reframes choices toward life-cycle cost. Tying contracts to performance guarantees and clear KPIs shifts procurement focus from price to outcomes.

Performance-based contracts

Performance-based contracts shift downside to contractors through outcome-linked payments and penalties, giving buyers greater leverage via service-level enforcement over long concessions; in 2024 STRABAG reported expanding O&M portfolios that provide richer asset performance datasets. Robust risk pricing and contingency planning are essential as penalties and availability clauses materially affect margins, and STRABAG’s facility management data improve predictability of lifecycle costs.

- Outcome-linked payments/penalties shift risk to contractors

- Long concessions increase buyer enforcement power

- STRABAG 2024 O&M data boosts predictability; robust risk pricing required

One-stop solutions leverage

Clients increasingly favor integrated planning-to-O&M partners to cut interface risk, and STRABAG’s bundled offerings raise switching costs and help capture share; STRABAG reported group revenue ~€20bn in 2024 and an order backlog north of €20bn, underscoring scale advantages. Reference projects such as Vienna Hauptbahnhof and growing use of digital twins strengthen trust and reduce buyer power where breadth matters.

- Reduced buyer power via end-to-end contracts

- Higher switching costs from bundled services

- Digital twins + flagship projects boost credibility

Buyers wield leverage in €2tn EU tenders; contractors must sell lifecycle value

Buyers wield strong leverage via transparent EU tenders (~€2tn pa) and low‑price bias, compressing margins; STRABAG (group revenue €19bn in 2024) must sell lifecycle value and reliability. Turnkey/integrated offers and O&M scale (order backlog €20bn+) raise switching costs and reduce buyer power. Outcome‑linked contracts transfer risk to contractors, requiring disciplined risk pricing.

| Metric | Value (2024) |

|---|---|

| Group revenue | €19bn |

| Order backlog | €20bn+ |

| EU public procurement | ≈€2tn pa |

Preview the Actual Deliverable

STRABAG Porter's Five Forces Analysis

This preview shows the exact STRABAG Porter’s Five Forces Analysis you'll receive after purchase—fully formatted and ready to use. It contains the complete competitive assessment, forces' ratings, supporting evidence and strategic implications. No placeholders or samples; instant access and download upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

STRABAG faces intense project-based competition, moderate supplier leverage for specialized inputs, growing buyer bargaining from large clients, and steady threat from substitutes like modular construction, while regulatory and capital barriers limit new entrants. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore STRABAG’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Critical materials volatility

In 2024 STRABAG remains heavily dependent on cement, steel, bitumen and aggregates, markets that have shown cyclical and geopolitical price swings; commodity suppliers can pass through cost increases rapidly, squeezing margins on fixed-price contracts. Long-term framework agreements and hedging programs partially mitigate exposure, while careful project timing and indexation clauses are crucial tools to rebalance supplier leverage.

Equipment OEM concentration

Heavy machinery and specialized tunneling/foundation equipment come from a concentrated set of OEMs (e.g., Herrenknecht, Bauer, Liebherr), giving suppliers pricing and uptime leverage through parts and service contracts. STRABAG mitigates this with a large owned fleet and in-house maintenance capabilities that lower dependence on OEM service windows. Active multi-sourcing and equipment standardization further strengthen STRABAG’s negotiating position.

Specialist subcontractors

Geotechnical, MEP and façade specialists can become critical bottlenecks on complex projects, raising mid-project switching costs and delaying schedules. STRABAG’s integrated capabilities and preferred-partner networks mitigate this supplier power, supported by a 2024 order backlog of about €22bn which strengthens procurement leverage. Early contractor involvement broadens the specialist pool and locks pricing, reducing variation risk and exposure to niche premium rates.

Skilled labor scarcity

Regional shortages in skilled trades and engineers drive wage inflation and raise supplier bargaining power, with STRABAG facing competition for talent amid a workforce of about 75,000 (2023) and rising industry wage costs in 2023–24.

Unions and cross-border mobility rules in the EU affect availability and rates, while STRABAG’s training pipelines and employer brand partially mitigate exposure.

Adoption of automation, BIM and lean methods boosts productivity, lowering per-unit labor dependency and negotiating leverage of scarce trades.

- Skilled labor scarcity: raises wage pressure

- Unions/mobility: constrain supply and increase rates

- STRABAG training/employer brand: reduces vulnerability

- Automation/BIM/lean: improves productivity, lowers supplier power

Logistics and permitting

Logistics and permitting drive supplier leverage for STRABAG: quarry access limits and haulage constraints can add 3–12 months to schedules and raise onsite cost per tonne-km, while complex site logistics amplify variability in margins.

Local regulators and utilities act as quasi-suppliers with timing power—2024 project reports show permitting delays remain a top-three schedule risk.

Early stakeholder engagement, permitting expertise, staging, just-in-time deliveries and digital planning (BIM/supply-chain tools) materially cut disruption and buffer costs.

- Quarry access: material flow bottlenecks

- Haulage constraints: cost/time volatility

- Regulators/utilities: critical timing power

- Mitigations: stakeholder mgmt, JIT, digital planning

Margins vulnerable to commodity swings; €22bn backlog strengthens procurement leverage

STRABAG remains dependent on cement, steel, bitumen and aggregates, exposing margins to commodity swings; 2024 order backlog ~€22bn gives procurement leverage. OEM concentration (Herrenknecht, Bauer, Liebherr) raises equipment service risk, mitigated by a large owned fleet and in‑house maintenance. Skilled labor scarcity (workforce ~75,000 in 2023) and permitting delays are material schedule/cost risks.

| Supplier category | 2024 impact | STRABAG metric |

|---|---|---|

| Commodities | Price volatility | Order backlog €22bn |

| OEMs | Service/parts leverage | Owned fleet/in-house maintenance |

| Labor | Wage pressure | Workforce ~75,000 (2023) |

| Permitting/logistics | Schedule risk | Top‑3 project risk 2024 |

What is included in the product

Tailored Porter's Five Forces analysis for STRABAG that uncovers competitive rivalry, supplier and buyer power, entry barriers, substitutes and disruptive threats, with strategic insights to inform investor presentations and internal strategy.

Clear one-sheet Porter's Five Forces for STRABAG—instantly visualise competitive pressure with a customizable spider chart, tweak force levels for market shifts, and drop the clean layout straight into pitch decks or boardroom slides.

Customers Bargaining Power

Public tender dominance

Governments and municipalities procure via competitive tenders with strict specs and transparency, a market that in the EU represents about €2 trillion annually (≈15% of GDP), making bids highly comparable and increasing buyer leverage on price and contract terms. STRABAG (group revenue ~€19bn in 2024) must differentiate through demonstrable lifecycle value, reliability and lower total cost of ownership to protect margins. Prequalification status and past performance are critical determinants of win rates in this environment.

Large private developers

Institutional developers and infrastructure funds bundle projects often exceeding €100m to secure volume discounts, demanding turnkey delivery, compressed schedules and transfer of construction risk. STRABAG’s end-to-end offering and PPP track record allow it to command time-and-risk premiums versus pure contractors. Focused key-account management in 2024 reduced churn and mitigated price pressure on major clients.

Price-driven procurement

Many buyers prioritize the lowest bid over best value, intensifying margin pressure and increasing change-order risk; STRABAG, active in over 60 countries, faces compressed bid margins in such tenders. Using design-build and systematic value engineering reframes choices toward life-cycle cost. Tying contracts to performance guarantees and clear KPIs shifts procurement focus from price to outcomes.

Performance-based contracts

Performance-based contracts shift downside to contractors through outcome-linked payments and penalties, giving buyers greater leverage via service-level enforcement over long concessions; in 2024 STRABAG reported expanding O&M portfolios that provide richer asset performance datasets. Robust risk pricing and contingency planning are essential as penalties and availability clauses materially affect margins, and STRABAG’s facility management data improve predictability of lifecycle costs.

- Outcome-linked payments/penalties shift risk to contractors

- Long concessions increase buyer enforcement power

- STRABAG 2024 O&M data boosts predictability; robust risk pricing required

One-stop solutions leverage

Clients increasingly favor integrated planning-to-O&M partners to cut interface risk, and STRABAG’s bundled offerings raise switching costs and help capture share; STRABAG reported group revenue ~€20bn in 2024 and an order backlog north of €20bn, underscoring scale advantages. Reference projects such as Vienna Hauptbahnhof and growing use of digital twins strengthen trust and reduce buyer power where breadth matters.

- Reduced buyer power via end-to-end contracts

- Higher switching costs from bundled services

- Digital twins + flagship projects boost credibility

Buyers wield leverage in €2tn EU tenders; contractors must sell lifecycle value

Buyers wield strong leverage via transparent EU tenders (~€2tn pa) and low‑price bias, compressing margins; STRABAG (group revenue €19bn in 2024) must sell lifecycle value and reliability. Turnkey/integrated offers and O&M scale (order backlog €20bn+) raise switching costs and reduce buyer power. Outcome‑linked contracts transfer risk to contractors, requiring disciplined risk pricing.

| Metric | Value (2024) |

|---|---|

| Group revenue | €19bn |

| Order backlog | €20bn+ |

| EU public procurement | ≈€2tn pa |

Preview the Actual Deliverable

STRABAG Porter's Five Forces Analysis

This preview shows the exact STRABAG Porter’s Five Forces Analysis you'll receive after purchase—fully formatted and ready to use. It contains the complete competitive assessment, forces' ratings, supporting evidence and strategic implications. No placeholders or samples; instant access and download upon payment.